This HFS Highlight on the Infosys acquisition of Optimum Healthcare IT is for IT services strategists, healthcare provider technology leaders, and competitive intelligence teams evaluating how the deal reshapes provider-market positioning in the AI era.

AI is compressing effort and commoditizing generic delivery. The firms that will lead the next decade are the ones that own irreplaceable industry expertise, can deliver at scale inside complex environments, and can wrap that depth in AI to change the economics of what their clients do. Infosys just made a significant move in that direction. Its $459 million acquisition of Optimum Healthcare IT is a clear-eyed profit x execution bet. The logic is sound, but the question is whether Infosys can turn it into a strong foundation for a category-defining position.

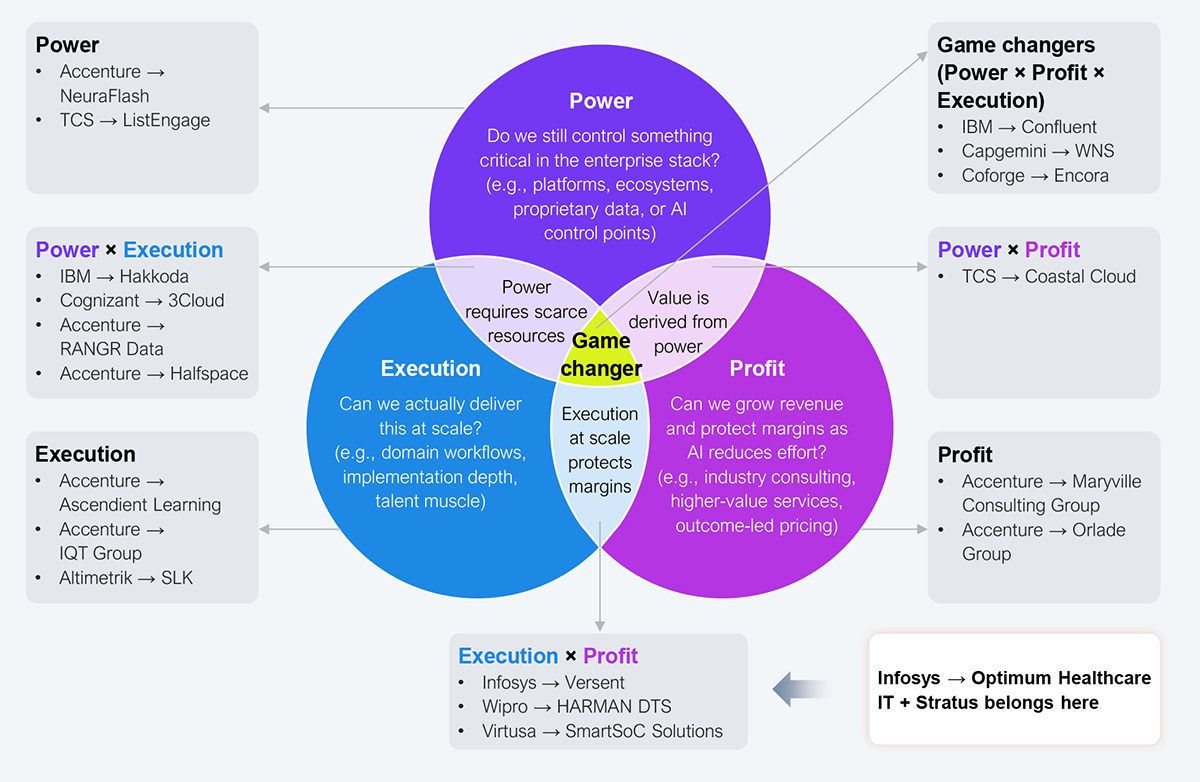

Every acquisition is really answering one of three questions.

The most valuable acquisitions sit at the intersection of two or three of these. Profit x execution is particularly important right now because AI is doing two things simultaneously: compressing effort in generic delivery, which destroys margin, and raising the bar on domain complexity, which rewards firms that can genuinely operate in specialized environments. Exhibit 1 maps several recent acquisitions by power, profit, and execution.

That combination is exactly what Optimum brings: deep healthcare provider workflows, scarce, domain-rich talent that takes years to develop and cannot be hired in bulk, and a delivery model that health systems already trust.

Source: HFS Research, 2026

The provider market is under structural pressure. Health systems are wrestling with shrinking margins, scarce clinical labor, growing administrative burden, and AI governance complexity. They need partners with genuine domain fluency, not generalist technology firms parachuting in with a pitch deck. Optimum has proven Epic expertise, Elite ServiceNow and Premier AWS partnerships, and strong health system relationships. These are not easy assets to replicate, and you cannot build them organically in any reasonable timeframe.

The combination with Topaz and Cobalt, Infosys’s AI and cloud platforms, is also a credible proposition. Infosys now has the provider-side domain layer that its AI and cloud platforms were missing. That is a meaningful gap closed, and the resulting proposition, domain fluency plus AI-powered transformation at scale, is exactly what provider buyers are starting to demand.

Optimum gives Infosys the right to compete in a market where Accenture, Deloitte, and Cognizant have been embedded for decades, and where Nordic is now structurally aligned to a health system through Accrete Health Partners. That credibility is real and hard-won. But provider buyers have moved beyond rewarding implementation capacity.

They want partners who can change the economics of care delivery: automating revenue-cycle leakage, reducing administrative burden, improving clinician productivity, and governing AI safely. The opportunity for Infosys is to use Optimum as the domain anchor and move deliberately toward outcome-based positioning. Price against outcomes rather than effort. Build relationships at the CFO and CMO level, not just the CIO. That is how profit x execution becomes a category position rather than a capability description, and how Infosys converts a strong market entry into durable provider-market leadership.

Infosys is positioning the deal as an AI-powered transformation move, linking Optimum to Topaz and Cobalt. That is the right instinct, but provider buyers will pressure-test it quickly, and Optimum alone does not make the AI story clinically credible. The opportunity is to move fast and layer in AI-native capabilities that change what clinicians and administrators actually experience day to day. Targeted partnerships or minority stakes in ambient AI clinical documentation leaders like Abridge or Suki would give Infosys a genuine AI-native flank in the provider market.

Specific, published proof points where Infosys plus Optimum is demonstrably changing provider economics, whether in revenue cycle, clinician workflows, care navigation, or cost-to-serve, will matter more than narrative. The platform wrapper is not enough. Clinical evidence is what wins.

Half a billion dollars buys Infosys something it could not manufacture: genuine provider-market credibility, domain-rich talent, and a trusted delivery model inside some of the most complex health systems in the country. But buying the right to compete is not the same as competing to win. The next half billion, whether deployed in capital, partnerships, or focused organic investment, needs to go into the future of care delivery, not the infrastructure of the past. Domain depth got Infosys in the room. AI-native outcomes are what will keep it there.

Register now for immediate access of HFS' research, data and forward looking trends.

Get Started

If you don't have an account, Register here |

With the exception of our Horizons reports, most of our research is available for free on our website. Sign up for a free account and start realizing the power of insights now.

Our premium subscription gives enterprise clients access to our complete library of proprietary research, direct access to our industry analysts, and other benefits.

Contact us at [email protected] for more information on premium access.

If you are looking for help getting in touch with someone from HFS, please click the chat button to the bottom right of your screen to start a conversation with a member of our team.