This HFS Research Market Impact Report is for CEOs, boards, CIOs, and transformation leaders diagnosing the process, data, technology, and talent debts that block AI value across the enterprise.

Across Global 2000 enterprises, $18 trillion in trapped value sits idle, not because of market conditions or competitive pressure, but because of four self-inflicted enterprise debts: process debt, data debt, technology debt, and talent debt. Each alone slows performance. Together, they compound to form a structural ceiling on enterprise performance. As enterprises accelerate their AI agendas, these four debts have become more consequential than ever. They are the reason AI investments fail to deliver. Those who address them unlock the $18 trillion opportunity.

HFS Research, in partnership with Genpact, surveyed 2,000+ enterprise executives globally to put a hard number behind what’s holding enterprises back from realizing their AI ambitions, supplemented by insights from a select roundtable of senior leaders convened by HFS and Genpact to surface real-world perspectives on the challenges of scaling AI.

What we found was stark: Four interconnected enterprise debts (process, data, technology, and talent) are compounding into a single system failure. This report quantifies the trapped value and charts the path to unlocking it.

While 92% of senior executives at Global 2000 companies believe agentic AI will fundamentally change how work is executed across their organizations, only 13% report that agentic AI is already integrated into their operations.

The single biggest reason enterprises cannot scale AI from pilots to production is not technology debt, even though it is often named. Instead, the problem is the foundation the technology is expected to run on: broken processes, untrustworthy data, decade-old systems, and a workforce not yet prepared for a human-agent operating model. These interconnected enterprise debts do not appear on financial statements, yet they are quietly keeping agentic AI trapped in pilot purgatory.

Every dollar spent on AI atop a broken foundation is a dollar working against itself. Resolving enterprise debts and agentic AI transformation are not separate programs. They are the same program. This report quantifies where the $18 trillion unlock sits, shows why AI investments are stalling, and draws on the 6% of proven resolvers to chart the path from ambition to measurable business impact.

The four enterprise debts are out in the open and impossible to ignore. They compound just as ruthlessly as any financial liability on a balance sheet: slowing decision-making, inflating costs, blocking AI, and grinding down the people who battle them every day.

