The insurance industry is ripe for disruption as consumers seek new and innovative ways to insure risk. While for many of the large carriers, basic digitalization is already enough of a headache, for those with a greater appetite for investment or the emerging disruptors taking their place in the market, digital change agents such as blockchain and IOT offer considerable opportunities. One of those opportunities is through the flexibility and agility of live-time insurance products, which would enable ever-changing insurance premiums determined by a range of variables that reward customers for safe usage of their insured goods, such as cars. The commuter driving over 100 miles per day would pay a considerably higher premium than the casual driver traveling to cricket once a fortnight. With 89% of consumers looking to switch providers, seeking improved service, over the next few years, executives must work harder to keep up with customer demands.

Insurers have adopted an inefficient pricing model, and it’s their customers who are left to shoulder the burden

Insuring something that is not constant is where the real cost inefficiencies sneak in. Take motor insurance, for example. The risk is considerably lower when the vehicle is not in use; however, consumers are left paying a single annual premium. Insurers must do this because the costs associated with a motor accident can be astronomical and could require payment for multiple car repairs and medical bills. Beyond mileage estimates, insurers don’t know when the vehicle is in use, this means they cannot differentiate between the higher risk associated with more usage and the limited risk of a parked vehicle. If insurers could track when a vehicle is in use, they could alter the premium accordingly and drive down premium prices.

Insurers could use blockchain and IoT to offer a live-time insurance product, which would drive down consumers’ premiums

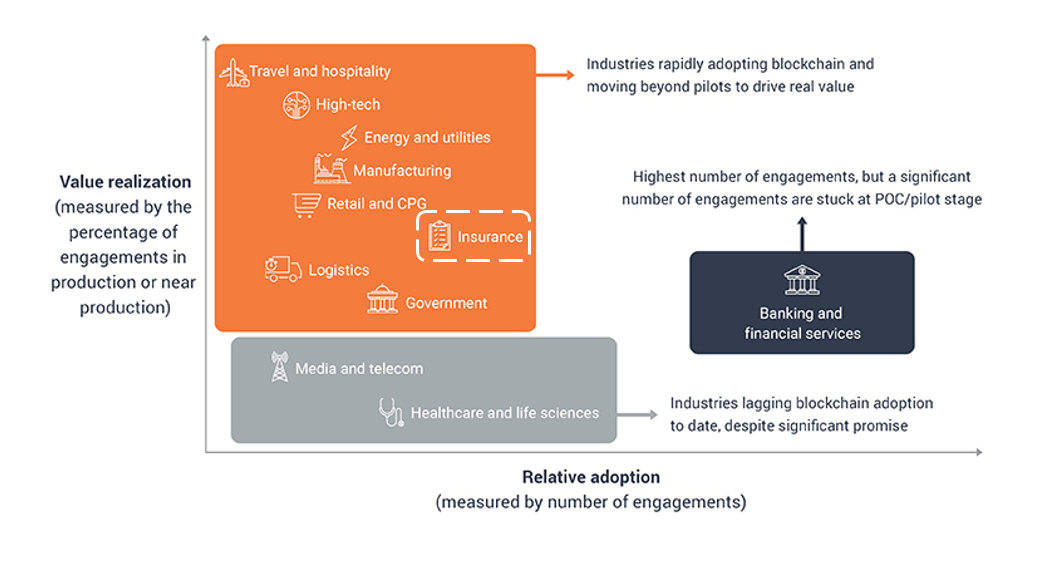

Exhibit 1 shows the extent to which business leaders are adopting blockchain technologies, with insurance carriers showing a positive reaction. And IoT is the same, For example, in the UK automotive industry, some insurers deployed IoT “black boxes”’ to willing customers that allow the carrier to examine risk more effectively in exchange for a lower premium. While on the face of it the program showed somewhat limited success with only 14% of motorists advising they would choose one of these policies, the policies do cater effectively to a market segment where premiums are punishingly high,

Exhibit 1: The insurance industry is rapidly adopting blockchain

Sample: 550 blockchain engagements across 15 blockchain service providers

Source: HFS Research, Top 10 Blockchain Platforms 2018

A new wave of disruptors has expanded IOT for insurance beyond the meager black box to smartphone driven sensors. Two of these innovators are Zendrive and Root Insurance, which use smartphone sensors to measure driver behaviors like acceleration and phone usage. Zendrive uses the information for offerings like collision notifications, safe-driving discounts, and driver coaching. Differently, Root Insurance uses it to offer affordable insurance policies only to safe drivers, drastically reducing their risk.

But the real benefits emerge when insurers experiment with combining both IOT and blockchain, opening up the potential for new “live-time” insurance products. Suppose a sensor in a vehicle could collect and upload driver data to a blockchain solution where other sources feed in data such as weather reports and traffic information; insurers would have a system that allows them to measure risk in real-time and have oversight of any potential wrongdoing.

And live-time insurance solutions are already entering the market, one example is Insurwave, by EY and GuardTime, which provides a blockchain-enabled marine insurance platform that allows insurers to track their exposures in near real-time.

Blockchain is an essential ingredient for live-time insurance: smart contracts can automate changing premiums and quickly resolve disputes

Before the naysayers chip in questioning the role blockchain plays, the technology is vital because it can facilitate an insurer developing its own hyperconnected ecosystems (which we explained in previous research) to quickly resolve disputes with transparency and immutability and enable smart contract roll-out, a necessary evolution for the industry.

If the market adopts live-time insurance, insurers must avoid a never-ending stream of accompanying manual labor, where employees constantly adjust premiums in response to new data. Smart contracts enable automatic adjustments in response to these changes, as well as policy changes submitted by customers. For insurers, this means driving down labor costs while quickly adapting policies to new circumstances and resolving disputes and claims with the speed and ease consumers are increasingly demanding.

