Process industries make up over 50% of the £35 trillion global manufacturing output, producing fuels, chemicals, cement, metals, paper, plastic, food, and drink, but their attributes differ significantly from general manufacturing or consumer goods. They have been historically lumped together with these “discrete manufacturers” on the journey towards Industry 4.0; it’s like adding insurance to banking and calling that market “financial services”. To bring process industries into the digital age, vendors need a different, tailored approach towards transformation.

For too long the manufacturing space has been an ill-defined market of murky, over-hyped Industry 4.0 technologies spun in a one-size-fits-all approach. Subsets of the manufacturing space face unique challenges, because of which continuous process industries lag behind in pushing towards the winners’ circle of Industry 4.0. To change this, vendors must rethink and refine their frameworks and service-strategies to the process industry, driving a different conversation with its leaders.

So far, Industry 4.0 has centered on discrete manufacturing that creates “things.” Vendors scarcely consider continuous process production in the quest for Industry 4.0 best practices and top-level models, and as a result, process manufacturers’ (very) legacy equipment and processes are struggling to evolve. There are stark differences between the discrete manufacturing of cars and laptops and the continuous production of chemicals or cement; however, when it comes to the transformational potential of Industry 4.0 technologies, no one has differentiated the process industry from the general manufacturing space. Analytics, robotics, IoT, AI, and all their friends, cannot be applied in blanket fashion throughout manufacturing.

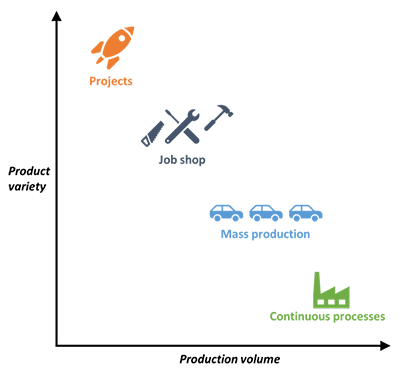

Let’s break down the manufacturing space. Exhibit 1 displays four top-level categories of manufacturing using production volume against product variety. They are

Exhibit 1. Different types of production

Making fast changes to a processing firm is like doing a three-point turn in a juggernaut. The luxury of experimenting and making changes on the fly is nonexistent; digital strategies must be tuned up front, alongside intense capital injection and project management, to avoid painful changes further down the road.

“Failing fast” has allowed many firms to rapidly prototype and reinvent. However, this is not straightforward for manufacturing, where change practically requires large up-front investments. Capital requirements are further exaggerated in process industries, where changing heavily integrated and specialized processes results in significant production downtime and a financial penalty. Mass assembly lines, such as car manufacturing, operate in a modular sense. The disconnect between each stage of production allows discrete manufacturers to test new technologies at a piloting scale or to install them only where they are required.

Profit margins play a part in process industries’ digital woes. By no means are we suggesting that mass-produced cars have a high-profit margin, but they certainly command a greater margin than oil, steel, plastic, paper, or cement. The ability of firms to deal with short-term hits to their profit margins generally decreases as they are categorized along the continuum from projects to continuous processes in Exhibit 1.

The products made in continuous processes rarely change significantly, fostering a culture that is hesitant and resistant to change. The recipe for cement, for example, has been rather consistent since its conception save for minor specification tweaks; compare this to how often car manufacturers change their model designs, and how many opportunities this gives them to reassess and reinvent their production lines. Upgrading these production lines is not a cheap or easy task, but evolving customer requirements keep most firms on their toes. The changes that process industries most commonly encounter involve product specifications, which can generally be accommodated by intensifying processes or bolting a new unit on the back-end.

From an AI, big data, and smart analytics viewpoint, the historical data in process industries is poor. Sensor malfunctions and inconsistencies, and unplanned downtime mean that even a manual analysis of data trends is difficult; engineers must often rely on their experience or gut instinct to decide what data is usable.

The variation between sites within a company, let alone an industry, makes standardized transformation challenging. Oil refineries vary drastically from each other based on the crude oil feedstock (its density, sulfur, and metal content), the site’s products (chemicals, gasoline, diesel, jet or ship fuel, etc.), and their specifications. Standardizing best practice across refining, paper mills, cement kilns, and other realms of the process industry is nearly impossible; their Industry 4.0 strategies must be built from the ground up.

Industry 4.0 transformation cannot be realized with one, all-knowing strategy – vendors who have historically pushed overly-broad solutions must change the conversation. Before falling further behind, the Industry 4.0 hype must be streamlined for the process industry to find the perfect balance between scalable solutions that can also be molded based on the industry, company, or single-site.

Register now for immediate access of HFS' research, data and forward looking trends.

Get StartedIf you don't have an account, Register here |

With the exception of our Horizons reports, most of our research is available for free on our website. Sign up for a free account and start realizing the power of insights now.

Our premium subscription gives enterprise clients access to our complete library of proprietary research, direct access to our industry analysts, and other benefits.

Contact us at [email protected] for more information on premium access.