We like to keep it simple at HFS Research. Despite lots of fun ways to carve up business outcomes into microcosmic key performance indicators, there are only four measures of success that matter: growing revenue, increasing profit, improving customer experience, and enabling effective regulatory compliance. When it comes to assessing the effectiveness and progress of digital transformation programs, these are the big buckets we look at.

For the banking and financial services (BFS) sector, there is plenty of media coverage of the massive digital transformation investments that the world’s biggest BFS brands are making. These investments are supposed to be “modernizing the core” and enabling new business. However, HFS’ latest look at the health of the sector shows continued anemic returns.

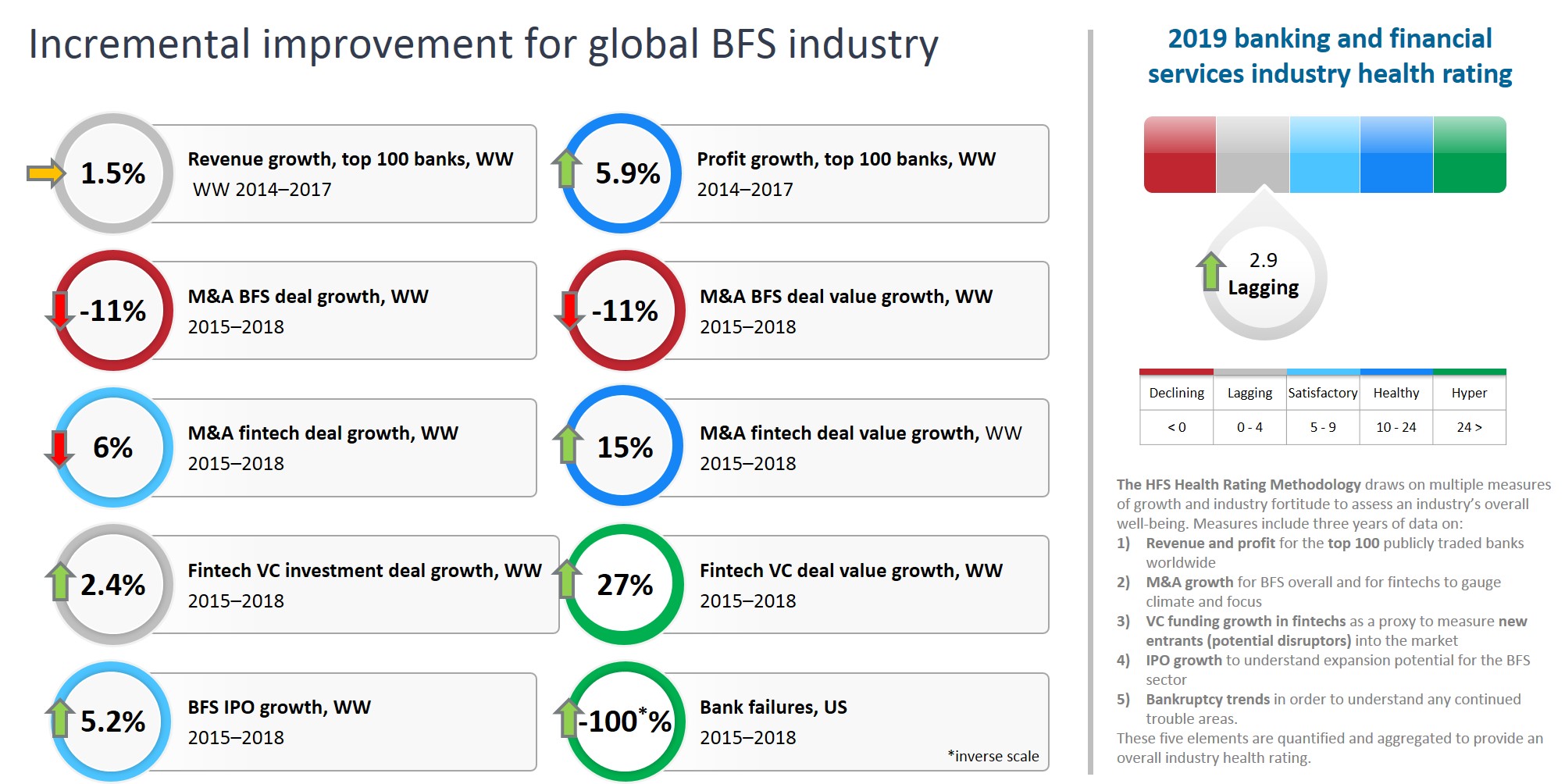

This POV examines the state of digital transformation in the BFS sector, leveraging the latest data from our Industry Digital Transformation survey. Spoiler alert: Funding new offerings through bottom-line gains only works if you reinvest the savings.

