This Market Impact Report is for CIOs, CTOs, chief operating officers, and enterprise technology leaders evaluating how to redesign operating models for Human+Machine delivery in a Services-as-Software™ world.

Most enterprises are sleepwalking into the Human+Machine era. Their operating models can’t keep up, and modernization alone won’t save them. Advances in AI, robotics, internet of things (IoT), and edge computing technologies, along with human capabilities, are propelling enterprises into the Human+Machine era faster than expected, driving real-time convergence between technology and human capability and delivering intelligence, agility, and resilience at scale.

This convergence is transforming the “adaptive enterprise” from concept to reality in organizations where people, data, physical assets, and digital intelligence coordinate into a system that responds dynamically to business needs.

For most enterprises, this shift to the Services-as-Software paradigm remains more aspiration than reality. Progress requires moving beyond an integration mindset toward a model of value orchestration by modernizing and combining disparate systems. Enterprises only realize true business outcomes when processes and data are at the center of the operating model fabric, guiding the design of technology portfolios, talent strategies, and sourcing relationships around them.

This research, based on a survey conducted by HFS and Hitachi with 505 enterprise leaders across financial services, healthcare, industrial manufacturing, energy, and consumer goods, explores what it will take for organizations to evolve into adaptive enterprises and the scale of the current readiness gap.

Enterprise leaders cannot afford to postpone this shift. Technology modernization may keep operations afloat, but it will not set enterprises apart from their competitors. Those who remain fixated on incremental upgrades will be trapped in vicious cycles of pilots.

The winners will be those who take on the harder challenge: rewiring ways of working by prioritizing processes and data, building Human+Machine operating models with embedded governance, fostering outcome-linked partnerships, and reskilling their workforce for trust and speed. These orchestrators will unlock the true power of their connected digital-physical ecosystems.

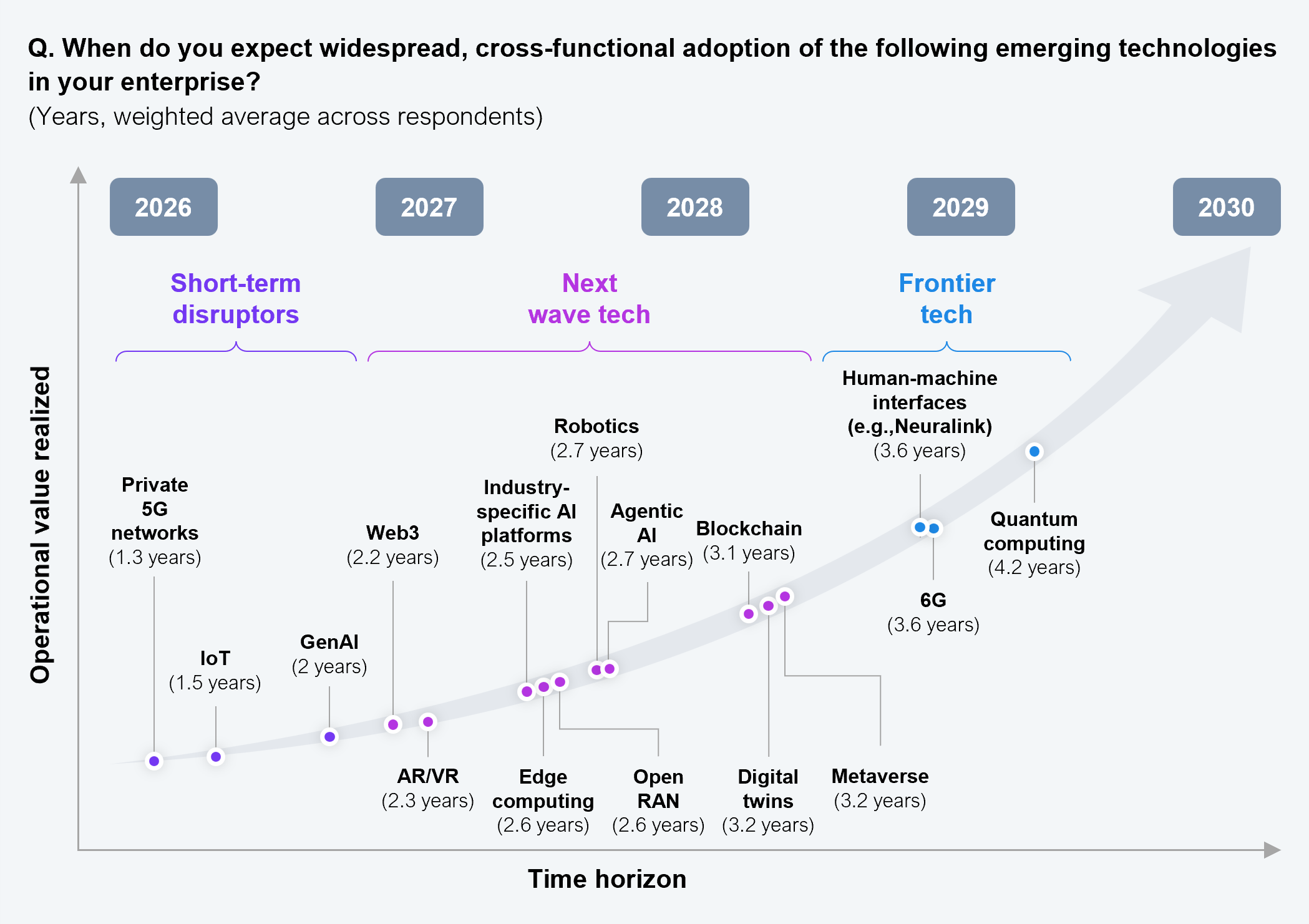

The pace of technological change has accelerated beyond expectations, forcing enterprises to rethink operating models sooner than planned. What seemed like a distant goal of integrating AI, real-time data, and physical systems into a single operating model is unfolding in real-time. Industries are scaling generative AI, private 5G, IoT, and digital twins into production at a rapid pace (Exhibit 1); enterprises no longer have the luxury of waiting years to adapt their operating models.

