This HFS Point of View, developed in partnership with Cognizant and Microsoft, is designed for media and entertainment CEOs, chief AI officers, and transformation leaders seeking to scale agentic AI across the content value chain.

The media and entertainment (M&E) industry is experiencing a growing divide between incumbent media broadcasters and tech-native media platforms. Broadcasters have become aggregators of leading IP and distribution platforms but still struggle with profit margins. Leading big tech media platforms, on the other hand, have reported double-digit profit margins. Publicly reported data indicates that tech-native platforms such as Netflix have achieved operating margins in the 30% range and annual revenue growth of over 20% in recent reporting periods (per company earnings reports and SEC filings), while legacy giants such as Paramount reported near-zero margins and a shrinking top line.

This divide appears to stem, in part, from rising content costs that may be outpacing revenue growth. Sports broadcasting is a visible example: rights costs keep climbing while audience fragmentation accelerates, exposing a disconnect with the core audience and an inability to build sustainable audience communities that can be monetized. To remain competitive, M&E CEOs must address their firms’ technical and process debt and leverage data and AI effectively to deepen audience engagement and improve monetization.

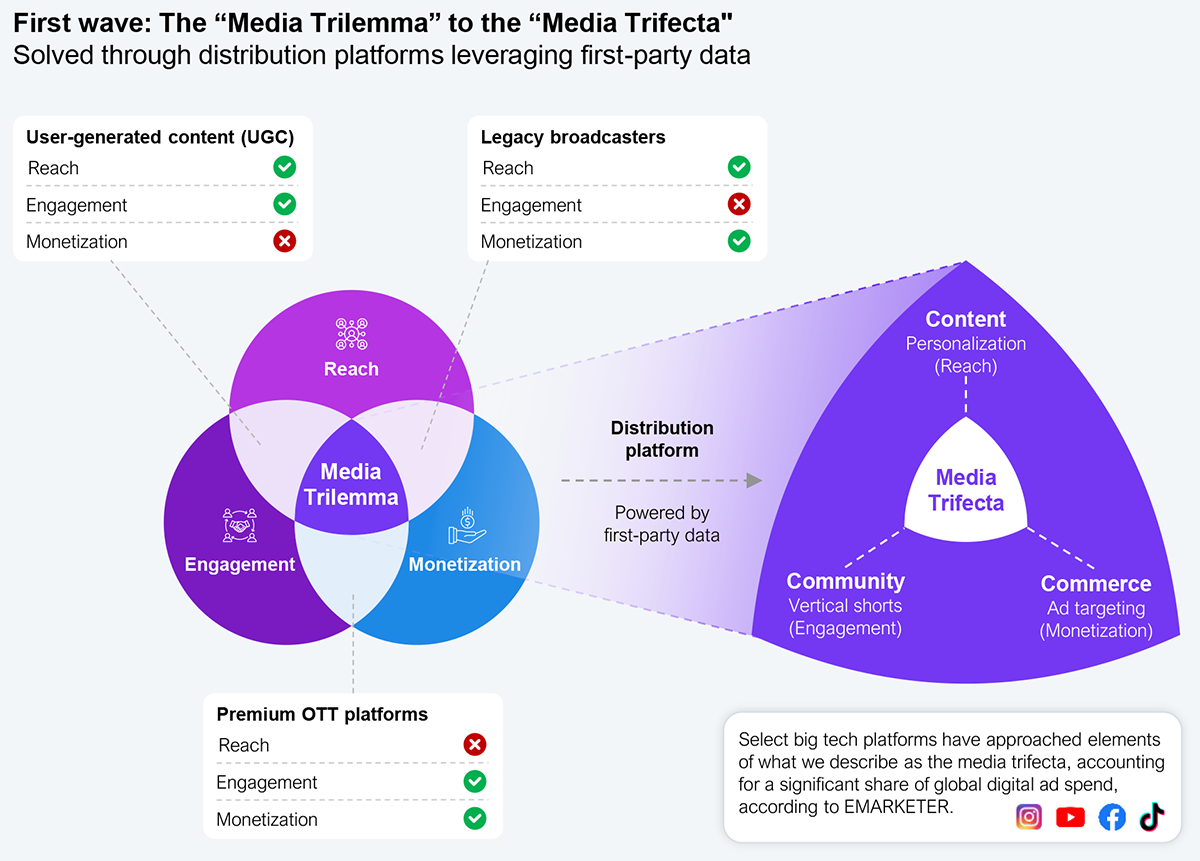

The three core pillars of the M&E industry are reach, engagement, and monetization. Legacy media houses controlled these three success factors before the streaming and mobile era by widely distributing a limited number of flagship IP, creating monocultural moments at scale. This pattern has been disrupted by the first wave of digital disruption with the rise of personalized content feeds on streaming and social media platforms, creating niches of content and corresponding pocketed audiences. Catering to a diaspora of multicultural audiences requires an in-depth understanding of these clusters, enabled by one’s own distribution platforms.

