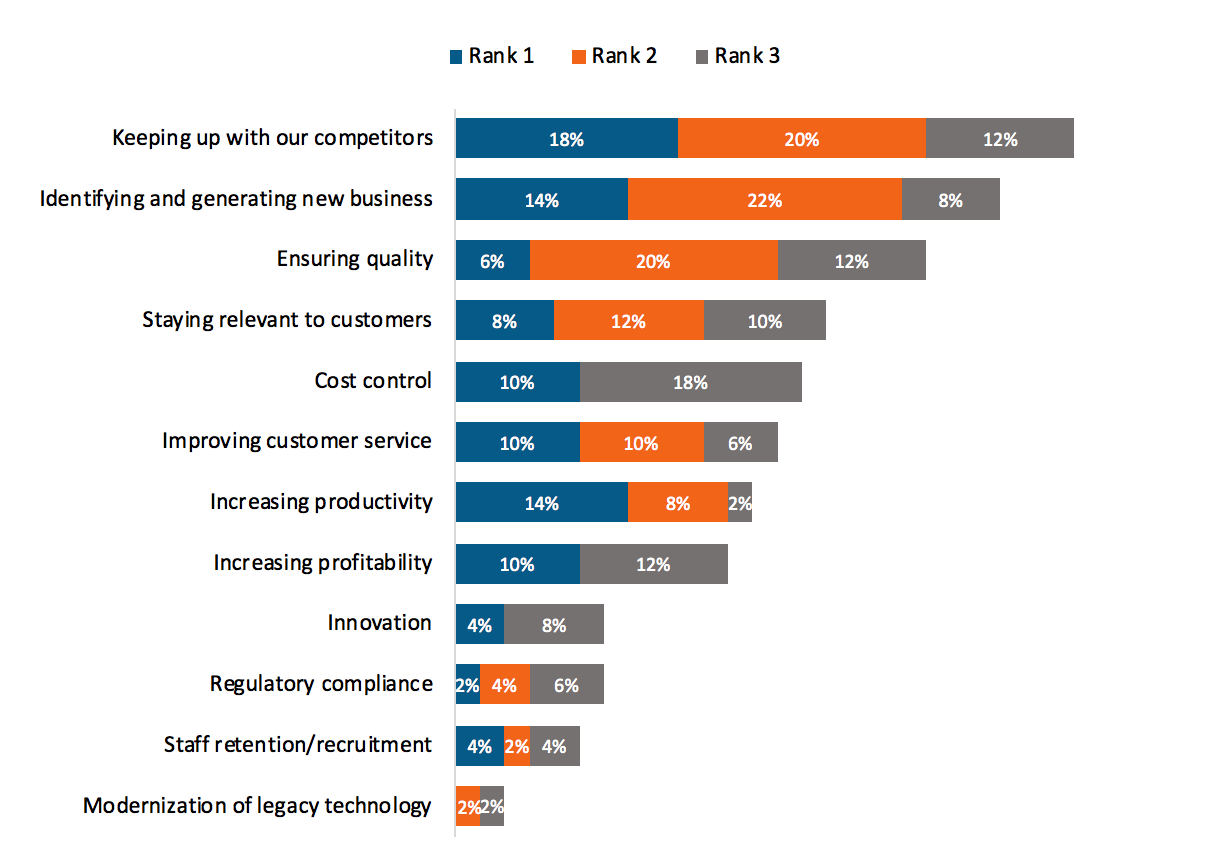

The onset of digital business has crept up on many traditional insurance providers and it may too late for several to fight back. Firms like Blockbuster Video, Toys R Us, and British Home Stores have already been put out of business by failing to respond to changing customer needs in the retail sector, and the same is happening in the insurance sector. And as this shift continues, several traditional firms have already missed their chance to salvage their business models (and in some cases, never stood a chance), and aren’t prioritising customer experience (see Exhibit 1).

Exhibit 1: Legacy insurers’ biggest business challenges for 2017

Q: What are the biggest challenges faced by your company at the moment?

Source: HfS Research 2017, n=50 US P&C decision makers

End customers’ suffering – get smart with AI and digital!

Insurance is notoriously difficult for consumers to understand and buy due to a prevalence of jargon, a lack of transparency about pricing and terms, and a convoluted application and approval processes.

Hence, if you can deliver insurance in a less cumbersome, more cost effective, and touchless model that delivers to customers what they need more quickly and conveniently, you can quickly inflict damage on traditional insurers unable (or unwilling) to change.

