The banking and financial services (BFS) market is big. The Banker’s Top 1000 World Banks Ranking for 2018 reports that total assets reached $124 trillion; the BFS industry’s extensive use of IT positions it as a large part of the IT services market. However, the BFS industry’s previous success could also prove to be its downfall, as some IT service providers rely heavily on BFS revenues to drive their own growth. Take Cognizant, for example: Since 2015, its financial services vertical has contributed an average of 38.4% of total revenue, and the firm’s total growth is closely correlated to the vertical’s growth (see Exhibit 1).

Cognizant isn’t the only firm with this precarious reliance on BFS; many other service providers must change things up quickly, or they also risk leaving themselves at the mercy of a single industry. A dip in performance, a major shift in the banking industry driven by current fintech and a digital wave, or even another financial crisis could cause a large portion of BFS service providers’ revenue to disappear overnight.

Exhibit 1: Cognizant’s financial services growth perfectly correlates to its total growth, Q1 2015–Q1 2019

Source: HFS Research and Cognizant’s quarterly earnings reports

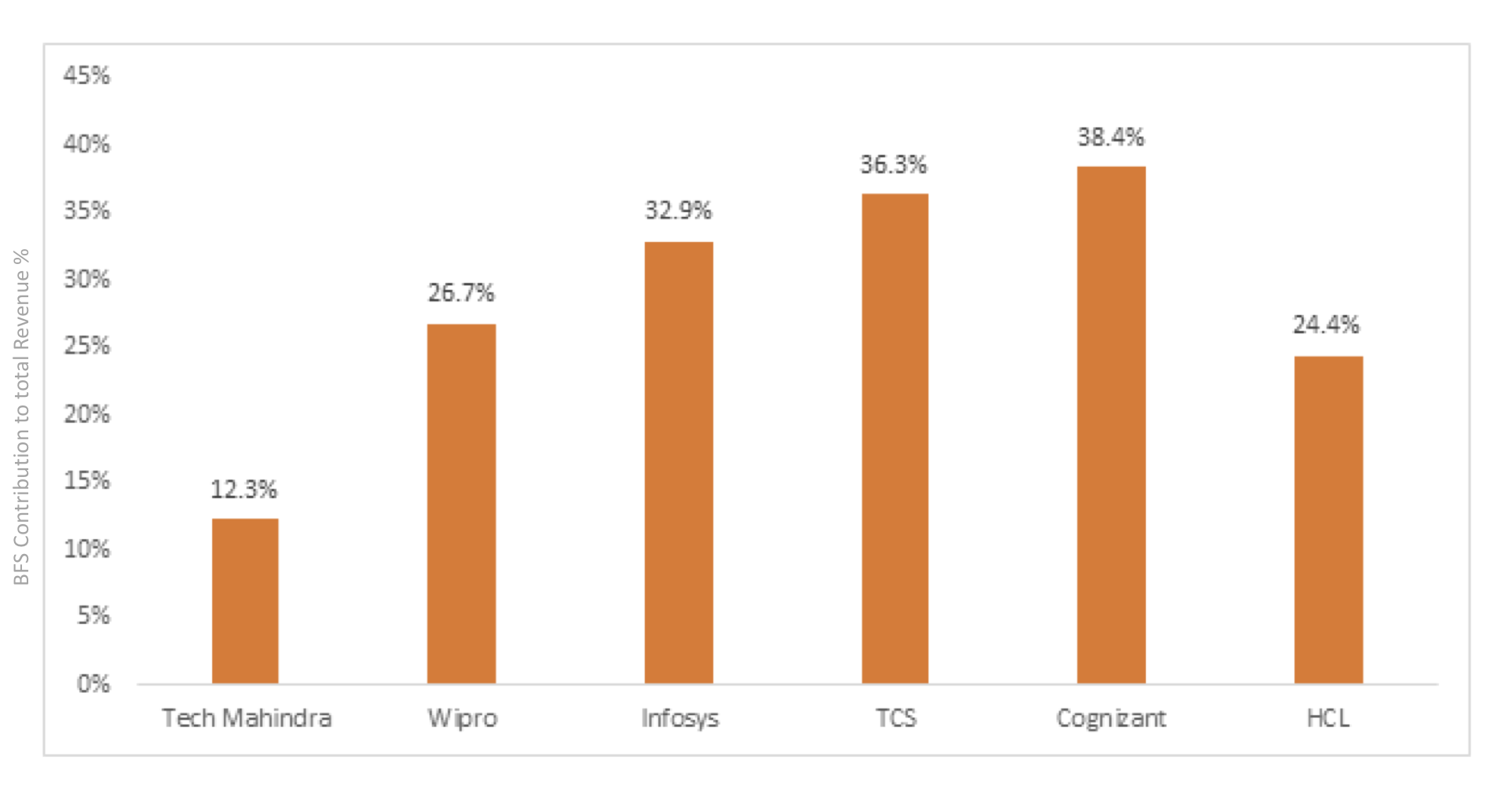

The problems extend beyond a single service provider—BFS contributes more than 30% of a majority of TWITCH firms’ total revenues

We examined the quarterly results of the TWITCH providers (see Exhibit 2), and found that four of the six companies earn more than a quarter of their revenues from their respective BFS verticals. This clear dependency on a single vertical leaves most of the largest service providers exposed to a substantial risk.

Exhibit 2: Banking and financial services verticals contribute a significant amount to every TWITCH provider’s revenue, average BFS contribution to total, Q1 2015–Q1 2019

