A handful of plucky start-ups sensed consumers’ disillusionment with their traditional banks following the 2008 financial crisis – and who could blame them? They were also quick to sense consumers’ rapid conditioning, by the likes of Amazon, to expect convenient, cheap, and digital services in all areas of their lives, and knew that this was something incumbent banks weren’t providing. This rag-tag bunch of initiators has since grown up, and today is known as the fintech industry: a multibillion-dollar global phenomenon. Fintechs are eating into incumbents’ market share and threatening to make former household names irrelevant, and banks have been slow to act and defend themselves.

Fintechs aren’t disruptive anymore, they’re the new face of finance

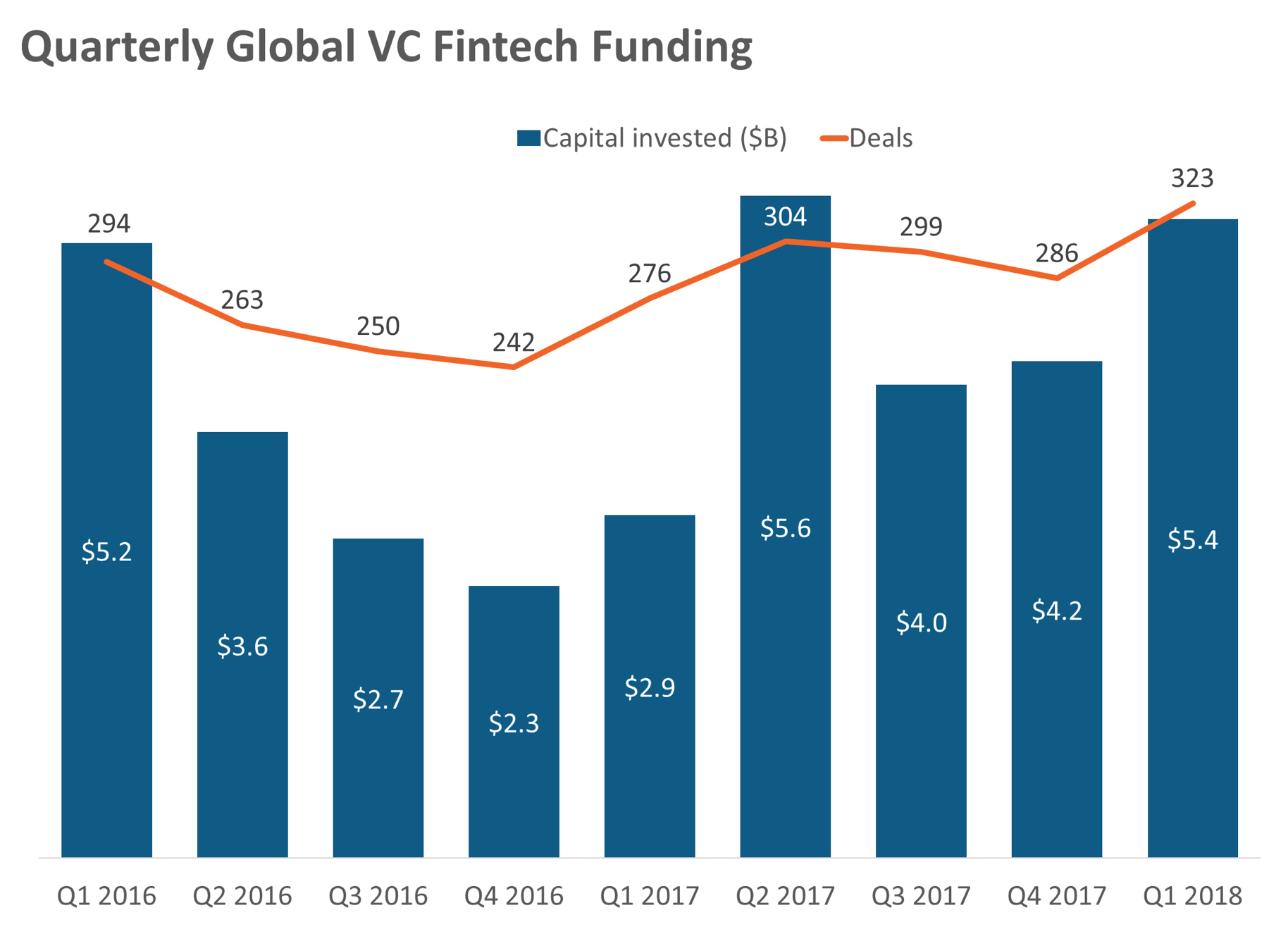

Since 2008, this failure to deliver the convenience consumers were demanding has spawned a massive global industry, in which financial technology start-ups (fintechs) have kept identifying more inefficient financial processes that they could fix using cutting-edge technology. Today, the fintech industry’s segments include (take a deep breath): Digital banking, alternative lending, personal finance management, robo-investment, regtech, insurtech, cryptocurrency platforms, blockchain infrastructure provision, and payments. What was once a group of underdogs who had plenty of ideals but no clue how to become sustainable businesses, is now a behemoth that rakes in billions in VC funding annually ($17 billion in 2017), and which, through partnerships and mergers and acquisitions, is putting down roots within the mainstream financial services industry. Fintech has become the force that’s changing finance from the inside – it has become the new face of the industry it set out to disrupt.

Fintechs pride themselves on letting consumers manage their finances – from their current accounts to their insurance policies to their investment portfolios – with ease through digital channels, all the while offering their services cheaply and transparently. They don’t hand out identikit products and services, either: They collect consumer behavior data to personalize their offerings to suit the individual. That sounds attractive, and it is: Banks, both retail and investment, have been at the frontline of the disruption fintech has wrought, as they were the primary targets of consumers’ wrath and of fintechs’ idealism. The big banks are now hemorrhaging market share to their digital rivals.