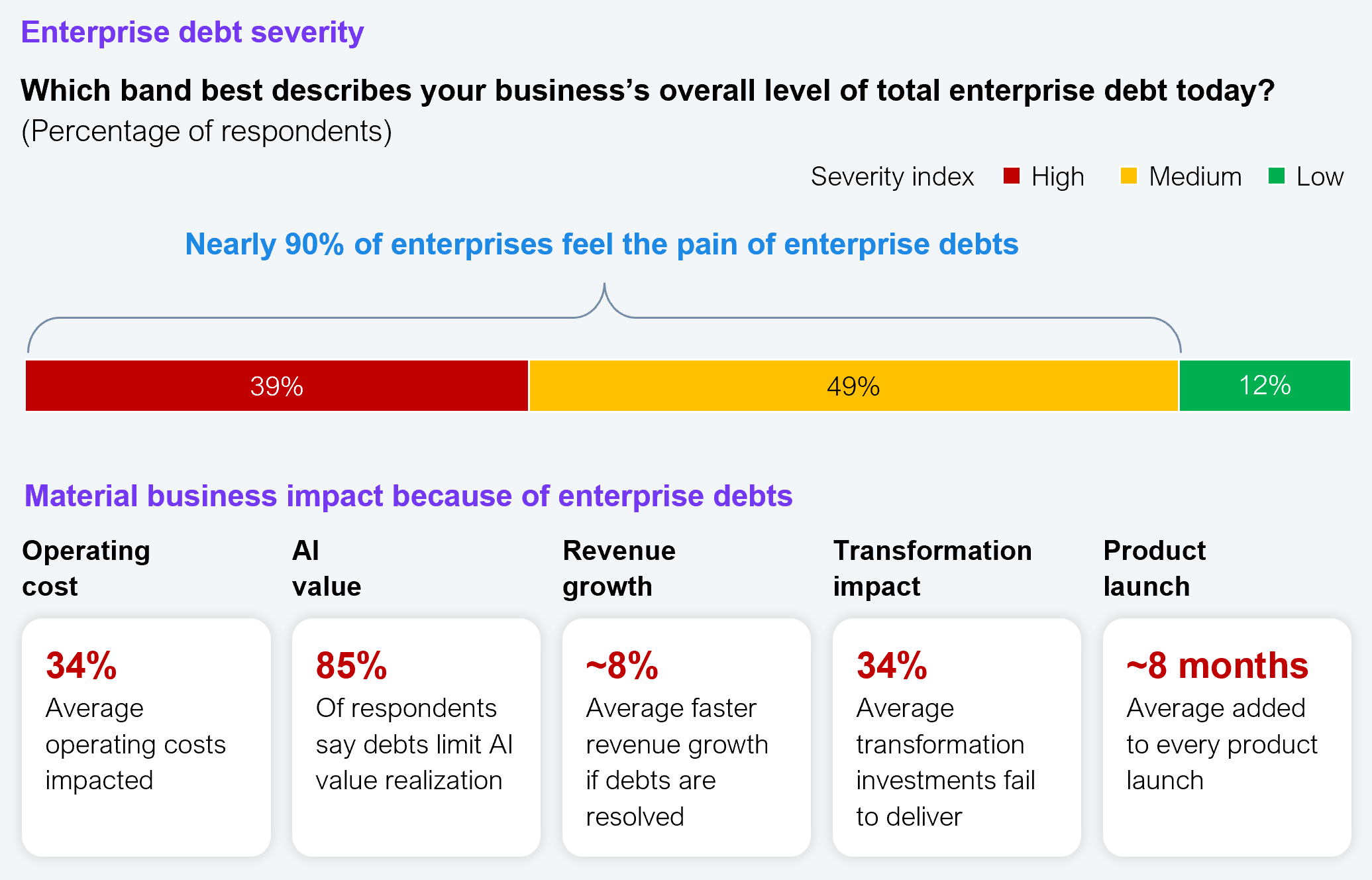

HFS asked more than 2,000 global executives to rate the severity of their total enterprise debt. Nearly nine in 10 enterprise leaders feel the drag, as shown in Exhibit 1.

Sample size: 2,002 global enterprise executives

Source: HFS Research in partnership with Genpact, 2026

Far from new, enterprise debts have been around for years, but the cost of inaction has changed. In the pre-AI era, legacy processes, aging systems, and patchy data were tolerable inefficiencies. In the agentic AI era, they are structural blockers. A model trained on dirty data will converge on the wrong answer. An agent dropped into broken processes will execute the wrong steps faster. An agentic system rolled out to an unprepared workforce will function and sit unused. Not failing visibly, just quietly preventing the outcomes that agentic AI was deployed to deliver. This different kind of threat demands a different kind of response.

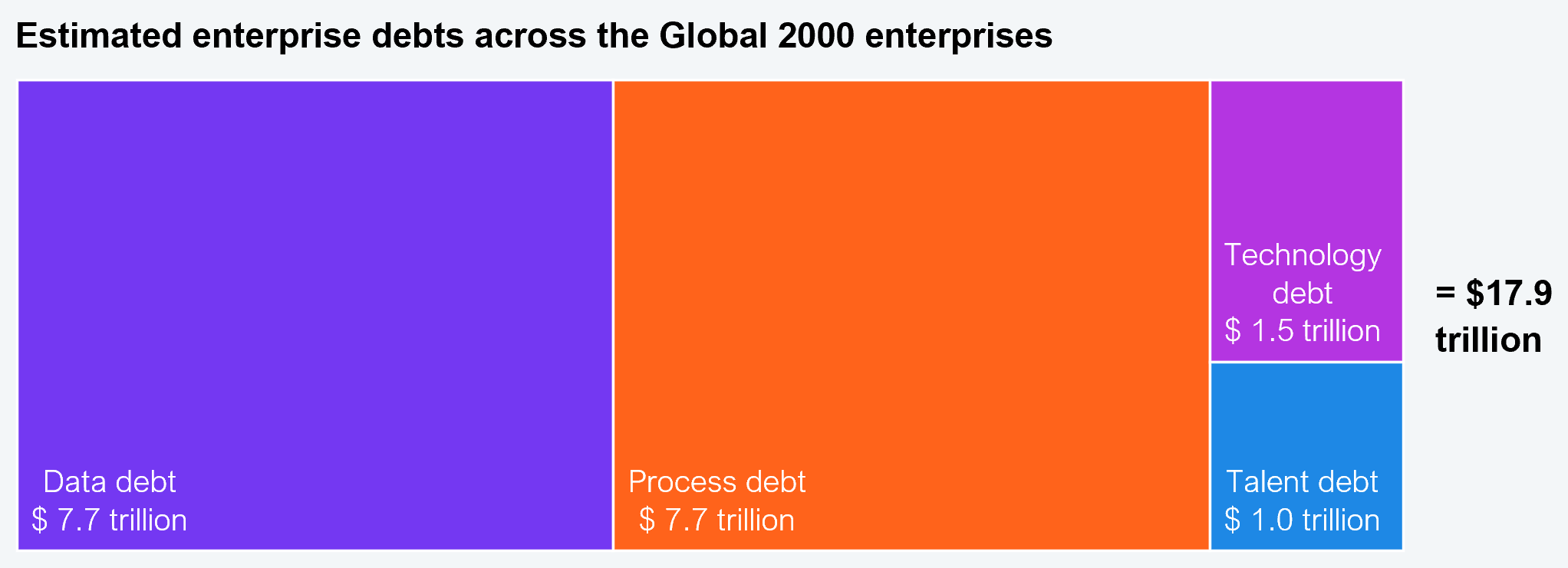

One of the biggest misconceptions in enterprise transformation is that technology debt is the whole story. It isn’t. HFS identifies four distinct but deeply entangled enterprise debts, each originating in a different place but inseparable in effect, as shown in Exhibit 2. Left unaddressed, they do not accumulate in parallel; they compound, collapsing into a single system failure greater than the sum of their parts. Treating one in isolation just shifts the bottleneck; it doesn’t fix the system.

