Cost arbitrage and headcount growth no longer define relevance in an AI-shaped operating environment. Recognizing this inflection point, HFS Research and Sutherland convened insurance GCC leaders to a roundtable in February 2026 to move the conversation from GCC rah-rah to grounded GCC realism.

For insurers and their captives, this shift is overdue. The discussion focused on AI maturity, end-to-end ownership and decision rights, whether GCCs are positioned to drive enterprise value rather than simply execute tasks, and how the talent model must evolve to support an AI-led future.

There has been a long-standing need for industry-level dialogue among insurance capability leaders. It took us 10 years, but I’m glad someone did it. And finally, we are in this room.

— GCC delegate at the roundtable

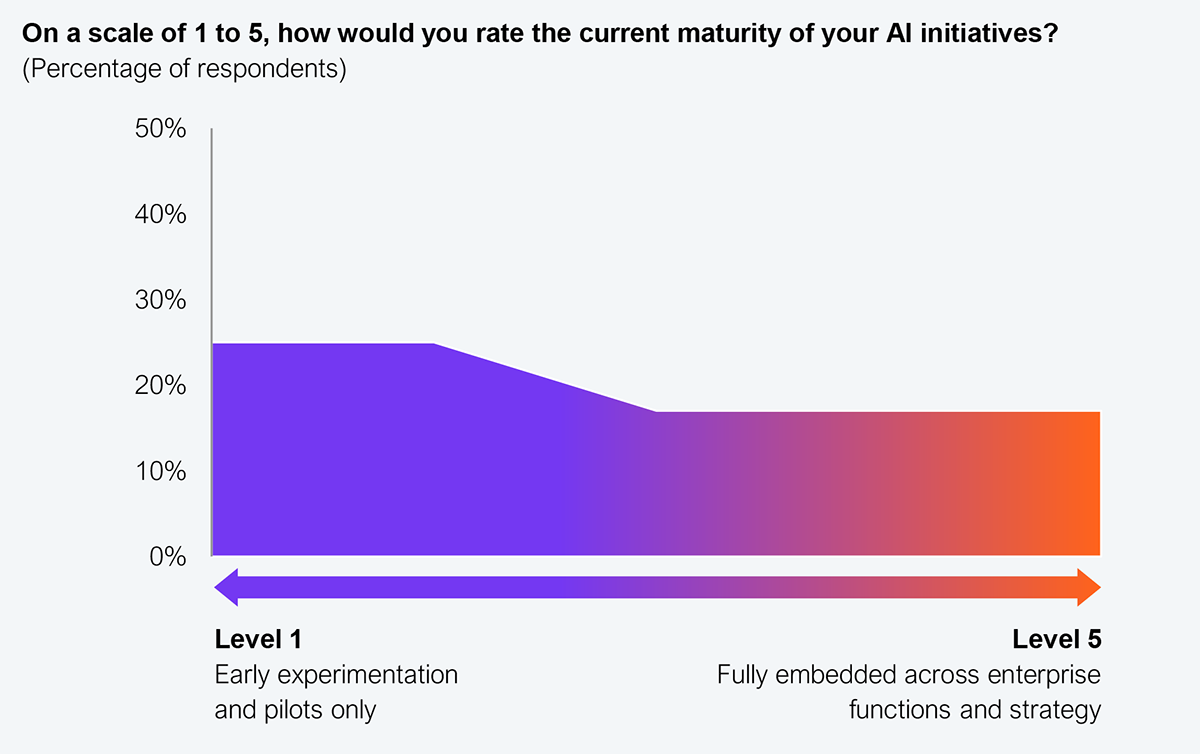

When asked about the GCC insurer AI maturity, participants clustered around level 2, with some beginning to edge toward level 3 (see Exhibit 1). There are meaningful pockets of advancement, particularly in software development, underwriting, claims augmentation, asset management, and internal service functions. However, adoption remains uneven across federated entities, geographies, and functions, limiting systemic scale.

Sample: 12 insurance GCC delegates

Source: HFS Research in partnership with Sutherland

The room agreed that the constraint is not technology. The “why” and the “what” of AI are largely settled. The real debate is the “how”: whether insurers can close the AI velocity gap between individual AI fluency and enterprise adoption, or whether leadership can rewire operating models fast enough to move beyond isolated pilots. Structural friction, decision-rights ambiguity, governance alignment, data and process debt, and matrixed ownership continue to slow institutionalization. Praveen Sasidharan, Chief Insurance Officer at Allianz Services, reflected on those points.

How we get the scale is definitely by ensuring we have standard and harmonized processes globally.

— Parveen Sasidharan, Chief Insurance Officer, Allianz Services

Our take: Insurance GCCs are not short on intent, experimentation, or even pockets of capability. The maturity gap is structural. The next leap will not come from better tools but from clarifying accountability, collapsing silos, embedding AI into end-to-end value streams, and shifting from process execution to end-to-end ownership of the value chain in the GCC centers.

Many GCCs believe they have the right capabilities to lead AI. However, formal mandates and product ownership still reside within headquarters, creating institutional hesitation. Others reject this divide altogether, operating as fully integrated enterprises where data, AI, and analytics are globally distributed and maturity advances as a single cohort rather than by geography. A third model, common among large, federated insurers, positions GCCs as engines of standardization and scale, anchoring data, analytics, and engineering capabilities, even if P&L accountability remains centralized.

