We are observing a tectonic shift in the business and technology landscape of the aerospace industry. As a result, aerospace OEMs and tier-1 and/or -2 suppliers are increasingly looking for business outcomes from their engineering service providers. In this PoV, we discuss the top five value drivers that clients of aerospace engineering services can expect from their engineering service providers.

The State of Aerospace Engineering Services

Aerospace is consuming new technologies faster than many thought possible. There is a strong emphasis on innovation and performance improvement as new civil aircraft development has more or less ceased. To overcome the challenges posed by a near-stagnation in civil aircraft development, aerospace engineering companies are taking the optimization route. The impetus is to improve design, streamline operations, and boost sustainability.

The focus is also shifting toward avionics, in-flight entertainment, maintenance research and overhaul (MRO) segments, and manufacturing excellence. Thus, quality, performance, and efficiency become the major areas where advanced technologies are leveraged. The aerospace engineering services buyers are consequently keener on service providers who have the ability to foresee what will come and are future-aligned in their approach. The ability to execute well is no more a differentiator; more buyers are looking to collaborate with service partners who have the ability to innovate and explore new avenues.

Design optimization for better utilization of space, weight reduction for higher agility and greater maneuverability, and automation to improve efficiency and gain cost advantage are some of the major thrust areas. The emphasis is thus on making intelligent use of technologies like 3D printing, AI, IoT, AR, and VR to go beyond the defined view of digital transformation and create new and sustainable assets and processes.

The western market is settling into a slow rhythm, whereas the APAC region is waking up to defense upgrades and creating new demand. Geopolitical situations and a renewed focus on strengthening defense capabilities in countries like India and the Middle East opens new avenues for service providers. The APAC region, which was hitherto seen largely as a suppliers market, is ripe to build strong collaboration as a new breed of buyers emerge.

Value Drivers in Aerospace Engineering Services

In our conversations with a cross section of aerospace engineering organizations, it was amply clear that they were willing to push the existing boundaries and bet on innovators who have the demonstrated ability to bring disruptive technology use cases to mainstream services. The ability to think beyond the current horizon and establish a clear vision is a major limiting factor of most of the service providers evaluated. Buyers are not keen to shake hands with service providers with an exceedingly transactional approach, tied to current projects. They are demanding visionary collaborators who can design a future and deliver it.

Building strong IPs and leveraging those as differentiators is the route very few service providers seem to be taking, be it for lack of investment or quality resource, or otherwise. With defense emerging as a big opportunity, specialized resources and expertise are becoming key dependencies. And, the market is keen on those who can circumvent these challenges with their unique value propositions. By analyzing current market trends and decoding the needs of buyers, we could zoom in on some clear and measurable metrics that could be seen all along the value chain and segments. We list five key value drivers that define aerospace engineering services today. These are the guiding factors for buyers in the segment that promise the best business outcomes from their engagements with service providers.

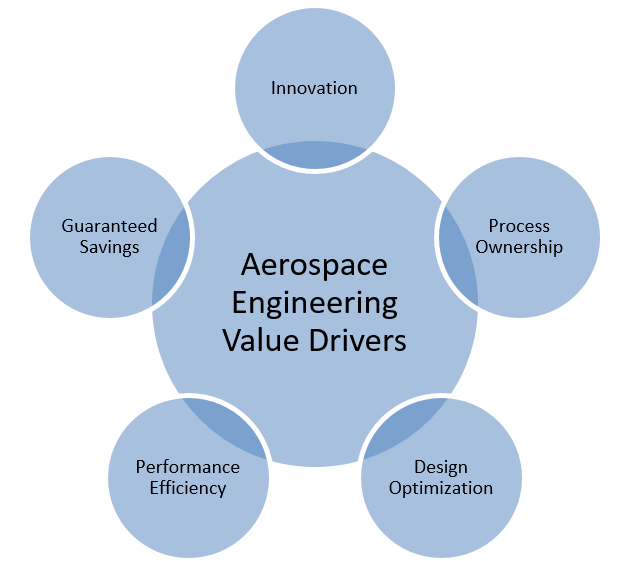

Exhibit 1: Five Value Drivers of Aerospace Engineering Services

Source: HfS Research 2018

1. Innovation — Applied, Tested, Delivered

Innovation that can be seen in action involves futuristic concepts pushing the threshold of technological expertise and creative application and taking the shape of modern day utilities. This is where buyers are putting their trust and money. Service providers need to rise above execution alone and be strategic innovation partners for their clients. Aerospace and defense engineering companies are exploring greater usage of additive manufacturing technologies, also known as 3D printing. These are no more limited to prototyping design but are being used to design and produce components used in aircrafts.

