This Point of View is for health plan CIOs and operations leaders evaluating how Services-as-Software™ can rewire delivery to recover margins, drawing on an HFS Digital Roundtable conducted on April 9, 2026 with a dozen health plan technology and operational leaders.

Declining membership, out-of-control medical loss ratio (MLR), and shrinking margins must force health plan CIOs and operations leaders to abandon the operational status quo.

The path forward is Services-as-Software™: an AI-enabled delivery paradigm that shifts from people-based to IP-led delivery, orchestrates outcomes that matter rather than process management, and leverages telemetry to realize value rather than static KPI-driven contracts. This conclusion draws on an HFS Roundtable with a dozen health plan technology and operational leaders, conducted on April 9, 2026, in collaboration with Sagility, a growing healthcare-only service provider (see Exhibit 1).

Source: HFS Research, 2026

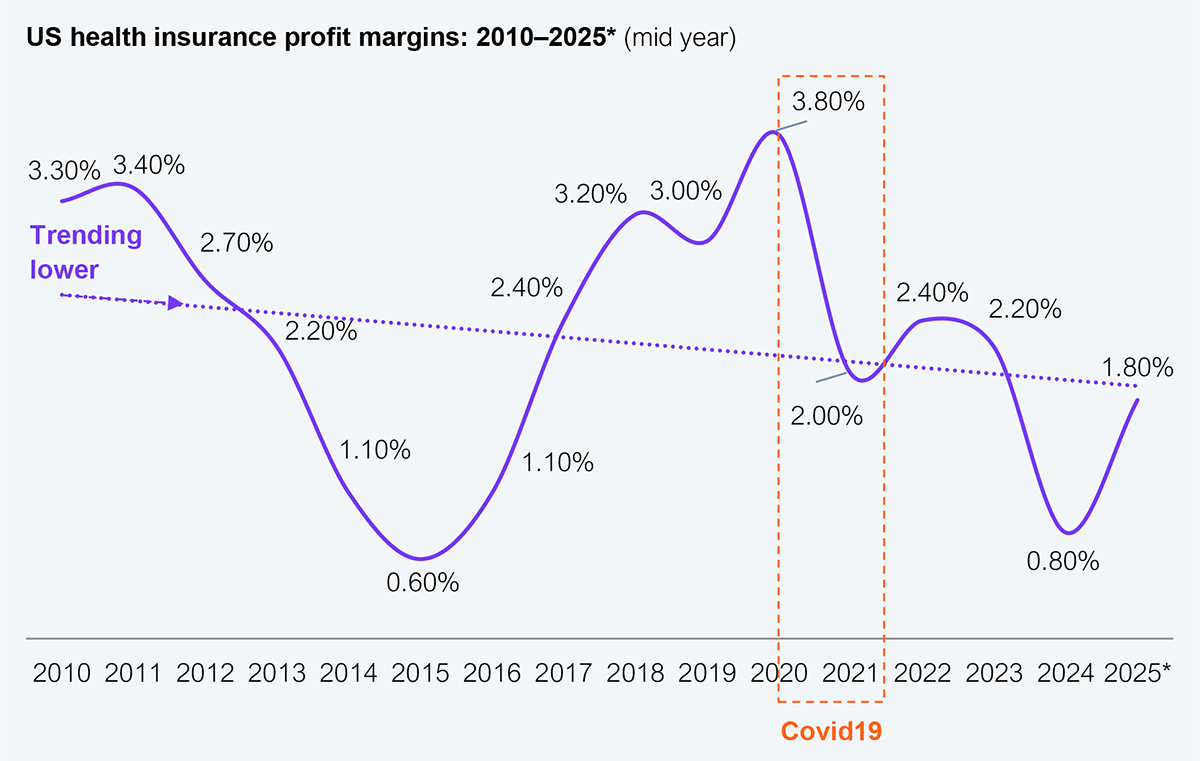

Health plan margins continue to deteriorate (see Exhibit 2) and will likely accelerate due to rising medical costs (MLR), underwriting accuracy as membership mix shifts, and administrative inefficiencies. Margins have been treading water for over a decade at this point, and the trajectory is decidedly downward and accelerating post-pandemic.

Source: NAIC (1000+ health plans reporting), HFS Research, 2026

To address margin deterioration, health plans are taking two key approaches: one to address administrative costs and the other to address out-of-control medical costs.

