Enterprise technology leaders are drowning in AI commentary. LLMs. Agents. Vibe coding. The analyst decks keep coming. But the hard question nobody is answering is this: Who actually wires AI into your live systems, governs it in production, and makes it keep working when the AI software vendors leave the room? The answer is forward-deployed engineering (FDE). If your transformation strategy does not have it, you are building an AI theater, not an AI operating model.

93% of enterprises are stuck in AI pilot purgatory. The missing layer is not better models or bigger budgets. It is forward deployed engineering, and the firms that crack it at scale will own the recurring revenue layer of enterprise AI.

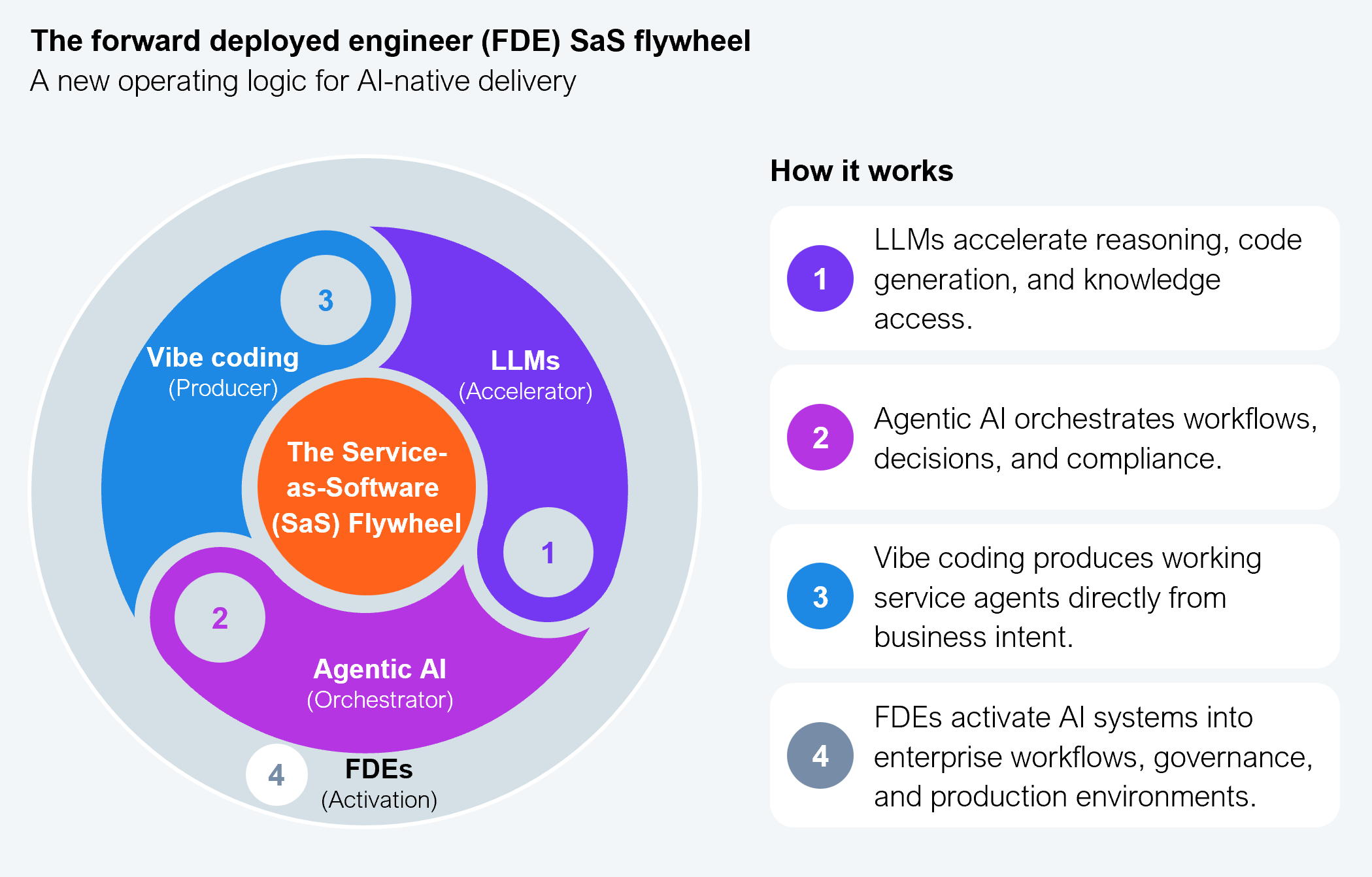

The HFS Services-as-Software Flywheel has four accelerants:

The result is a compounding system where intent becomes production workflows, workflows generate data, and that data improves the next generation of agents.

