Health plan CIOs and operational leaders must recognize a new risk emerging from the consolidation of the core admin processing systems (CAPS) market. This consolidation will result in health plans losing access to some of their CAPS and, consequently, their ability to address members and providers. Yes, that will put the business at risk.

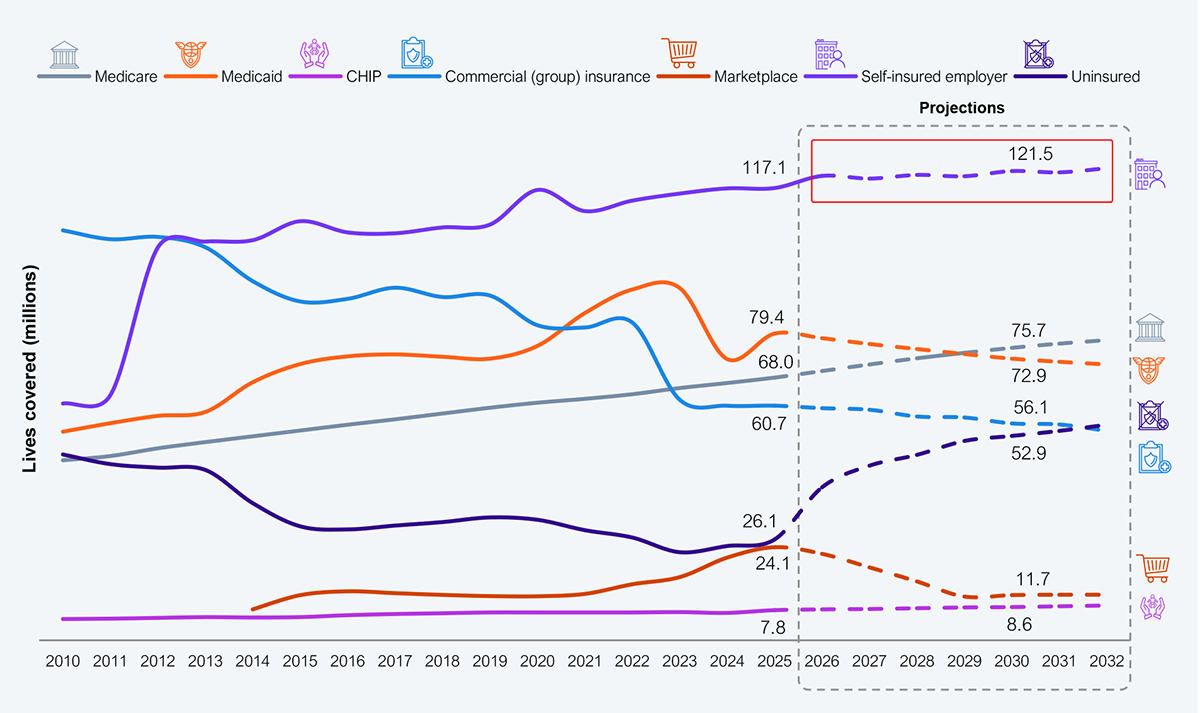

The consolidation cycle is being driven by reduced demand (increased uninsured rates) due to HR1 (the One Big Beautiful Bill Act, or OBBBA), the expiration of the Affordable Care Act (ACA) subsidies, and the escalating cost of healthcare, which are pressuring revenues and eroding margins (see Exhibit 1). As health plan memberships decline, so will their administration and technology needs, particularly their CAPS.

HFS Research published a playbook for health plan CIOs to help with the transition. A direct impact of the market changes and health plans’ pivot to survival will rapidly shrink the market for CAPS, driving consolidation among vendors; however, some CAPS providers may have the opportunity to reinvent themselves if they embrace Services-as-Software.