Based on inputs from 505 IT and business leaders with Global 2000 enterprises

Source: HFS Research, 2025

As these tools scale, they are transforming not just IT architectures but how work gets done. Enterprises are rethinking decision-making, operations, and outcome delivery. This shift is giving rise to the adaptive enterprise: an organization that unites digital intelligence, human judgment, and physical assets into a coordinated system capable of responding dynamically and delivering results in real-time. The adaptive enterprise is not a theoretical model. It is becoming the operating blueprint for leaders navigating continuous disruption.

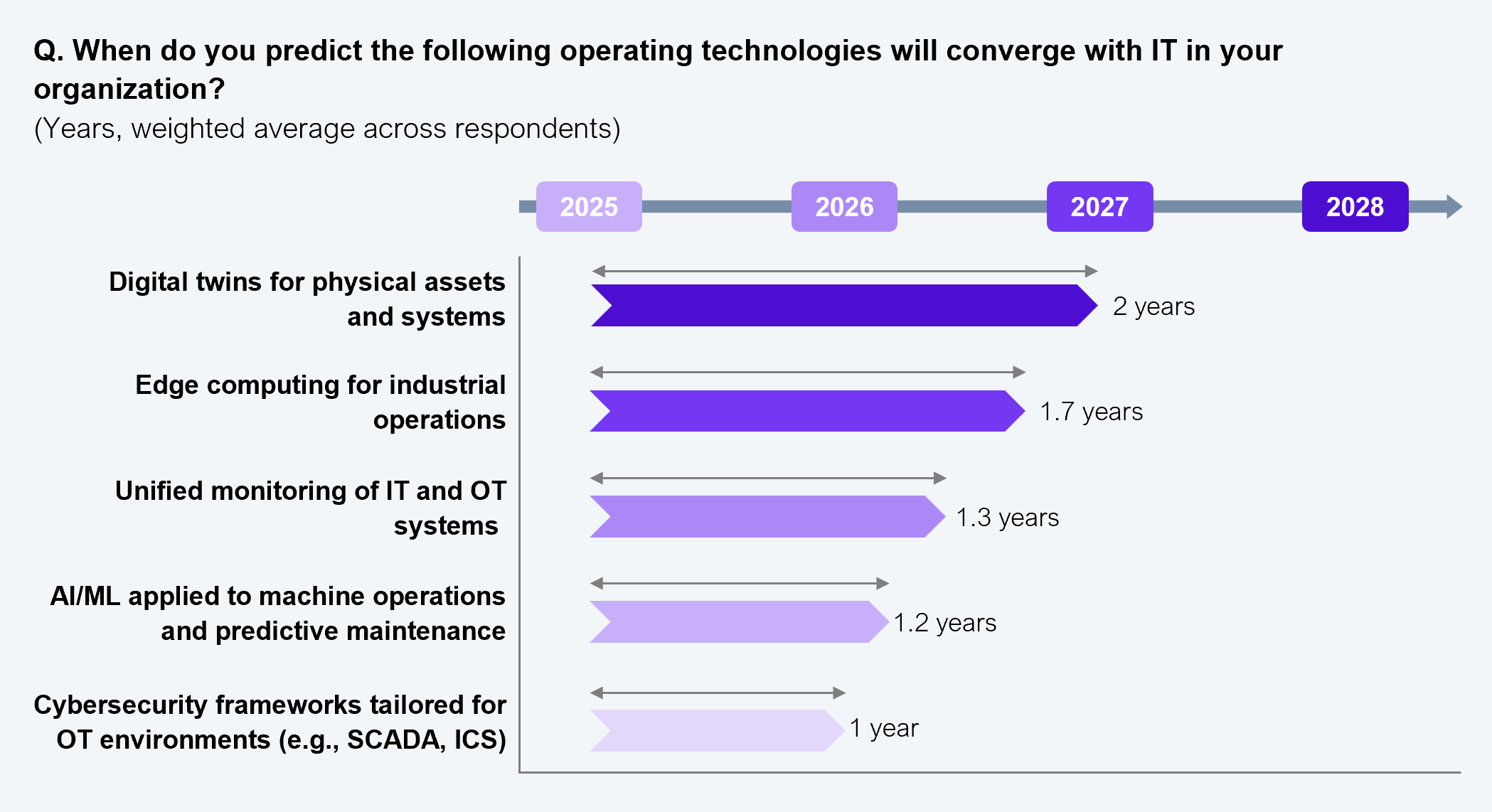

Enterprise ambitions reflect this momentum. Nearly half expect to run AI-assisted workflows at scale within the next 12 months, and more than 50% aim to achieve fully integrated digital-physical (“phygital”) operations by 2028 (Exhibit 2). These timelines reflect a growing consensus that AI, OT, and digital platforms must be closely integrated to deliver business outcomes at scale.

Based on inputs from 505 IT and business leaders with Global 2000 enterprises

Source: HFS Research, 2025

To operationalize adaptive models, early movers in several industries are redesigning core functions to orchestrate intelligence, assets, and people in real-time.

In these examples, what distinguishes the leaders is not the technology stack, but their ability to orchestrate digital systems and physical assets into coordinated, intelligent workflows.

AI value is unlocked only when IT and OT systems talk to each other—digital twins and predictive maintenance need real-time orchestration across layers.