Live-time insurance products won’t be an overnight success; there are privacy concerns that mean insurers’ goals must remain realistic

We can blame the shortcomings of the black box movement at least partially on the intrusive nature of the product. In fact, 56% of motorists claimed one of their main problems surrounding them was that they are not comfortable with sharing their personal driving data with insurance providers. This reluctance presents a hurdle that insurers must overcome if they hope to launch a data-driven insurance product.

The Bottom Line: The insurance industry needs to adapt to a rapidly changing market; it can no longer rely on traditional models as the sole source of revenue.

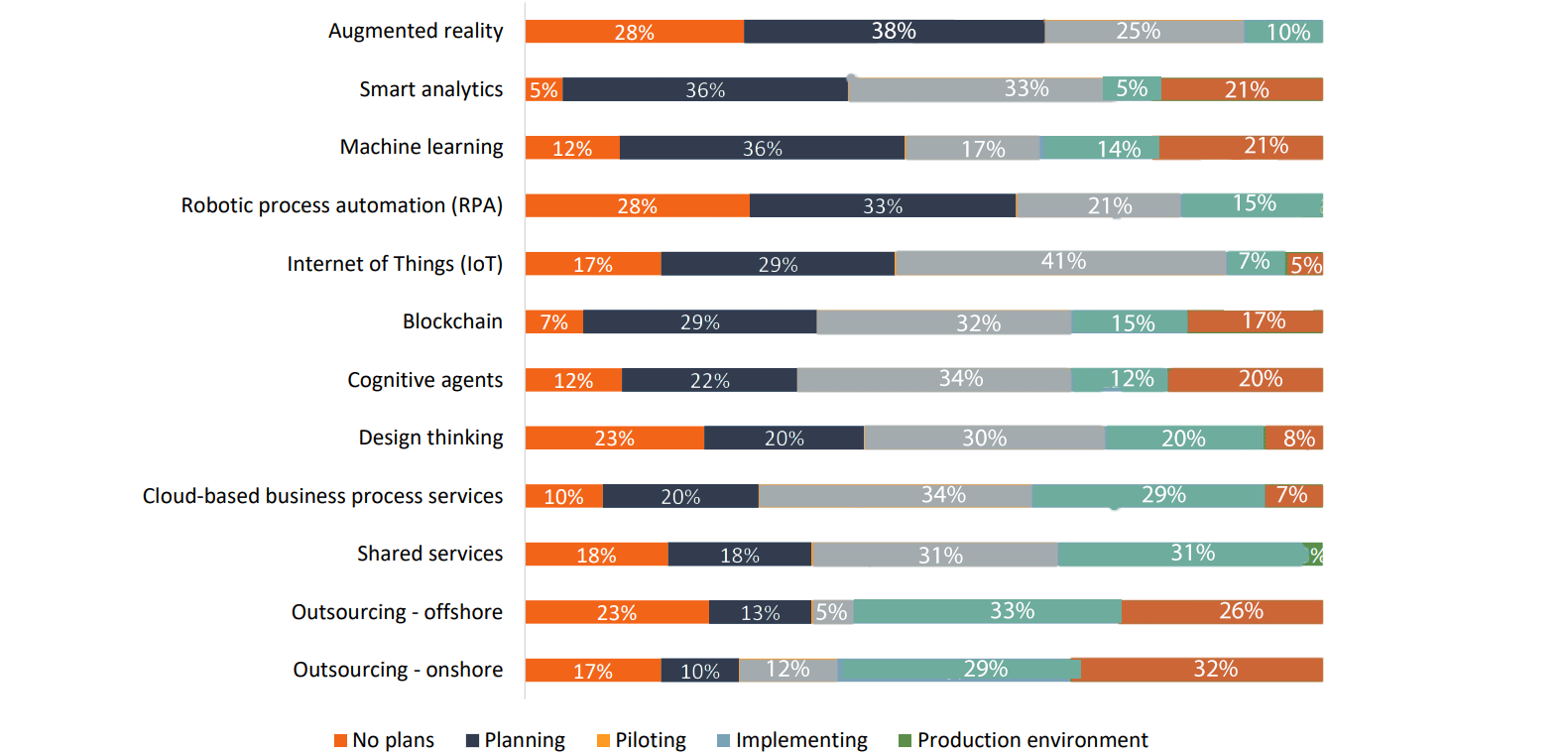

Consumers want speed and flexibility, but they are less keen on risking their habits feeding higher risk profiles. For example, 19% of motorists said they didn’t want to risk their insurance premiums going up after purchasing a black box insurance policy. The reality is that the insurance market needs to diversify its capabilities—there will still be a market for traditional policies, but there is also a growing market of consumers looking for cheap and flexible insurance products that entrenched firms are unable to provide. When looking to adapt, blockchain and IOT should be the champion change agents in the field as they can drive down operating costs, develop hyperconnected ecosystems, and enhance customer experience, but Exhibit 2 shows it is a long road ahead for insurers.

Exhibit 2: Insurers are still in planning and pilot stages with many change agents

Please characterize your organization’s current use of the following value creation levers to achieve the business outcomes described in the previous question

Sample: 39 insurance companies and 318 from other sectors

Source: HFS Research, Industry Blueprint: Insurance Operations Services 2018

Register now for immediate access of HFS' research, data and forward looking trends.

Get StartedIf you don't have an account, Register here |

With the exception of our Horizons reports, most of our research is available for free on our website. Sign up for a free account and start realizing the power of insights now.

Our premium subscription gives enterprise clients access to our complete library of proprietary research, direct access to our industry analysts, and other benefits.

Contact us at [email protected] for more information on premium access.