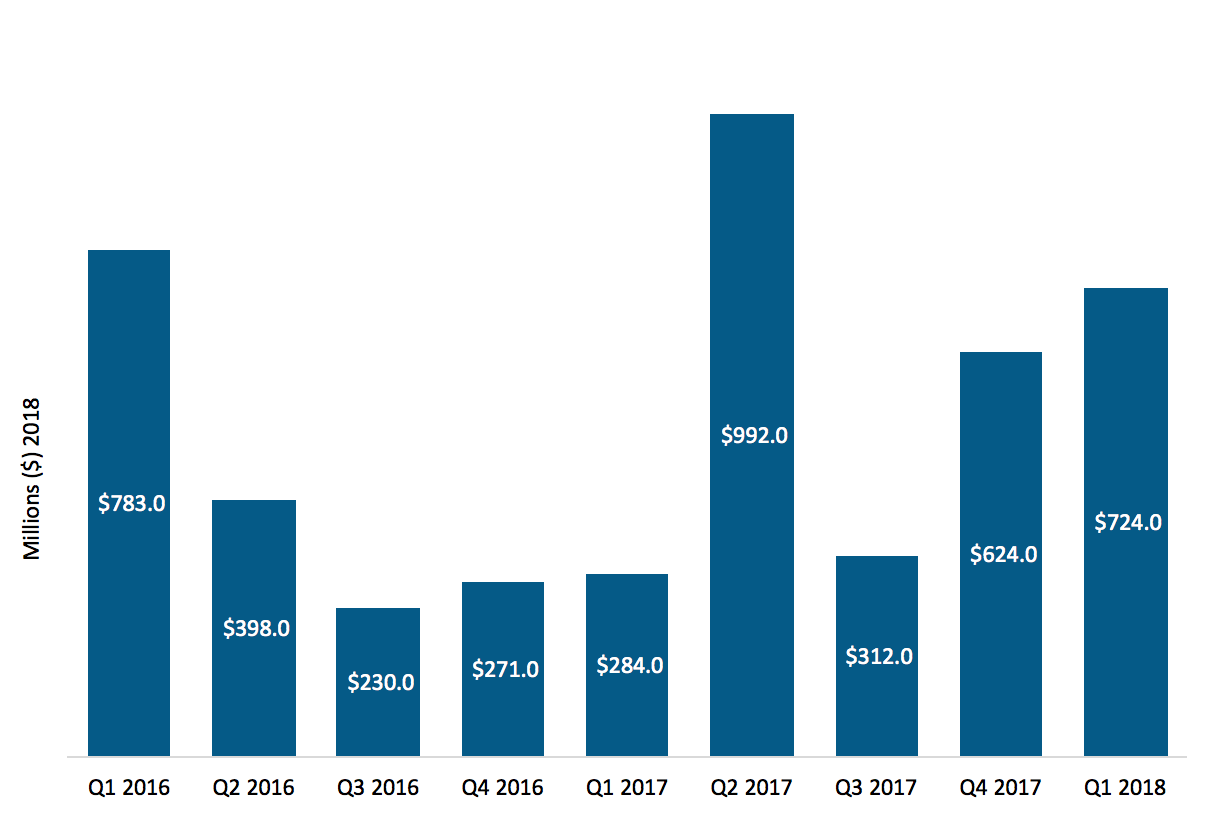

Trust between carriers and consumers is low, due to an often-contentious claims process predicated on mutual distrust. These pitfalls have resulted in the insurtech sector enjoying a massive influx of funding quarter after quarter (see Exhibit 2), as innovative new entrants keep finding new methods of exploiting inefficient legacy insurance business practices. However, many new entrants in the space have tended to focus on distribution without disrupting the way the traditional insurance model works. It is one thing to deliver augmented value to improve traditional business models, another to alter the very fabric on which those business models are predicated. And this is how the current insurtech landscape is shaping out.

Exhibit 2: Global VC insurtech funding

Source: PwC

To this end, several innovative firms are vying to uproot traditional insurance models and, interestingly, not all of them happen to be startups. Next, we take a look at five insurance innovators with the potential to revamp insurance fundamentally in the near future: Lemonade, Haven Life, Trov, AllLife, and AXA.

