This Point of View is for service provider leaders, enterprise services buyers, and industry observers evaluating how Accenture’s persona-led Reinvention Services unifies strategy, technology, and operations at scale.

I spent one week with Accenture leadership; here is what I took away.

When ChatGPT launched in 2022, Accenture had 30 people working on GenAI, generating less than $1 million in revenue. Since then, Accenture has booked $5 billion in AI revenue and $12 billion in AI sales. Accenture employs 800,000 people, but it is not afraid to reinvent itself.

I spent the better part of last week with Accenture leadership learning about Accenture Reinvention Services. What is it and what does it mean for clients?

Accenture Reinvention Services is the HFS OneOffice in action

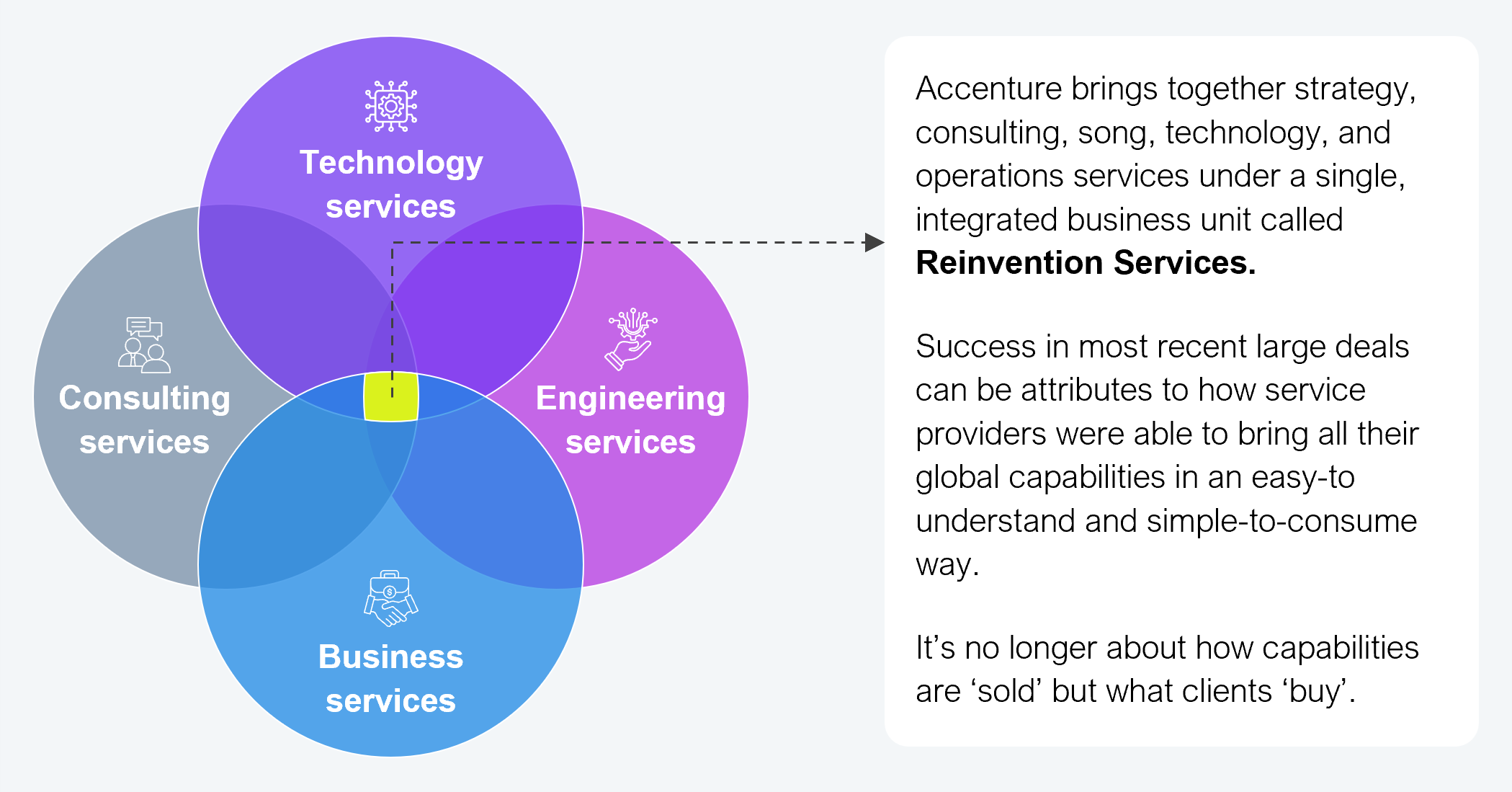

HFS has long argued that how clients buy is more important than how capabilities are sold. Yet, IT and BPO service providers have spent decades organizing themselves by capability: consulting, technology services, and BPO. They go to market by practice and sell by tower.

Accenture is changing all of it by betting that the answer is to go to market by persona, not by capability. Seven personas, to be precise, each anchored to a buyer domain: CEO (industry and enterprise), CISO (cybersecurity), CTO/ CIO (digital core), CFO (finance), CMO (Song), CSCO (supply chain and engineering), and CHRO (talent).

The Big 4 offer strategy but lack the scale to deliver. Leading ITO and BPO providers have strong delivery capabilities but lack consulting. Accenture is the only provider that brings strategy and execution at scale, and by bringing them together, Accenture’s Reinvention Services showcase its differentiation.

Exhibit 1: Accenture Reinvention Services accelerates the “OneAccenture” service experience

Source: Accenture, 2026

Case in point: Accenture Reinvention Services for CFO

Here’s how Accenture’s full stack comes together for a CFO:

- Accenture earns the right to go deeper via finance transformation strategy, operating model design, cost-to-serve analysis, and the business case for change.

- Before it touches a single process, Accenture builds a computational twin of the finance function. This digital replica models the current state, simulates transformation scenarios, and stress-tests outcomes before any real-world change. The CFO can see the future of their function before committing to it.

