Insurers are no longer on the sidelines while AI reshapes other industries. The technology is redefining the very core of insurance: understanding risk, pricing it right, and serving policyholders effectively with empathy. To unpack the how, HFS Research, in partnership with IBM, brought 17 top insurers to a New York boardroom. The message was clear: the era of “death by 1,000 POCs” is over.” AI is live in production across underwriting, claims, customer service, and operations.

Source: HFS Research; August 19, 2025; New York

AI’s potential is massive, but it’s easy to get caught up in the hype and scattered use cases. What makes AI, particularly GenAI, truly different is the reusability of its core components—the building blocks that power multiple functions of claims, pricing, and underwriting. For example, a natural language processing (NLP) engine designed for customer queries can easily be tuned for claims adjudication. A foundation model trained to analyze BOTH structured and unstructured data can flex across the claims cycle and underwriting.

A smarter approach is to apply AI to transform high-value functions such as pricing, underwriting, claims, and policy servicing while steering clear of subscale experiments. But this requires a complete rethink of workflows, moving away from sequential handoffs toward straight-through resolution or connecting workflows and data pipelines to stream IoT and behavioral data from telematics, wearables, and smart homes to recalibrate risk in real time for dynamic pricing. This function-wide view unlocks shared enablers such as data preparation, systems integration, and change management, turning a single investment into compounding ROI across the enterprise.

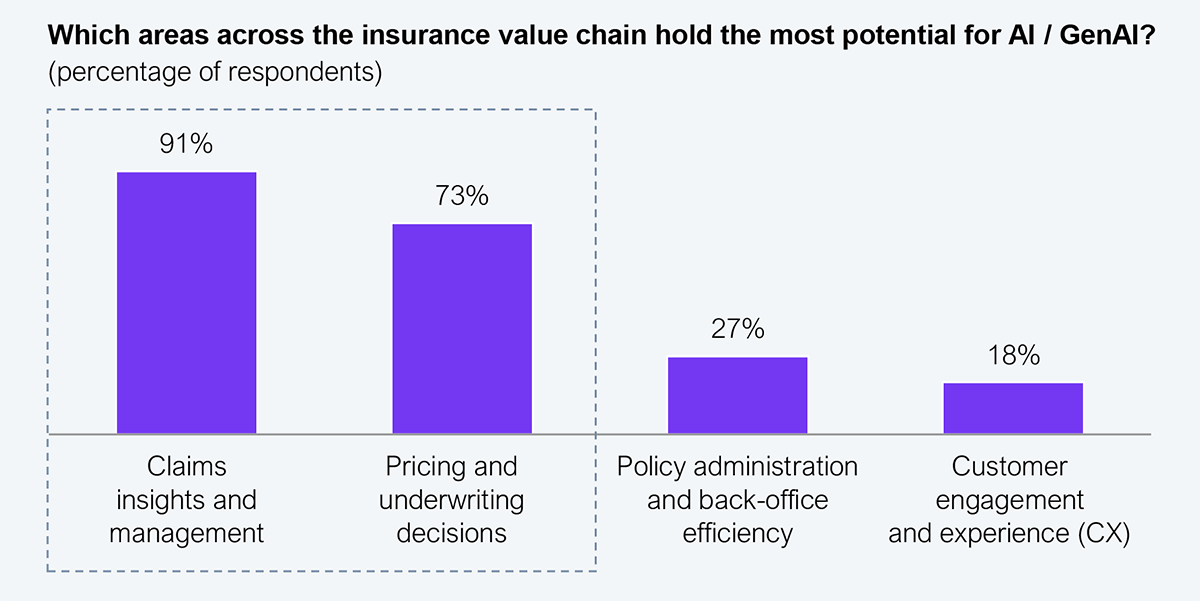

Our discussion with the delegates bears out the case for transforming AI by function. Within the fiefdom of these functions, we take a closer look at opportunities that resonated strongly (see Exhibit 2).

Source: HFS Research, 2025; insights from 17 insurance leaders in the boardroom

The rise of telematics and IoT in insurance ameliorates data collection by transforming static snapshots into real-time intelligence. In automotive, the old playbook of age, address, and credit history gives way to data on how, when, and where people drive. Claims are evolving too; video, audio, and images create a living record that reduces litigation risk, accelerates resolution, and deepens customer insight. The proliferation of this rich data fuels dynamic policies, usage-based premium models, and sharper personalization. Ultimately, those with the best data will increasingly lead in creating new sources of value. Here are a few steps to get started:

Insurance leaders who embrace such disruptive technologies are building the skills, talent, and culture to succeed, riding the wave instead of resisting it. The individuals in the room exemplified this mindset, proving that the future belongs to those who harness disruption, not fear it.

Register now for immediate access of HFS' research, data and forward looking trends.

Get Started

If you don't have an account, Register here |

Register now for immediate access of HFS' research, data and forward looking trends.

Get Started