— CTO, global industrial manufacturer

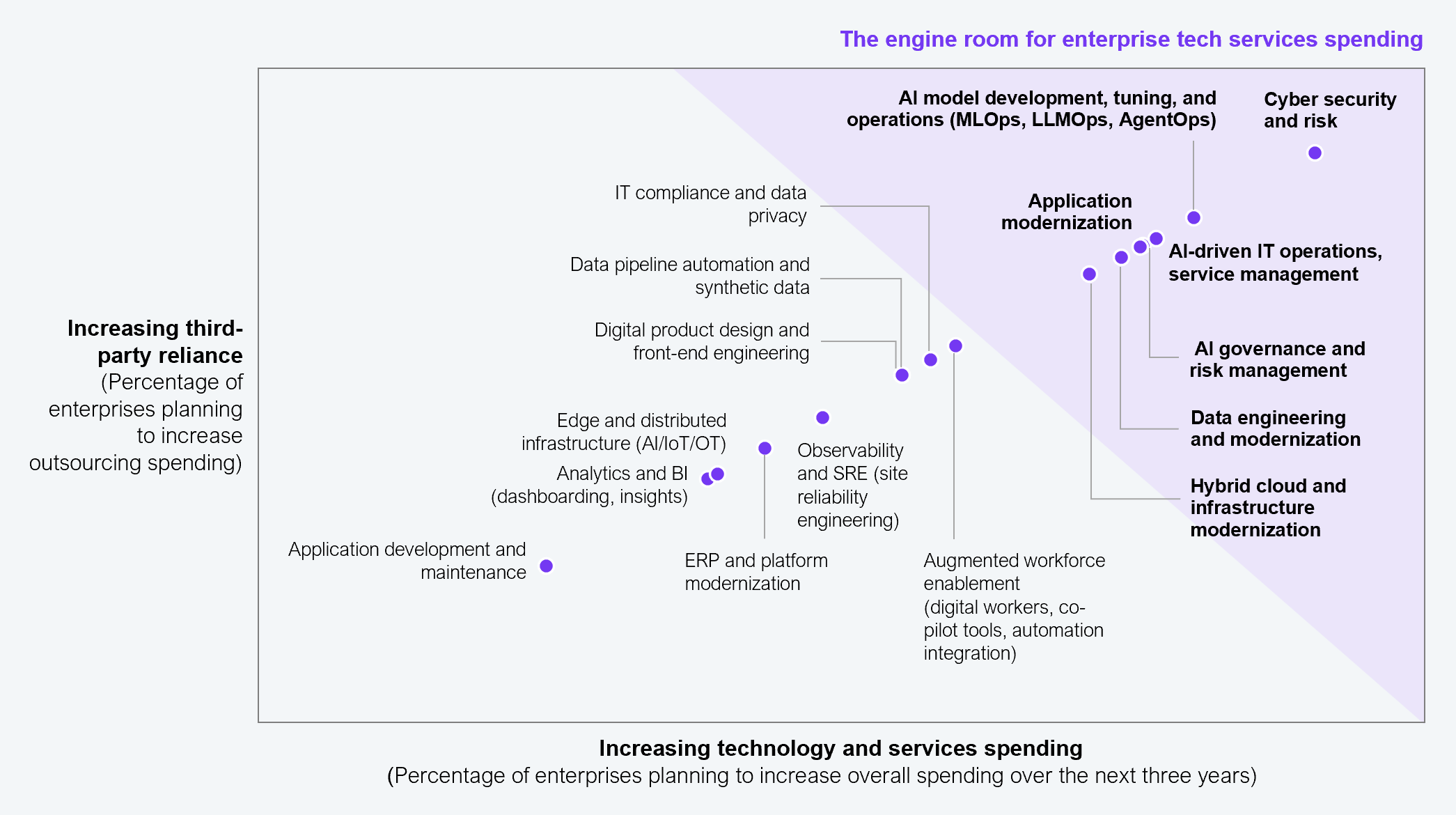

Convergence is not a systems upgrade; it is a decisive competitive factor, hardwiring processes, workflows, resilience, and business outcomes into transformation roadmaps, using IT, OT, and AI as enablers. To this end, enterprises are investing in unified monitoring, cyber-resilient edge infrastructure, and real-time AI-driven insights as core to operations (Exhibit 3).

In this scenario, AI acts as the connective tissue linking people, data, and machines across the stack. By embedding intelligence at the point of service delivery, AI enables faster decisions, smarter risk management, and greater visibility across functions. As AI transitions from pilot projects to embedded systems, it is redefining how enterprises measure performance and deliver value.

Based on inputs from 505 IT and business leaders with Global 2000 enterprises

Source: HFS Research, 2025

These operating shifts directly influence how enterprises structure and consume technology services. Modernization has become the baseline, not the goal. The focus is moving to service capabilities that deliver intelligence, speed, and resilience across the stack.

Over the next three years, the biggest increases in demand will be for cybersecurity and risk management (71%), AI model development and tuning (63%), and AI-enabled IT operations (61%). Data engineering and cloud modernization remain critical enablers of these priorities (Exhibit 4).

Enterprises are rebuilding their technology services as adaptive platforms that power Human+Machine operations, with security, AI, and data at their core. Simultaneously, sourcing strategies are shifting. More than half of enterprises expect to increase reliance on third-party partners for cybersecurity and risk, with AI development, tuning, governance, and operations close behind. Demand for external expertise in data engineering, hybrid cloud, and application modernization also remains strong. These services will be foundational to building adaptive enterprises.