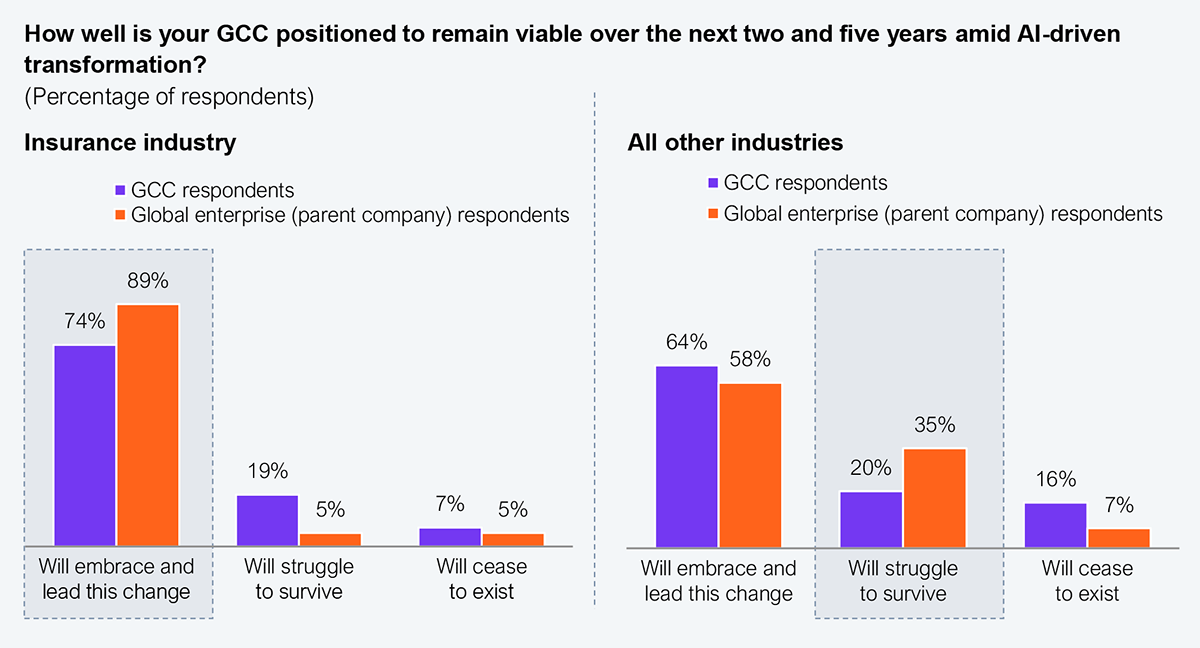

Regardless of structure, expectations from headquarters continue to rise. Compared to other industries, insurance places greater emphasis on GCCs to accelerate their AI implementations (see Exhibit 2). But in practice, many wait for clearer empowerment and accountability before moving decisively.

Sample insurance industry: 79 Insurance enterprise (across global captive centers (42), GCCs, and their global enterprise (37) parent companies

Sample all other industries: 121 enterprises (excluding insurance; across global captive centers [64], GCCs, and their global enterprise [57] companies)

Source: HFS Research, 2026

We have to be intentional by design about ownership and decision rights.

— GCC delegate at the roundtable

Our take: Stop organizing work around geography. Instead, align the decision rights and business accountability with where work sits and make that ownership explicit and measurable.

Talent emerged as a pivotal theme. Leaders made it clear that the conversation can no longer be about headcount growth but about capability density. The mandate is to “do more with less,” shifting from scaling to building and skilling product thinkers, domain-led technologists across risk selection and asset management, and AI-native teams.

Several participants emphasized creating an environment where people can learn, experiment, and close the AI velocity gap between how individuals use AI and how enterprises operationalize it. Purpose and exposure to meaningful business outcomes were seen as stronger retention levers than compensation alone.

At the same time, a pragmatic counterview surfaced: attrition is not always a threat. Managed well, it refreshes capability, creates room for new skills, and supports the transition to a leaner, AI-enabled operating model.

Our take: Re-architect the GCC talent model for AI. Audit future-critical skills, redeploy and reskill aggressively, embed learning into performance systems, and build a culture that rewards reinvention, not scale.

The roundtable discussion revealed that insurance GCCs no longer want to be defined by cost arbitrage or headcount growth. They want to be valued for the enterprise capabilities they bring to the AI arms race. While some are beginning to operate at that level, many are constrained by the legacy operating drag, ambiguous decision rights, and talent structures that are not yet designed to scale AI.

Future relevance will be determined by the ability to secure a mandate, re-architect workflows, and build the capability scaffolding required to operate as the enterprise AI center of capability, not merely a captive arm.

When you connect enterprise imperatives to how you structure the GCC as a strategic asset, that’s where the magic happens.

— Vijay Pahuja, SVP, Chief Business Officer – Insurance, FS, Lending, Sutherland

Register now for immediate access of HFS' research, data and forward looking trends.

Get StartedIf you don't have an account, Register here |

With the exception of our Horizons reports, most of our research is available for free on our website. Sign up for a free account and start realizing the power of insights now.

Our premium subscription gives enterprise clients access to our complete library of proprietary research, direct access to our industry analysts, and other benefits.

Contact us at [email protected] for more information on premium access.

If you are looking for help getting in touch with someone from HFS, please click the chat button to the bottom right of your screen to start a conversation with a member of our team.