Sample size: 2,002 global enterprise executives

Source: HFS Research in partnership with Genpact, 2026

Development teams spend more than 40% of their time addressing existing technology debt, anchored in decade-old cores

Legacy core systems, run-effort crowding out change capacity, weak engineering discipline, integration complexity, and infrastructure drag top the list of root causes for technology debt. As a result, over 40% of development team time goes to servicing these debts rather than building new capability, leaving little headroom for the transformation agenda the business expects IT to deliver.

The consequences compound into higher build-and-run costs, reduced delivery speed, elevated security and cyber risk, and reduced agility. Every innovation initiative is paying a legacy tax before it starts. Every agentic AI deployment that touches a legacy core amplifies that tax.

Your AI is only as good as the data it runs on, and half your enterprise data is unfit

Data debt is where AI ambition stalls. Its roots are systemic: fragmented source systems, legacy data architectures, weak governance and ownership, poor data quality management, and tooling gaps. These are the accumulated consequences of decades of tactical data decisions and deferred action. What enterprises once tolerated as manageable inefficiency has now become a hard constraint on AI value. The constraint tightens sharply with agentic AI, where every decision in a chain inherits the quality of the data feeding it and a single weak signal upstream cascades into compounding errors downstream. Long-deferred data debt is now the binding constraint on the agentic operating model enterprises are betting their next decade on.

There is no artificial intelligence without process intelligence

Manual, ungoverned, hard‑to‑change processes tax every workweek. Process debt creates a structural trap of high‑cost, low‑agility operating models and AI deployments that fail in production because the workflows they rely on are inconsistent and ungoverned. Process intelligence is the last mile of every agentic AI deployment.

You hired people to think, but enterprise debts have turned them into firefighters

Talent debt does not just drain workforce expertise; it amplifies every other form of enterprise debt. High attrition bleeds institutional knowledge. Workforce frustration reduces the readiness to adopt and iterate on new tools. And low AI-readiness directly constrains the human–agent operating model, where judgment, exception-handling, and last-mile decision-making remain distinctly human. People are the engine of agentic transformation.

The enterprise debts cannot be fixed in isolation; they share root causes and compound one another. Legacy infrastructure constrains technology modernization while degrading data quality. Skills gaps drive talent debt and technology debt simultaneously. Unclear ownership produces data governance failures, process drift, and talent misalignment. And manual operations create both process debt and data debt through the same patterns of work.

Enterprises keep failing to fix their debts, not because they lack awareness, but because they frame their problem incorrectly. When leadership frames reducing enterprise debts as a technology modernization program, they get a technology fix. When they frame it as process improvement, they get process improvements. Neither frame encompasses the whole system. The enterprise debts are interconnected because the business is interconnected. Finance’s data problem is IT’s integration problem is Engineering’s legacy problem is HR’s capability problem. Leaders who understand this stop asking which debt category to fix first and start asking how to redesign the operating model that keeps generating all of them.

In this study, we calculated the aggregate value at stake for the more than 2000 enterprises by applying respondent-reported revenue uplift and cost-reduction estimates across a combined revenue base. The number is almost too large to be intuitive: $18 trillion of recoverable enterprise value.

Note: Read the methodology in the appendix to understand how we valued each of the enterprise debts

Sample size: 2,002 global enterprise executives

Source: HFS Research in partnership with Genpact, 2026

The $18 trillion figure reframes the conversation. Addressing enterprise debts has often not been recognized or treated as a coordinated enterprise-wide mandate. While pockets of capability building and modernization are happening across organizations, they are rarely addressed intentionally or holistically, and they are rarely funded with the urgency the scale of the opportunity demands.

Technology debt has historically been the most visible and widely recognized form of debt, but the data shows the real value unlock comes from addressing process, data, technology, and talent debt together.

The payback from resolving enterprise debts is clear in this research; it unlocks faster revenue growth and meaningful cost reduction. The issue is that too many enterprises are deferring action while continuing to invest in AI and transformation programs that depend on foundations that are not ready. Leaders need to treat debt resolution as a high-ROI investment in growth, efficiency, and AI value realization. Adi Shetty, SVP, Global Head of People Operations and Systems at Visa, reinforces why this cannot be treated as a technology problem alone and requires a holistic approach:

It’s not the technology; it’s organizational design, culture, people, and leadership. That’s what the biggest challenge is here.

