High street banks, you have a problem! Customers are demanding new ways to access and interact with their finances – if they don’t get it from you, they will from someone else. In fact, 59% of banking customers report they are willing to try a platform that gathers banking products and other services to save money and simplify financial transactions. Even though the fintech onslaught seems to be abating, the emergence of open banking, which forces banks to share customer’s data, such as spending habits, with third parties who have been granted permission, means there is still a new breed, like Meet Cleo and Moneybox, settling into the market and offering banking consumers better access and control over their finances.

Banks can no longer be complacent; they must emulate these firms and drive a greater customer experience in the process, or risk losing out to these upstart competitors.

Complacent banks are not feeling the urgency to address the customer needs

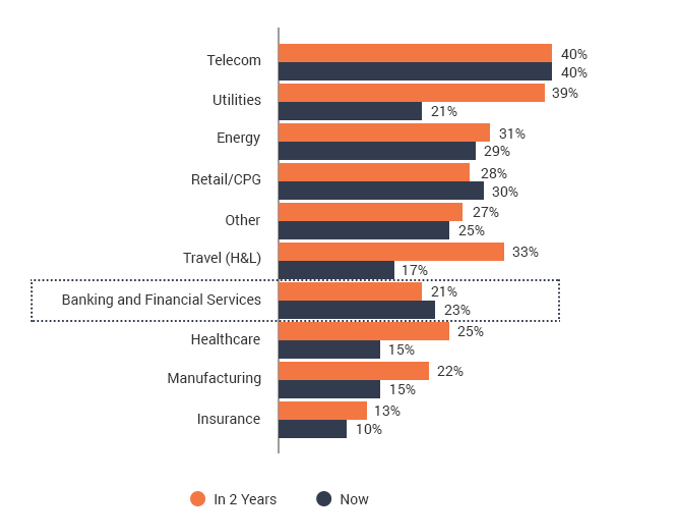

We can see the theme of complacency play out in Exhibit 1, where only 23% of Banking and Financial Services (BFS) firms feel pressure to make significant changes to their operating models. Indeed, there is a growing perception that traditional banks have less of an incentive to drive customer-facing improvements in light of shifting digital demands, fuelled by the understanding that “people need banks” and switching to competitors is difficult.

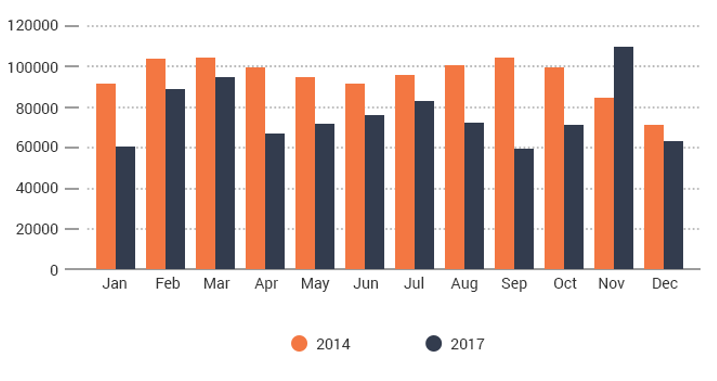

This has led to direct intervention from regulators: in the UK, this came in the form of the Current Account Switch Service (CASS) in 2013. The scheme encourages frictionless transfer between banks by ensuring all changes are complete within 7 working days and any payments to the old account will be redirected for the following 3 years. The hope was to create a competitive banking sector, but in practice, relatively little was done to reorder the state of the market. Exhibit 2 compares the number of switches a month in 2014 and 2017 demonstrating the limited success of the scheme -instead of the improved customer service they had hoped for CASS led to the rise of financial incentives for switching. Clearly, this is alone did not unseat the old guard, but with the emergence of open banking and the fact that money continues to find its way into fintech startups, who raised record $39.6 billion globally in 2018, a new opportunity has been presented for consumers to seek alternative providers to wrestle back control of their finances.