- Skills are dynamic, not static. The finance analyst of 2030 will look nothing like the finance analyst of today. Accenture runs simulation models to keep a live pulse on work changes, new skills needed, workflows to build or adapt, new capabilities, and how to close the skills gap at speed.

- Strategy becomes operational reality. Accenture applies AI-powered orchestration of people, data, and technology across the finance function via intelligent workflows, continuous monitoring, and real-time insights. It’s a permanently running operating system for finance.

- Agentic AI outcomes are present across every major finance process:

- Order-to-Cash: AI agents manage credit, billing, collections, and cash application with faster cycle times, lower DSO, and higher recovery rates.

- Procure-to-Pay: AI agents handle intelligent procurement, invoice processing, and payment execution. Compliance is built in, and exception handling is automated.

- Record-to-Report: AI agents take care of automated close, reconciliation, and reporting. Months are compressed to days, and audit trails are embedded.

- Financial planning and analysis: AI drives forecasting, scenario modeling, and variance analysis. The CFO’s office becomes genuinely forward looking.

The result is a permanently adaptive finance function, priced on results, with strategy, digital intelligence, workforce, operations, and AI agents fused into a single, continuously delivered outcome.

Scale is Accenture’s most cited advantage, but most people stop at headcount

Accenture’s 800,000 people show real scale, but the more interesting scale story is told in everything else:

- Scale of C-suite relationships: Relationships aren’t just with the CIO. They extend to the CFO, COO, and CEO, across industries, geographies, and business functions. Accenture can influence, not just participate.

- Scale of M&A. Accenture deployed nearly $6 billion in fiscal year 2025, averaging more than 30 acquisitions a year for five straight years. What’s even more impressive is its ability to integrate. For instance, Faculty’s former CEO is now Accenture’s CTO—you don’t hand your technology leadership to someone you just bought unless you are betting the strategy on what they bring.

- Scale of the ecosystem. Accenture has 2,000 people trained on Palantir, and deep integrations with OpenAI, Anthropic, Google, Microsoft, and others. Its ecosystem is not logos on a slide; it is co-engineered solutions, joint go-to-market, and shared revenue at a scale that makes Accenture the default partner of choice for every major technology platform trying to reach the enterprise.