— Adi Shetty, SVP, Global Head of People Operations and Systems, Visa

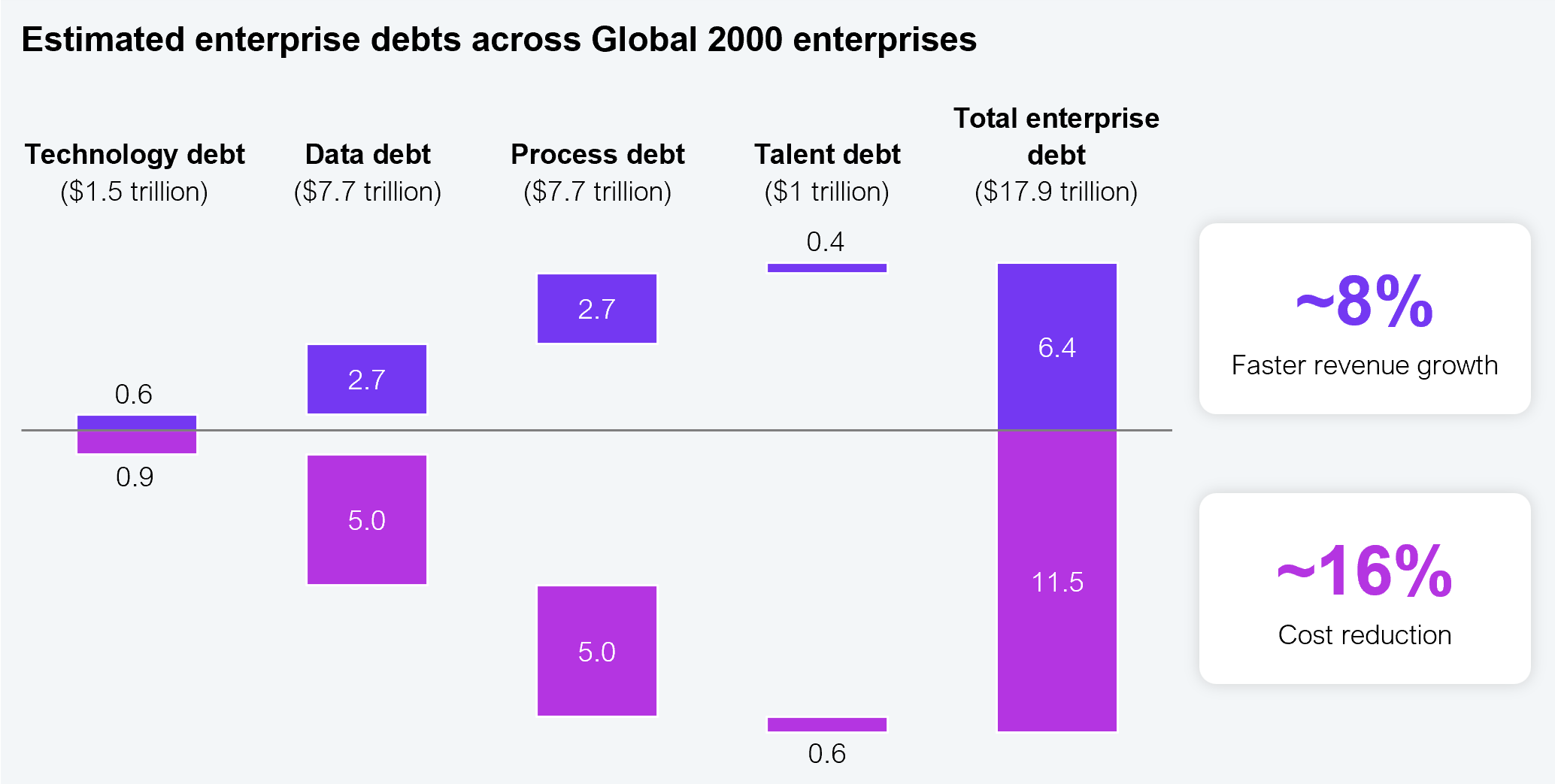

Resolving enterprise debts is a dual-return investment. When we asked respondents to estimate the value unlocked by resolving their top-two-ranked enterprise debts, the results were clear: approximately 8% faster annual revenue growth and 16% annual cost reduction across the Global 2000. These are not separate outcomes requiring separate investments. The same actions that reduce cost also unlock growth (see Exhibit 4). While the balance shifts by debt type, leaders who chase only one outcome risk leaving the bigger opportunity on the table; resolution is not just an efficiency play, it is what frees the enterprise to grow.