Source: HFS Research and TWITCH service providers’ quarterly results

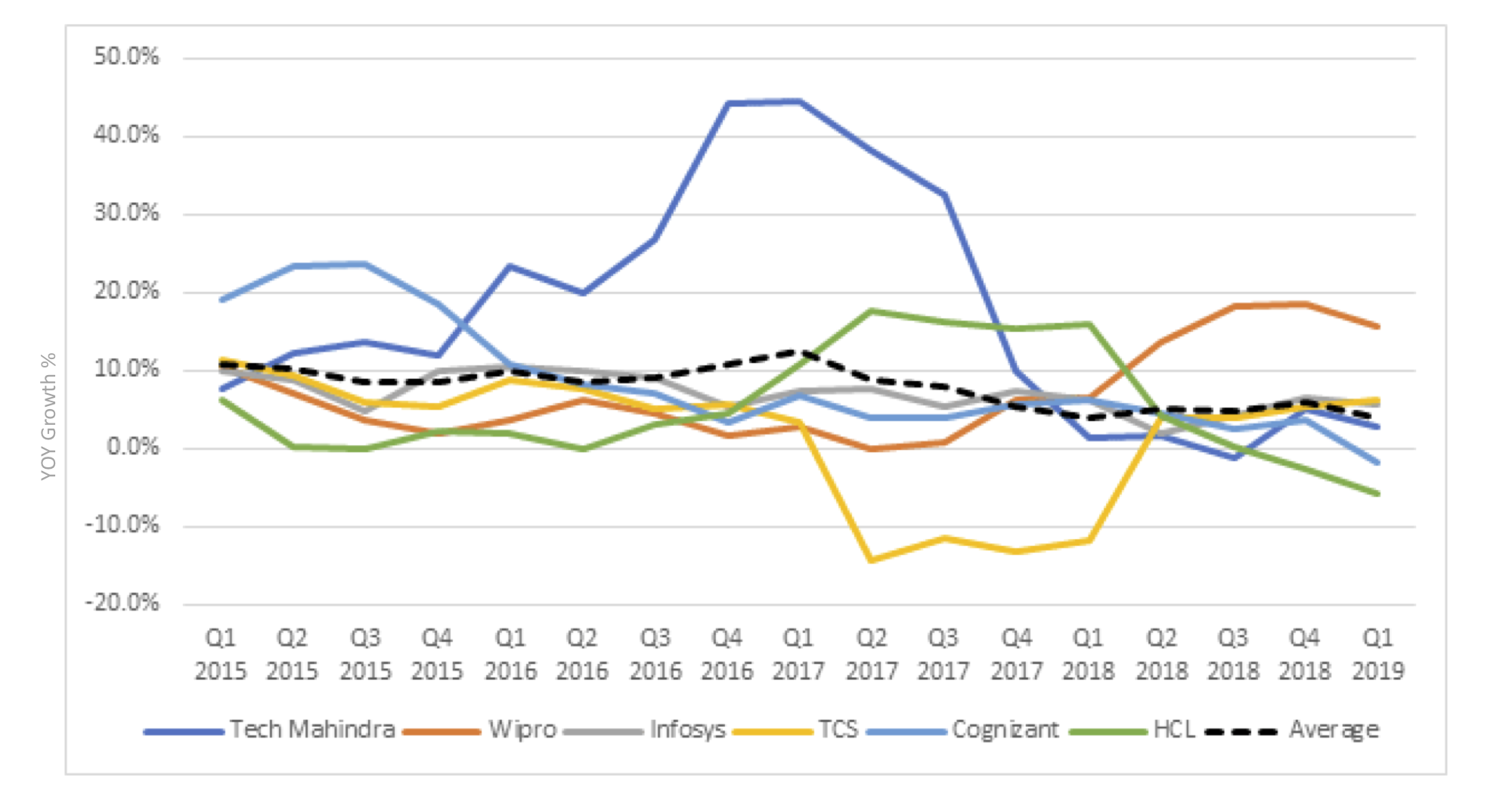

Banking and financial services has a volatile growth history, but the slowdown has already begun—TWITCH providers are running out of time to broaden their horizons

Single industries are left to suffer the highs and lows of their craft, and revenues are affected by anything ranging from consolidation to seasonality. Additionally, the BFS space is highly competitive. All the service providers compete aggressively for the same business; however, the difference for the BFS industry is that while it has remained volatile, there is a consistent theme of slowing growth (see Exhibit 3).

The TWITCH providers’ competitors, regardless of size, must understand that relying on a single industry vertical can lead to a strong correlation between the industry’s and the firm’s overall success—wonderful in an upswing but potentially disastrous if things turn sour.