Based on inputs from 505 IT and business leaders with Global 2000 enterprises

Source: HFS Research, 2025

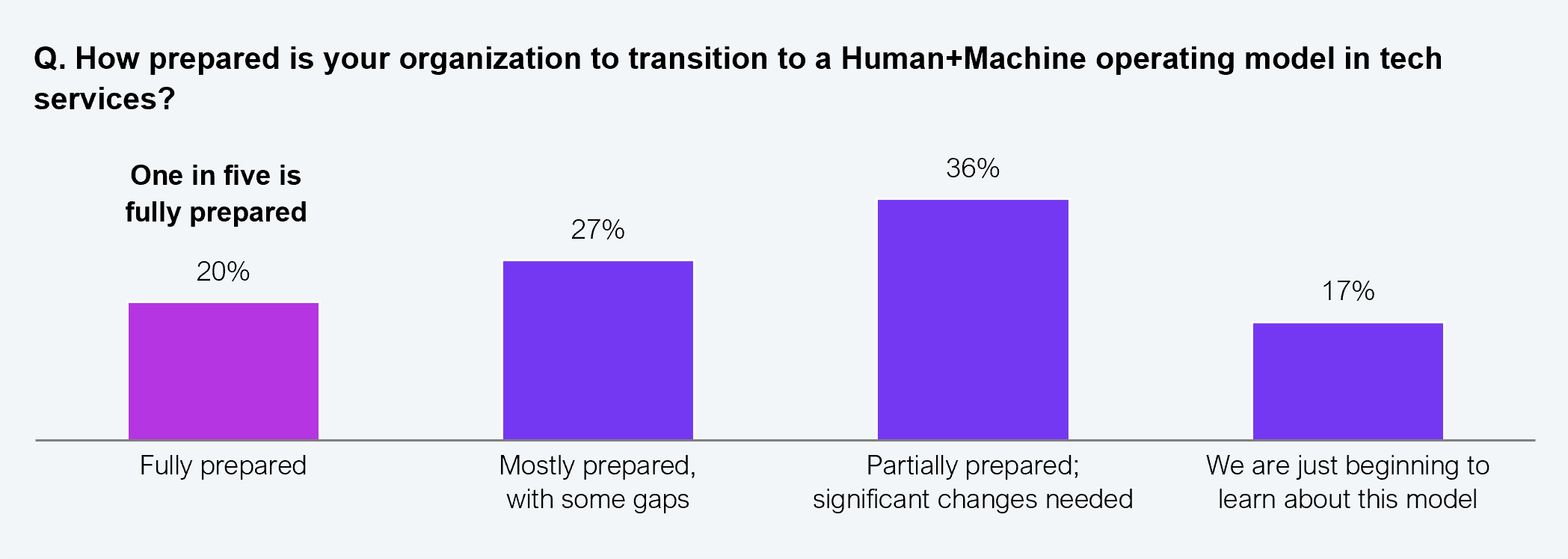

While the move to the Human+Machine is now an enterprise imperative, readiness lags far behind ambition. Only one in five enterprises feels fully prepared, and over half admit they are still exploring or only partially ready for this transition (Exhibit 5). Evidently, the gap between technology adoption and operating model maturity is stark.

Sample: 505 IT and business leaders with Global 2000 enterprises

Source: HFS Research, 2025

The possibility for unlocking AI in the business is very high, but it depends entirely on how well we treat data as a business asset and integrate it into intelligent workflows.

— CTO, investment banking firm

Enterprises cannot close this readiness gap solely through platform upgrades. Infrastructure modernization is necessary, but not sufficient. Real progress comes from reimagining workflows, redesigning data pipelines, and integrating governance into systems that operate in real-time.

In industrial, energy, and mobility environments, the vast untapped potential to be realized through IT–OT convergence makes the urgency to pivot sharper. Predictive maintenance, digital twins, and unified security create value only when embedded within a coordinated framework that fuses digital and physical layers. Without this, convergence remains a technology investment rather than a performance driver.

Achieving this requires action across every layer of the operating model:

We’re all-in on AI, but the real challenge is less about technology and more about integrating AI outputs into legacy processes and workflows.

— IT leader, healthcare enterprise

AI thrives in environments where data and expertise flow freely. It’s forcing us to flatten hierarchies, build cross-functional teams, and rethink decision-making.

