Increasingly everything, including voice, is data. Over the past two decades, beleaguered and consolidating telcos upgraded their networks at an extraordinary expense, enabling digital natives to slurp revenues over-the-top (OTT) and out of telco pockets. We see displacement across the telecoms landscape from cable and satellite operators losing share of wallet to Netflix to Facebook’s WhatsApp replacing mobile operators’ once highly popular and profitable SMS service. In the current era of hyper-connectivity, the emerging possibilities for connecting the last mile could well change the game completely. Facebook’s Mark Zuckerberg has described connectivity as a “human right.” The potential for disruption and disintermediation is high and telcos need to look beyond cost cutting and innovate their offerings and operations.

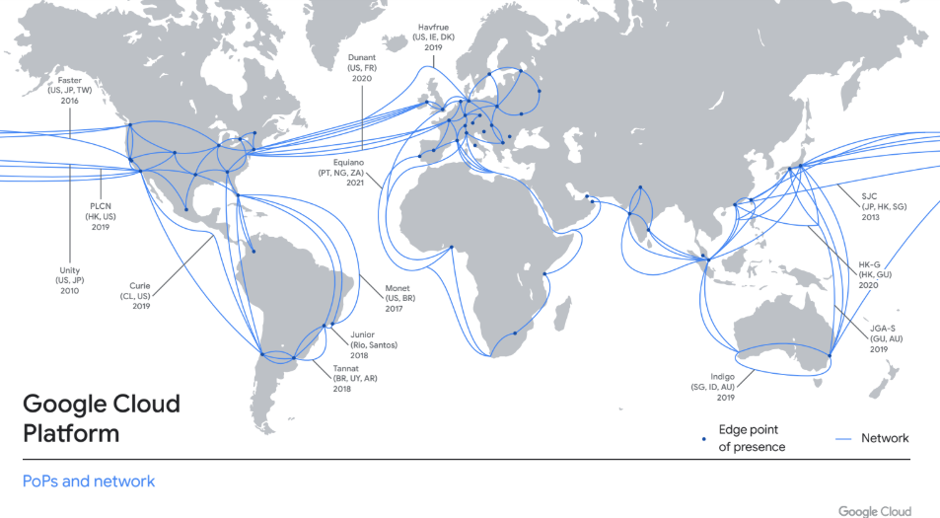

Tech giants are investing heavily in cable projects that form the backbone of the internet’s global connectivity. Many are consortium-owned, such as MAREA and Jupiter. Some are private, such as Google’s Junior, Curie, and Dunant (see Exhibit 1). Along with data-center investments, these cables create extremely large private networks. Commentators have long presupposed the threat these growing networks present to telecoms providers.

Exhibit 1: Google’s network is one of the largest private networks in the world, headed toward 73 zones across 24 cloud regions in 2020

Source: Google, 2020

New network initiatives involving tech giants are on the rise (and SpaceX is setting up Starlink too).

In tandem with their growing networks, the brand power of Big Tech is second to none. Interbrand’s best global brand rankings place Apple, Google, Amazon, and Microsoft in places 1-4 for 2019. No telcos appear in 2019’s top 100 global brands. Strong brands invoke trust, influence customer choice, and create loyalty. They also attract, retain, and motivate talent. Arguably, nothing but a massive tech backlash could impact these brands unfavorably. What appears more likely in the current climate is that they will be broken into smaller companies, diluting the brands’ power in the process.

What people love about consuming Big Tech’s delights is the simplicity of engagement. Digital natives know how to onboard and serve their users, making it easy to consume. Big Tech is not facing the cost pressures, complex legacy systems landscapes, and convoluted business processes that serve to frustrate telco employees and customers alike. On the contrary, wildly profitable tech giants are far more capable of investing in data-driven operations than legacy telco players.

Connectivity was traditionally something that consumers paid to “access.” A paradigm shift started when Google and Facebook began to monetize their offerings, still widely misunderstood by too many to be free offerings of search and social media, respectively. But, the main product they sell is ads to eyeballs. Digital advertising targeting is at a level of granularity that enables powerful options in segmentation that were unprecedented at scale by any previous media form. Despite Facebook deriding Cambridge Analytica’s data science offering as snake oil, the world began to understand the mechanics and sheer scale of targeted digital advertising as that scandal unfolded. Both Facebook and Twitter are experimenting with versions of their platforms and user settings to reduce the data load for users that are sensitive to data volumes, whether to manage financial costs or environmental ones.

Today, the myriad of wireless options from wi-fi to wireless mesh networks (WMNs) are better, faster, and more resilient than in the past. As more high-throughput wireless networks begin operating using consistent policies across wireless and wired networks, the possibilities become infinite. Traditional access mechanisms are at risk of becoming less relevant as other means of connectivity improve.

WMNs are organic, bottom-up networks upon which only some devices (or even just one) require an internet connection. They can form, disperse, and re-form (self-form and self-heal) quickly and easily. So WMNs enable communication anywhere, at low cost, and without fixed infrastructure. Before being purchased by Cisco, Meraki was on a mission to deliver wi-fi through volunteers and mesh networks across San Francisco. Peer-to-peer messaging can work with or without internet access or cellular data to send text and images—even during natural disasters. Is this robust enough to support corporate communications or gamers? Probably not. Yet. But like Moore’s law for compute, WMNs are steadily becoming stronger and faster.

The Bottom Line: As connectivity options expand and interoperability improves, telcos need to increasingly step up the digitization of operations and innovate beyond current offerings of connectivity to keep pace with digital natives. Persistent cost-cutting to shave pennies off operations will not suffice.

Where tech giant’s business models rely on network effects or the volume of users to make their commercial product offering compelling, they will facilitate users’ access to grow and maintain that network. Along with more efficient data formatting, we can clearly see the seeds of subsidies and supported consumers’ connectivity, much like a product retailer offering free delivery. The networking mechanism that ultimately disrupts is not the point; advances in interoperability will probably prove more crucial than any single networking method alone.

The point is there are new ways to connect, and they keep getting better; the tech giants look like they are onto this fact and advancing toward providing connectivity sometimes commercially and sometimes for free. The question is how far they will get across that last mile of connectivity, especially when they bypass telcos. Facebook’s Free Internet Initiative was welcomed in Africa, but the Indian telecom regulator stopped it—it looks like a “new colonialism”. Facebook-led Internet.org met with strong backlash. Now Facebook is collaborating with telcos, tech vendors and academia on the Telecom Infrastructure Project (TIP).

Telcos’ network investments must yield top-line revenue growth, or telcos run the risk of being in the unfortunate position where they build more network capacity for the commercial benefit of others who are simultaneously exploring alternative means of connectivity.

Register now for immediate access of HFS' research, data and forward looking trends.

Get StartedIf you don't have an account, Register here |

With the exception of our Horizons reports, most of our research is available for free on our website. Sign up for a free account and start realizing the power of insights now.

Our premium subscription gives enterprise clients access to our complete library of proprietary research, direct access to our industry analysts, and other benefits.

Contact us at [email protected] for more information on premium access.