Source: CMS, CBO, KFF, US Bureau of Labor Statistics, HFS Research, 2026

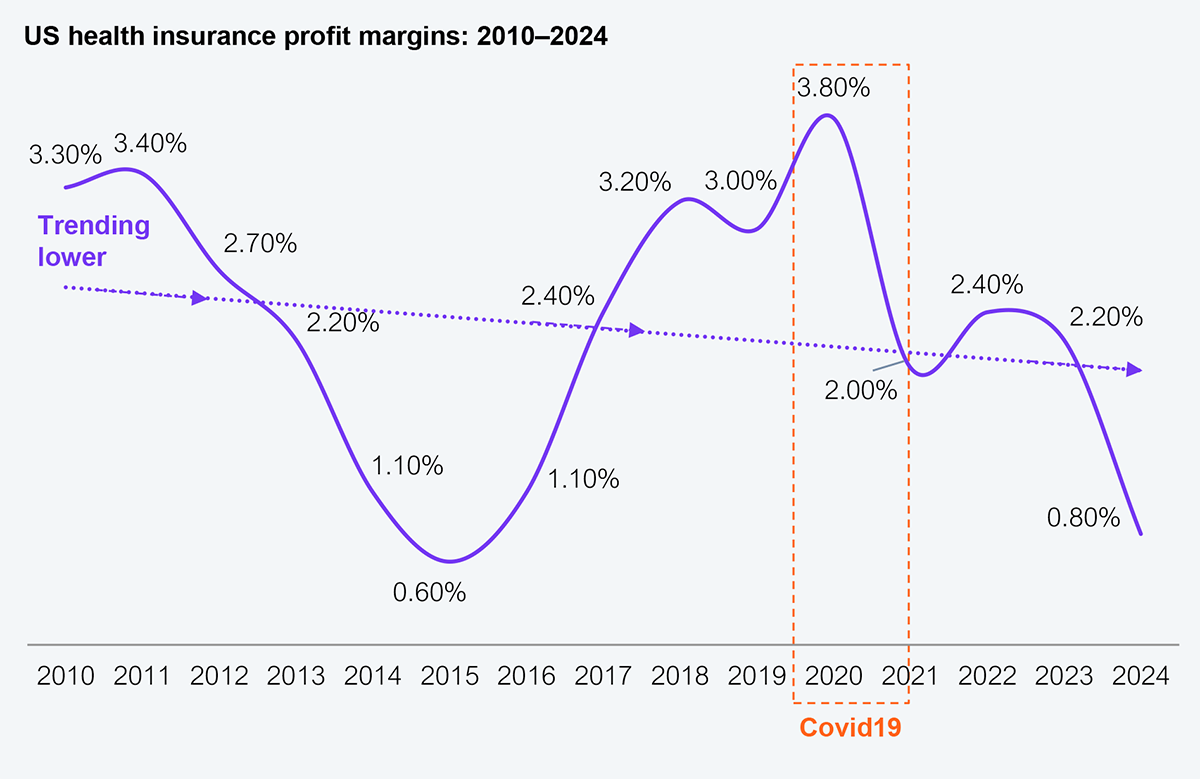

The prognosis for health plans’ revenues and margins is dire (see Exhibit 2), rendering any technology spend beyond keeping lights on untenable. Nearly three-fourths (72%) of all US lives are underwritten by either the government (via Medicare, Medicaid, or CHIP) or self-insured employers, not health insurers. The profitable commercial underwriting service line continues to decline to below 30%, while other value propositions like provider networks have become commodities that can be rented.

Source: NAIC (1,000+ health plans reporting), HFS Research, 2026

As populations age, the prevalence of comorbidities rises, clinical shortages grow, and medical costs increase. There is no path, even with the promise of AI, for margins to improve in this traditional coverage market.

Given these headwinds, health plan CFOs will eschew spending or investing in CAPS or tech modernization efforts and make the bare minimum outlays to keep the lights on. This will drive a negative pressure on CAPS vendors, leading to consolidation, which began with the sale of HealthEdge and UST Health Proof in 2025.