— Business executive, insurance and financial services

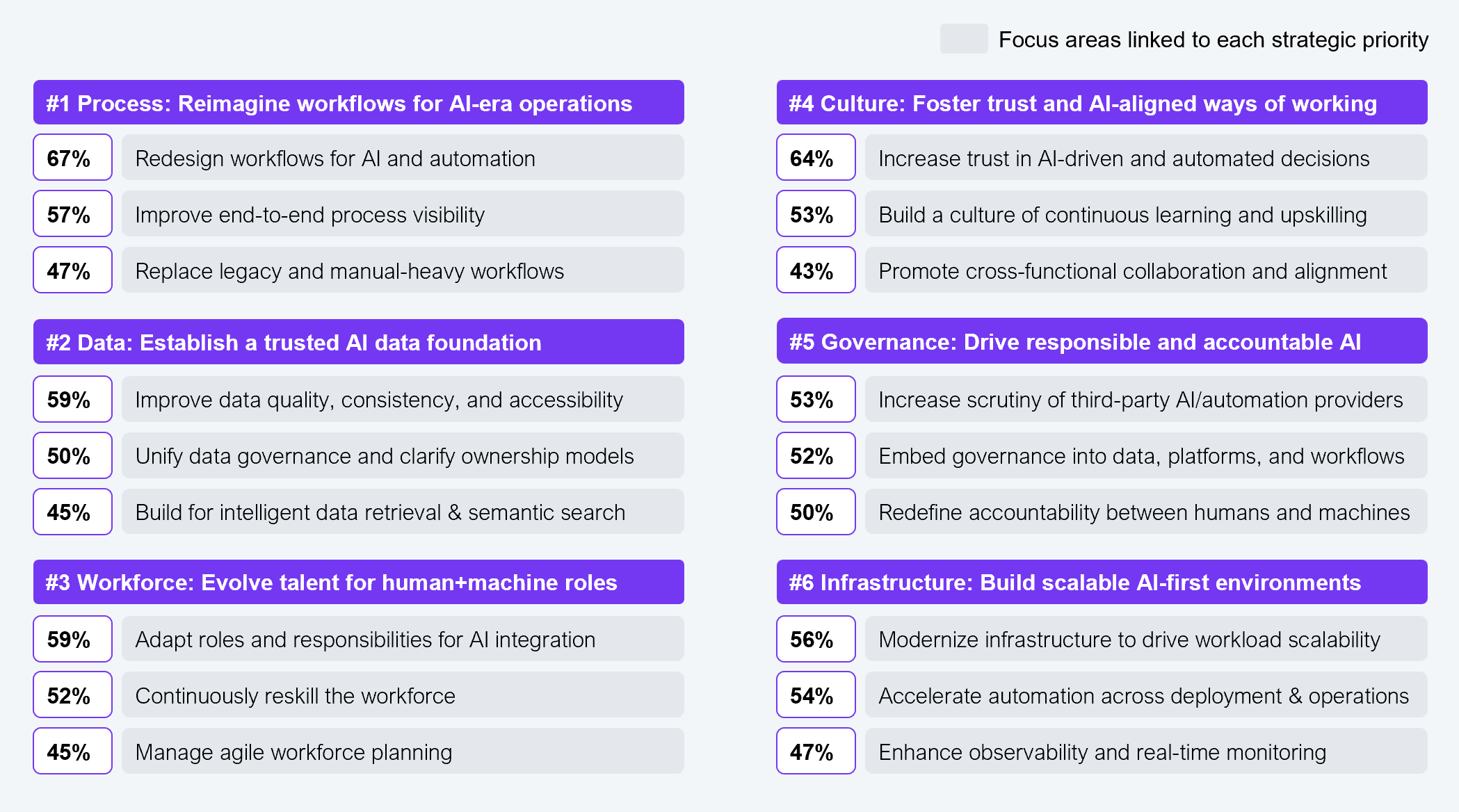

The evidence suggests that the readiness gap is not about technology availability but about operating model design. Closing these gaps requires more than modernization projects. Enterprises must undertake the complex yet inevitable rewiring of the enterprise fabric, which requires coordinated progress across six interconnected fronts: processes, data, workforce, culture, governance, and infrastructure (Exhibit 6).

Sample: 505 IT and business leaders with Global 2000 enterprises

Source: HFS Research, 2025

AI adoption in manufacturing is as much about retraining people and rethinking processes as it is about deploying advanced robotics or analytics.

— Plant innovation leader, automotive manufacturing

The readiness gap is not a question of technology availability but of operating model design. Enterprises repeatedly cite processes and data as the primary obstacles to Human+Machine delivery (Exhibit 7). Siloed workflows, fragmented ownership, and manual handoffs prevent AI and emerging technologies from operating in context and stop enterprises from functioning as orchestrated systems.