Exhibit 1: Fintech VC funding

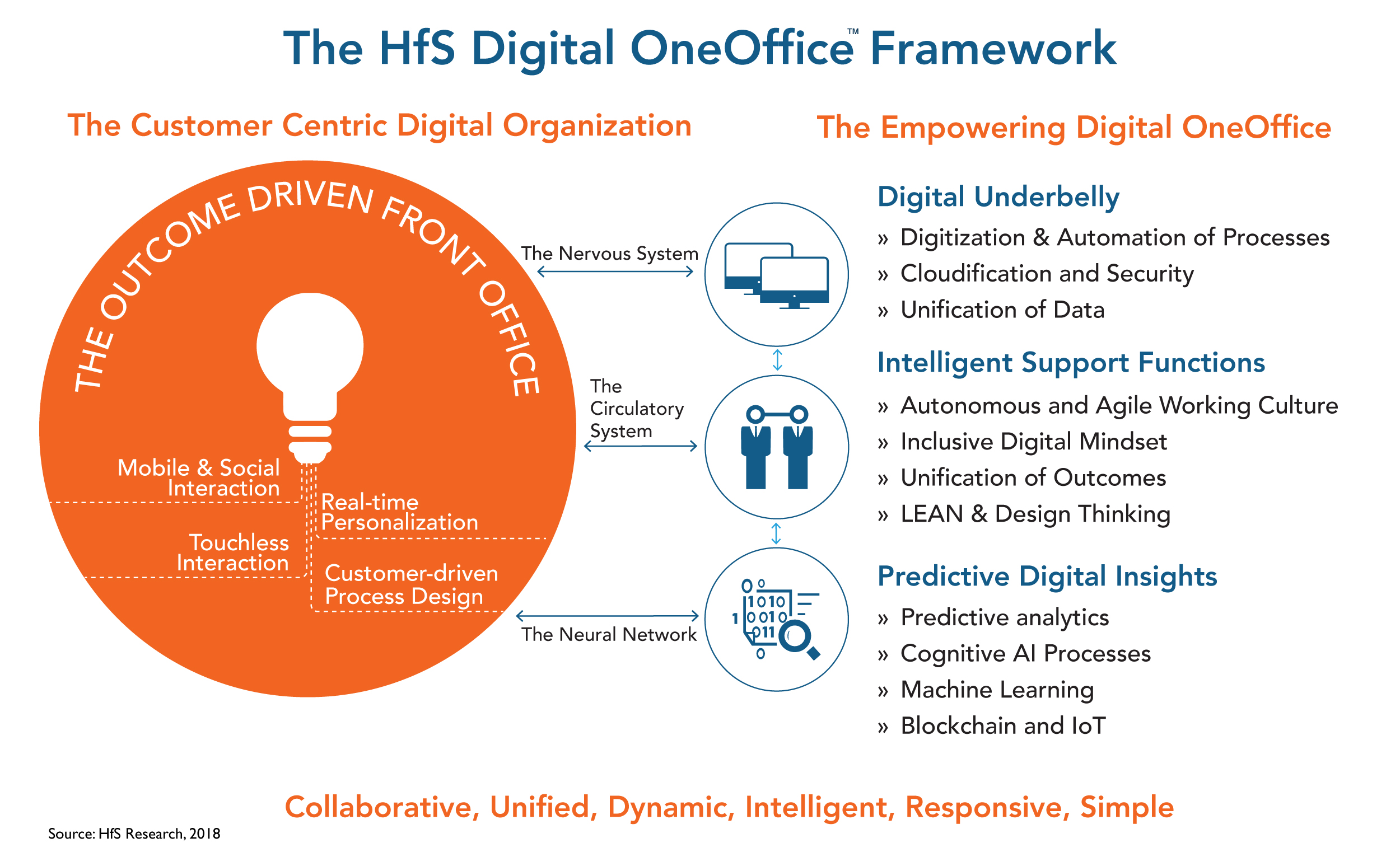

Fintechs help banks get to the digital OneOffice framework

Digital organizations must have an operating framework that maps out how they have to operate in the future. Traditional operating models, while creating some incremental productivity value if managed effectively, struggle to drive the unification of digital business models with emerging technologies across a business’s operations. Fintechs haven’t grown up with this legacy and can bring an operating framework to traditional banks that can help them to success in the future.

Exhibit 2: The OneOffice ideal

It’s important to note, though, that fintechs are more than just a threat for slow-moving incumbents. For those firms which can harness the power of the fintech juggernaut rather than be run over by it, the opportunities are vast.

Banks, like virtually all other legacy organizations, are in a race to transition to the OneOffice model: That is, unify siloed business departments, think more abstractly and look at the big picture when creating business roadmaps, be predictive rather than reactive in using data, and – above all – put the consumer at the center of everything they do. But, despite their vast capital reserves and renowned reputations, they are old and slow-moving. Many don’t have the requisite technical know-how, the mindset, or the talent to make this transition.

While some banks turn to consultants or service providers to get help, the fact is that many of these organizations also lack the necessary technology and talent to help their clients. So, for a growing number of banks, fintech startups are beginning to look like the obvious partners to get them to the OneOffice model. A growing number of banks are partnering, investing in, or acquiring fintechs to leverage their technology and tech-savvy staff, in the race to reach the OneOffice ideal.