The BFS sector continues to lag more than a decade after the global financial crisis

The world is constantly evolving to match new technologies, yet a large part of the BFS sector continues on the same legacy systems. It has failed to fully recover from the financial crisis, which was more than 10 years ago. HFS has tracked the industry’s struggle, and Exhibit 1 showcases the “lagging” health rating. Profit margins show some signs of improvement (5.9% growth), but revenue growth remains anemic (1.5%).

Meanwhile, the 27% rise in fintech venture capital deal value growth and the 15% rise in merger and acquisition fintech deal value indicate that the market remains flooded with upstart disrupters and is increasingly competitive. The $14 billion Series C round by Ant Financial and the $12.8 billion Worldpay acquisition by FIS are two examples of this, with the latter demonstrating how an increasing number of BFS firms are looking to compete through acquisitions (buy) rather than development (build). Ultimately, the ultra-competitive trajectory of the BFS sector is showing no signs of slowing down. If banks hope to survive, they need to focus on competing more effectively and achieving tangible results with their deep investments in digital transformation.

Exhibit 1: While there is a slight improvement, the BFS industry continues to lag

Source: HFS Research 2019, public financial filings, Institute for Mergers, Acquisitions and Alliances M&A statistics, KPMG and Pitchbook fintech data, EY IPO data, and FDIC failed bank database.

What are the roadblocks to banks’ digital transformation dreams? Talent, data, and investment funds

In our annual Industry Digital Transformation survey, we asked a mix of business and IT leaders about their plans for digital transformation. Exhibit 2 shows that the top strategic objective for digital transformation for BFS firms is the prioritization of topline revenue (36%). Other sectors identified increasing bottom–line profit as their leading priority (33%).

Exhibit 2: Not surprisingly, BFS firms’ strategic objectives for digital transformation favor revenue growth

![]()

N= BFS 37, other industries 331

Source: HFS Research, 2019

Revenue growth won’t come just from investing in digital. There needs to be transformation—doing things differently and offering new value and benefit to customers. The emergence of challenger banks like Monzo, which has over two million customers, showcases the positive response to change. What sets challenger banks apart is their model, which allows customers complete transparency and control of their finances, wherever they are.

Change agents are levers for transformation

Efforts to innovate regularly involve experimenting with change agents. Banks are well ahead of other industries in terms of the volume of change agents they have in production environments, with cloud leading the way (35%). Despite this seeming glow of maturity and scale, using change agents doesn’t drive transformation unless the bank applies them to specific problems and desired outcomes. Many tend to drive operational efficiency rather than revenue gains.

Exhibit 3: BFS investments in change agents to drive digital transformation—production environment view

![]()

N= BFS 37, other industries 331

Source: HFS Research, 2019

As a decade of sluggish performance has demonstrated, transformation for BFS firms is no easy task. Exhibit 4 outlines the top inhibitors holding BFS firms back from getting there. It’s no surprise, given the anemic revenue growth in recent years, that uncertainty about required financial investments is the biggest concern with the greatest concentration of respondents ranking it as the top inhibitor.

If traditional BFS firms fail to generate consistently solid revenue, it is unlikely that they will have the necessary funds to reinvest into the development of new offerings or services. The mild profit recovery suggests that operations are getting more efficient, but more effort is required to achieve topline returns.

Exhibit 4: BFS firms’ top barriers to achieving digital transformation

![]()

N= BFS 37, other industries 331

Source: HFS Research, 2019

While risk and compliance concerns will remain a perpetual inhibitor in BFS, data quality issues and lack of talent loom large as very practical obstructions. It’s easy enough to procure the latest technologies, but having data ready to use and the right skills to drive execution remain major challenges. The reality is that these factors must align funding, enablement of vast data stores, and evolving talent profiles for BFS firms to have a decent shot at transformation. However, if the focus remains on operational efficiency, then revenue growth may not follow.

The Bottom Line: If traditional financial services firms want revenue growth, they need to stop prioritizing operational efficiency alone.

Traditional firms have loads of legacy to remediate to begin to approach anything vaguely resembling the Digital OneOffice. However, the investment needs to serve a dual purpose of driving operational efficiencies as well as enabling new revenue streams. Waves of fintechs are challenging traditional banking models, utilizing their ability to maneuver the market to satisfy customer needs without the burden of legacy technology. The survival of incumbent BFS firms hinges on their willingness to pivot their business models, not just how the work gets executed.

Register now for immediate access of HFS' research, data and forward looking trends.

Get StartedIf you don't have an account, Register here |

With the exception of our Horizons reports, most of our research is available for free on our website. Sign up for a free account and start realizing the power of insights now.

Our premium subscription gives enterprise clients access to our complete library of proprietary research, direct access to our industry analysts, and other benefits.

Contact us at [email protected] for more information on premium access.