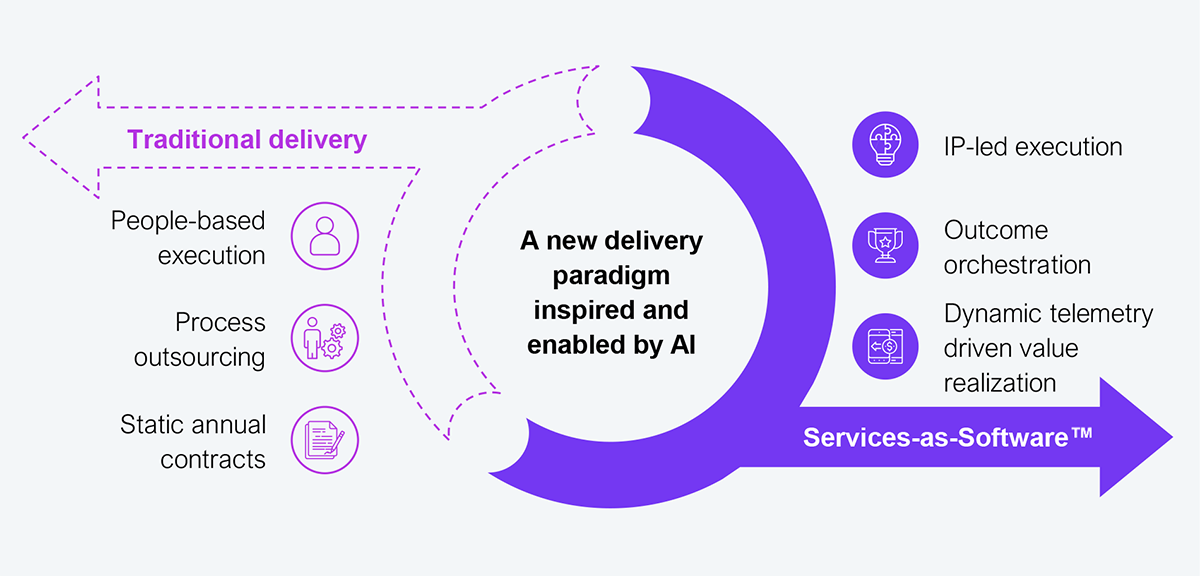

Services-as-Software™ (SaS) will be the preeminent 21st-century AI-enabled delivery model (see Exhibit 3) that will be central for health plans to effectively and consistently maximize the potential of AI. SaS is how the transition from predominantly people-led to IP-led delivery will take place. SaS is about delivering outcomes that matter through ecosystem orchestration rather than features and functionality. SaS is about continuously realizing value, reflected in real-time telemetry rather than static annual contracts. This is a paradigm increasingly adopted across the technology landscape, as regulations and compliance are built in as table stakes.

Source: HFS Research, 2026

Health plans are notoriously known for maintaining operational control, down to the minutiae of delivery. However, SaS will need them to step back operationally, which will make operational leaders, in particular, very uncomfortable. The C-suite will be biased toward SaS as a function of risk and financial management, both of which are intrinsically tied together. The operational risk of managing platforms and the infrastructure that support them, along with the unpredictability of cost increases, is no longer worth the squeeze for health plan CFOs. While we expect CIO resistance, CFOs’ mandates will likely triumph over any pushback from technology leaders.

