HFS recently launched our inaugural Industry Primer, focused on the insurance vertical. The Industry Primers offer a comprehensive view of industry trends, including the HFS Industry Health Index, sector-specific business drivers and challenges, enterprise adoption trends for IT and business process services, supply-side trends in offerings and capabilities, and perspectives on the adoption and impact of emerging technologies.

We discuss one of the key findings of the Primer in this Highlight – the insurance industry’s need to carefully balance business and financial risk in the post-COVID environment.

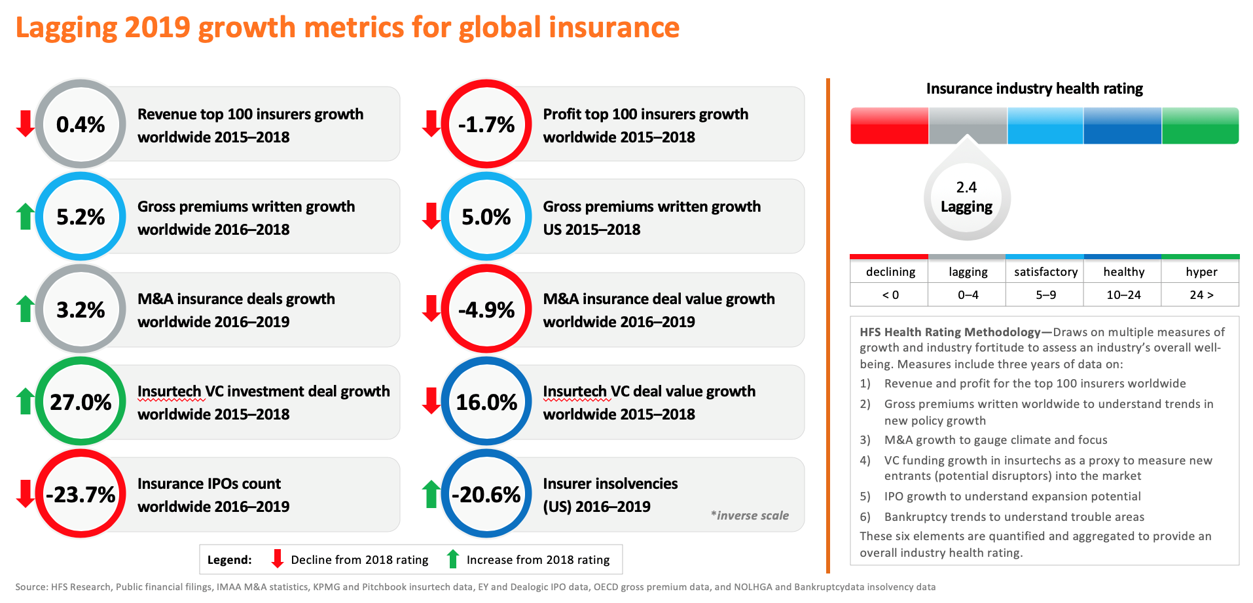

Global insurance markets had been growing sluggishly, pre-pandemic

Whether dealing with life and annuities, property and casualty, reinsurance, commercial, or personal lines, this much is common for the insurance industry—change is coming, and the next decade for the industry will be radically different than the last. New players will come to the forefront with new business models, and truly forward-thinking traditional carriers will be able to adapt and survive, and perhaps even thrive, in the digital age. To cut through the hype around the state of the insurance industry, HFS has developed its health rating approach—a methodology that draws on multiple measures of growth and industry fortitude to assess an industry’s overall well-being. The high-level findings indicate that insurance as a whole is lagging growth (see Exhibit 1).

Exhibit 1: Global insurance markets continue to register lagging industry growth

Some of the input metrics that significantly impacted this score include:

Other metrics that impacted the insurance health rating negatively include a slower rate of IPOs, while we instead saw hyper-growth in VC funding for insurtech, and satisfactory growth in gross written premium, reflecting increased sales.

Business disruption due to the pandemic is already forcing many market changes for insurance carriers

The anemic industry health rating for the global insurance sector pre-pandemic already suggested that change was critical. The pandemic has hastened some of the sector’s shortcomings placing a fine point on what works and does not work from a physical versus digital context. Key observations include:

The Bottom Line: The insurance market can benefit from more operational efficiency, but ultimately needs to make itself relevant to customers’ changing insurance needs

One of the data-centric findings in the HFS Insurance Industry Primer revolved around the plans for digital transformation. We found that insurance carriers are more focused on increasing bottom-line profit than the cross-industry average. Insurance carriers across P&C and L&A segments continue to operate on wafer-thin margins, with profits barely eclipsing the cost of equity to them. It is no wonder that cost containment is among the top priorities.

However, carriers need to press onward toward digitizing customer-facing processes, providing interfaces and portals for better communication, and data exchanges across policyholders, brokers, and other intermediaries. Hyper-personalization continues to be a priority as many insurtechs change the type and duration of risks covered, and concepts such as just-in-time and pay-per-use insurance gain traction. Similarly, digital competitors, including tech giants like Amazon, fast-moving incumbents, and disruptive insurtechs, are putting significant pressure on carriers globally. HFS expects these priorities to become even more relevant in the post-COVID 19 world. Bottom-line improvements may help carriers buy time as economic conditions remain uncertain, but ultimately they need to rethink existing business models and products to create net-new market growth.

Register now for immediate access of HFS' research, data and forward looking trends.

Get StartedIf you don't have an account, Register here |

With the exception of our Horizons reports, most of our research is available for free on our website. Sign up for a free account and start realizing the power of insights now.

Our premium subscription gives enterprise clients access to our complete library of proprietary research, direct access to our industry analysts, and other benefits.

Contact us at [email protected] for more information on premium access.