Insurance carriers have remained distanced from their end customers due to the nature of the industry. Connected ecosystems now offer a way for carriers to plug in exactly where their customers need them the most. Insurance CIOs and IT executives need to rethink their core insurance platforms to create and participate in these ecosystems built around their customers’ and intermediaries’ everyday lives. The next phase of hyperconnected growth calls for a far more open, leaner, and maintainable core. Integration is fast becoming the most important technical and business goal for insurance.

Insurance is one of those consumer-facing industries that was designed to be responsive in nature. “Buy a policy and forget it” was the traditional operating principle. This model and the cognitive distancing limited carriers’ level of understanding of the evolving needs and servicing expectations of customers. Now many carriers find themselves rethinking their customer engagement models to ensure new products and services address the most relevant aspects of a customer’s everyday life such as travel and shopping.

Due to the emergence of digital ecosystems aggregated around consumers and businesses, the fundamental structure of the insurance industry going to change, and it is already becoming more fluid. These digital ecosystems already dictate the access points and means of interactions for customers between themselves and with their brands of choice – for example:

Leading insurance carriers have been actively spotting opportunities, and they are already plugging into existing ecosystems mentioned above and further, such as new interaction channels like Google Assistant, new data-based products in wearables, and usage-based insurance. For example, a long list of companies, including Prudential, Liberty Mutual, and Geico, created Alexa skills to encourage customers to undertake voice-based activities including shopping for products, accessing information, and comparing quotes.

The choice for most carriers, then, is to either join an existing or emerging ecosystem or to create a new ecosystem altogether through a platform play. HFS expects to see examples of both, and even a combination of strategies, as carriers develop more data-driven products and services in the next few years. This evolution will lead ambitious carriers down the path of creating their own ecosystems, partnering with insurtechs, and creating new kinds of companies such as wearable manufacturers for the next generation of data-driven policies, real estate apps and platforms for new homeowners’ insurance, and event companies for short term insurance.

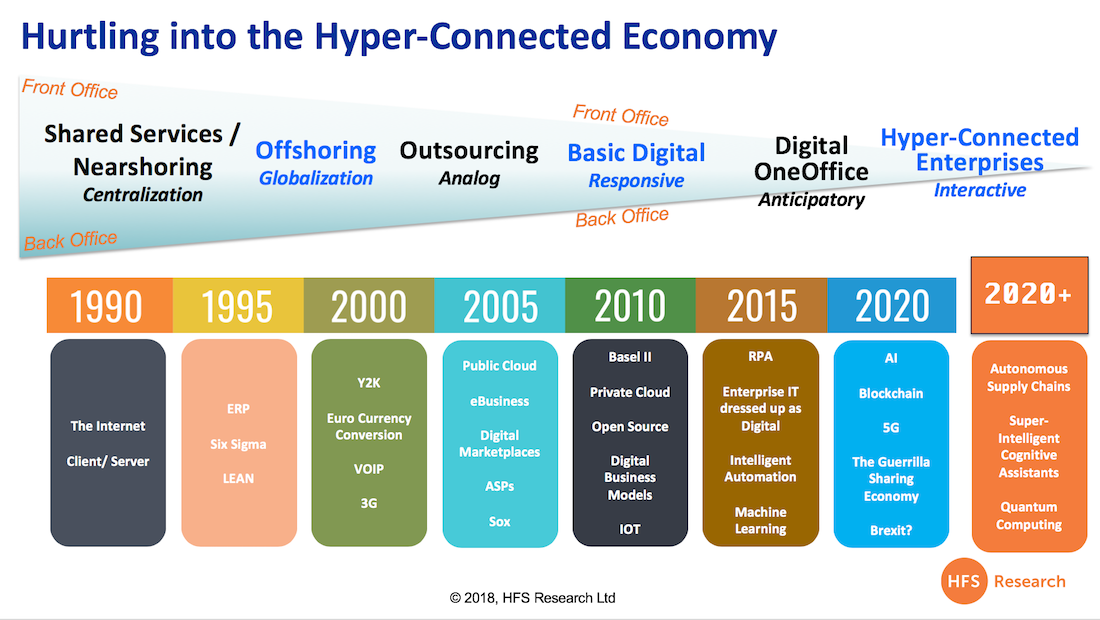

HFS envisions the emergence of hyperconnected enterprises, where businesses have to extend outward to interact and create meaningful and differentiating connections with ecosystem partners and end customers (Exhibit 1).

Exhibit 1: The hyperconnected economy will create new opportunities for businesses to become interactive

This interconnected, ecosystem-fueled future has profound implications for insurance carriers from a technology platforms perspective. Current progress from CIOs is taking the form of technology modernization efforts to update or replace legacy systems to keep up with insurtech developments. However, technology advancements are creating the opportunity for carriers to bring in (and swap out) new functionalities on platforms through an API and microservices approach. This would allow carriers to roll out capabilities that are most valued by customers, as well as foster new ecosystem plays as they develop. For example, as home automation becomes more pervasive, customers will increasingly expect their carriers to be present in and offer incentives through connected home ecosystems. Each wave of insurtech brings new expectations to the forefront, and carriers need to be able to respond—or else they risk obsolescence.

Some of the biggest insurance majors are starting to think of core technology platform functionalities as an ecosystem of tools in and of itself. For example, Oliver Lauer, former Head of Architecture and Head of IT Innovation at Zurich has publicly stated, “Your Open API approach has to become the main principle or strategy of all your business and technical ambitions. You have to evolve your systems to an open platform and ecosystem—like the ones Amazon and other digital retailers have made very successful—selling everything to everybody, not only your own products.”

A big part of this equation is your core platform partner’s views on interoperability and flexibility. Core platform vendor OneShield’s co-founder and CTO Vivek Gujral outlines the role of platform vendors, stating, “…Software vendor partners [need] to respond to changing insurer customer demand. They must embrace an architecture that allows parts of their software products to be swapped in and out by clients. They may well need to coexist with other vendors of the same class, for example, two vendors’ claims systems living side-by-side. Vendors need to operate within a framework of application programming interfaces (APIs) and must be extremely flexible in the ways their software can be used within that ecosystem.”

Ultimately, success doesn’t hinge on an insurance carrier’s ability to use a particular interaction channel or technology platform. Instead, it is their ability to adapt to use new functionalities and engage in emerging ecosystems through an open, leaner, and more maintainable core. Integration will be the name of the game for insurance CIOs and IT executives. Seek out software services partners that are embracing ecosystem-based approaches instead of walled gardens to collaboratively build your insurance value chain that is sustainable through the future of hyperconnectivity. Building connectivity to other systems is an internal technical goal. The business outcomes you can impact are the differentiators—being able to flexibly offer new product and service concepts, meeting customers where and when they need insurance the most, driving greater engagement and loyalty, and building new risk models that match the technology-enabled nature of consumer lives today.

Register now for immediate access of HFS' research, data and forward looking trends.

Get Started

If you don't have an account, Register here |

With the exception of our Horizons reports, most of our research is available for free on our website. Sign up for a free account and start realizing the power of insights now.

Our premium subscription gives enterprise clients access to our complete library of proprietary research, direct access to our industry analysts, and other benefits.

Contact us at [email protected] for more information on premium access.