This HFS Operational Playbook is for CEOs of mid-tier Indian hospitals seeking to grow their share of international medical tourism by orchestrating the end-to-end patient journey.

This playbook is for CEOs of mid-tier Indian hospitals seeking to grow their share of international medical tourism by orchestrating the end-to-end patient journey rather than managing it as disconnected handoffs across hospital teams, facilitators, and travel partners.

This approach should yield a forecastable international patient pipeline, with inquiries answered within 24 hours, 20%–30% inquiry-to-treatment conversion, pre-arrival logistics locked in within 5–10 days, and measurable follow-up-driven referrals.

HFS Operational Playbooks are practical guides to solving key enterprise challenges that consume significant costs, time, and resources. The playbook provides enterprise leaders a realistic roadmap with specific “to-dos” to address their everyday challenges so they can clear mental and financial space to deliver next-level value.

Mid-tier Indian hospitals receive a steady stream of international inquiries but fail to convert them into treated patients, losing share to Tier-1 players who have built end-to-end orchestration around the same demand pool.

Healthcare systems across the US, the Middle East, and Europe are under growing strain. In the US, employer-sponsored family health premiums rose 6% in 2025, outpacing both wage growth (4%) and inflation (2.7%), a gap that has compounded for over a decade. Wait times for elective procedures routinely stretch past six months in many public systems, and access to timely, high-quality care is becoming harder to obtain. For many patients, crossing borders for treatment is no longer a matter of convenience; it is a necessity.

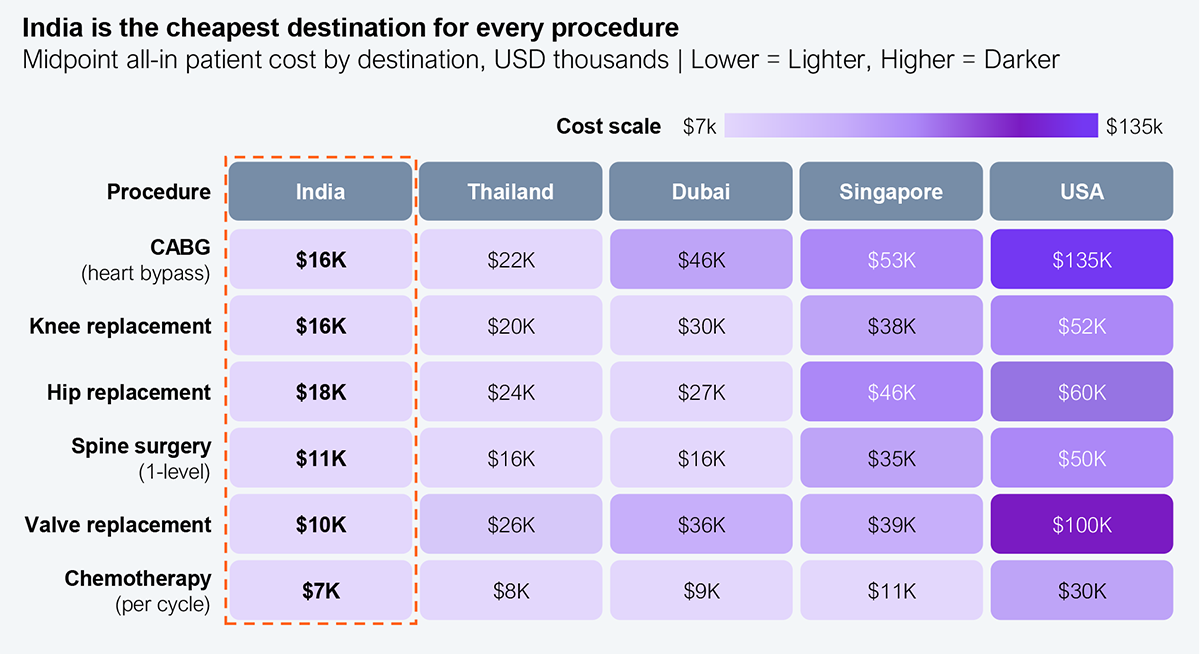

Indian hospitals offer a rare combination of advantages: clinical capabilities that match global standards, a 60%–90% cost advantage over the US, and near-zero waiting periods. Few destinations solve both cost and access at once.

