This Point of View is for provider CFOs, CIOs, and revenue cycle leaders building self-pay into the operating model to offset 2026 public funding cuts.

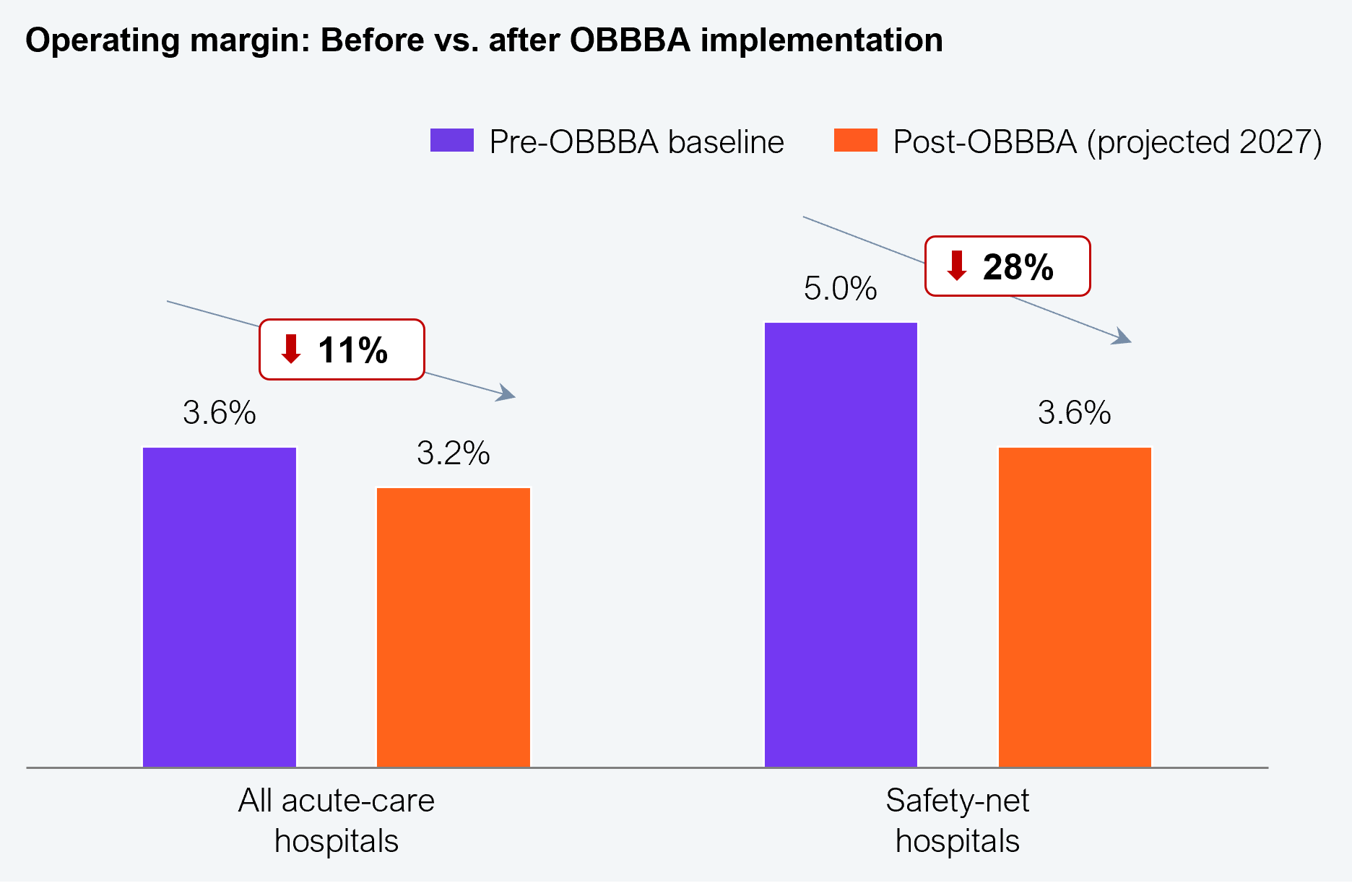

The unprecedented 10% decline in public health funding due to OBBBA, Medicare sequestration, and ACA subsidy expiry will translate into an estimated overall 18% reduction in care delivery margins in 2026, worsening in 2027. For example, in acute care hospitals, operating margins are expected to decrease by 11% in 2027, and safety-net hospitals will endure an approximate 28% decrease (see Exhibit 1). However, the increasing share of self-pay by consumers who are ignoring poorly negotiated payer rates in favor of deeply discounted cash-pay rates from hospitals is a positive story that will address some of the margin challenges.