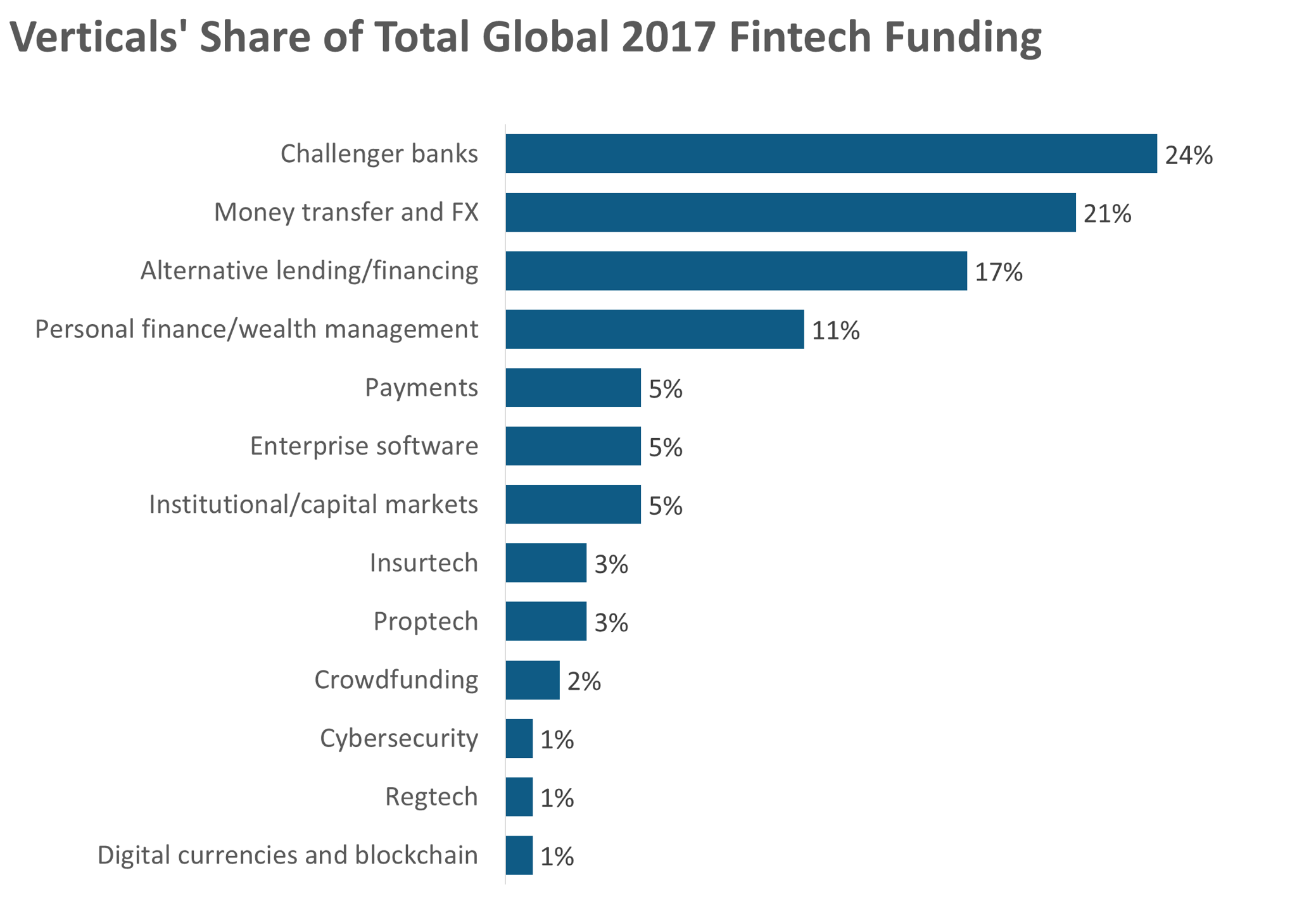

Exhibit 3: Fintech funding, by vertical

You’ll find the most exciting propositions by looking past the big brands

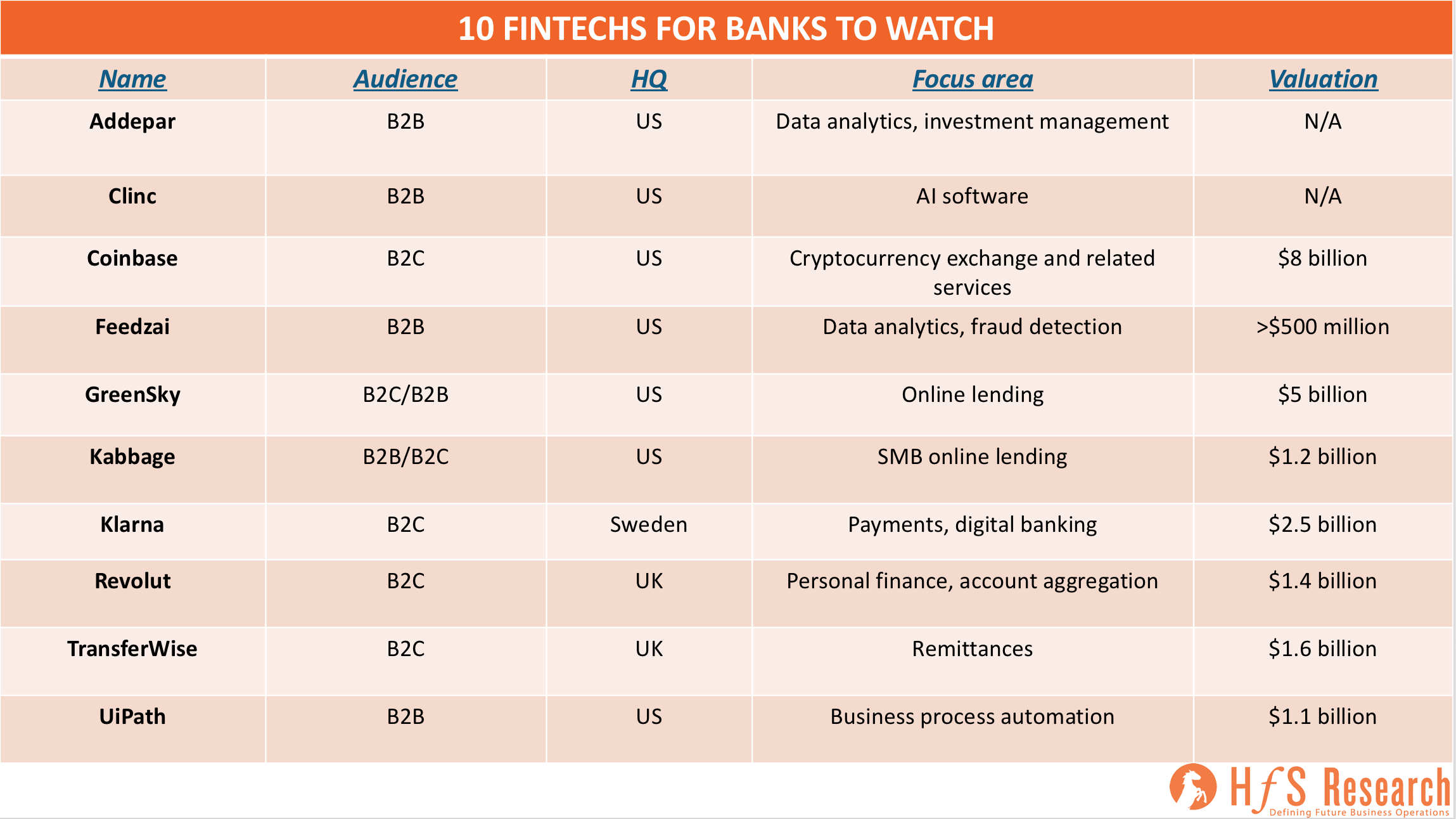

The fintech industry has now reached vast proportions, to the point where a bank looking to partner would have to spend a very long time weighing up its options. Below, HfS has drawn up a list of ten fintechs that banks – both retail and investment – should have on their watchlists as they seek to boost their digital capabilities. These include both business-to-consumer (B2C) fintechs, which cater directly to consumers, and business-to-business (B2B) players, which sell their technology or solutions directly to organizations like banks. While the B2Cs are tending to get the most attention and fame, it’s important to keep an eye on the B2Bs, whose offerings may be less flashy, but which have the potential to revolutionize a legacy organization from the ground up.

So, here is our shortlist of the fintechs – both B2B and B2C players – which we find most exciting for the curious and forward-looking to keep on their radars. This list includes names which frequently make the headlines, and others who keep a lower profile. All have been selected based on their potential to make a perceptible difference to consumers, and/or to legacy organizations.

Exhibit 4: Our ten to watch

And here is why, in our humble opinion, each of these players deserves their place on our list:

Keep your fintechs free-range

Now, you might be wondering: ‘Knowing what’s out there is all very well, but how do I engage with these start-ups?’

The answer is that there is no right answer – it all depends on the nature of your organization’s needs and corporate culture.