Source: HFS Research, 2026

Tier-1 hospitals, primarily large chains such as Apollo, Fortis, Manipal, Medanta, and Max, have built coordinated international patient operations and are attracting a disproportionate share of the volume. Apollo expects international patient revenue to rise from 7% to 10% in FY25; Manipal draws 20%–25% of its medical-value-travel revenue from West Asia alone.

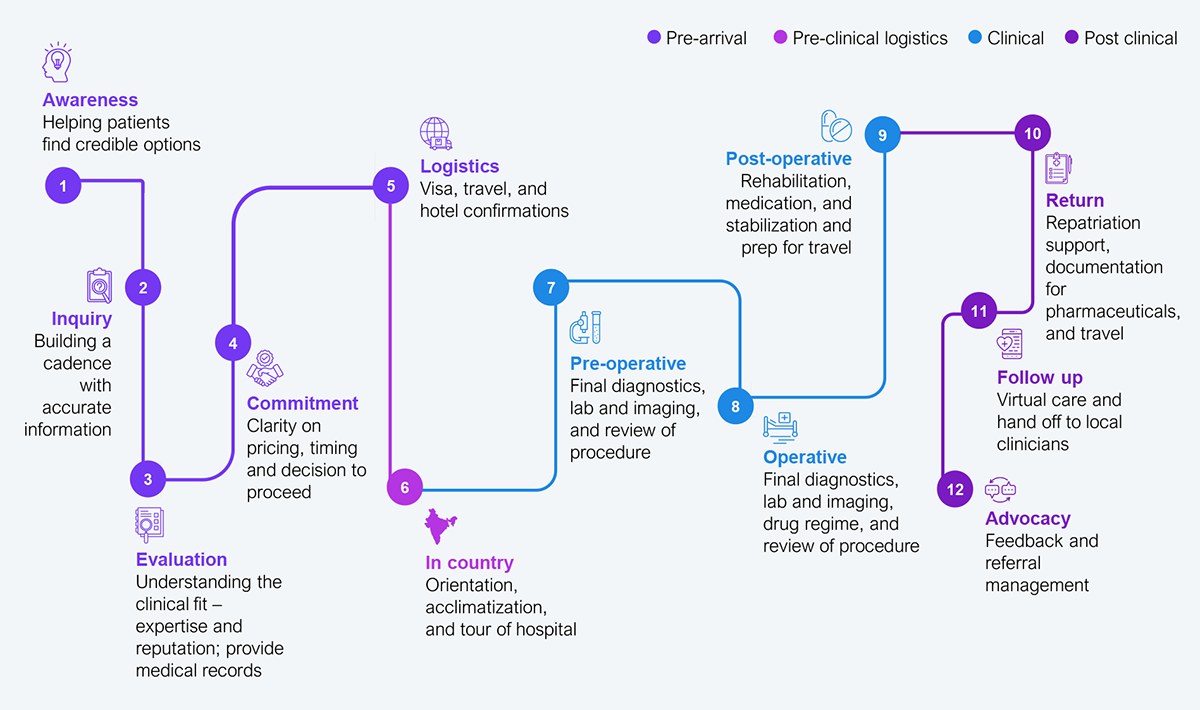

Mid-tier hospitals are less equipped to convert the international inquiries they already receive, not for lack of clinical capability, but because the journey is fragmented across inquiry, estimate, visa, travel, admission, and follow-up, with no single owner orchestrating the case. Today’s model is fragmented. Patients move across hospital websites, facilitators, travel agents, and internal hospital teams without a single, connected flow. Capabilities such as international patient departments (IPDs) are strong in some hospitals but inconsistent across the full journey; they are typically concentrated in the small cohort of internationally accredited chains, while the broader market operates without dedicated IPD infrastructure. The international patient journey across medical tourism today spans multiple fragmented touchpoints (see Exhibit 2).

Source: HFS Research, 2026

The current reality of medical tourism is a 12-step journey fragmented across hospitals, facilitators, travel partners, and internal teams (see Exhibit 2). These steps operate in silos, resulting in delays, inconsistent experiences, and significant conversion losses. But these are not 12 independent processes. They are fragmented pieces of a smaller set of core functions every hospital must manage.