The aerospace market is looking for real innovation to bring new-age concepts into real life use cases, be it in the form of fixing the first 3D printer onboard a space station or creating a complete interactive replica of a real aeronautic factory that can be monitored and controlled in a virtual reality environment. These are innovative uses of technology that offer speed, agility, ease of operation, and above all, considerable business advantage. Apart from being the premise of innovative design, these uses facilitate higher efficiency across the system by building an ecosystem for future-aligned capabilities.

Innovation that rises above the cliché is thus a tangible business outcome that aerospace engineering services buyers definitely demand from their service providers.

2. Complete Process Ownership — End-to-End Value Delivery

Aerospace services buyers see distinct value emerging from those service providers who can take complete ownership and deliver end-to-end projects. When it comes to new product development, some clients demand demonstrative capabilities in complete ownership to deliver on the entire lifecycle—from concept to prototype, to testing and product development. This not only inspires confidence among aerospace buyers but also brings a new product to market faster and capitalizes on first-mover advantage.

End-to-end aerospace engineering capabilities, including proprietary tools and platforms, IP, and accelerators, providing value across the chain of new product development, product sustenance, manufacturing support, testing and certifications, MRO/after-market services, and software implementation are certainly a huge value driver. Aerospace buyers may not have the required infrastructure required to build and test new capabilities. It may not be economically or strategically viable for them to invest in such facilities. Thus, they are keen on service providers who can help them get the entire solution built and tested in remote environments and demonstrated on premise.

3. Optimization — IT Meets Engineering

Digital transformation and streamlined IT infrastructure is still an exception rather than a norm in aerospace engineering companies. However, the focus is slowly but steadily shifting toward a more digitized manufacturing environment. Service providers are required to meet design expectations and deliver products that increase performance with their unique design. With more and more impetus on in-flight entertainment, flight safety, passenger comfort, and space optimization, manufacturers are pushing the envelope in reducing the weight of various components to provide agility to the aircrafts. They demand that the entire process for improved design—from idea generation to feasibility assessment to actual implementation—be owned by service providers. Aerospace buyers are setting aggressive weight reduction targets and demanding on-time delivery, saving time and money and building a much smarter product in the bargain.

In-flight space optimization is a major opportunity where aerospace engineering leverages the best in technology. While addressing the concerns of functionality, accessibility, maintainability, and airworthiness on one hand, and aesthetics on the other hand, the ask from service providers is to rise above time constraints and deliver optimum products or components within compressed design cycles. The fact is if you push the bar, more than 10 percent weight reduction of various components can be achieved within reasonably short timelines while the entire design thinking to value delivery process is completely owned by service providers.

4. Performance Efficiency — Tangible, Transparent, Timely Outcomes

Reduced cycle time of over 50 percent, or more than 90 percent FTR rates, or 30 percent reduction in DMU check cycles—these are just some of the indicators of tangible performance efficiency across aerospace segments and all through the value chain. With advanced analytics and integrated web-based architecture, not only do systems become more efficient but also display improved performance, delivering more than 25 percent flow time reduction for managing PLM. The market is thus focused on engaging with partners who can deliver on these lines. Such business outcomes are measurable and can be easily tracked and reported to aid business decision-making.

5. Guaranteed Savings — Cost, Effort, and Time

Aerospace engineering services buyers can definitely gain over 50 percent cost savings across the value chain in different aerospace segments with the right systems in place. They can demand more than 30 percent reduction in should costing, 20–30 percent cost reduction in supply chain management, and 15–20 percent cost reduction with value engineering. In addition, with automation leveraging AI and design optimization, aerospace engineering companies can garner an additional 30–40 percent savings that can give them a huge benefit on the bottom line.

Apart from cost savings, automation and technologies like AR, VR, and 3D printing are bringing down effort and time requirements drastically. Products are delivered not just on time, but also within the shortest possible timeframe. These advantages contribute directly to the competitiveness of aerospace players in the market and give them a marked differentiator.

The Bottom Line: Value Delivery Needs to be Tangible and Sustainable

Aerospace engineering is going through a transformative period. The value they seek is beyond present day challenges—the market wants service providers to be aligned with the future. Since traditional aircraft manufacturing is giving way to more nuanced avionics and in-flight systems, the focus is now on improved agility, speed, and performance. New designs and unique capabilities will rule the air. This is one industry where ideas are worth millions, provided they can be quickly productized and brought to operations, keeping regulatory and compliance constraints in mind. Aerospace buyers should consider vendors who focus on new IP development and are capable of innovative design thinking that can be implemented without a glitch.

Register now for immediate access of HFS' research, data and forward looking trends.

Get StartedIf you don't have an account, Register here |

With the exception of our Horizons reports, most of our research is available for free on our website. Sign up for a free account and start realizing the power of insights now.

Our premium subscription gives enterprise clients access to our complete library of proprietary research, direct access to our industry analysts, and other benefits.

Contact us at [email protected] for more information on premium access.