However, legacy media enterprises treated new distribution methods as additional channels to propagate their existing IP through third-party distribution platforms. They were late in building their own digital communities and platforms to create first-party databases. Meanwhile, big tech platforms reverse-engineered their approach by creating IP on top of the first-party data aggregated over the past decade. Netflix is the purest example of a media distribution platform pivoting early to the digital era and building a loyal community through its IP catalog.

These developments gave rise to what we call the “media trilemma,” where no media broadcaster has been able to conquer all three: reach, engagement, and monetization. Legacy media networks (spanning global media enterprises and national broadcasters) have reach due to their established distribution channels and monetization through years of advertiser relationships. However, they lack audience engagement because they’re not well connected to their clustered audiences (e.g., diminishing fan engagement across traditional sports media networks). Premium OTT platforms, such as Netflix, excel in audience engagement and have built monetizable communities, but they lack the massive reach of legacy media houses or even ad-based streaming platforms. Social media platforms are dominated by a new format, user-generated content (UGC), which has driven massive reach and engagement through the most democratic approach to content creation. Yet content creators have been unable to scale their monetization, with much of it heavily controlled by big tech social media platforms.

Big tech platforms have emerged as leading players in addressing elements of what we describe as the media trilemma while advancing toward what we call the media trifecta of content, community, and commerce (see Exhibit 1). This is a consequence of massive first-party data aggregation by their social media platforms, giving rise to IP that reaches audiences in multiple formats, establishes communities via platform tools, and monetizes them through innovative avenues such as advertising, subscriptions, and purchases.

Source: HFS Research, 2026

And while the digital era brought new distribution platforms focused on consumer data collection, AI platforms/large language models (LLMs) are shifting away from first-party data to first-party context. This may help media platforms and advertisers inform monetization strategies by enabling more personalized engagement with viewers.