Exhibit 1: How much has your operations / operating model changed to reflect the increasingly digital world? And how much do think it will change in the next 2 years? (Just existential change)

Source: HFS Research in Conjunction with KPMG, State of Operations and Outsourcing 2018. Sample: Global 2000 Enterprise Buyers = 381

23% of banks are facing existential change now, but fewer expect to face it in the future

Consumers are likely to continue demanding more as the emergence of the second payment services directive (PSD2) means a new generation of fintechs can provide them increased access to information. PSD2 is an EU regulation which forces banks to open their infrastructure to third parties to encourage open banking. Open banking combined with improving technologies means a wave of new fintechs are emerging offering consumers new methods of interacting with their finances – be it saving, investing or spending – posing a threat to traditional banks and their traditional methods of accessing finances.

Earlier this year in the UK, the Financial Conduct Authority (FCA) and the Competition and Markets Authority (CMA) commissioned a survey, which banks were forced to publish. Questions were based around the service consumers are receiving from their banks, including the quality of overall service provided, their overdraft services and their in-branch service to name a few. The goal was to fuel consumers with information to easily compare banks. One question asked how likely consumers would be to recommend their current account to a friend; in the case of two major incumbents, only around half of their customers would recommend them.

Exhibit 2: Comparing the number of recorded switches per month in 2014 and 2017

Source: Bacs Payment Scheme Limited (BACS) current account switch service statistics

This gap in the market continues to be filled by a new breed of digital disruptor. We have profiled two emerging fintechs looking to profit from weaknesses in the current market by tackling challenges head-on.

Meet Cleo: gives consumers a new way to communicate with their capital

A significant challenge for large banking institutions is to provide consistently high customer service. In an industry where the service provided is virtually homogeneous, there are huge opportunities for enterprises able to provide better, more consistent customer service.

Meet Cleo is an AI-powered cognitive assistant that offers the insight customers want using a platform already well known to many — Facebook Messenger. Users can ask financial questions like “Can I afford to buy pizza tonight?” and Cleo will analyze their bank statements, account for outgoings, and give an informed response. Over 11,000 people have already sent Cleo messages beginning with “Can I afford….” Ultimately, however, Cleo only makes recommendations, and the final decision is left to the user. Cleo can also be used to ask basic questions about an account, like the balance. Already the firm has accumulated over half a million active users throughout the UK, US, and Canada.

At a deeper level, the founders of Meet Cleo share a belief similar to the FCA and CMA. Consumers are too loyal and switching banks in search of the best customer service and fees should become common practice. This is where the real power behind Meet Cleo is — its application of data. It collects information on users and compares their spending. It uses this information to calculate if customers are paying above average for anything ranging from utilities to overdraft fees and recommends alternative cheaper providers. Crucially, Cleo is not a bank, and it holds no capital stock, allowing the firm to leverage an impartial view of the banking and financial services market.

HFS Viewpoint – Giving third-party access to private financial information isn’t without its risks.

Of course, it’s highly unlikely we’ll see banks openly admitting to customers that their competitor could offer them that loan at a more competitive rate. But, in a competitive market, there is some logic to taking aspects of this platform — such as its friendly and personalized financial advice — to drive improved services. This notion may see the firm, or similar players, finding itself acquired by the larger banks looking to develop their edge. Indeed, research published by HFS found that banks were purchasing fintechs at an increasing pace, and the trend is expected to continue.

But, the model isn’t bulletproof. Foremost, there are already intermediaries with digital marketplaces that allow customers to find the best products and services without giving full access to their personal financial data. The Meet Cleo model may be too high a security risk for some customers who could be reluctant to give away their data simply for easier interactions. Understandably, consumers will be anxious when providing a third party with access to their financial data; although, with most consumers forced to trust existing financial institutions with their data, a few key partnerships with incumbents would help Meet Cleo build more market traction and prove its security pedigree. Furthermore, Cleo’s abilities are limited. Asking a question about more complex financial information such as mortgage criteria or how much to save is met with stock answers that offer little help or information.

Another challenge is that there is currently little regulation surrounding the services they advertise — meaning there is a sea of potential ethical dilemmas. There are immense opportunities for them to just promote the highest bidder rather than prioritize the customer’s needs as promised, an accusation already thrown at some intermediaries in the insurance and financial services space.

