As a CIO, you are no longer evaluating AI tools in isolation. You are being forced to decide which vendors will control the flow of work, data, decisions, and governance inside the business. Oracle, Microsoft, and SAP are not simply adding AI to their platforms. They are each trying to become the preferred AI control plane around enterprise execution, data gravity, governance, and economics. If you leave that choice to vendor momentum, you will find them dictating the operating model, governance structure, and switching costs.

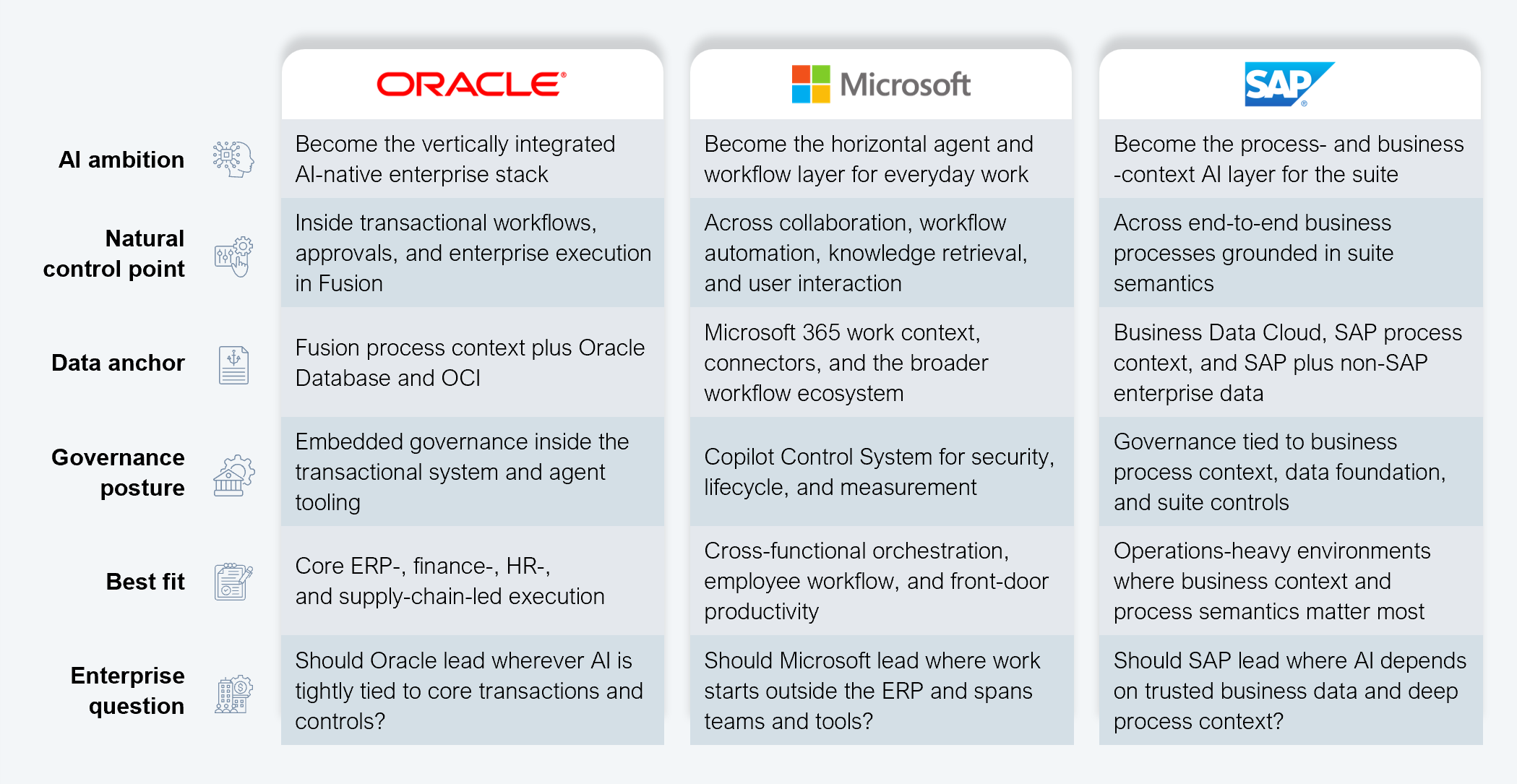

In March 2026, Oracle introduced Fusion Agentic Applications, expanded AI Agent Studio for Fusion, and unveiled new agentic AI capabilities in Oracle AI Database, while continuing to invest heavily in AI infrastructure through Oracle Cloud Infrastructure. And not just Oracle. Microsoft is scaling Copilot Studio, agent flows, and the Copilot Control System, and SAP is pushing Joule agents alongside Business Data Cloud and its Reltio acquisition to make SAP and non-SAP data more AI-ready. CIOs must note that these announcements conceal something beyond simple product roadmaps: they are attempts to redefine enterprise architecture, economics, process ownership, and dependency around AI-native execution (see Exhibit 1).