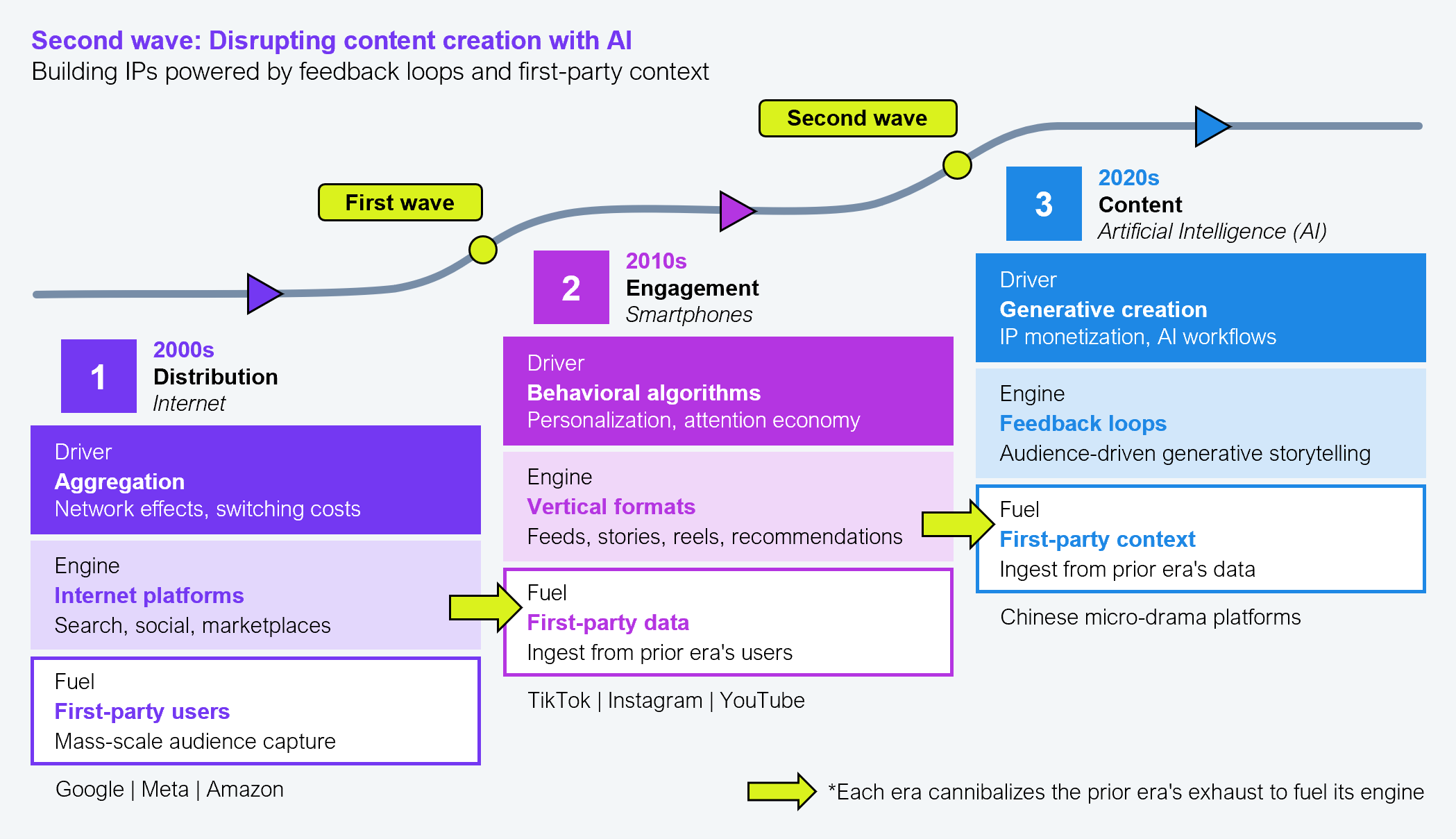

The previous decade was defined by the disruption of content distribution. The next one may be shaped by a second wave of disruption in content creation, driven by quick feedback loops.

A pattern stands out across the last two decades for media enterprises: each era of the media value chain ran on a different engine, and each engine was fueled by the exhaust of the previous one (see Exhibit 2). The 2000s ran on distribution and aggregation, with first-party users as the prize that Google, Meta, and Amazon captured at scale. The 2010s ran on engagement and the smartphone, with behavioral algorithms turning those users into first-party data for big tech platforms.

The 2020s era is driven by content and AI, shifting again from first-party data to first-party context, signaling audience engagement and attention through feedback loops for refining content IP. This is the layer where the value chain inverts: audiences move from the end of the chain to the front, and the content IP becomes a downstream expression of the audience’s affinity. The Chinese micro-drama industry shows what that looks like at scale, where the content IP is iterative, informed by community feedback and gravity, and intended to support faster realization of value, depending on implementation and context. WBD’s Unbreakable platform is another example where audience engagement is the centerpiece and the advertising IP is driven through feedback.