Lemonade is upending the renter and homeowner insurance market

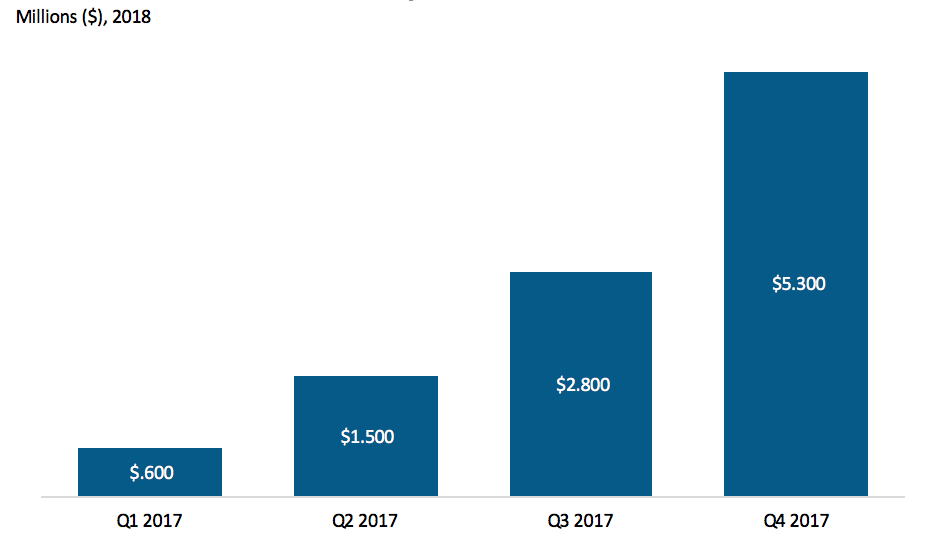

An insurance company relying on the traditional model will need to deny as many claims as it can to turn a profit. And where it can’t deny a claim, it will raise the premiums the following year to cover part of its loss. Lemonade, a US-based online insurance agency, is turning this model on its head. The firm offers renters and homeowners insurance via both online and mobile. It has been amassing customers at a healthy clip and siphoning users away from legacy insurers since 2016 (see Exhibit 3). Instead of monthly premiums, it charges one flat fee, pays claims instantly at a rate based on the flat fee a customer has paid, and donates any leftover money to a charity of the customer’s choice. Lemonade uses premiums pooled from each peer group to pay for the group’s claim, and gives the leftover money to the customers’ common cause.

Lemonade’s cost structure shifted away from agents through use of AI technology to create their bot, Maya. Maya helps customers get insurance quickly, either through a mobile app or online. In addition, Lemonade leverages AI to create competitive advantage. Coders building their underwriting software are advised heavily by a group of hyper-qualified behavioural economists to help their algorithms better predict what kind of person might make a claim and why and to better be able to detect and mitigate fraud. Lemonade is also offering its API to companies who might want to use it for their own clients.

Lemonade can attribute its success to fearless business model changes that boost customer loyalty. For instance, in August 2017 it announced that it was making its policies “live”, giving users the ability to update or even cancel their policies instantly from within Lemonade’s app without having to speak to a customer service agent. This is in stark contrast to most incumbents’ approach, where users are required to contact customer service and wait several days to confirm a change to or cancellation of a policy. This is how HfS views true digital business: creating the ability, through interactive technologies, to respond to customer requests as and when they occur. Digital is about immediacy of customer impact, where front and back office are perfectly integrated to create OneOffice that works in real-time.

Even more radically, in September 2017 Lemonade unveiled a new product, Zero Everything, which offers policies with no deductibles. Its users can now file up to two claims per year with no deductible payments, and without raising their premiums. A deductible is the amount the policyholder has to pay out to cover a claim before their insurer will make a contribution, often resulting in customers having to foot the bill for smaller damages. Simply filing a claim also often results in a premium hike. Lemonade’s move is likely to put pressure both on rival providers to follow its example or risk being left at a significant competitive disadvantage.

Exhibit 3: Lemonade quarterly insurance sales revenue

Source: Lemonade Transparency Chronicles

Haven Life’s smart data use and exam-free insurance policies are transformational

US-based life insurtech Haven Life is tackling the notoriously difficult area of life insurance, a product that’s hard to sell because it offers no tangible reward to the buyer in their lifetime and as such is often viewed as a low priority.

Haven Life is unusual as it’s licensed in all 50 US states, something no other insurtech has achieved. It’s fully owned by traditional insurer MassMutual, making it easy to gain consumer trust and navigate the US’ tricky state-by-state licensing system. Haven Life’s proprietary underwriting system enables it to underwrite applicants in real time, by drawing on self-reported information, as well as details from public databases, and has ready access to MassMutual’s historical data.