Source: HFS Research, 2026

The missing insight in many AI strategies is that velocity alone does not create enterprise value. The Services-as-Software flywheel requires an embedded execution layer that connects these technologies inside real operational systems. FDE forms that layer, ensuring the flywheel spins inside production environments rather than inside sandbox pilots. Here is what happens without FDE:

The Flywheel does not spin because there is no embedded engineering force to connect the components inside real systems. That is the dirty secret of AI services. The gap is not technological. It is operational. Services-as-Software does not eliminate services. It embeds them deeper into the software. FDE is the mechanism that makes that shift real.

Palantir built its competitive advantage not on model superiority but on proximity to operational reality, with forward-deployed engineers embedded inside client environments, wiring models into live data, real permissions, regulatory controls, and the messy ontologies that reflect how enterprises actually function. They did not sell transformation roadmaps. They shipped production workflows.

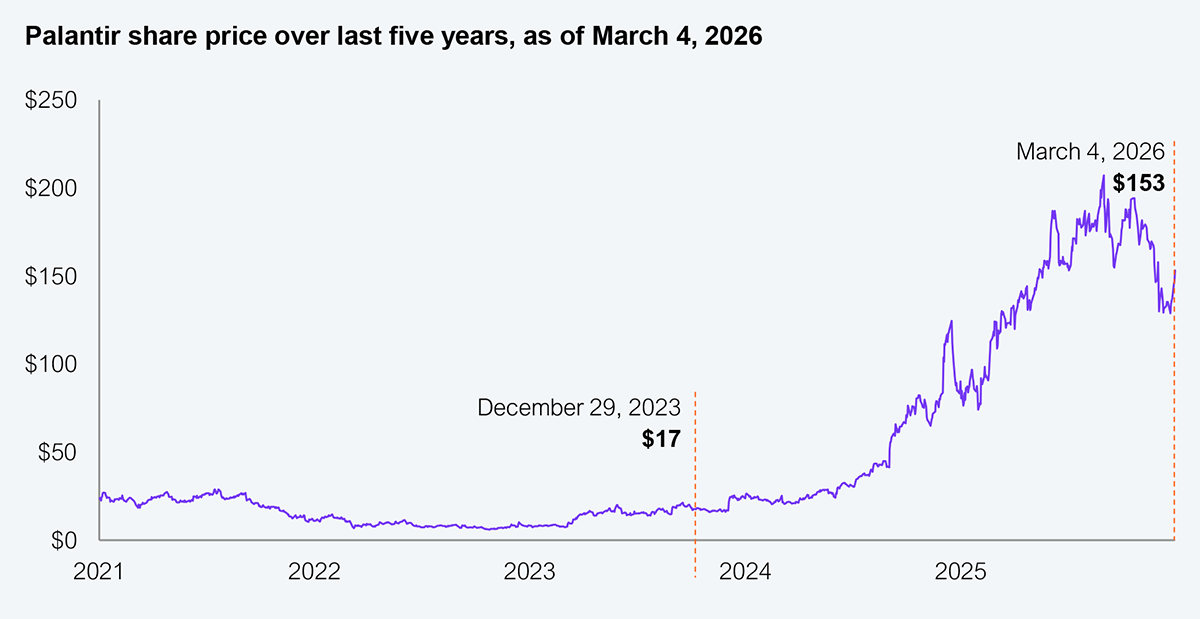

The market is increasingly recognizing this model. Palantir’s share price has increased roughly 10x in the past two years, reflecting investor belief that the future of enterprise AI lies not just in models, but in the ability to embed those models into operational systems.

Source: Investing.com (March 6, 2026), HFS Research

That approach is now being industrialized through AIP Bootcamps, which are structured engagements that take a team from a scoped problem to a working production deployment in one to five days. Not a proof of concept in a sandbox. A live workflow with real data and real controls. That changes the entire commercial dynamic.

There is a persistent misunderstanding in the market. FDE is often conflated with systems integration or technical implementation. It is neither. FDE is the discipline that turns AI capabilities into durable enterprise mechanisms. The Palantir model makes this concrete: FDE teams build ontologies that reflect how the enterprise actually operates, wire models into real data with real permissions, and design the governance architecture that keeps autonomous systems accountable.