In the current scenario, most media enterprises are stuck in previous eras, trying to build vertical distribution platforms to gather consumer behavioral data. The agentic AI era provides a level playing field to make a comeback against big tech platforms. Only this time, media enterprises may be better positioned in certain areas, with content creation as the key driver, falling right up their alley. This differentiation, if well coupled with their IP ownership advantage, may support efforts to regain the media trifecta as they help reduce costs in certain workflows and support expanded monetization approaches, depending on implementation.

Source: HFS Research, 2026

With the mass adoption and commercialization of agentic AI, the M&E industry is most vulnerable to direct value disruption. While other industries see workflow efficiencies through agentic AI, M&E’s core value proposition, i.e., content creation, is being disrupted across all formats: text, audio, and video.

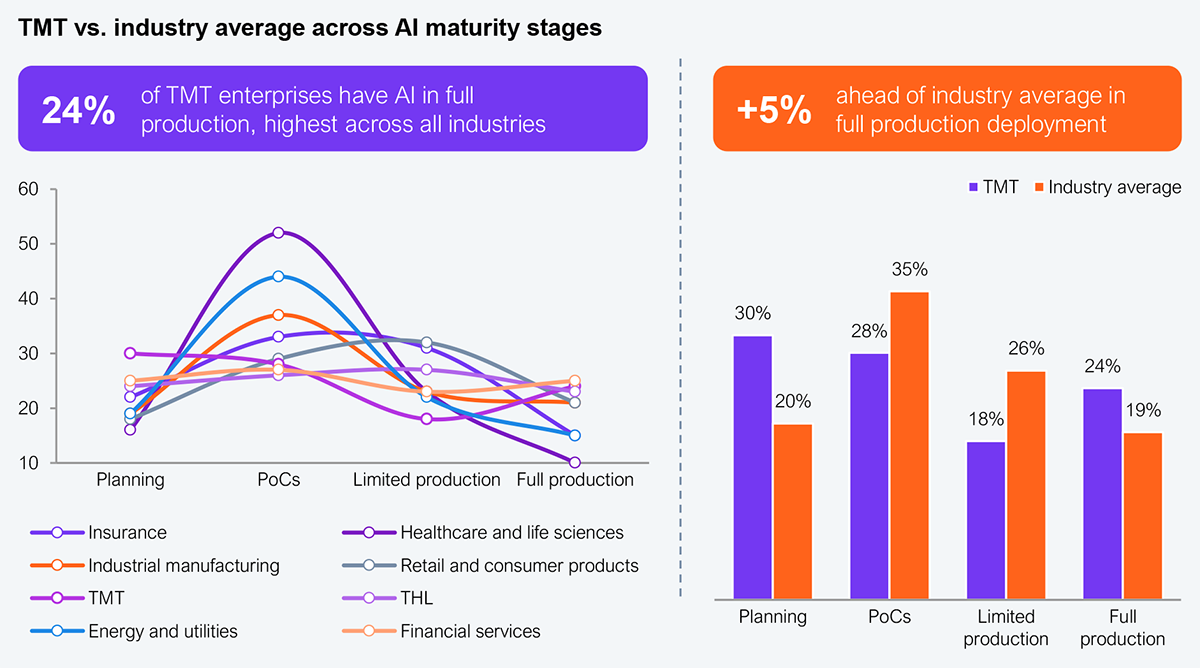

Notably, the telecom, media, and technology (TMT) industry is leading enterprise AI adoption at scale. HFS Research reports that approximately 24% of surveyed TMT enterprises have AI in full production (source: HFS Research AI Maturity Survey, 2025; global), over 5% above the industry average. The data suggests the industry has a relatively balanced deployment profile across all maturity stages (see Exhibit 3).

