The PwC: Services Capabilities for HCP, 2026 profile is for healthcare provider C-suites, transformation leaders, and finance and risk executives evaluating advisory-led, partner-enabled service partners.

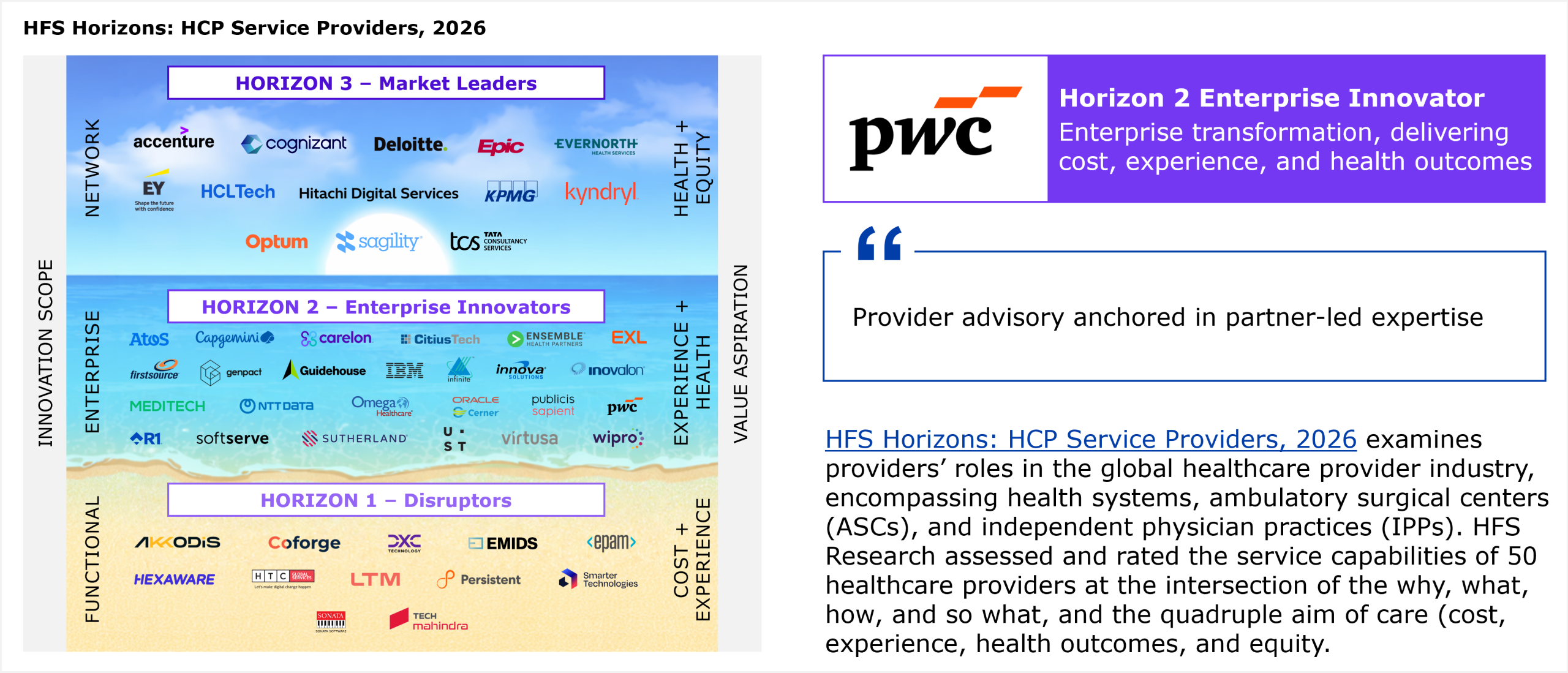

Note: All service providers within a Horizon are listed alphabetically

Source: HFS Research, 2026

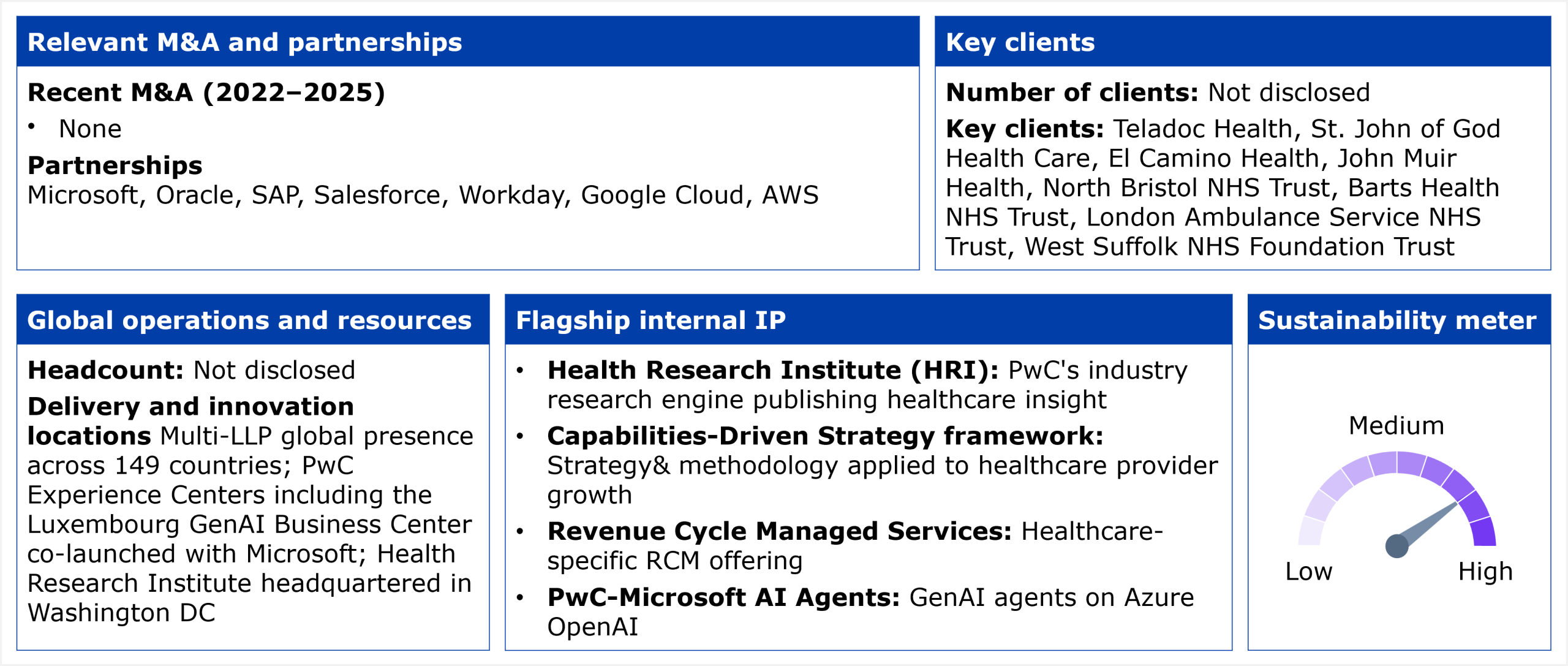

Source: HFS Research, 2026

Source: HFS Research, 2026

To read the complete report, click the download button below.

Register now for immediate access of HFS' research, data and forward looking trends.

Get StartedIf you don't have an account, Register here |

With the exception of our Horizons reports, most of our research is available for free on our website. Sign up for a free account and start realizing the power of insights now.

Our premium subscription gives enterprise clients access to our complete library of proprietary research, direct access to our industry analysts, and other benefits.

Contact us at [email protected] for more information on premium access.