Oracle’s strategy is the most vertically integrated of the three. It is embedding AI agents directly into Fusion workflows and extending AI development and orchestration through Agent Studio, while tying those capabilities back to Oracle’s application, data, and infrastructure layers. Microsoft’s strategy is more horizontal: it wants Copilot Studio and its governance stack to sit across collaboration, workflow, and agent orchestration. SAP is leaning into process semantics and business context, using Joule agents plus Business Data Cloud to make AI act on trusted enterprise data across SAP and non-SAP landscapes.

Source: HFS Research, 2026

The real proving ground will be on the data context and which platform becomes most trusted and usable rather than which model is faster. As explored in our AWS AI resilience rivals at lunch POV, long-term advantage is increasingly shaped by ecosystem control, infrastructure resilience, and proximity to enterprise data rather than raw model performance.

The question is no longer “which vendor has the best AI agents?” It is “which vendor do we allow to sit in the middle of execution?” This is where our AI control mapping and dependency perspective becomes critical, highlighting how control often sits across layers that enterprises do not fully see or govern. Once AI moves from assistance to action, the winning platform influences workflow design, data access, escalation logic, auditability, and switching costs.

The traditional playbook assumes that platforms can evolve independently. However, that approach breaks down in the AI era because each of these platforms is now trying to mediate decisions and actions, not just store records or support users. As each vendor tries to expand its gravitational pull, letting them scale AI on their own terms creates multiple control systems, governance models, data assumptions, and definitions of what “automated” means. The result will not be an AI-enabled enterprise, but an AI-fragmented one.

As vendors package more orchestration, agent-building, and governance into the platform, some traditional implementation work becomes less differentiated. But that does not mean enterprise costs fall neatly. Spend shifts toward data remediation, process redesign, controls, observability, and premium platform consumption. The real risk is paying more for AI while underestimating the operating model changes needed to realize value.

Simultaneously, governance shifts from a compliance exercise to an operating discipline. CIOs can no longer manage AI primarily by app tower. The unit of governance shifts toward end-to-end processes such as order-to-cash, source-to-pay, hire-to-retire, or financial close. If CIOs continue to govern AI only by platform, then they will create overlap, duplication, and accountability gaps. Governance must become a part of how AI is designed, deployed, monitored, and justified from day one.

The AI roadmap of SAP, Oracle, and Microsoft shows how quickly each is moving from AI assistance to AI-mediated execution, becoming the layer enterprises depend on to coordinate work, data, and decisions. CIOs should not evaluate these moves as parallel product announcements.

Oracle has a lead where AI is tightly coupled to transactional execution, with controls embedded and processes already anchored in Fusion and Oracle data. Microsoft has an advantage in collaboration, knowledge retrieval, approvals, and orchestration across the employee workflow layer. SAP’s deep process semantics, suite context, and trusted business data across operational domains make its AI a natural fit in these scenarios.

It is natural that most large global enterprises will explore a heterogenous AI ecosystem. That makes it necessary for boundaries to be designed by enterprise architecture and operating model leaders, not left to vendor momentum. No vendor should define accountability, human override, policy enforcement, or value realization on its own terms. Those are enterprise decisions. Vendors can provide tooling and accelerators; they should not set the operating model.

The answer does not lie in parallel pilots and siloed roadmaps. It is about defining where each platform leads, putting governance above the vendors, insisting on interoperability before scale, and measuring success in business outcomes rather than AI activity. CIOs that do this well will turn vendor competition into advantage. Those that do not will wake up with multiple AI operating models, unclear accountability, and a fresh layer of transformation debt.

Register now for immediate access of HFS' research, data and forward looking trends.

Get StartedIf you don't have an account, Register here |

With the exception of our Horizons reports, most of our research is available for free on our website. Sign up for a free account and start realizing the power of insights now.

Our premium subscription gives enterprise clients access to our complete library of proprietary research, direct access to our industry analysts, and other benefits.

Contact us at [email protected] for more information on premium access.

If you are looking for help getting in touch with someone from HFS, please click the chat button to the bottom right of your screen to start a conversation with a member of our team.