Source: HFS Research AI Maturity Survey, 2025; global

On the other hand, regional AI adoption patterns in M&E vary sharply, with the impact of agentic AI looking different across geographies (as per HFS Research Pulse Survey, global, 2026). AI maturity here masks four distinct regional postures, each shaped by market structure, regulation, and incumbency. North American broadcast networks are leaning on customer-facing impact (personalization, fan experience, IP content refinement) to defend audience share against streamers and platforms. European broadcasters are prioritizing secure, regulatory-compliant deployments (AI Act, GDPR, public-service mandates), with cost takeout as the near-term return. Middle East broadcasters are pursuing large-scale transformations that bundle agentic AI with the modernization of legacy estates, addressing technical debt and AI adoption in a single program. In APAC, networks are adopting AI at the workflow and use-case level, targeting the highest-ROI, low-hanging fruit (captioning, localization, ad operations, content tagging) to demonstrate quick wins before scaling.

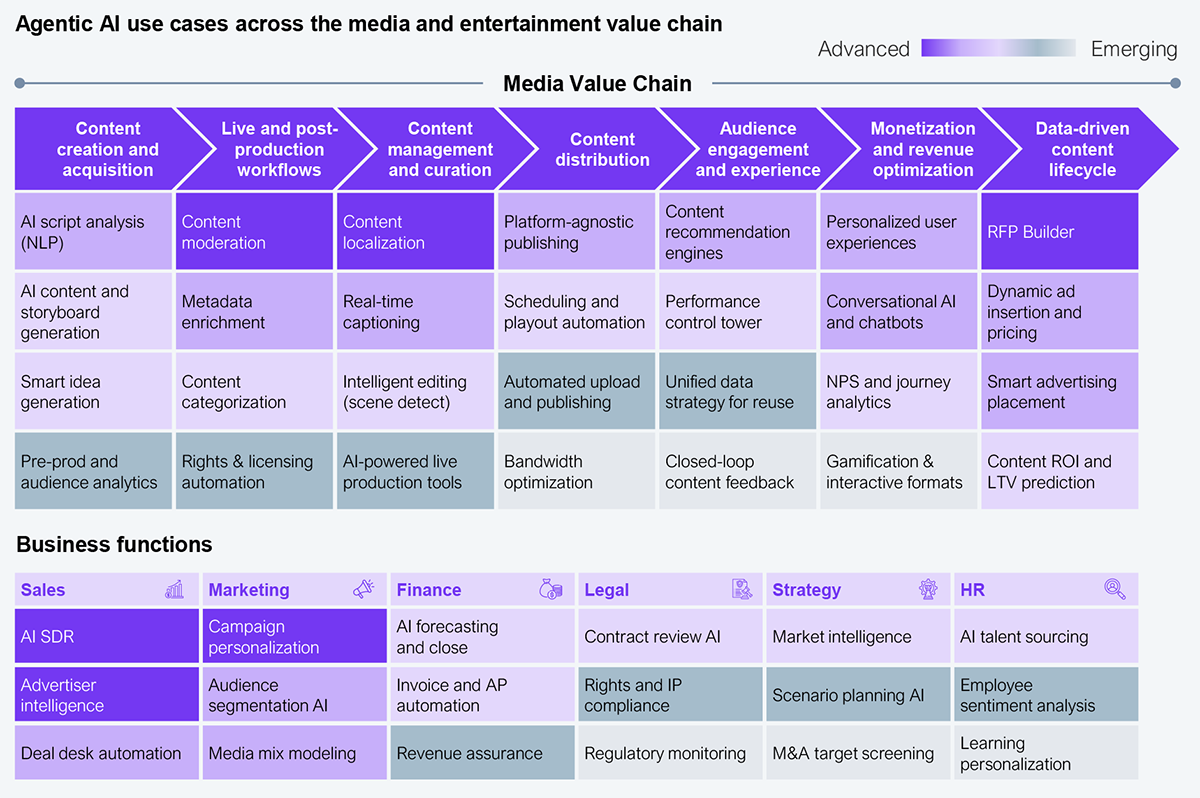

A key contributor to this is the range of use cases across the entire value chain, not just content creation. Accelerating sales and marketing through agentic AI will be key to unlocking monetization for every media network. Exhibit 4 presents a complete picture of the top use cases across each value chain element, with a focus on impact. Use cases such as content moderation, localization, and RFP builder demonstrate higher impact and are easier to implement. In sports broadcasting, agentic AI is already powering real-time highlight generation, multilingual commentary, automated player and tactical insights, and personalized second-screen experiences. WSC Sports, for example, turns a single live feed into hundreds of monetizable, audience-specific cuts for leagues such as the NBA and PGA Tour, while Genius Sports delivers live tactical insights and fan-facing graphics into Premier League and Liga MX broadcasts.