Sample: 505 IT and business leaders with Global 2000 enterprises

Source: HFS Research, 2025

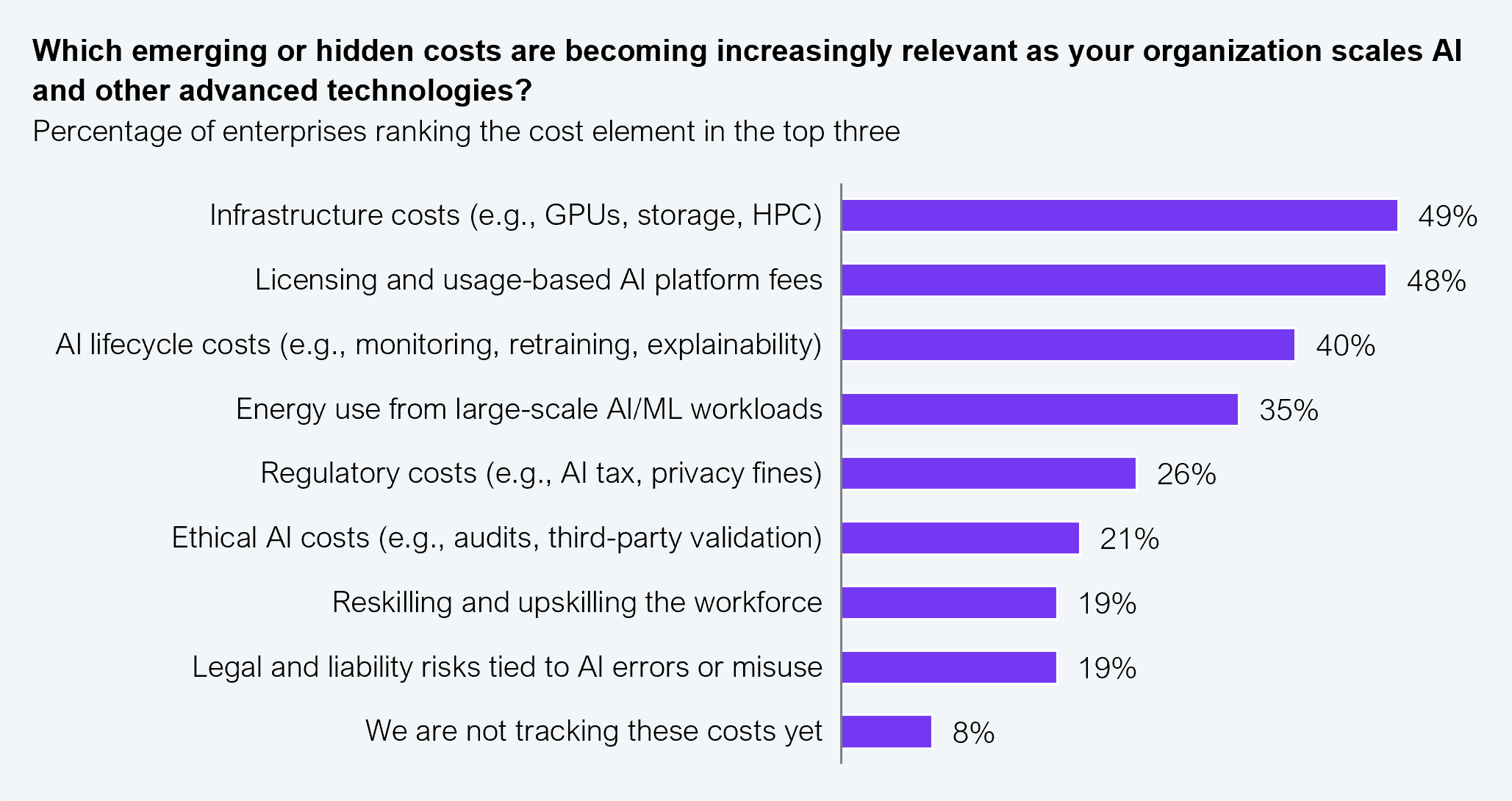

Enterprises that fail to factor in these hidden costs risk underestimating the true investment required to scale Human+Machine delivery. Enterprises must go beyond tech spend to plan for the long-term costs of explainability, governance, and workforce adaptation

(Exhibit 8).

Sample: 505 IT and business leaders with Global 2000 enterprises

Source: HFS Research, 2025

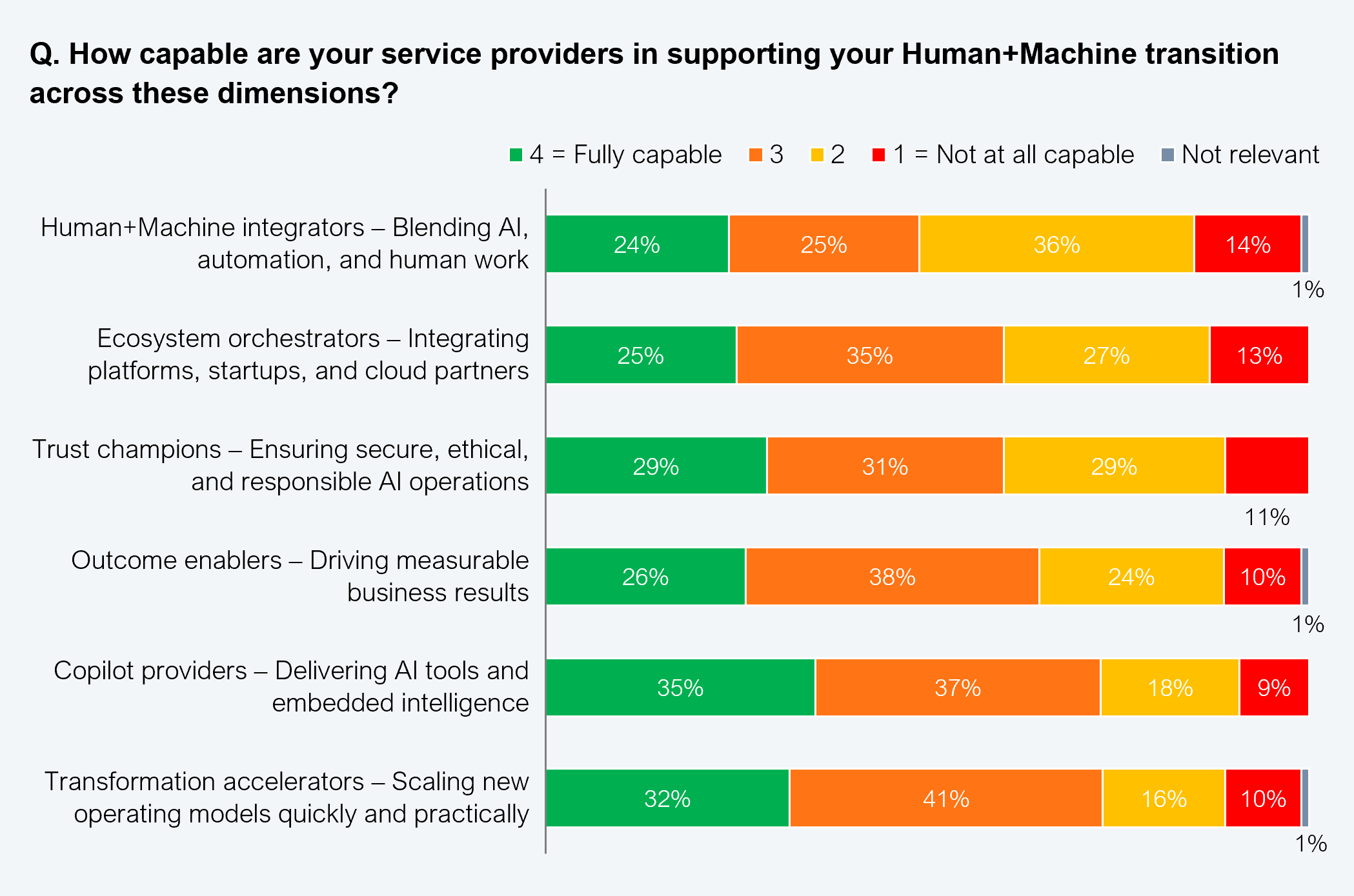

The Human+Machine era is forcing a reset in how enterprises evaluate and manage their partners. Basic integration, staff augmentation, and platform upgrades are no longer enough. Enterprises need partners who act as value orchestrators, helping to bridge IT, OT, data, and AI into coordinated systems that deliver measurable business outcomes.

Yet fewer than one-third of enterprises believe their current providers are ready to support this shift (Exhibit 9). This trust gap underscores the urgency for new sourcing models and new provider capabilities that transcend traditional system integration chops.