Accenture’s bet builds on top of its core to unlock revenue pools the industry has never touched

Accenture’s bet is to unlock revenue pools the industry hasn’t touched. The platform for that bet is a core that is gaining share, not under pressure. Revenue has nearly tripled over 16 years. The 10-year CAGR is about 8%. FY25 grew 7% to nearly $70 billion. H1 FY26 delivered $43 billion in new bookings, with Q2 a record. From that base, Accenture’s answer is to go after much bigger bets:

- Industry core operations, in addition to CIO and enterprise functions. The services industry has historically accounted for 15%–20% of enterprise spend, covering IT, support functions, and the back office. Clinical operations, manufacturing lines, trading floors, and capital project delivery remained largely out of reach, considered too complex, too integrated, and too hard to crack with a capability-organized model. Accenture is going after this bet directly with a model organized by domain, not capability, via acquisitions targeting capital projects in energy, utilities, aerospace, and defense, and through partnerships with AWS and others on agentic AI that automates whole processes. GenAI is driving change across nuclear power plants, power grids, rolling stock, and defense systems.

- Services to products plus services. This is the non-linear bet; services revenue scales with people. Product revenue scales with adoption. Accenture is building and acquiring codified IP, proprietary platforms, and domain-specific products that it can deploy repeatedly without proportional headcount growth. Frontier, Faculty’s decision intelligence platform with a computational twin for clinical trials, is the clearest example. Every product that ships further proves Accenture can generate revenue that does not look like traditional services.

- FTE to IP and outcomes. About 60% of work is fixed price today, with an expanding share tied to productivity, cycle time, and business KPIs. AI compresses effort and timelines, and pricing follows. The asset base makes commitments to value, not effort, credible.

Now comes the difficult bit…

- AI pricing is broken, and Accenture needs to fix it. AI tokenomics is complicated. If Accenture wants to lead the next category, it needs to define the model for AI pricing that is simple to understand and easy to consume, not just for itself, but for the industry.

- The SaaS displacement dilemma. With Services-as-Software™, software can eat services and services can eat software. Accenture has the IP, the domain, and the delivery scale to play offense here. But they also have deep relationships with almost every major technology platform—SAP, Salesforce, Oracle, Microsoft, and Google. How will Accenture manage its ecosystem of partners that remain critical to its growth strategy? That tension does not have an easy answer, but it needs one.

- Incentive alignment. Reinvention is a cultural change as much as it is a structural one. Getting people to sell and deliver differently is not a reorganization problem; it is a behavior change problem. Compensation structures, promotion criteria, and account incentives need to align and communicate, “We incent you to pass the ball, not only score the goal.”

- The market buys have not kept up. AI capabilities are improving at a ridiculous speed. Every quarter looks different from the last. And yet most enterprise clients are still buying services using 1990s procurement infrastructure, with dog-and-pony shows and a timeline of six to eight months to select a provider. By the time a contract is signed, the AI landscape has moved twice. Accenture has the responsibility not only to sell reinvention services but also to influence how the market buys.

- Competition is not sitting idle. Scale is an advantage, and so is the lack of scale. Smaller players move faster and price more aggressively. They make commercial bets that a $70 billion firm with existing client relationships and partner ecosystems to protect simply cannot. Boutique AI-native firms are already winning deals on speed and simplicity that Accenture could own. The reinvention window is real. But it is not exclusive.

The big picture shows that Accenture is betting on the Jevons Paradox to become a reality

Jevons claimed that when technology makes a resource cheaper and more efficient, total consumption of that resource goes up, not down. It happened with steam engines. It happened with electricity. Will it happen with AI?

Accenture is betting its reinvention strategy on Jevons being right, that AI efficiency unlocks demand at a scale the industry has never seen. The winners won’t be the ones who cut the most costs with AI, but the ones who use AI to go after problems they could never touch before. But it is going big and with conviction, making real bets at real scale with real money. It expects $5 billion in acquisitions this year, a SpaceX-launched satellite, and a decision intelligence platform for clinical trials. These are not incremental moves.

The question for Accenture is, “Can you reinvent your clients faster than AI reinvents your business model?” For now, Accenture seems ahead of that curve.