Moneybox: makes it easy for consumers to build an investment portfolio with pennies

People’s outlook on investment has changed over the last few decades. An entire generation subject to frequent financial crashes has become increasingly cautious. In fact, a recent survey of a thousand 35- to 70-year-old people who had invested in the past found that 44% would never invest in the stock market again and 58% had completely lost faith in the markets. Moneybox aims to change this by challenging traditional banks to give more control to the consumer. Its model completely breaks down the idea that investing is only accessible to people with thousands in savings and makes it a viable option for everybody by building a portfolio out of small everyday investments. Moneybox can tailor the experience depending on each customer’s risk tolerance by providing the option of three different portfolio structures with varying risk levels. The cash portion of the portfolio spread can range from 85% to 5%, with capital held in higher or lower risk holdings. The firm advises it has experienced an average return of 6.4% over the last 10 years and only two of these years saw negative returns.

In a testament to the success of the firm so far, it advises it is currently managing approximately one million transactions a week. Additionally, it is FCA approved and has launched partnerships with digital-only banks including Starling Bank in 2017 and Monzo in 2018. The method it has devised to accumulate funds for its clients’ portfolios is truly unique—through partnerships with these digital banks, Moneybox can “round up” a customer’s purchase. When a customer makes a purchase, the app increases the purchase price to the nearest round number and saves the difference for the customer. For example, if a customer purchases coffee for £2.60, the app removes £3.00 from their account and transfers 40p of that for investments. This is the main appeal of the service—the idea that consumers will slowly build up savings for an investment portfolio through denominations small enough that they go unnoticed as they exit their account. The success of the partnership with Monzo has caught the attention of some high street banks; in recent months Moneybox announced a similar partnership with Santander also allowing Santander customers to build a portfolio with minimal effort showing that the big players in the industry are also looking to redevelop offerings in the savings and investment space.

HFS Viewpoint – A lack of microtransactions could be a big problem for some consumers.

Moving savings and investments closer to the consumer is undoubtedly a positive move, but Moneybox is not without its challenges. For one, Moneybox is still developing microtransaction capabilities, the lack of which has hampered the firm’s perception as an immediate repository for rounded up savings. Currently, the amount Moneybox takes from rounding up spending is calculated and stored throughout the week and taken from customer accounts every Wednesday. This means that customers are hit with a larger sum leaving their account all at once rather than the continuous smaller ones that they may expect. While it does not appear to be a deal breaker at this stage, it may prove troublesome in the future as customers’ perceptions of rounding up differ from those available from the firm.

The model’s success has been partially attributable to its emphasis on increasing every consumer’s access to investment services. There is certainly an appetite for new products that offer consumers a different savings experience than the traditional monthly direct debit. At its core, the proposition from Moneybox seems to tackle these shifts in the market—but the firm must continue to innovate by building microtransaction capabilities into the platform, enabling clients to build savings and investments into their everyday purchases.

Bottom Line: Banks can no longer rely on implicit customer loyalty; their archaic incentives do not compensate for the lack of information and control they offer compared to new innovators.

As we have discussed, it is truly easy for consumers to switch so they must innovate and develop services that fend off disruptors that have set new benchmarks in the market.

In the UK, Q1 2018 saw bank switches rise 10% over the same quarter in 2017. The emergence of open banking combined with CASS means customer loyalty is fast becoming a luxury the banking sector cannot rely on. Digital disruptors have proven themselves to be a useful addition to the market; many are now working with the large traditional players rather than against them. Banking and financial services players can leverage the new models and approaches by:

Register now for immediate access of HFS' research, data and forward looking trends.

Get StartedIf you don't have an account, Register here |

With the exception of our Horizons reports, most of our research is available for free on our website. Sign up for a free account and start realizing the power of insights now.

Our premium subscription gives enterprise clients access to our complete library of proprietary research, direct access to our industry analysts, and other benefits.

Contact us at [email protected] for more information on premium access.