The self-pay opportunity is emerging inside the commercially insured population with high-deductible health plans, where rising patient cost-sharing, prior authorization friction, claims denials, and opaque benefit design have turned millions of insured Americans into de facto cash buyers for a meaningful share of their care, equivalent to over $75 billion in potential higher-margin revenues for providers in 2026. This is the opportunity care delivery CFOs must chase down in collaboration with their CIOs to ensure there is a durable systems solution to it.

Source: Commonwealth Fund, KFF, CBO, Center on Budget and Policy Priorities, HFS Research, 2026

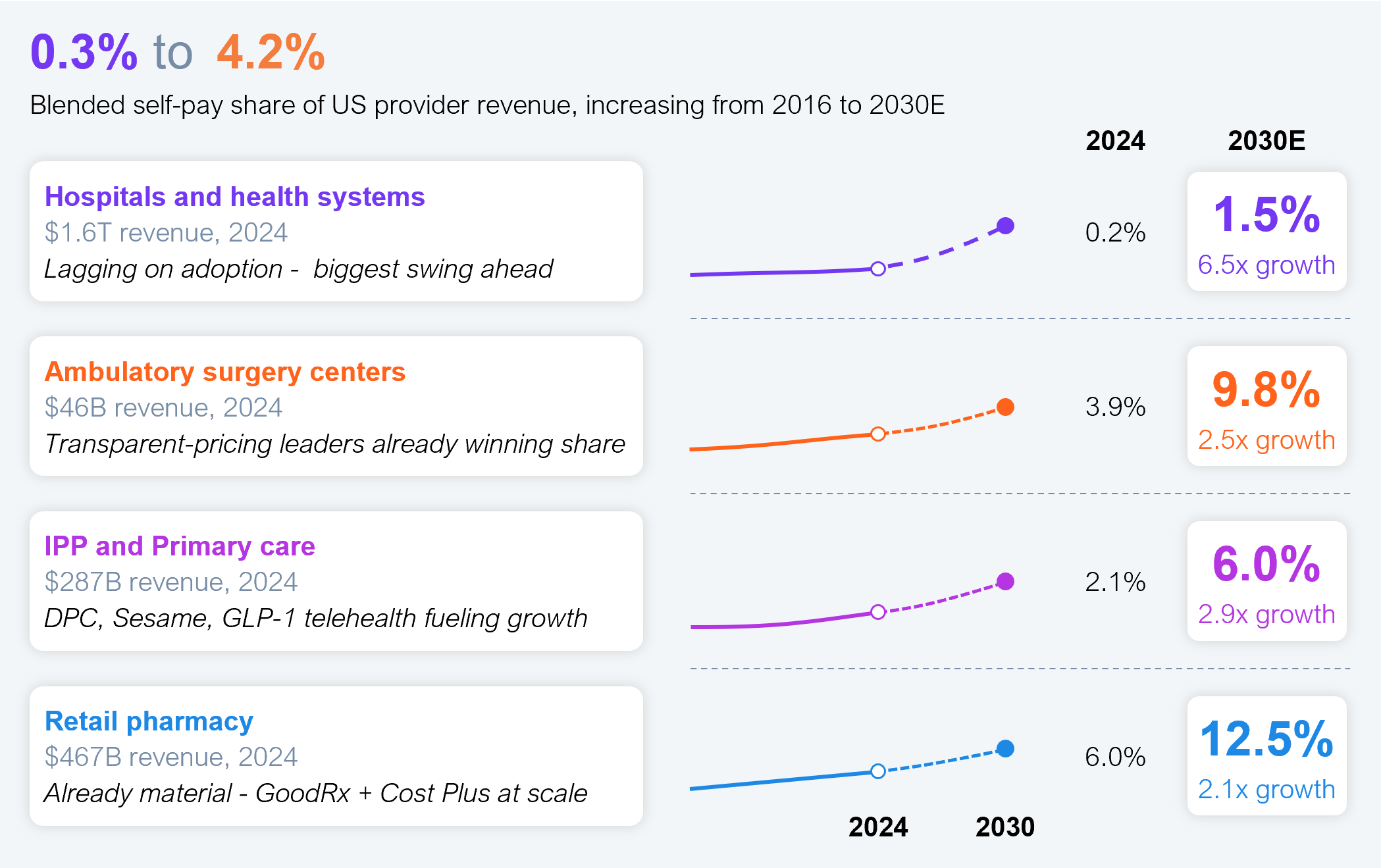

Adam (real name withheld) was prescribed a cardiac CT scan, and his prior authorization was denied. A typical approach would have been for Adam’s provider to appeal the denial or for Adam to forgo the imaging, but, since he had already made an appointment with the provider, the provider leveraged its knowledge of Adam’s patient benefits and pitched a cash-pay option that was 60% lower than Adam’s deductible. This ensured the provider did not lose the revenue, and Adam got the imaging he needed at a steeply discounted rate. This is not a one-off; rather, it is an increasing trend that providers must institutionalize rapidly (watch this space for an HFS playbook on how to), given the estimated hockey-stick growth expected, as seen in Exhibit 2.

Source: CMS NHE 2024, KFF, GoodRx, AAFP DPC, Surgery Center of Oklahoma, Becker’s, HFS Research, 2026