Source: HFS Research, 2026

These use cases may help reduce production costs in certain workflows and support scaling of content production to a point where it is almost good enough for publishing, potentially contributing to shifts in value capture over time.

As multimodal formats become the new norm, value may increasingly shift away from content production and toward IP ownership. For media enterprises, if content is cash flow, IP is valuation.

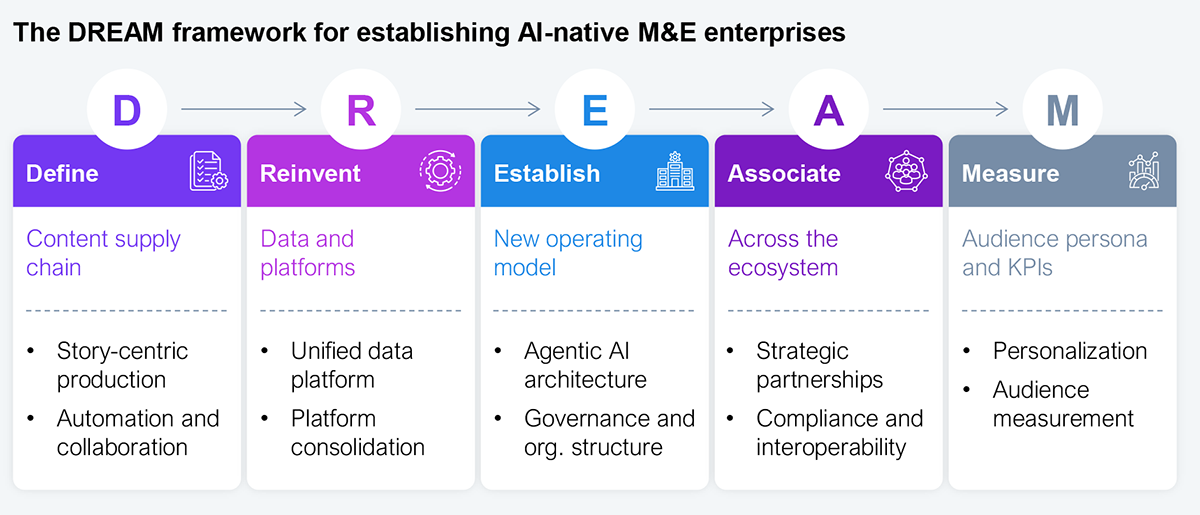

In today’s market, AI adoption is at the crossroads of “How to AI,” with enterprise leaders seeking an operational plan, operating model, and governance structure to run/scale agentic AI within their organizations. Media broadcasters face the scale-up problem due to siloed proofs of concept (POCs) within the content creation cycle, a problem that existed even before the AI boom. Sports media broadcasters, in particular, should address this quickly to leverage agentic AI, as they have the most loyal communities and the most demanding live workflows.

To solve this problem, we propose the DREAM framework to help CEOs support their agentic AI ambitions and help address potential gaps in AI adoption velocity. It provides a step-by-step guide to a comprehensive enterprise AI transformation, spanning content, data, operations, ecosystem, and outputs (see Exhibit 5).

Source: HFS Research, 2026

The DREAM framework is structured around five components:

D — Define the content supply chain

Keeping IP as the centerpiece, shift to story-centric, modular production with a “create once, publish everywhere” model. Automate multiplatform delivery, enable real-time cross-team collaboration, and embed AI tools for research, fact-checking, and metadata enrichment. AI-driven multimodality will support IP revenue diversification through a wide range of formats, geographies, and monetization streams.