The absence of a single, orchestrated layer is the core bottleneck, making it clear that while India may deliver excellent care, it does not have a predictable or seamless experience.

The opportunity cost of staying fragmented is measurable. India attracted nearly 650,000 international patients in 2024, up from approximately 180,000 in 2020, and medical tourism now contributes 7%–12% of revenue at major corporate hospitals. India’s premium hospital chains are growing international-patient revenue in the low-to-mid double digits—Max 27%, Medanta 24%, and Fortis 12.2% in FY24—while mid-tier hospitals likely under-convert international demand. However, the exact leakage rate is not publicly available for verification.

This playbook delivers three compounding outcomes (commercial, operational, and experiential) that convert medical tourism into a forecastable, scalable business.

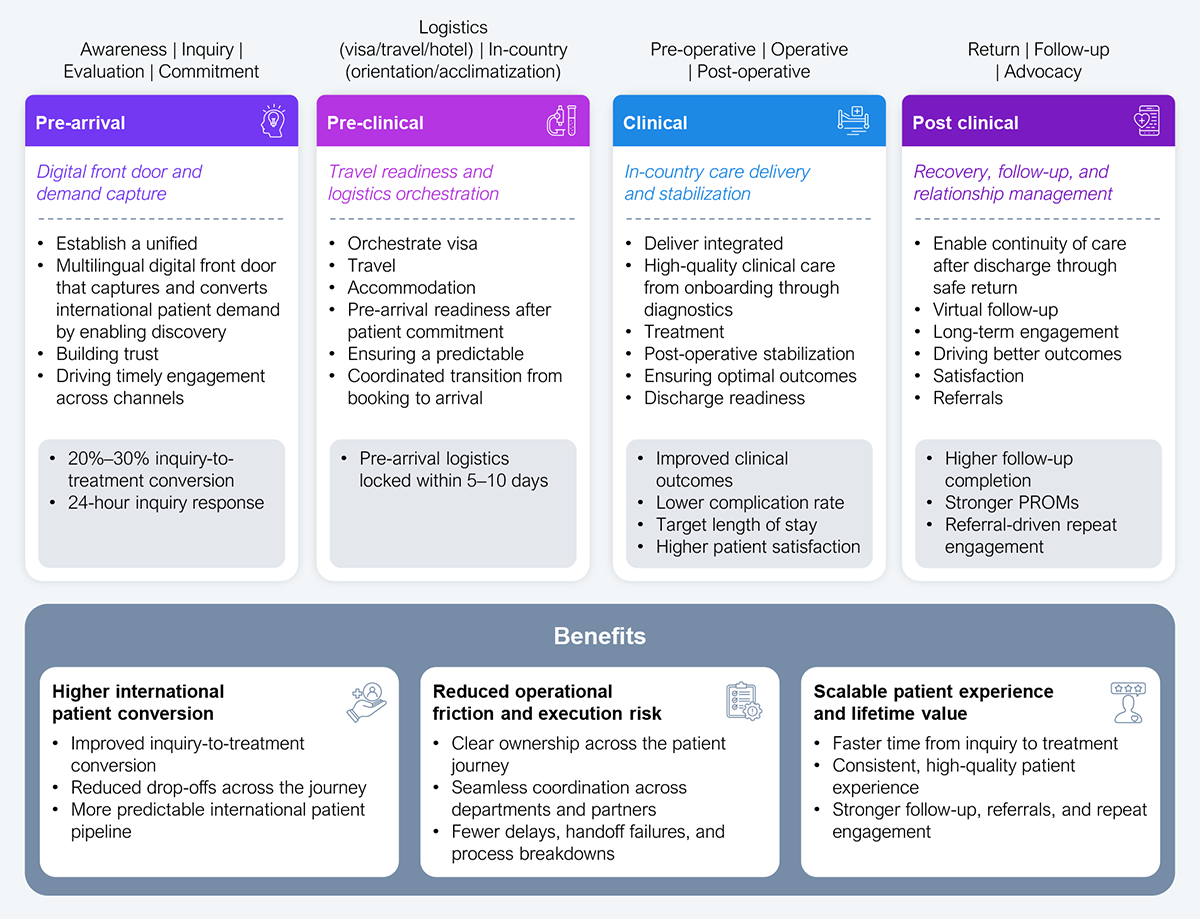

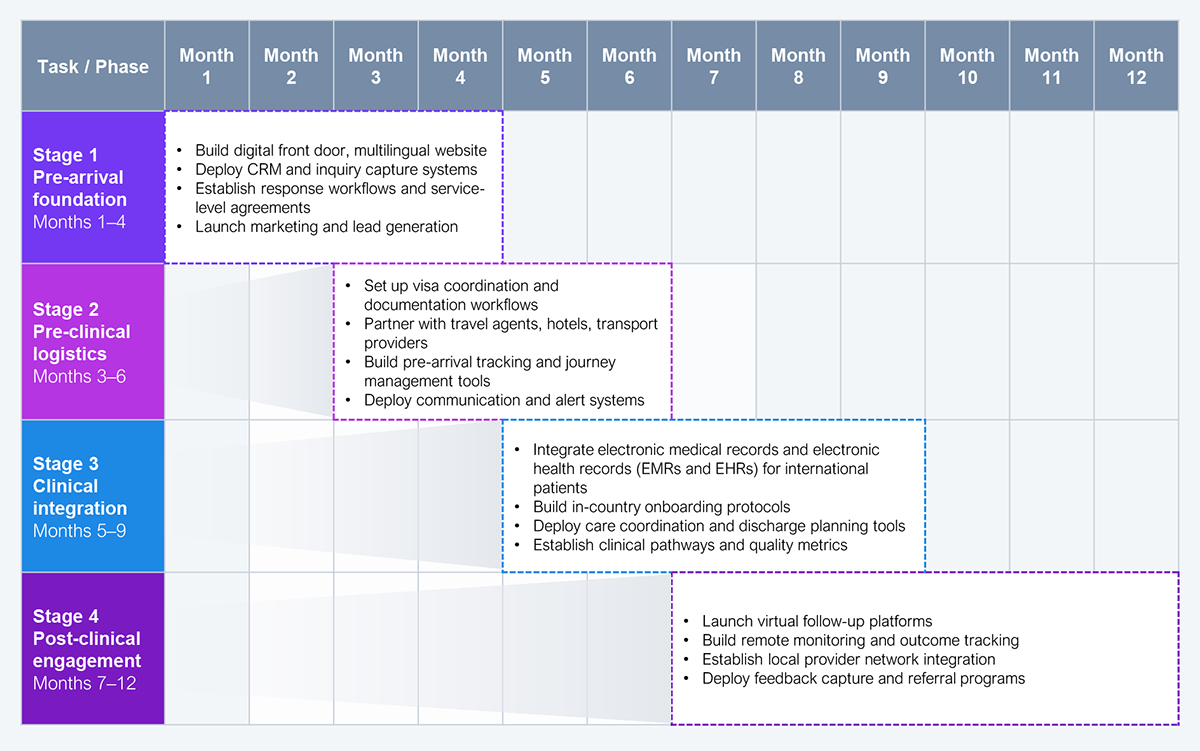

The opportunity represents a completely different operating model. Indian hospitals must transition to a platform-based, patient journey orchestration model. The focus should move from investing in discrete capabilities to managing measurable results for the entire patient journey, including conversion rates, patient experience, and continuity. Since the international patient journey involves many stakeholders, regions, and processes, execution can’t be ad hoc. It must be structured, phased, and operationally orchestrated end to end (see Exhibit 3).