Exhibit 3: TWITCH providers’ year-over-year BFS vertical growth, Q1 2015–Q1 2019

Source: HFS Research and TWITCH service providers’ quarterly results

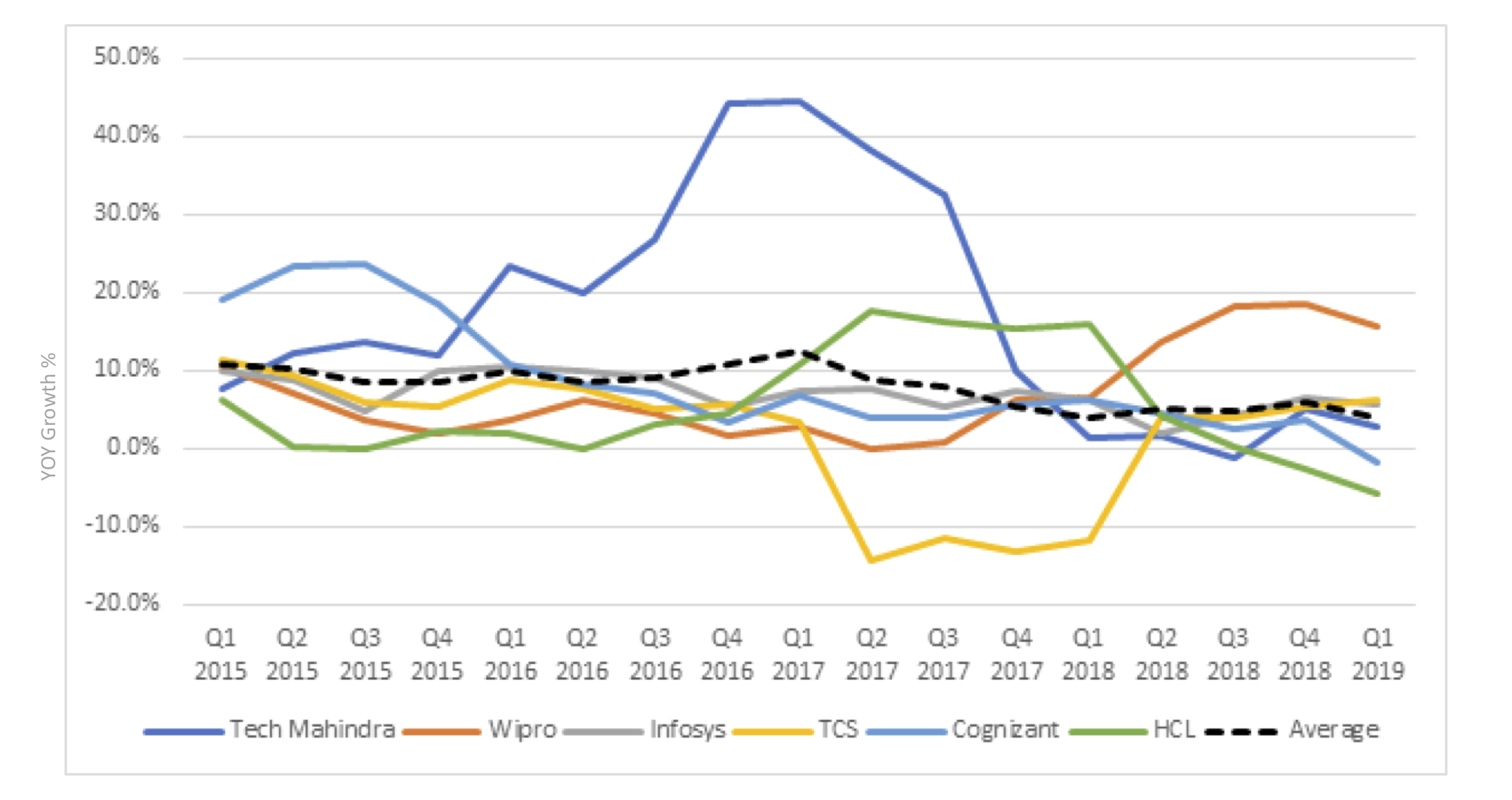

Not every TWITCH provider has fallen in the same trap—HCL may be setting the example its competitors need to follow

While providers’ overall growth tells a similar story of volatility, shown in Exhibit 4, HCL has consistently delivered double-digit growth and is one of the fastest-growing TWITCH providers. HCL is one of the two TWITCH providers that gain less than a quarter of their total revenues come from banking and financial services. To their competition, this data must signal that there is a strong possibility that investing in a range of verticals and spreading risk is a solid system for growth that can protect them from any dip in the performance of a single vertical.