Self-pay may seem like lost revenue compared to the payer-contracted rate. But consider imaging, minor procedures, or lab panels for a commercial HDHP patient who hasn’t met their deductible. For example, the fee for Adam’s cardiac CT scan is $1,000, but he hasn’t met his deductible yet. The contracted rate is typically 50% of the chargemaster. So, in Adam’s unmet deductible scenario, he must pay the entire $500, and the industry collection benchmark is 35% to 45% over 90 to 180 days. So realistically, the provider will only realize between $125 and $200. Compare that to $250 paid at the point of service. No-brainer, you say?

Let’s stick with Adam for a bit longer. When he called the provider to schedule his imaging visit, the provider conducted an EDI 270 eligibility check to determine his coverage status, plan type, and network status, as well as his financial information (such as deductibles and copays). The smart opportunity here would have been to act on his EDI 271 response, which returned Adam and his family’s deductible (total and amount already accrued year-to-date), the out-of-pocket maximum (total and amount already accrued), copays by service type, and the coinsurance percentage after deductible. At this point, the provider could have offered Adam its self-pay option, which would have reduced Adam’s fee, saved the provider the administrative cost of prior authorization, and improved Adam’s experience by scheduling him sooner.

Providers must become proactive and use the EDI 271 information to determine which patients and procedures are candidates for discounted self-pay options and make such offers before the visits. Furthermore, proactive self-pay is also a driver of prioritizing schedules: self-pay patients get faster access than those with less attractive insurers.