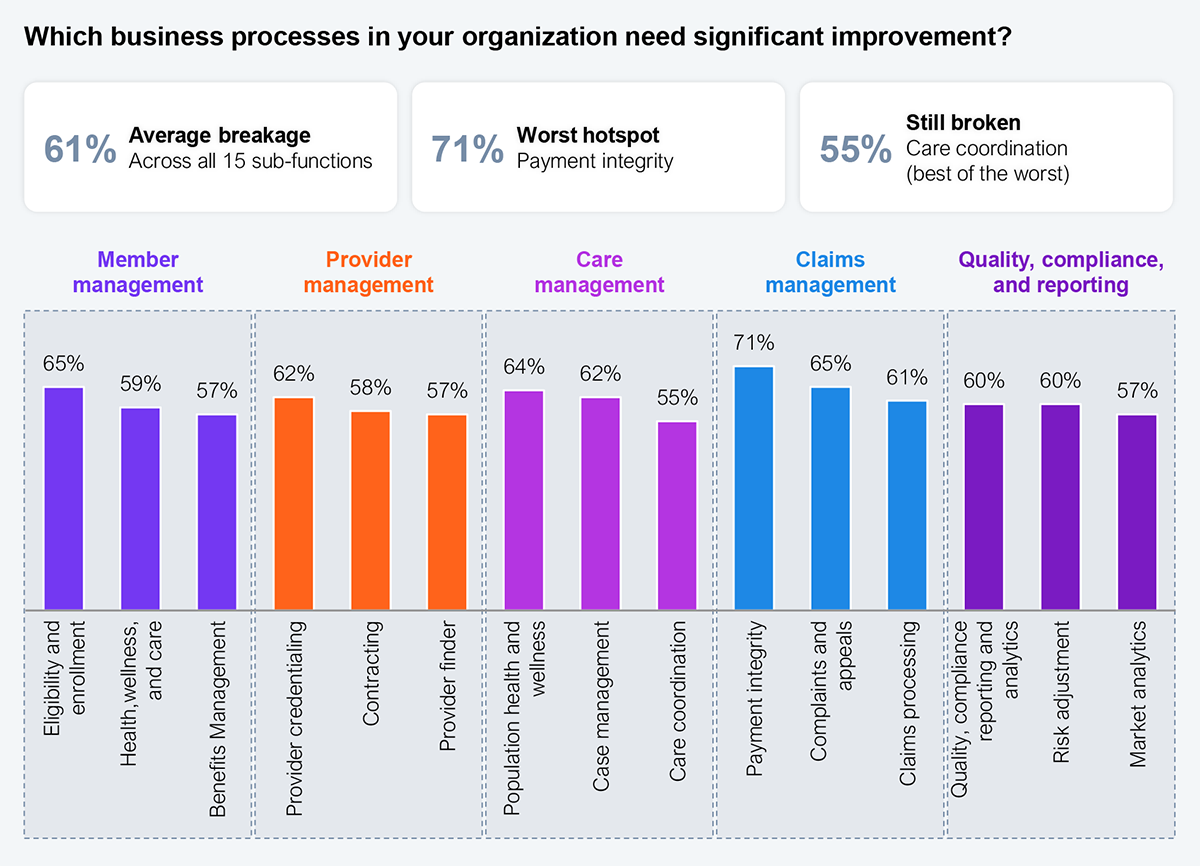

As health plans seek to address their financial challenges, a place to look is at the value chain that drives the outcomes. The health plan value chain was crafted in the last century to address challenges that have shifted significantly in the 21st century. An HFS study indicated that approximately 70% of the value chain is broken (see Exhibit 3), across claims orchestration, provider handoffs, and member experience, among others. Some in the panel alluded to the fact that applying AI to that value chain is a missed opportunity and a perpetuation of the same set of outcomes, albeit arriving there faster and potentially at a lower cost.

Sample: 107 health plan CXOs

Source: HFS Research, 2026

When AI is bolted onto legacy processes in the current value chain, governance, accountability, and the ability to scale outcomes will suffer. AI as a tool can enable the fail-fast trap by reaching the wrong answer more quickly when the underlying process is broken. Instead of eliminating steps in a process that made sense in the past, those unnecessary steps will continue to proliferate faster and at a cost that must be avoided when the value chain is not reimagined.

Everybody would agree that health plans are incredibly risk averse, and if we’re going to survive, we’ll have to adjust our calibration on risk.