Sample: 505 IT and business leaders with Global 2000 enterprises

Source: HFS Research, 2025

Enterprises can no longer reward modernization for its own sake. To deliver impact, providers must demonstrate true full-stack capability, spanning infrastructure and OT platforms, data pipelines, and AI models, all the way through to business workflows. For enterprise leaders, this means raising the bar on partner selection.

Advisory on AI-first operating models, platform-based delivery assets, and real-time orchestration must be mandatory. Simply offering tools or generic consulting will no longer be sufficient. Winning partners will combine domain expertise with AI-enabled orchestration to create integrated “performance fabrics” that deliver outcomes (Exhibit 10).

Sample: 505 IT and business leaders with Global 2000 enterprises

Source: HFS Research, 2025

Vendors talk about full-stack, but unless they can integrate domain workflows, physical systems, and AI-driven data orchestration, they’re not delivering outcomes.

— Head of Automation, financial services

The companies that win will be those that combine AI with ecosystem partnerships and hyper-personalization, not just automation.

— BU Head, retail and consumer products

One-off advisory engagements are no longer relevant in an era where transformation must be continuous. Enterprises now expect consulting partners to bridge strategy with execution by remaining embedded throughout the transformation and adoption journey. Over half (56%) prefer specialized providers with deep expertise in workflows, AI, and integration, while nearly half (46%) want platform players that can combine scalable tools with strategic guidance.

Enterprise leaders should judge providers on more than their technical fluency; providers should be able to

The most effective consulting partners will not only advise but co-create outcomes continuously, combining domain knowledge, full-stack coverage, and design-led approaches to deliver measurable value.

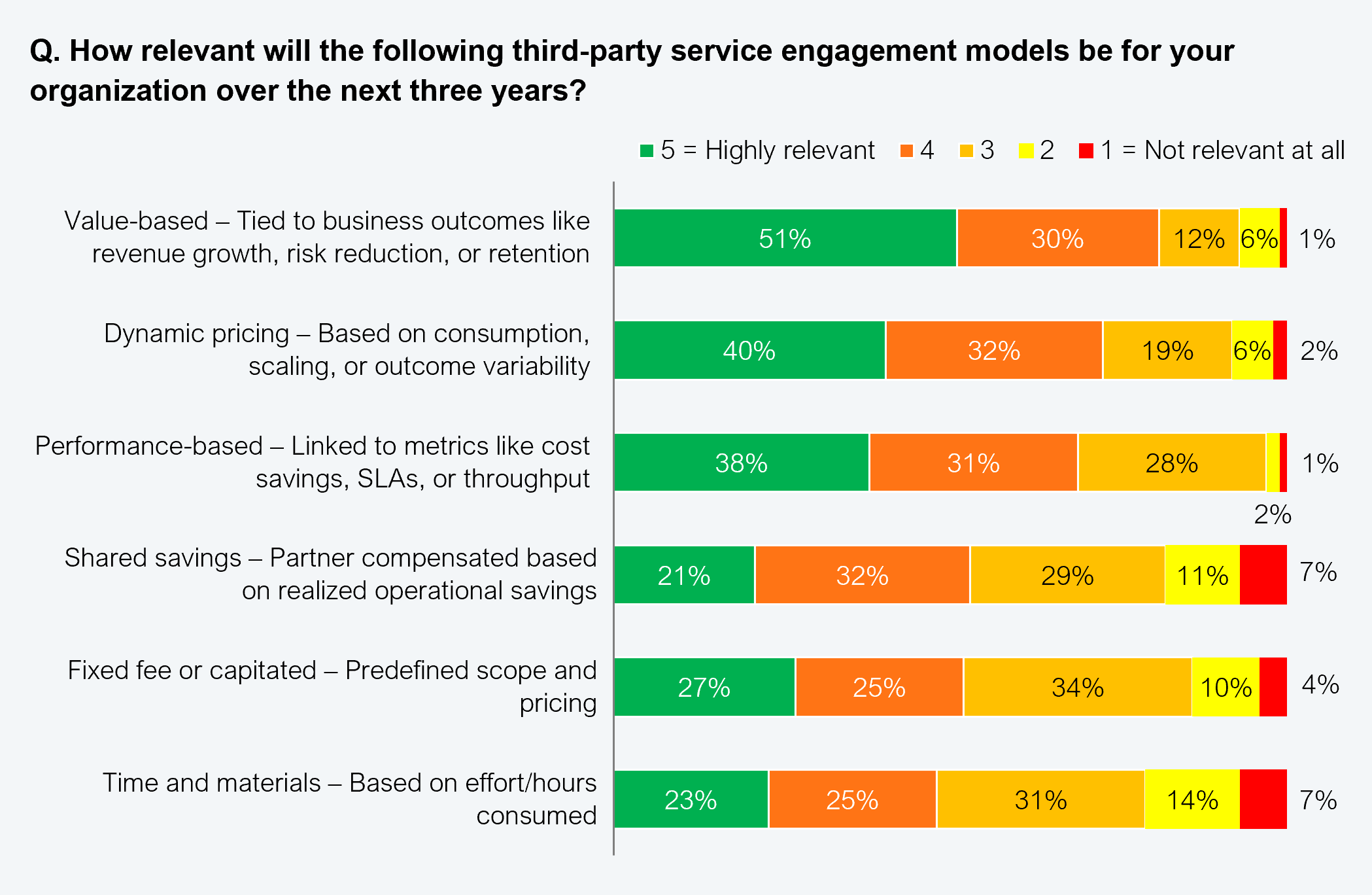

The provider model is evolving, but enterprises must evolve with it. More than half now view value-based contracts that link fees to revenue gains, risk mitigation, or cost savings as highly relevant (Exhibit 11). Traditional time-and-materials models are steadily giving way to performance-linked pricing and consumption-based structures that reflect the adaptive, always-on nature of modern services.