Note: Read the methodology in the appendix to understand how we valued each of the enterprise debts

Sample size: 2,002 global enterprise executives

Source: HFS Research in partnership with Genpact, 2026

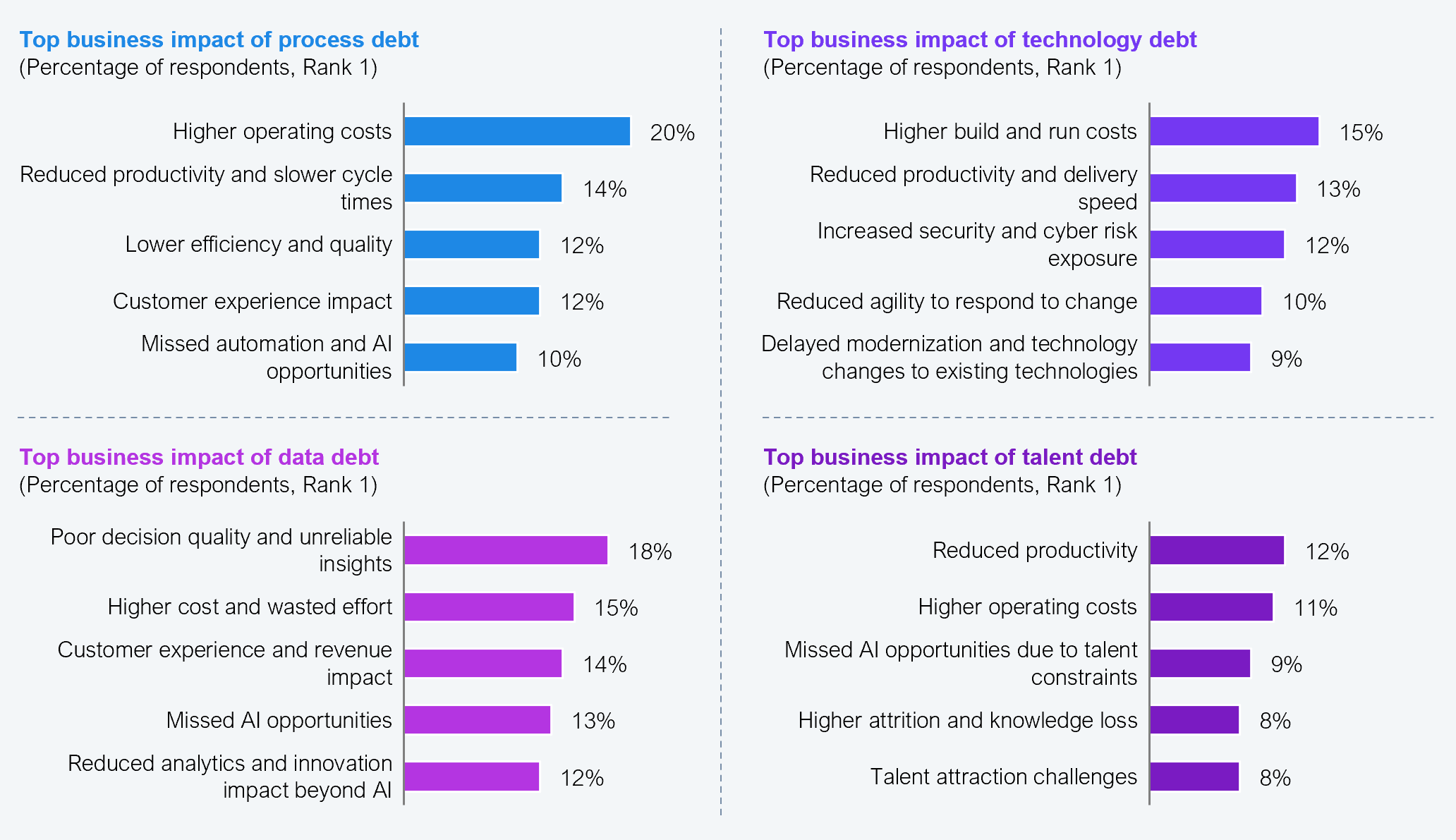

Process debt represents one of the largest combined opportunities at $7.7 trillion, split between $2.7 trillion in revenue uplift and $5.0 trillion in cost reduction. The revenue opportunity is concentrated in speed, faster product launches, shorter sales cycles, and the ability to respond to market conditions without the drag that process debt adds to every major initiative. It’s reflected in transformation failures and product launch delays ranking among the top value leakage survey respondents report.

The cost-reduction opportunity is immediate, including fewer manual interventions, less rework, and lower operating costs per transaction across every function running on ungoverned workflows. It’s consistent with higher operating costs ranking as the single biggest business impact of process debt (20%) and reduced productivity and slower cycle times close behind (14%).