— Midmarket health plan CIO

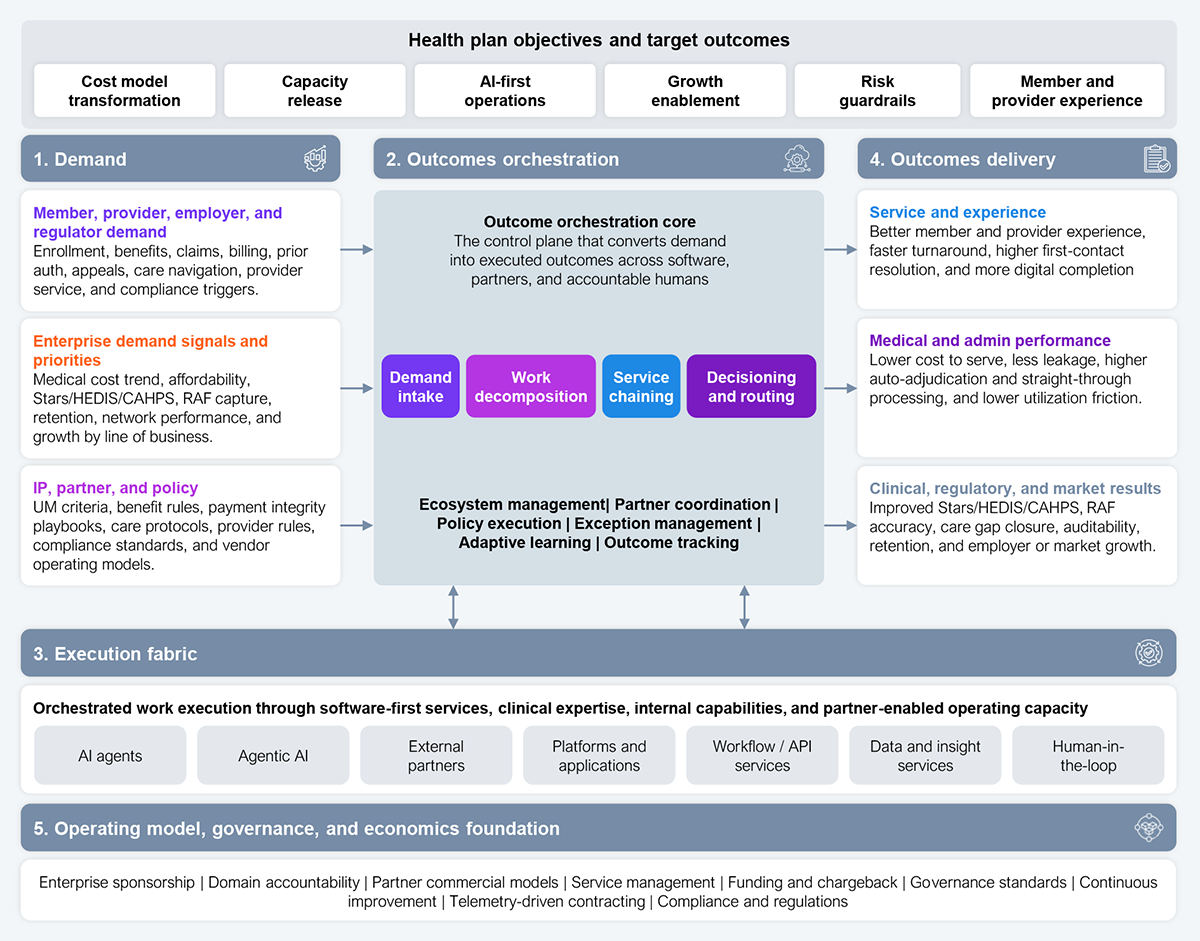

AI must be a catalyst for reimagining the health plan value chain as health plans adjust to their new realities and create value for their stakeholders. Outsourcing harder, pruning membership, and bolting AI onto legacy workflows all leave the value chain intact; only Services-as-Software rewires it. A comprehensive business architecture (see Exhibit 4) clarifies how health plans must rewire the value chain.

Source: HFS Research, 2026

At a practical level, many in the panel indicated that governance must shift away from the traditional path, where the questions include “Did the vendor meet the service-level agreement (SLA)?” “Did the team process the queue?” and “Did the cost per full-time equivalent (FTE) go down?” Governance must shift toward Services-as-Software (SaS) with questions such as “Did the model reduce avoidable work, improve speed and quality, preserve trust, and create measurable financial and member and provider value?” Similarly, exceptions should not be “fallouts” but must be designed up front, where they are not edge cases but the core of autonomy. SaS moves controls into workflows rather than relying on quarterly compliance reviews.

Claims are foundational to the health plan business. Over the years, health plans have invested in technology, process reengineering, and partnerships to enhance claims management, reduce costs, reduce provider abrasion, and improve the member experience. Yet, they have fallen short for a variety of reasons. SaS can enable touchless claims management only if it is treated as an end-to-end outcome orchestration model, not as another claims automation layer. That agentic-enabled orchestration can occur to enable a true touchless claim by moving from intake to payment, denial, pending, appeal prevention, or recovery with no human touch unless a governed exception threshold is breached.

The current state of claims operations treats exceptions as part of claims work. SaS manages exceptions as signals to redesign the software-led claims outcome engine. The key is that humans are not the production model. They are used only when the orchestration layer cannot safely complete the claim.

AI is not just a tech thing; it’s about business process orientation.

— Health plan data analytics leader

This fundamental shift in operational approach will allow for telemetry-driven meaningful measures that matter, such as these:

The first move is to treat claims as the proving ground for an end-to-end outcome orchestration model, not as another automation layer on top of the existing process. Then, replace SLA and cost-per-FTE dashboards with telemetry: safe no-touch rate, exception recurrence, payment accuracy, appeal and overturn rate, and provider abrasion. Ultimately, the choice is to keep tuning legacy claims automation while MLR pressure compounds and AI investment underperforms or to make humans the exception, not the production model, and let the orchestration layer carry the volume.

Register now for immediate access of HFS' research, data and forward looking trends.

Get StartedIf you don't have an account, Register here |

With the exception of our Horizons reports, most of our research is available for free on our website. Sign up for a free account and start realizing the power of insights now.

Our premium subscription gives enterprise clients access to our complete library of proprietary research, direct access to our industry analysts, and other benefits.

Contact us at [email protected] for more information on premium access.