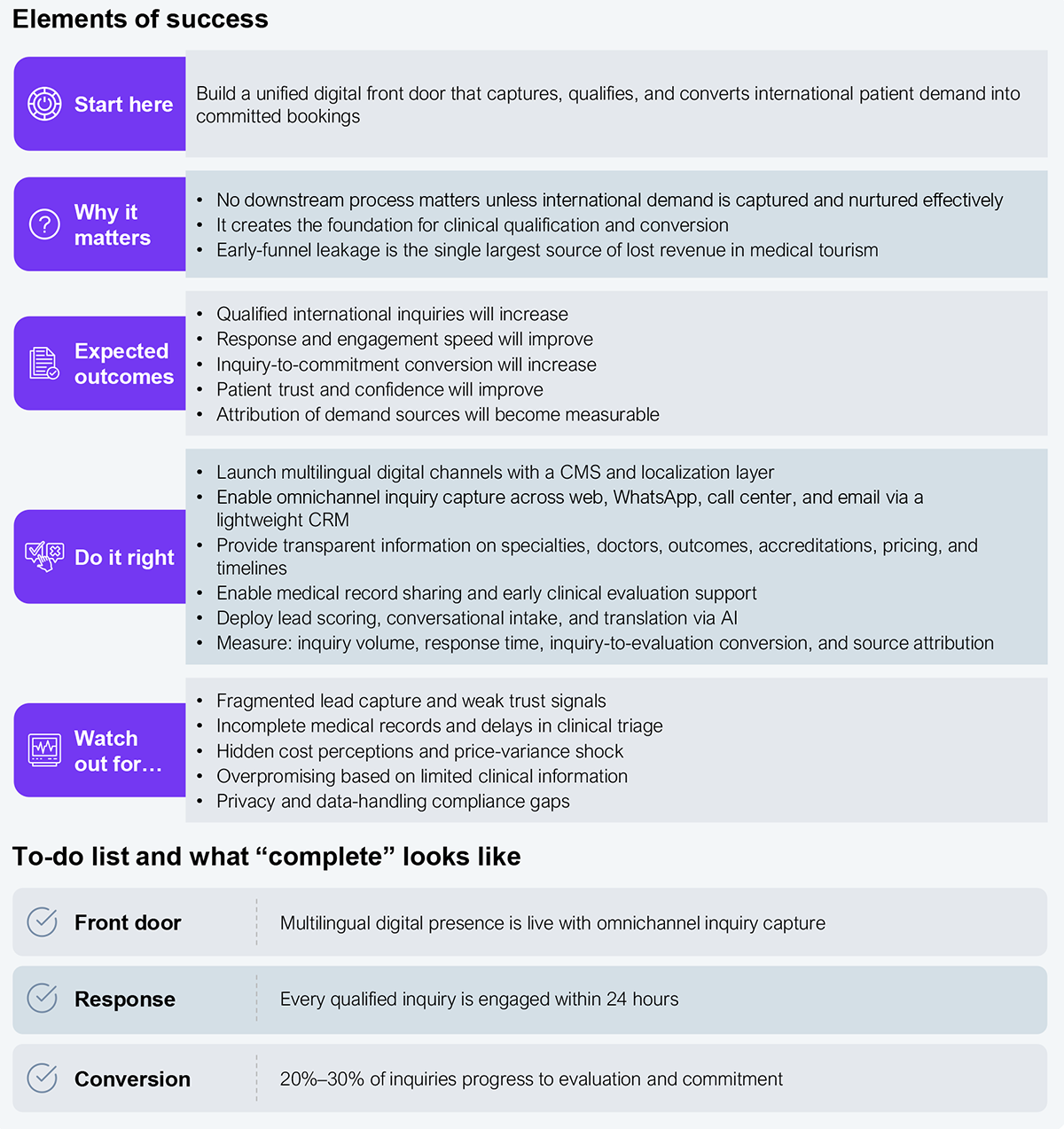

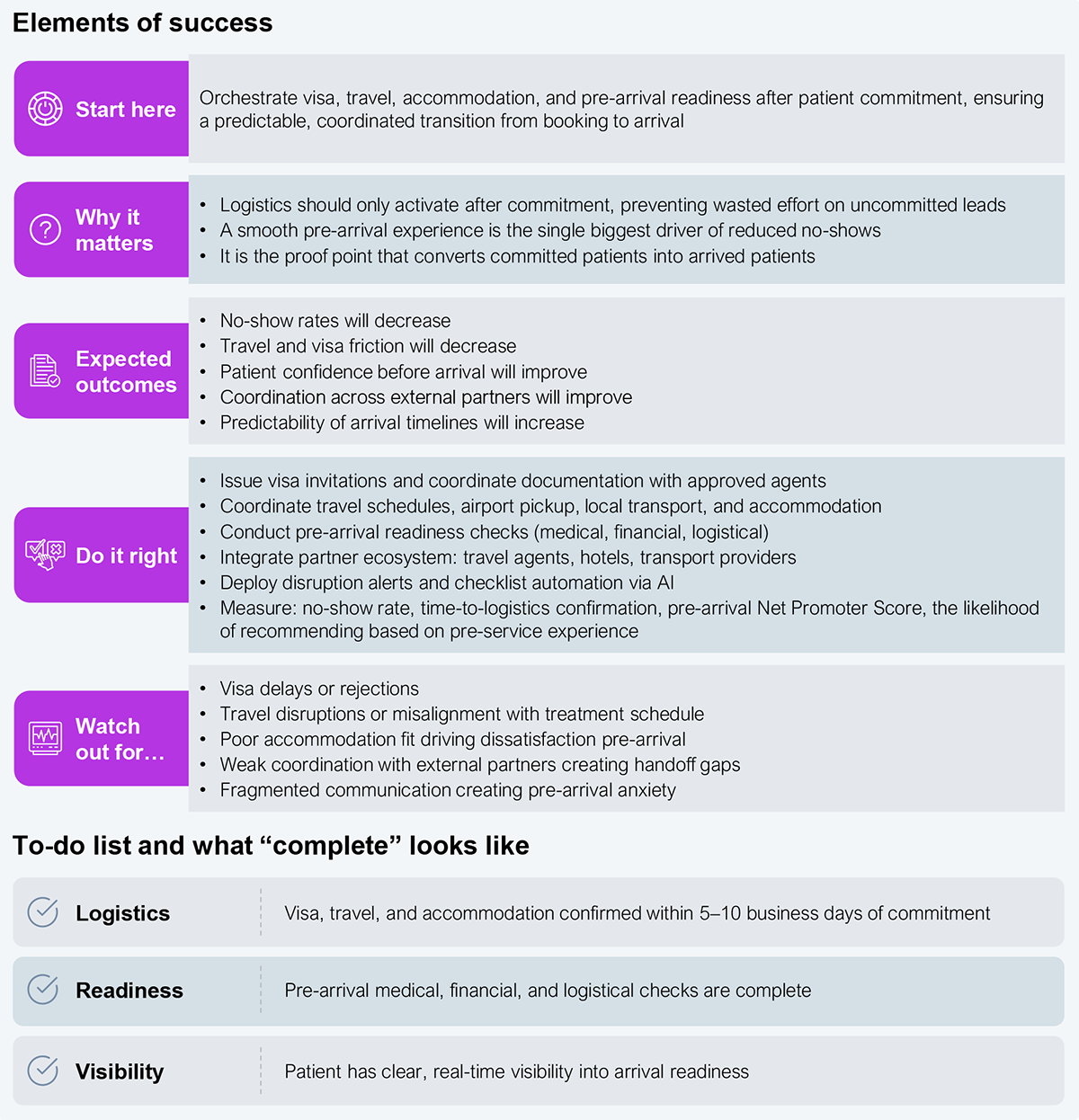

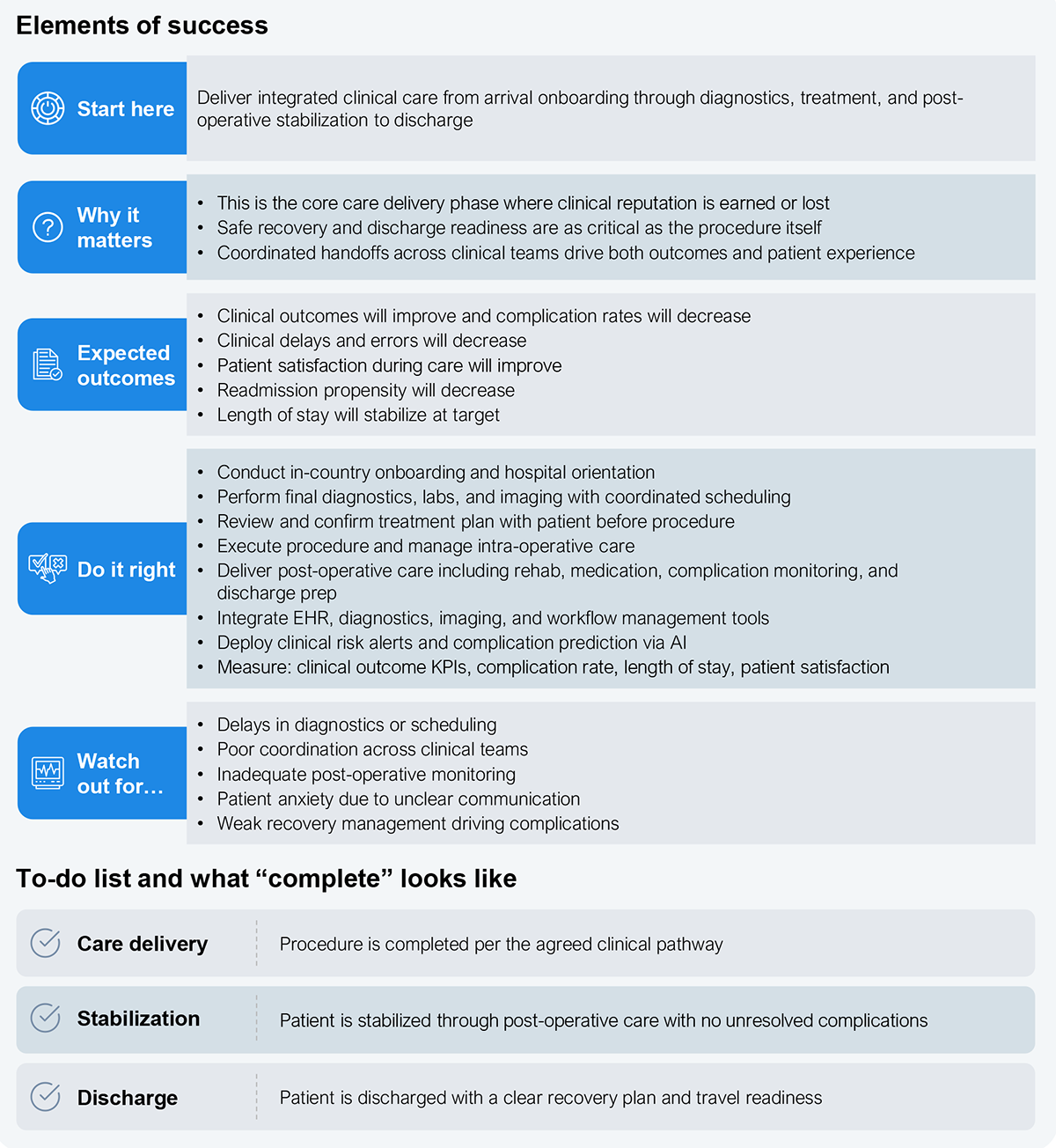

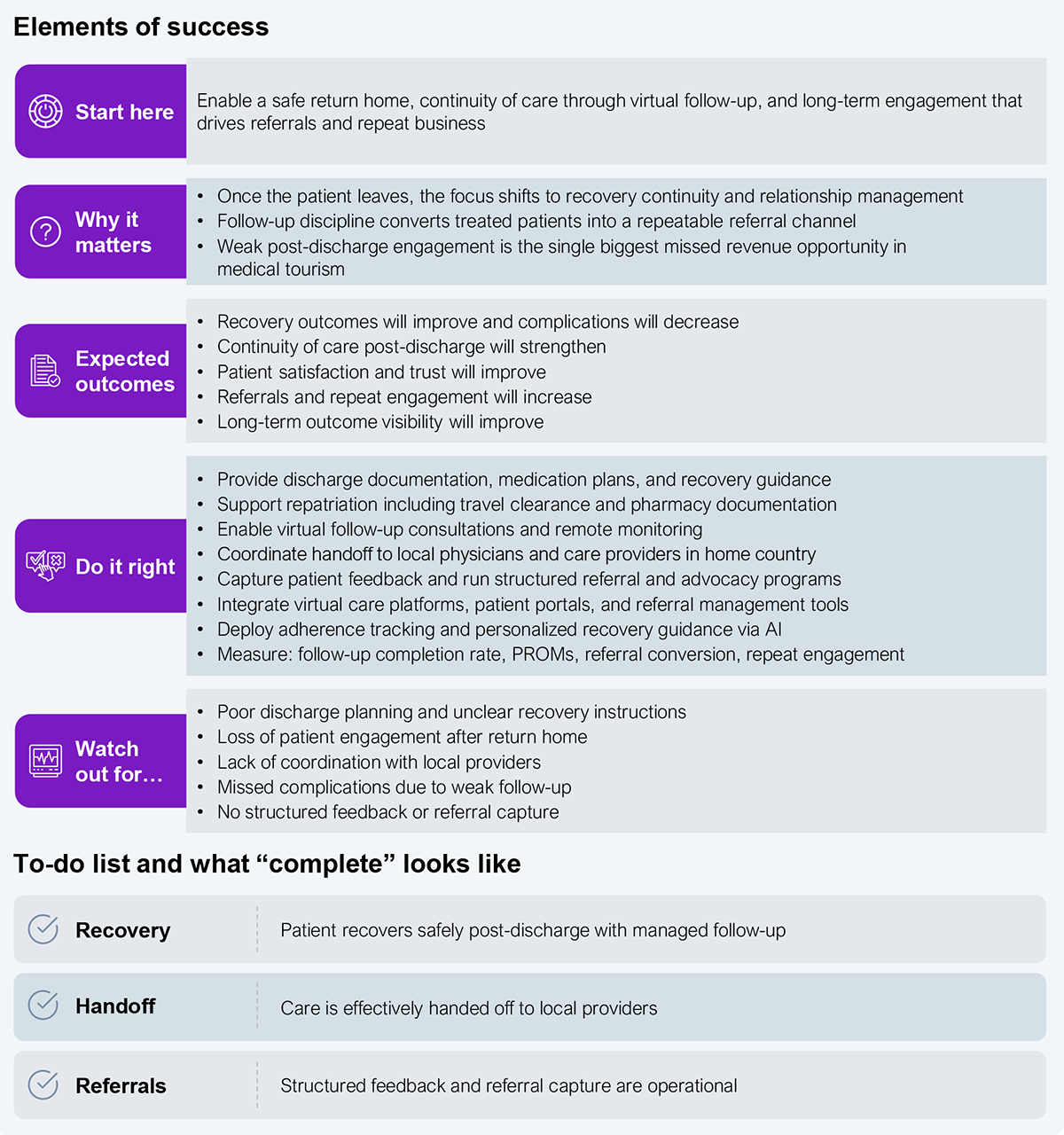

We consolidated the 12-step patient journey into four orchestrated stages, aligning clinical, operational, and commercial workflows under clear ownership. Each stage bundles multiple touchpoints into an accountable end-to-end process, powered by integrated technology and measurable outcomes.

The four-stage framework in Exhibit 3 encompasses all steps from the unorchestrated process in Exhibit 2:

This approach transforms hospitals from fragmented touchpoint management to journey orchestration:

Source: HFS Research, 2026