Sample size: 2,002 global enterprise executives

Source: HFS Research in partnership with Genpact, 2026

Ashish Gupta, SVP, Global Business Services (GBS) Transitions & Operations at Reckitt, captures how this process debt shows up inside enterprises and why it becomes such a barrier to AI-led productivity:

The struggle is real within enterprises. Anywhere between 30% to 40% of work is wasted on ineffective processes and duplication. Too many people doing the same work, too many hierarchies, everybody trying to demonstrate that they are adding value. It’s a big hindrance to AI-led productivity because then you try to automate it, and what you end up doing, rather than transforming, is scaling more inefficiency and more mess in the organization.

— Ashish Gupta, SVP – Global Business Services (GBS) Transitions & Operations, Reckitt

Data debt matches process debt at $7.7 trillion total, split between $2.7 trillion in revenue uplift and $5.0 trillion in cost reduction. The revenue case is direct; trusted, AI-ready data enables enterprises to personalize at scale, accelerate decision cycles, and build the analytical edge that translates into market share. Delayed AI value and slower revenue growth are ranked as the top two leakage points that survey respondents attribute to data debt. The cost case is equally compelling, eliminating the data reconciliation, rework, and quality resolution that currently consumes up to 40% of employee time in data-intensive functions. This observation is consistent with higher costs and wasted effort (15%) ranking as the second business impact, following poor decision quality and unreliable insights (18%) (see Exhibit 5).

Technology debt contributes $1.5 trillion in total value, with $0.6 trillion from revenue uplift and $0.9 trillion from cost reduction. The revenue opportunity is primarily about capability. Modern systems unlock integrations, data pipelines, and AI deployments that legacy cores actively prevent, consequences that manifest directly in product launch delays and higher operating costs, as the leakage points survey respondents feel most acutely. The cost opportunity is the most visible, reclaiming the approximately 42% of developer time currently consumed by servicing existing technology debt and redirecting it toward work that actually generates returns. This burden surfaces as higher build-and-run costs (15%) and reduced productivity and delivery speed (13%), the two dominant business impacts cited by survey respondents (see Exhibit 5).

Talent debt represents a total opportunity of $1.0 trillion, comprising approximately $0.4 trillion in revenue and $0.6 trillion in cost reduction. AI-ready talent operating within a well-designed human-agent model closes the gap between AI investment and measurable business outcomes. This connection surfaces directly in slower revenue growth and delayed AI value as the leakage points survey respondents feel. The cost case is driven by attrition. A 15% annual voluntary attrition rate in critical roles incurs hiring, onboarding, and knowledge-loss costs that compound at scale; this is consistent with reduced productivity and higher operating costs, which respondents attribute to talent debt as the top business impacts.

Talent debt carries the smallest dollar figure in the $18 trillion breakdown, not because it matters least but because it’s hardest to visualize and measure. The cost of talent debt does not accumulate neatly in a talent ledger. It accumulates in every other type of enterprise debt. It shows up as data debt when governance programs stall due to a lack of skilled owners. It shows up as process debt when redesigns fail to stick because the workforce was never trained. It shows up as technology debt when AI deployments underperform because neither the builders nor the users were ready.

Talent debt is the silent tax on every resolution effort. Amanda Turcotte, SVP and Chief Actuary at Amalgamated Life Insurance, captures how this lack of fluency becomes a practical barrier to adoption:

The thing that’s holding us back is generally a lack of fluency. A good chunk of our workforce doesn’t have basic AI skills. Our employees aren’t using AI in their daily lives at home, so it’s very hard for them to make the bridge and learn something new at work.

— Amanda Turcotte, SVP & Chief Actuary, Amalgamated Life Insurance

Within every category, cost savings outweigh revenue uplift by approximately 1.8x. A ratio that reflects the post-2023 enterprise mood, where CFOs find it easier to quantify “fix X, save Y” than “fix X, grow Z.” But that efficiency framing undersells the real prize. Debt resolution unlocks value on two fronts, growth and cost, in different proportions by debt type. It is also the foundation AI needs to deliver at scale.

There are exceptions, though. For instance, life sciences and capital markets skew toward revenue because growth is gated by speed-to-market (for example, drug launches and deal velocity) rather than by operating efficiency. For them, the debt resolution case is equally compelling, just framed differently. The next section unpacks how the $18 trillion opportunity is distributed across industries.