R — Reinvent data and platforms

Unify first and third-party data into a single platform, consolidate into a single source of truth, and build a distribution-agnostic architecture guided by principles of automation-first, modularity, and self-service access. This will help address gaps in fragmented processes and siloed platforms, integrating AI across the unified distribution architecture.

E — Establish a new operating model

Start with a centralized center of excellence (CoE) model and work your way to a federated autonomous model while balancing speed, governance, and risk. The goal is to make each business unit self-sufficient, driving its own AI agenda with an effective governance structure. A central AI transformation office will serve as an omnipresent body overseeing the entire organization.

A — Associate across the ecosystem

Establish vendor-agnostic integrations with strategic partners, content vendors, and startups via MCP servers, A2A agents, and API-first connectivity. To address the full stack of agentic AI, enterprises should look for end-to-end partners that are essential across the data, platform, application, and orchestration layers.

Most AI vendors may provide tools across all four layers. However, the right partner complements them with trust, security, and governance, co-invests in outcomes and IP, and prices on a Services-as-Software™ outcome-based model. They provide governance for agents and enable augmentation across large-scale media enterprises. Point solution vendors drop agents into your stack, leaving you with chances of data leakage, brand-safety incidents, and audit trails on your own. End-to-end partners keep agents governed throughout their lifecycles (provenance, guardrails, human-in-the-loop checks, model versioning, observability) so trust holds up even after the partnership ends.

The Cognizant–Microsoft partnership exemplifies this end-to-end partner structure. It combines Cognizant’s deep M&E domain knowledge across content workflows, rights management, and audience engagement with Microsoft’s scalable cloud infrastructure and generative AI capabilities to help accelerate time-to-value for studios, broadcasters, and streaming platforms, depending on implementation. This integrated approach is designed to help clients modernize legacy systems, support more data-informed approaches to content monetization, and support deployment of AI-powered experiences across multiple parts of the content lifecycle. It also embeds responsible AI principles to sustain audience trust as markets become flooded with AI-generated content.

M — Measure audience persona and KPIs

Clear and relevant metrics are critical yet currently underdeveloped in AI implementations. Effective measurement of agentic AI success begins with benchmarking the current KPIs before AI introduction to map improvements. In the initial stages, the focus should be on AI workflow accuracy as the key indicator. This transitions to workflow efficiency across the content creation lifecycle. The final stage sees KPIs aligning with the enterprise’s goal to optimize one or more of the three usual suspects: reach, engagement, and monetization.

The success of this framework, however, requires a centralized AI Transformation Office that defines vision and governance, designs value/change management capabilities, and activates prioritization across all transformation workstreams.

Media broadcasters, both global media enterprises and national broadcasters, have burned their fingers in the digital era by treating the internet as just another distribution channel. This left the door open for big techs to capture a major share of digital ad spend.

Agentic AI presents a breakthrough opportunity for them through disruption in content creation. As content becomes easier, faster, and cheaper to produce, the value shifts to IP ownership. To benefit from this shift, media enterprises must judiciously and responsibly leverage agentic AI to expand and monetize their IP across global and national markets at cheaper production costs.

For CEOs of media broadcast networks, the imperative is to act on market developments and invest in the “How to AI” planning and operationalization process across their organizations, not just in mature pockets of the content creation lifecycle. This requires redefining business functions and processes to help improve efficiency across the agentic AI ecosystem and address margin pressures. The DREAM framework offers a practical roadmap for this transformation, emphasizing shared ownership of initiatives across the organization and a strong leadership vision.

Register now for immediate access of HFS' research, data and forward looking trends.

Get StartedIf you don't have an account, Register here |

With the exception of our Horizons reports, most of our research is available for free on our website. Sign up for a free account and start realizing the power of insights now.

Our premium subscription gives enterprise clients access to our complete library of proprietary research, direct access to our industry analysts, and other benefits.

Contact us at [email protected] for more information on premium access.