There is one thing that’s for certain, though: If you think there’s something in the fintech world that your organization ought to harness, then you need to make your move now. If you run a bank, you should be interested because a fintech relationship will give you access to the provision of new products and services that consumers are demanding, without having to build them yourself, saving you money and shortening time-to-market. You’ll also get access to the valuable and rare tech talent we all know you’re struggling to lure. (Millennials continue to shoulder the aftermath of the financial crisis and are often loath to work for the companies that played such a part in it.)

But before you start trying to hoover up start-ups, give some thought to how you should engage with them. Acquisitions might promise to give your organization more control over a fintech, as well as valuable additions to your workforce… but there’s a catch (or several). There are often irreconcilable cultural differences between a big bank and a trendy tech start-up. The start-up wants to ‘move quickly, move fast and break things’, so to speak. Your emphasis, however, will likely be on regulatory compliance, and weighing all options and risks carefully. This can mean that your acquisition will lose the things that made it valuable once it’s been subsumed into your organization – you’ll be left with a small group of people who’ve lost their start-up spirit. Furthermore, it’s very likely that your bank is still using technology and infrastructure dating back to the dark ages, whereas fintechs usually employ cloud-based infrastructure and cutting-edge systems you probably know little about. APIs will only go so far in smoothing this over.

With all of that in mind, you may want to consider a bilateral partnership with a fintech, instead. This will leave the start-up with the work-dynamic that has allowed it to innovate, and it will spare you the trouble of trying to integrate its cutting-edge systems into the morass of your antiquity. Of course, there is always the option of turning to a consultancy or other integration partner to guide you through such integrations – but it will be on you to conduct due diligence and choose a partner that has the technical know-how to make this happen.

The bottom-line: Start forming fintech relationships now or risk being left behind

Whatever engagement approach your organization decides is best, what’s certain is that now is the time to act. Fintech acquisitions and partnerships are intensifying across all geographies, and competition for the most attractive start-ups is really heating up. If you don’t already have a strategy team looking at this, get one together – now – to map a careful overview of the fintech landscape. You need to start thinking of the wild, young things as valuable partners, rather than upstarts who’re out to eat your lunch. These are the companies setting the new standards within your industry, and if your organization doesn’t give them a deserved seat at the table, your competitors most certainly will.

Register now for immediate access of HFS' research, data and forward looking trends.

Get StartedIf you don't have an account, Register here |

With the exception of our Horizons reports, most of our research is available for free on our website. Sign up for a free account and start realizing the power of insights now.

Our premium subscription gives enterprise clients access to our complete library of proprietary research, direct access to our industry analysts, and other benefits.

Contact us at [email protected] for more information on premium access.