Platform vendors are scaling their agentic AI capabilities faster than enterprises can absorb, making it tough for CIOs to keep up with the pace of innovation. This makes the implementation partner decision even more critical to prepare them for the vendor innovation curve, not just deploy the technology.

However, most CIOs continue to shortlist service providers using rate cards, certifications, and case studies. They must start asking whether their global system integrators (GSIs) have a seat at the product table with SAP, AWS, Salesforce, or other platform vendors. If the answer is no, they are buying a structurally weaker strategic position for the life of that platform.

A GSI’s tier status or executive relationship with a platform vendor no longer translates into product influence. SAP, AWS, Salesforce, and others have fundamentally changed what earns roadmap access. In our 100-plus interactions with platform vendors last year, we found that resell velocity isn’t the main indicator of a partnership’s success anymore. Vendors now prioritize partners that bring structured evidence across multi-client proof of repeatable architecture patterns, quantified operational impact, and AI-scale deployment data.

This shift has a direct consequence for enterprise buyers. When their GSIs lack a systematic mechanism to convert delivery insights into product feedback, they pay the price in three ways:

This, in turn, raises two questions that every CIO must ask their GSI:

GSIs are federated enterprises, organized by industry vertical, geography, and service line, with each unit optimized for client P&L ownership and delivery scale. This architecture was always there to help them track revenue and cross-service line conflicts better. However, this often doesn’t translate the patterns seen across industries/geographies into actionable insights for either the platform partner or their internal IP/product team.

Escalations remain account specific and are deprioritized by vendor product managers because cross-client signal is what moves roadmap priority. For instance, a SAP migration insight from a pharma engagement in Germany does not make it to the product team, or a clean-core pattern cracked in a financial services deployment in Singapore becomes a bespoke asset that never gets reused. This broken feedback loop is also the reason why most products/industry IP built by service providers have very few takers, and clients have zero or no recall of these solutions.

The ecosystem is already shifting. Boutique AI-native specialists and independent software vendors (ISVs) are filling the roadmap influence gap that federated GSIs leave open. With enterprise platform vendors actively de-prioritizing the alliance tier status in favor of engineering-led partnerships, the structural penalty for selecting a GSI without product influence will compound over time and result in unused product modules, delayed access to new capabilities, reduced co-investment access, and renewal negotiations where GSIs can’t advocate for platform roadmap needs. The critical moment to address this risk is during partner selection before the relationship hardens.

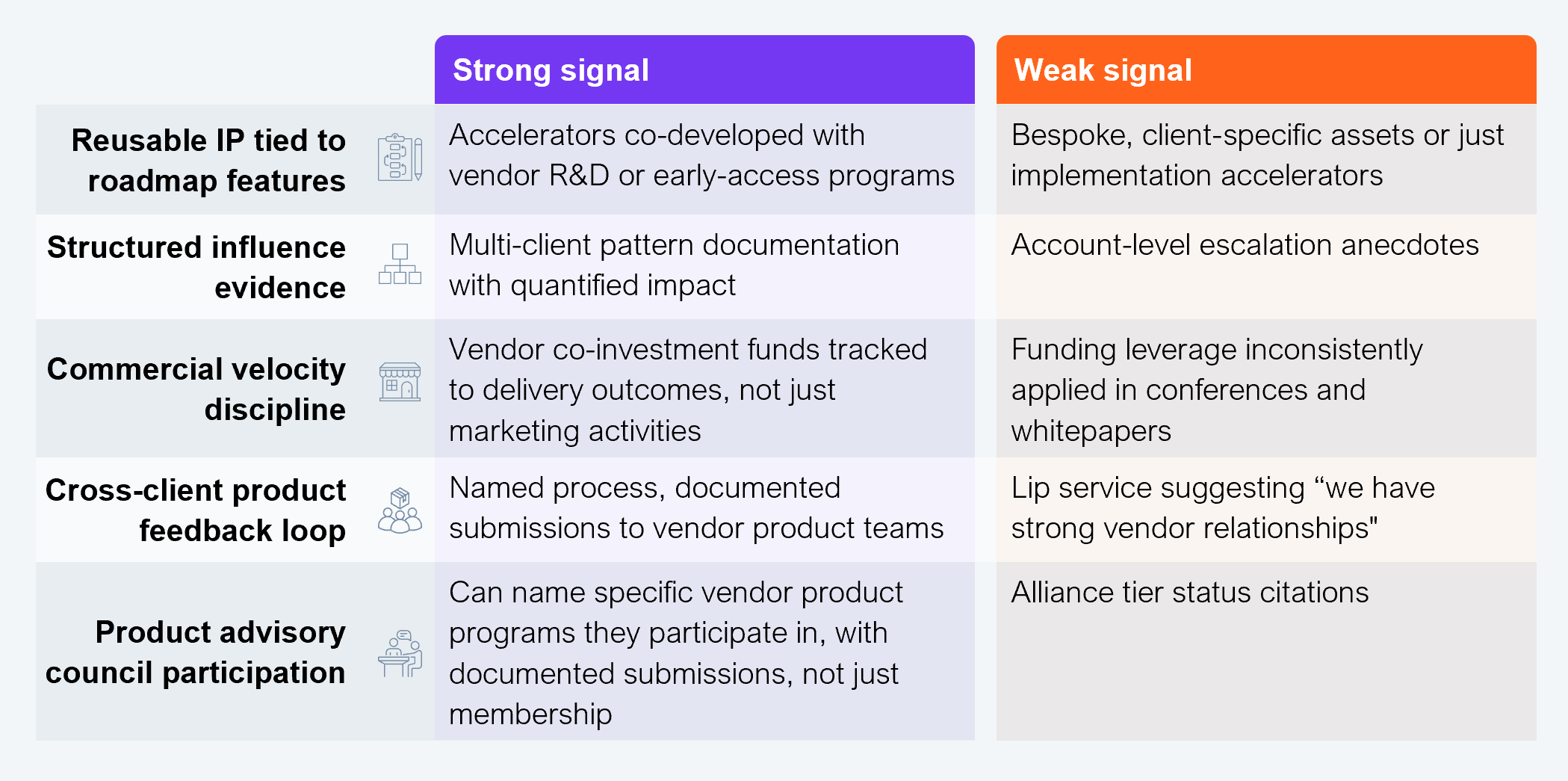

However, expecting a GSI to have deep roadmap access across the platform vendor’s entire portfolio is unrealistic. Platform ecosystems are too large and too specialized for that. Enterprises should instead evaluate whether their GSIs have targeted product influence in platform domains that matter most to their transformation. The following exhibit lays out an evaluation framework to help enterprises validate the roadmap access in specific domains:

Source: HFS Research, 2026

CIOs should ask their GSIs three questions that separate those signals from noise:

While the speed of platform innovation has increased multi-fold over the years, enterprises are stuck in technical debt because their implementation partner is too slow to keep up with the platform vendor’s speed. Assessing the influence of the service provider on the vendor’s roadmap for the products that are central to transformation needs can help CIOs build long-term strategic advantage by staying ahead of the innovation curve.

Register now for immediate access of HFS' research, data and forward looking trends.

Get StartedIf you don't have an account, Register here |

With the exception of our Horizons reports, most of our research is available for free on our website. Sign up for a free account and start realizing the power of insights now.

Our premium subscription gives enterprise clients access to our complete library of proprietary research, direct access to our industry analysts, and other benefits.

Contact us at [email protected] for more information on premium access.