Sample: 505 IT and business leaders with Global 2000 enterprises

Source: HFS Research, 2025

To make this shift viable, pricing must be tied to real-time performance metrics such as throughput, adoption, or resilience. AI and autonomous systems now make it possible to generate and track such precise metrics. This convergence makes outcome-linked contracting viable at scale in a way it wasn’t a decade ago.

Buying AI is no longer just about licensing. It’s about gain-sharing, proving outcomes, and making sure the savings justify the complexity.

— IT leader, industrial manufacturing

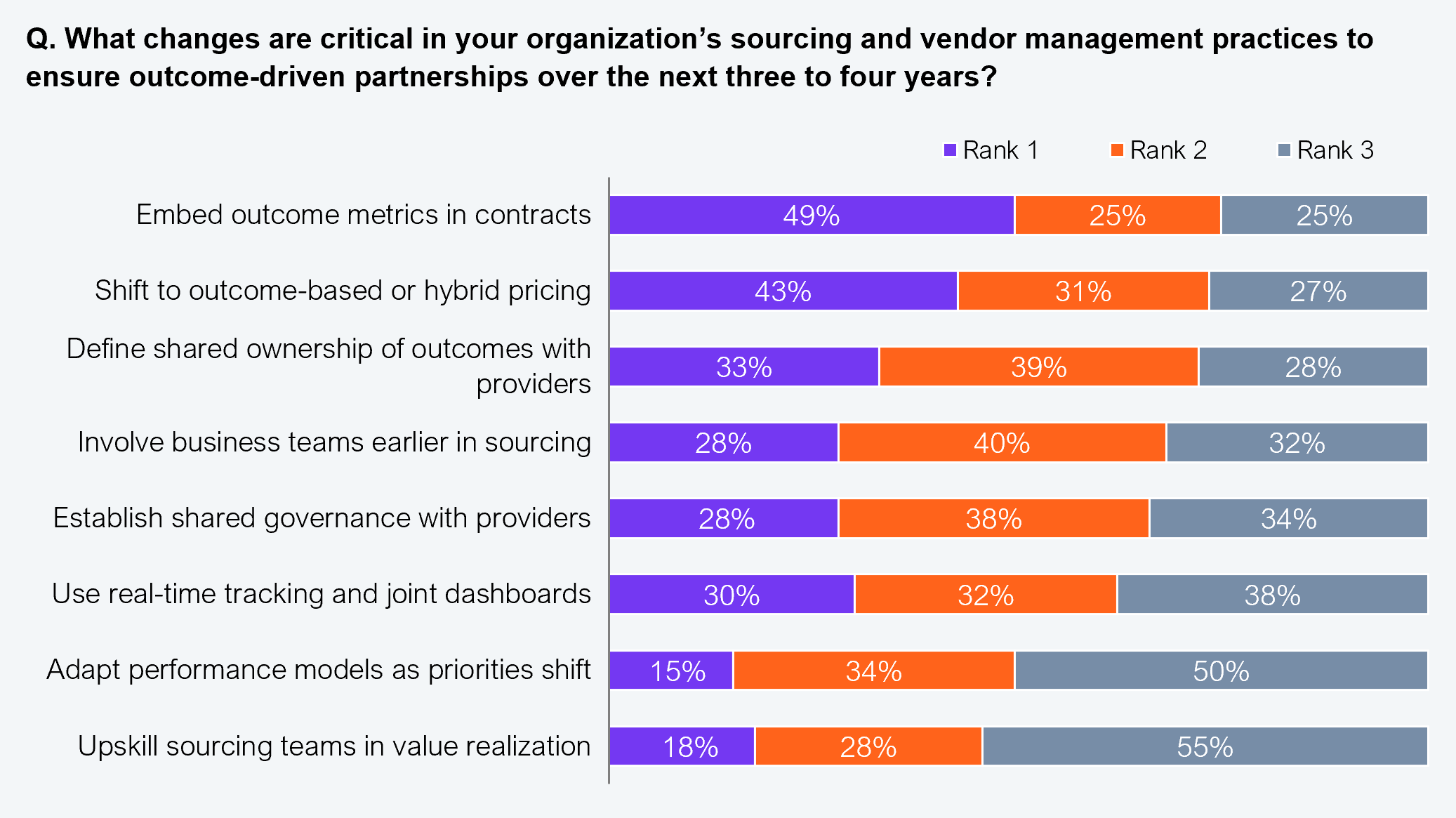

For value-linked partnerships to succeed, enterprises must rewire sourcing and vendor management practices:

Procurement leaders who once prioritized cost and inputs must now prioritize outcomes and impact, acting as orchestrators rather than transaction managers.

These shifts will give enterprises the leverage to demand continuous innovation and ensure providers adapt to evolving priorities (Exhibit 12).

Sample: 505 IT and business leaders with Global 2000 enterprises

Source: HFS Research, 2025

The real winners will be those who can combine AI, IoT, edge, and all other emerging tech with process redesign, data trust, and ecosystem partnerships to drive measurable business outcomes.

— Business leader, retail and consumer goods

The Human+Machine era has arrived, marking a new operating reality. Enterprises that treat AI, data, and emerging tech as bolt-ons will fall into cycles of failed pilots, rising costs, and eroding customer trust.

To lead in the Services-as-Software era, enterprises must

Modernization may keep enterprises afloat, but orchestration will determine who leads. The future belongs to those who turn convergence into resilience, speed, and growth at scale.

Register now for immediate access of HFS' research, data and forward looking trends.

Get Started

If you don't have an account, Register here |

With the exception of our Horizons reports, most of our research is available for free on our website. Sign up for a free account and start realizing the power of insights now.

Our premium subscription gives enterprise clients access to our complete library of proprietary research, direct access to our industry analysts, and other benefits.

Contact us at [email protected] for more information on premium access.