On their own, LLMs cannot perform the required operational work:

FDE teams own all of that. The cost of not having them is not a missed optimization. It is a compliance event, a reputational failure, or an AI system that quietly degrades until someone notices the outputs stopped making sense.

LLMs accelerate. FDE operationalizes. Without the second, the first is a liability, not an asset.

Agentic AI is the most significant shift in enterprise technology in a generation. Agents can trigger workflows, coordinate decisions across systems, execute multi-step logic, and enforce compliance rules in real time. But autonomous workflow proliferation without governance architecture is dangerous in regulated industries.

A financial services firm cannot allow agents to make credit decisions without explicit decision rights, immutable audit trails, escalation paths, and human override mechanisms. A healthcare system cannot let clinical workflow agents operate without continuous performance monitoring and documented accountability chains. This is not a chatbot problem. It is a systems engineering problem, and FDE is the only delivery model currently designed to solve it at enterprise scale.

FDE solves this because it delivers the governance architecture that autonomous systems require:

Vibe coding lowers the barrier to building service agents to near zero. Business analysts can express intent and receive working agent code in return. That is a structural change in enterprise operating capacity. It is also a fragmentation risk without an engineering discipline layer.

When every business unit spins up agents independently, you get redundant logic across siloed codebases, compliance exposure from agents built outside the governance perimeter, and an AI estate that is technically diverse but operationally unmanageable. The firms in the Palantir ecosystem, building reusable ontology libraries and control frameworks for specific verticals, are creating precisely the discipline layer that makes vibe coding sustainable. That is not a feature. It is a defensible competitive position with real switching costs attached.

FDE provides the structural discipline that keeps vibe coding productive rather than fragmented:

In a Services-as-Software market, the client is not buying a transformation roadmap. They are buying working outcomes, such as claims triage that runs autonomously, supply chains that self-correct in real time, and compliance systems that audit continuously.

The AIP Bootcamp proves this model is real: a structured engagement, one to five days, that lands a specific workflow in production with real data and real controls. Instead of selling a roadmap, you sell a working workflow, and the client sees production capability before committing to scale. That changes the entire conversation about what AI services should cost and how they should be structured.

The downstream commercial implications are structural:

FDE-service providers are no longer selling hours. They are selling production systems that keep delivering outcomes. That distinction separates the AI platform builders from the AI plumbers.

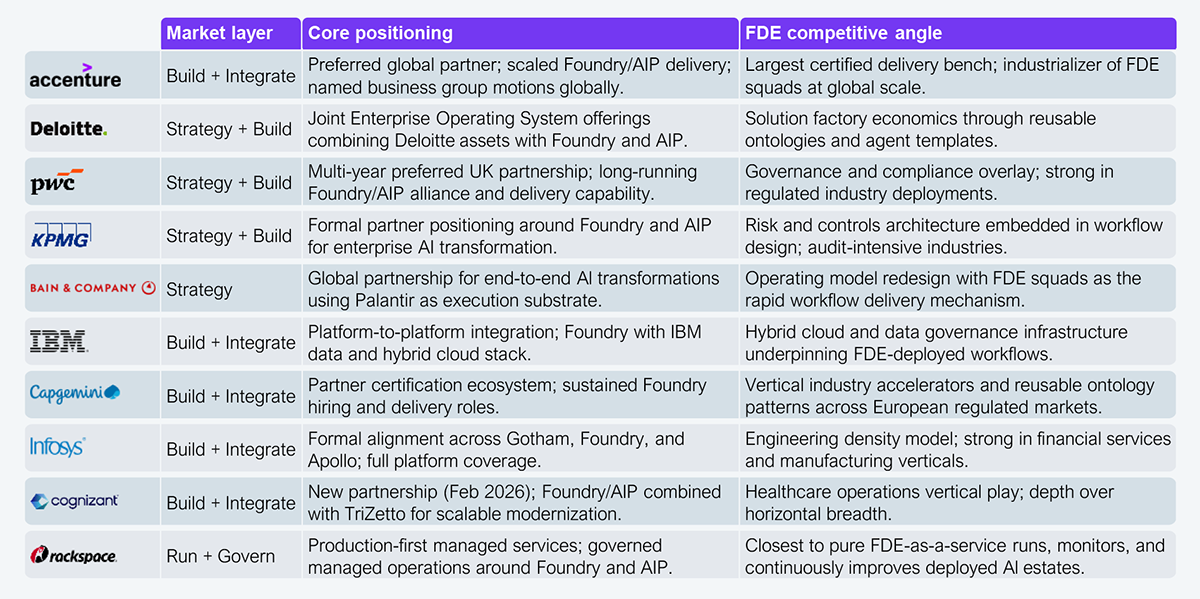

The partner lineup is significant not just for who is in it, but also for how it is splitting, with strategy-to-execution consultancies on one side and industrial-scale integrators and operators on the other. That split is not accidental. It is the three-layer market structure forming in real time.