While the four-step playbook defines what hospitals must do across the international patient journey, execution ultimately depends on how underlying systems and workflows support these steps.

The following steps translate the international patient journey into a structured operating model that delivers measurable outcomes rather than remaining a coordination exercise.

Overall transformation may not be feasible all at once, so it is better to approach it in stages, starting with basic capabilities and progressing to more complex ones (see Exhibit 4). This approach tends to have a greater cumulative impact than building the entire ecosystem simultaneously.

Initial capabilities, such as a digital front door, inquiry capture, and clinical intake, should be established within the first 8–12 weeks, enabling hospitals to begin converting international patient demand early. Commercial conversion, case confirmation, and basic logistics coordination should follow immediately to create a visible and predictable patient pipeline.

In the next phase, hospitals should operationalize in-country care orchestration, including scheduling, diagnostics coordination, and patient experience management. This is where fragmentation is most visible and where operational discipline delivers immediate impact.

Finally, continuity capabilities, including discharge standardization and virtual follow-up, should be layered in to extend care beyond hospital walls and unlock referral-driven growth.

Source: HFS Research, 2026

The following list includes relevant HFS perspectives on India’s medical tourism opportunity and the operating model shifts shaping it.

Register now for immediate access of HFS' research, data and forward looking trends.

Get StartedIf you don't have an account, Register here |

With the exception of our Horizons reports, most of our research is available for free on our website. Sign up for a free account and start realizing the power of insights now.

Our premium subscription gives enterprise clients access to our complete library of proprietary research, direct access to our industry analysts, and other benefits.

Contact us at [email protected] for more information on premium access.