This real-time approach to analyzing data enables Haven Life to offer an instant decision on coverage in minutes, in contrast to incumbents’ lengthy application procedures. Haven Life is also reducing the need for medical exams by using information gathered in applications, as well as by analyzing third-party data in real time. Once an application is submitted, customers are notified whether or not they qualify for the company’s InstantTerm, which does not require a medical exam process. When an exam is needed, Haven Life sends a medical professional to the client. Being able to eliminate the need for an exam even for some consumers makes for a unique selling point in the US life insurance landscape and is likely to gain Haven Life traction.

Trov’s international partnering savvy and effective app fueled rapid growth

US-based Trov (so far available in 23 states), which provides on-demand insurance for personal items such as bicycles and electronic devices via an app, is achieving scale at an unusually fast past among insurtechs.

In April 2017 it raised $45 million in a Series D round led by Munich Re’s HSB Ventures, bringing its total funding to $85 million. Interestingly, Trov said the funding will be used to expand into Europe, Asia, and South Africa. In addition to its investment, Munich Re will also underwrite Trov’s policies in these markets. Trov is also looking to move into Japan: It will be doing so with new partner and investor Sompo Japan Nipponkoa, Japan’s largest non-life insurer, which will distribute its policies in Japan.

Most insurtechs find it difficult to expand internationally due to a complex licensing process for each new market, so most choose to stay in their home markets, making Trov an outlier. Going international with powerful partners like Munich Re and Sompo, which have industry and local market knowledge, regulatory experience, and take care of the complicated underwriting process on Trov’s behalf, is therefore a clever play that stands to make Trov a significant player on the global stage.

AllLife insures chronic illnesses quickly with hi-tech risk assessment

South African AllLife—which provides life insurance for people with chronic illnesses—is shaking up the insurance industry by making it easier for carriers to cater to groups previously deemed too risky. In April 2017, AllLife announced a partnership with UK-based life insurance and pensions giant Royal London, under which Royal London will leverage AllLife’s Kalibre platform to offer life insurance coverage to UK type 1 and 2 diabetics who were previously deemed too high-risk to be eligible for such products.

AllLife, whose products are re-insured by Gen Re, provides real-time risk assessment technology and continual underwriting that give insurers a more accurate idea of the risk profile of prospective diabetic clients, allowing them to price policies more fairly and insulate against risk. This shortens the time it takes a diabetic to be approved for coverage.

Moreover, the continual underwriting means that if a client’s diabetes management improves with time, their premium can be brought down. By mitigating the risk of providing life insurance to individuals with long-term and incurable illnesses, risk assessment technology like AllLife’s opens up a large and still very underserved market for risk-averse incumbent insurers, an opportunity more incumbents are likely to want to explore.

AXA efficiently delivers flight-delay insurance using blockchain and smart contracts

French insurance giant AXA gets a place on this list for its flight-delay insurance product, Fizzy, which stores and processes payouts via “smart contracts”—self-executing contracts triggered automatically once pre-determined parameters are met in the real world.

Smart contracts stand to streamline the compensation process for providers and claimants. When an AXA customer buys flight-delay insurance on the Fizzy platform, the purchase is automatically recorded on an Ethereum-based immutable ledger and a smart contract is created on the blockchain. The smart contract is linked to global air traffic databases, which means that as soon as a delay of over two hours is registered on the ledger, compensation is triggered.

Fizzy also removes the need for a customer to file a claim, and the compensation decision is delegated entirely to an automated arbitrator, eliminating potential insurer-client disputes. This promises to boost trust between customers and providers, whose interests are often at odds.

The bottom line: Start leveraging data to design smarter ways to improve CX, or become obsolete

Simply put, improving the customer experience is the endgame; using smart data and leveraging digital and AI technologies are conduits to achieving it. If we examine some high-profile cases of disruption in recent years, we can see the common denominator is a transformation of the end user experience, where technology has been the enabler to get to this point:

Register now for immediate access of HFS' research, data and forward looking trends.

Get StartedIf you don't have an account, Register here |

With the exception of our Horizons reports, most of our research is available for free on our website. Sign up for a free account and start realizing the power of insights now.

Our premium subscription gives enterprise clients access to our complete library of proprietary research, direct access to our industry analysts, and other benefits.

Contact us at [email protected] for more information on premium access.