Source: HFS Research, 2026

The Palantir partner ecosystem is the clearest early map of the market structure that will define enterprise AI services through the next five years. Three durable layers are forming, and the window to establish a defensible position is narrowing.

Layer A: Strategy and operating model redesign

Bain, Deloitte, PwC, and KPMG will own the AI operating system transformation layer. They define how enterprises restructure around AI-enabled workflows, with Palantir and other platforms as execution substrates. Competitive differentiation is proximity to senior leadership and the organizational change capability built over decades.

Layer B: Build and integrate

Accenture, Capgemini, Infosys, and Cognizant will compete on certified delivery capacity, vertical industry accelerators, and speed-to-production. The winners will build the largest libraries of reusable ontologies, workflow templates, and control frameworks for specific verticals. Switching costs accumulate here, and margin density improves over time. Accenture’s preferred global partner positioning signals a land-and-scale economics model already pulling away from the field.

Layer C: Run and govern

This is where Services-as-Software becomes genuinely recurring. Rackspace has made the most explicit move here, positioning governed managed operations as a production service with operational SLAs. As more workflows go live, demand for disciplined AI estate management becomes a standalone commercial category with high switching costs and defensible margin.

A critical dynamic cutting across all three layers is that government and regulated industries will disproportionately drive spend. Palantir’s center of gravity remains in defense, intelligence, and regulated enterprise, and it is expanding. Partners with existing clearances, regulatory delivery experience, and government relationships have a structural advantage that pure commercial integrators will struggle to replicate quickly.

Foundry’s ontology concept, modeling the enterprise as an interconnected operational system, is the stickiest element in the platform. Partners building deep, reusable ontologies for specific verticals are not just accelerating delivery. They are creating lock-in that travels with the client relationship and compounds with every additional use case deployed.

The firms still assembling their Palantir partnership and staffing for generic Foundry delivery are already behind. Ontology depth, workflow libraries, and delivery track record cannot be purchased quickly. The advantage is compounding in favor of early movers.

As AI-assisted building accelerates, services differentiation moves further up-stack into domain architecture, accountability frameworks, and measurable outcome guarantees. Providers competing on implementation capacity will find the floor dropping under them.

Enterprise technology leaders evaluating their service relationships need to ask a direct question: “Is this firm’s growth model built on expertise density or labor leverage?” The answer determines everything about value delivery in an AI-driven market.

Traditional IT services scaled revenue by scaling headcount. LLM acceleration and agentic automation are compressing the labor required per delivered outcome. A provider whose economics depend on headcount growth faces a structural margin problem regardless of what their AI partnership announcements say.

FDE-style delivery inverts the model: smaller squads, higher context density, faster deployment, higher-value outcomes, and recurring run revenue from systems they operate. The Palantir partner firms moving fastest on this are growing their expertise density and workflow libraries, not their headcount. That is the Services-as-Software endgame.

You are not choosing between AI vendors. You are choosing between providers who can deploy AI into production and those who will keep you in the pilot phase indefinitely.

Every quarter your enterprise spends in pilot mode is a quarter your competitors are driving production AI advantages. Demand FDE-capable delivery from your services partners, and measure them on production deployments, not roadmap slides.

If a partner cannot show a working workflow in your live systems within 90 days, they are not your AI transformation partner. They are your most expensive source of false confidence. The Palantir partner ecosystem has already shown what production-first delivery looks like. There is no excuse left for settling for anything less.

Register now for immediate access of HFS' research, data and forward looking trends.

Get Started

If you don't have an account, Register here |

With the exception of our Horizons reports, most of our research is available for free on our website. Sign up for a free account and start realizing the power of insights now.

Our premium subscription gives enterprise clients access to our complete library of proprietary research, direct access to our industry analysts, and other benefits.

Contact us at [email protected] for more information on premium access.

If you are looking for help getting in touch with someone from HFS, please click the chat button to the bottom right of your screen to start a conversation with a member of our team.