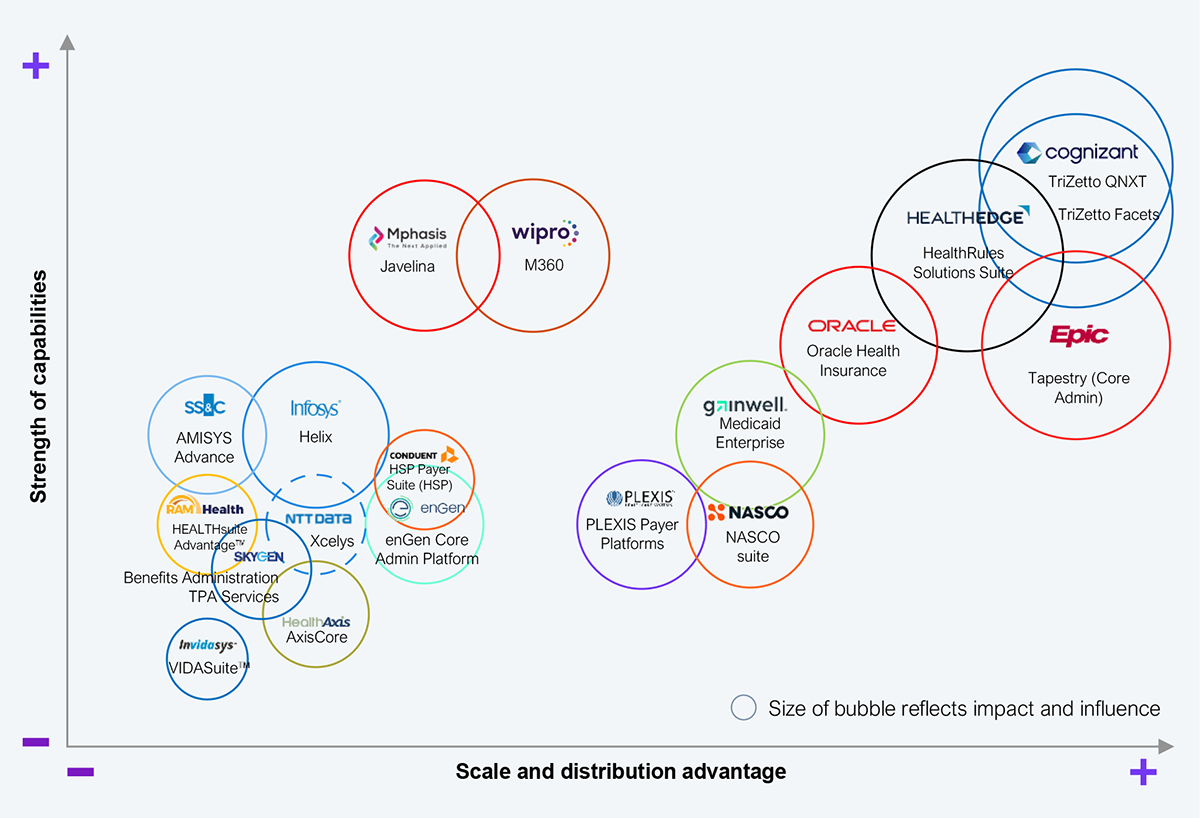

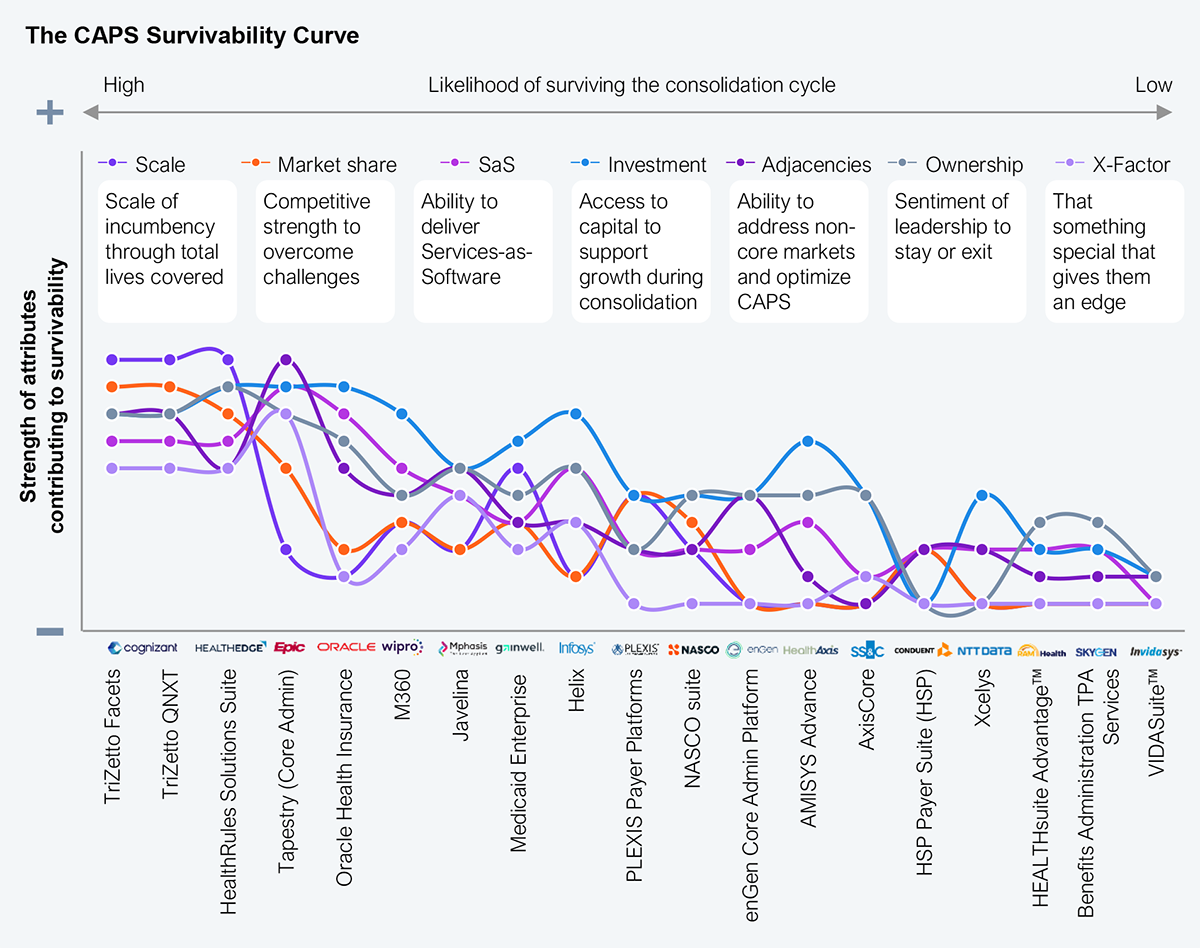

Over the last 40 years, approximately 20 CAPS providers have participated at some scale, delivering platforms, services, and functions to health plans. Exhibit 4 shows the current CAPS vendors at the intersection of their capabilities and distribution advantage. The chart is a retrospective view of market perception. While it is not indicative of CAPS vendors’ future success or lack thereof, it certainly provides a foundation for what might happen with their products.

Source: HFS Research, 2026

We analyzed 18 CAPS across seven dimensions: scale, market share, ability to deliver through SaS, access to capital, value to adjacent markets, ownership sentiment, and that special something. The market is likely to consolidate over the next 24 to 36 months to about 50% of the current list, as health plans’ shifting priorities clash with CAPS vendors’ inability to support them (see Exhibit 4).

Source: HFS Research, 2026

Most CAPS vendors do not have what it takes to win in the AI-enabled SaS paradigm. There is a propensity to implement AI as they have with other technologies in the past, applying them to address productivity rather than reimagining the value proposition. To compound the legacy thinking and capability gap, their history-based hubris falsely gives them confidence that health plan buying behaviors will not change, that the pressure to negotiate lower prices will be managed by enabling AI at a feature-functionality level, and that margins will be maintained. However, what they are missing in that calculus is exposure to the real decision-makers (CFOs) and their shifting sentiments toward a new delivery paradigm.

Health plan CIOs must choose to either partner with CAPS vendors who can deliver through SaS or transition to those who can. For CAPS leaders who have long believed that the cost of change is too high for health plans, think again. This roadmap will help health plans’ CIOs make the exit faster and simpler than you think.

Register now for immediate access of HFS' research, data and forward looking trends.

Get StartedIf you don't have an account, Register here |

Register now for immediate access of HFS' research, data and forward looking trends.

Get Started