Exhibit 4: Total YoY growth for TWITCH providers, Q1 2015–Q1 2019

Source: HFS Research and quarterly results of TWITCH service providers

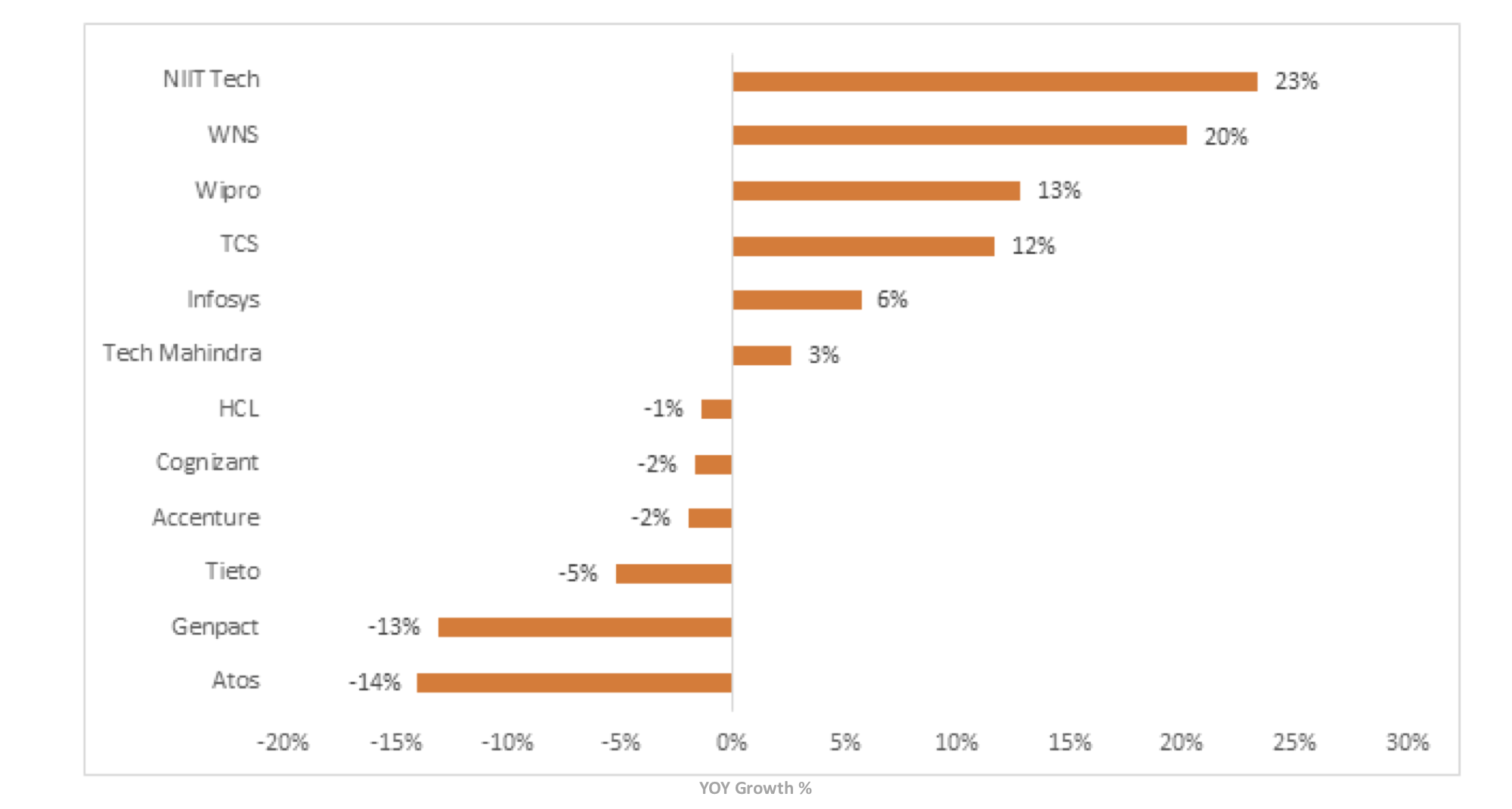

It’s not all doom and gloom—while some providers struggle, others find great success in their BFS vertical.

There is a clear overreliance on the BFS vertical, but it isn’t all bad news. Some service providers are experiencing a slowdown in growth, true, and others are even seeing an outright decline—but some are posting double-digit growth. Exhibit 5 displays the four biggest BFS winners and losers for Q1 2019, plus any TWITCH providers not in one of those two categories. Elevated IT service activity in the BFS space has attracted competition, which is making it difficult to succeed in the market. Smaller firms have recently recorded some of the highest growth rates, with WNS and NIIT Technologies showing double-digit growth and total revenues between $200 million and $300 million for the quarter.

One of the main takeaways from this is the shocking gap between the winners and losers. On one end, NIIT Technologies reported YoY growth of 23% and WNS 20%, while for the same period Genpact and Atos posted double-digit declines. Although we should note that Atos growth in Q1 2019 was negatively impacted by the divestiture of Worldline – Atos’s Q1 2019 results show an organic growth of 1.3% for its financial services business.

Exhibit 5: The winners and losers of banking and financial services, Q1 2019

Note: Atos growth impacted by Worldline divestiture – organic growth for Q1 2019 was 1.3%

Source: HFS Research and service providers’ quarterly results

The Bottom Line: By relying on the banking and financial services market for a sizeable portion of revenues, service providers leave themselves open to unnecessary risk. To mitigate this, they must diversify and invest in a wider range of verticals.

It’s clear that some providers are overly dependent on BFS, and while there is a possibility of continuing success, the increasing levels of competition and chance of existential disruption of the traditional banking sector could leave exposed providers lagging more diversified competitors. If these providers hope to continue delivering consistent and sustainable growth, they must spread the risk posed by an overreliance on BFS by investing in a range of verticals—cushioning negative consequences of future slowdowns or outright crises in the BFS space.

Register now for immediate access of HFS' research, data and forward looking trends.

Get StartedIf you don't have an account, Register here |

With the exception of our Horizons reports, most of our research is available for free on our website. Sign up for a free account and start realizing the power of insights now.

Our premium subscription gives enterprise clients access to our complete library of proprietary research, direct access to our industry analysts, and other benefits.

Contact us at [email protected] for more information on premium access.