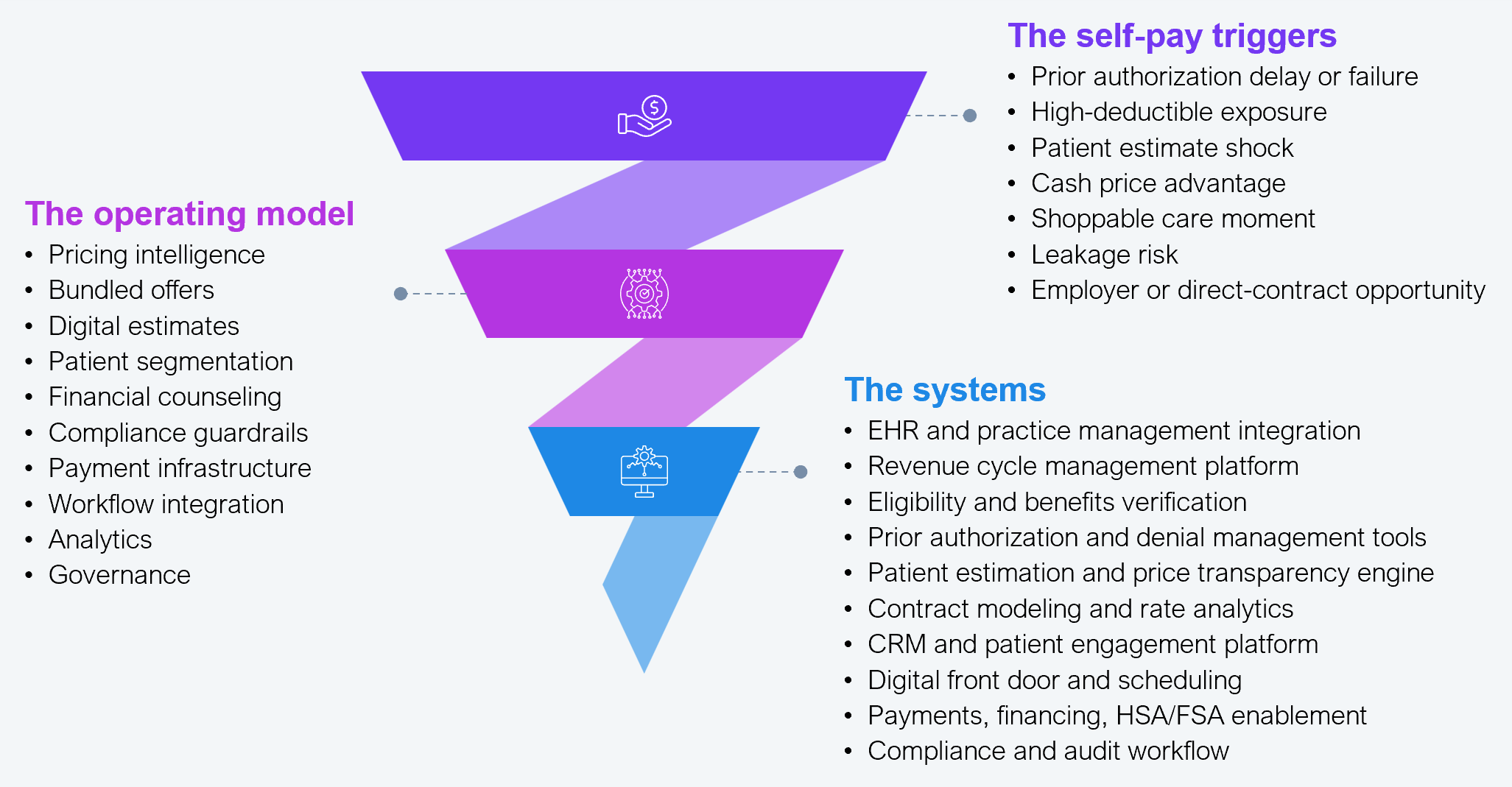

The self-pay opportunity will not scale through static price transparency pages, call-center scripts, or one-off discounting. Providers need an operating model that identifies the right patient at the right moment for the right service with the right compliant offer.

Providers must bring together the three levers in Exhibit 3 to embed self-pay into the business’s economics, with CFOs and CIOs working together. The CFO owns the economics, including mandating processes to support it, while the CIO owns the architecture, and revenue cycle, access, compliance, clinical operations, and service-line leaders own execution.

Source: HFS Research, 2026

To be clear, self-pay is not a discount; rather, it is a decisioning capability. The winners will know when to offer it, how to price it, how to explain it, and how to operationalize it without creating regulatory or contractual blowback. Are you the winner?

Register now for immediate access of HFS' research, data and forward looking trends.

Get StartedIf you don't have an account, Register here |

With the exception of our Horizons reports, most of our research is available for free on our website. Sign up for a free account and start realizing the power of insights now.

Our premium subscription gives enterprise clients access to our complete library of proprietary research, direct access to our industry analysts, and other benefits.

Contact us at [email protected] for more information on premium access.