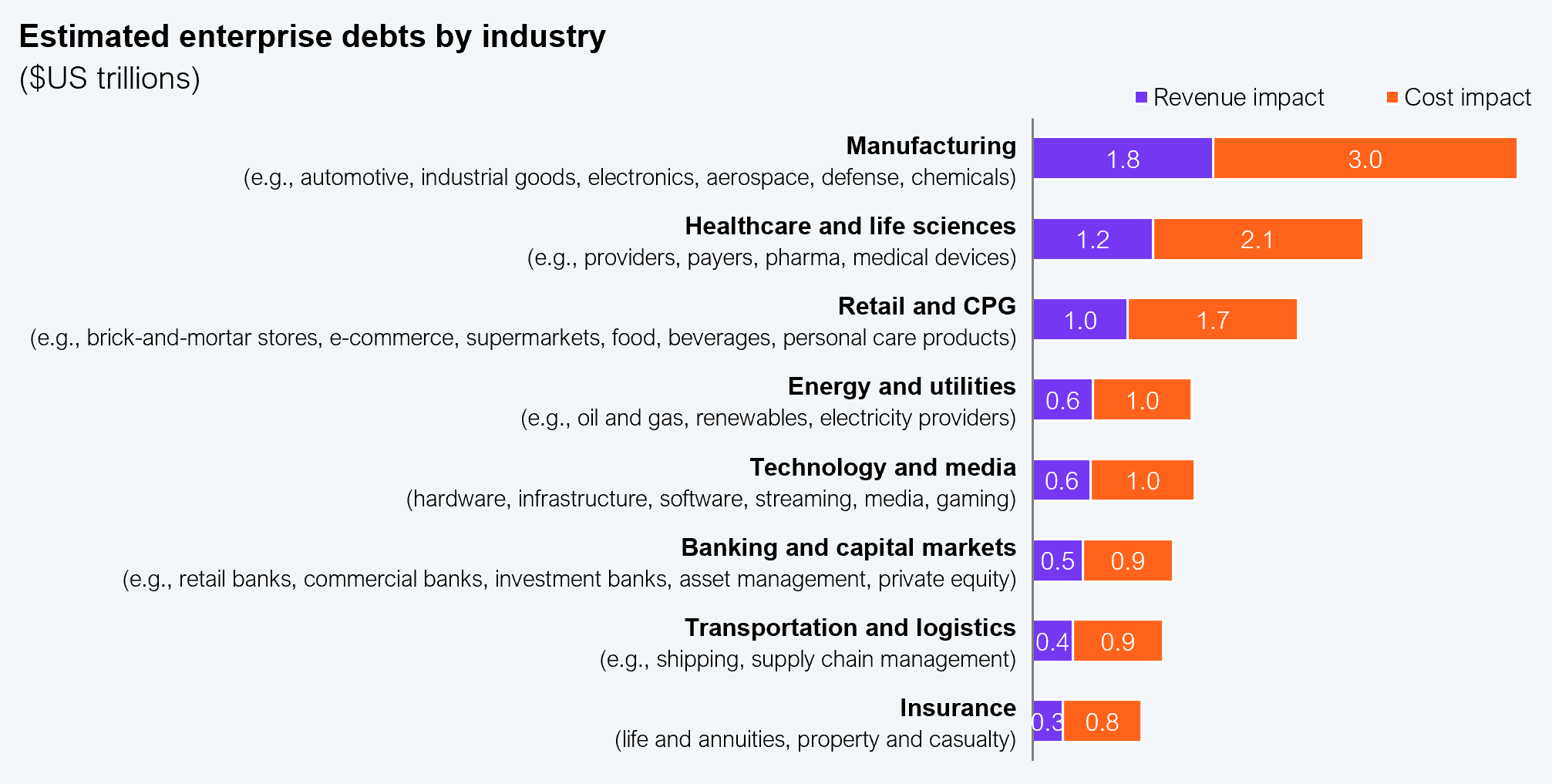

Manufacturing leads with $1.8 trillion in revenue impact and $3 trillion in cost impact, the highest of any industry (see Exhibit 6). Healthcare and life sciences follow at $1.2 trillion and $2.1 trillion, respectively. Both sectors run the longest, most complex multi-party workflows in the global economy, meaning process debt accumulates at every handoff across supply chains, production lines, and care pathways. Their core systems (ERP, MES, WMS, and EHR platforms) were layered in over decades without fundamental re-engineering, creating technology and data debt that are structural rather than incidental, with the resolution opportunity proportionately large.

Note: Read the methodology in the appendix to understand how we valued each of the enterprise debts

Sample size: 2,002 global enterprise executives

Source: HFS Research in partnership with Genpact, 2026

The type of debt also differs meaningfully by sector:

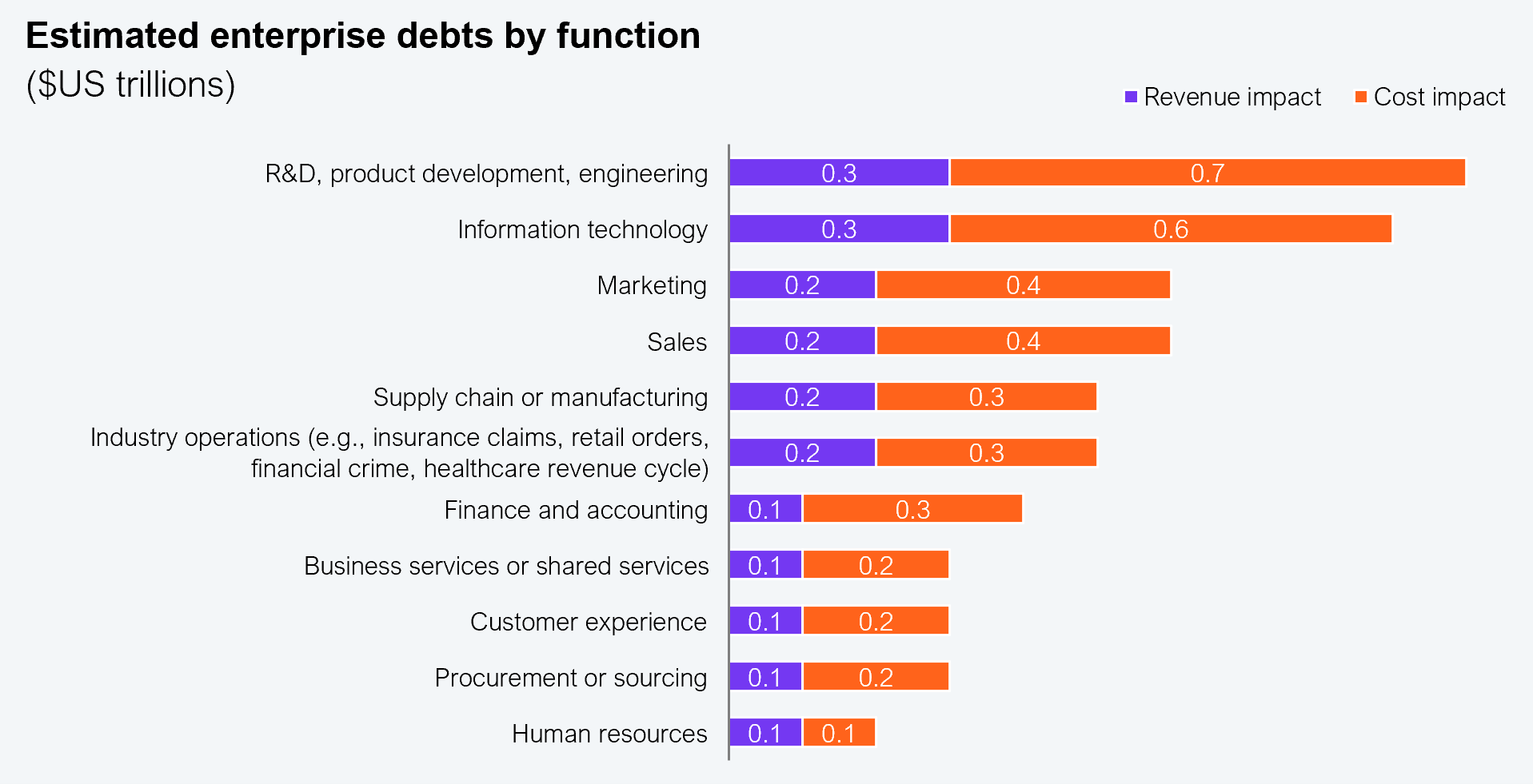

Engineering, R&D, and product development have the greatest potential to unlock value from resolving enterprise debts (approximately $1 trillion), as shown in Exhibit 7. Engineering sits on the deepest technology stacks (CI/CD, test infra, model pipelines) and longest-lived legacy code; debt compounds at the speed of releases. Talent debt spikes here more than anywhere else because scarce specialized skills (ML, embedded, security) create an outsized drag. Enterprise debts in R&D, product development, and the engineering function throttle speed-to-market; resolution ROI here is a growth lever, not just a cost lever.

IT is a close second, but it is a symptom as much as a cause. IT owns both its own debt and the substrate every other function runs on. When finance has data debt or CX has process debt, IT pays for the underlying platform. Fixing IT without fixing demand-side functions yields diminishing returns.

Note: Read the methodology in the appendix to understand how we valued each of the enterprise debts

Sample size: 2,002 global enterprise executives

Source: HFS Research in partnership with Genpact, 2026

Growth-facing functions like sales, marketing, and CX tend to skew toward process and data debts. These functions live across CRM, MAP, CDP, and too-many-to-count point tools bought tactically and never integrated. Every campaign or customer journey crosses five to 10 systems, so data and workflow become the same problem. Revenue-side functions also have the strongest revenue-uplift case versus cost, and every fixed handoff converts directly to pipeline or retention.

The finance and accounting function is data-heavy because it consumes everyone else’s mess. Finance pulls from every other function’s system into close, FP&A, and reporting. It’s the canary for upstream data quality issues. Process debt nearly equals data debt, reflecting brittle close cycles, reconciliations, and manual journal entries. “Fix finance” almost always means “Fix the data feeding finance.”

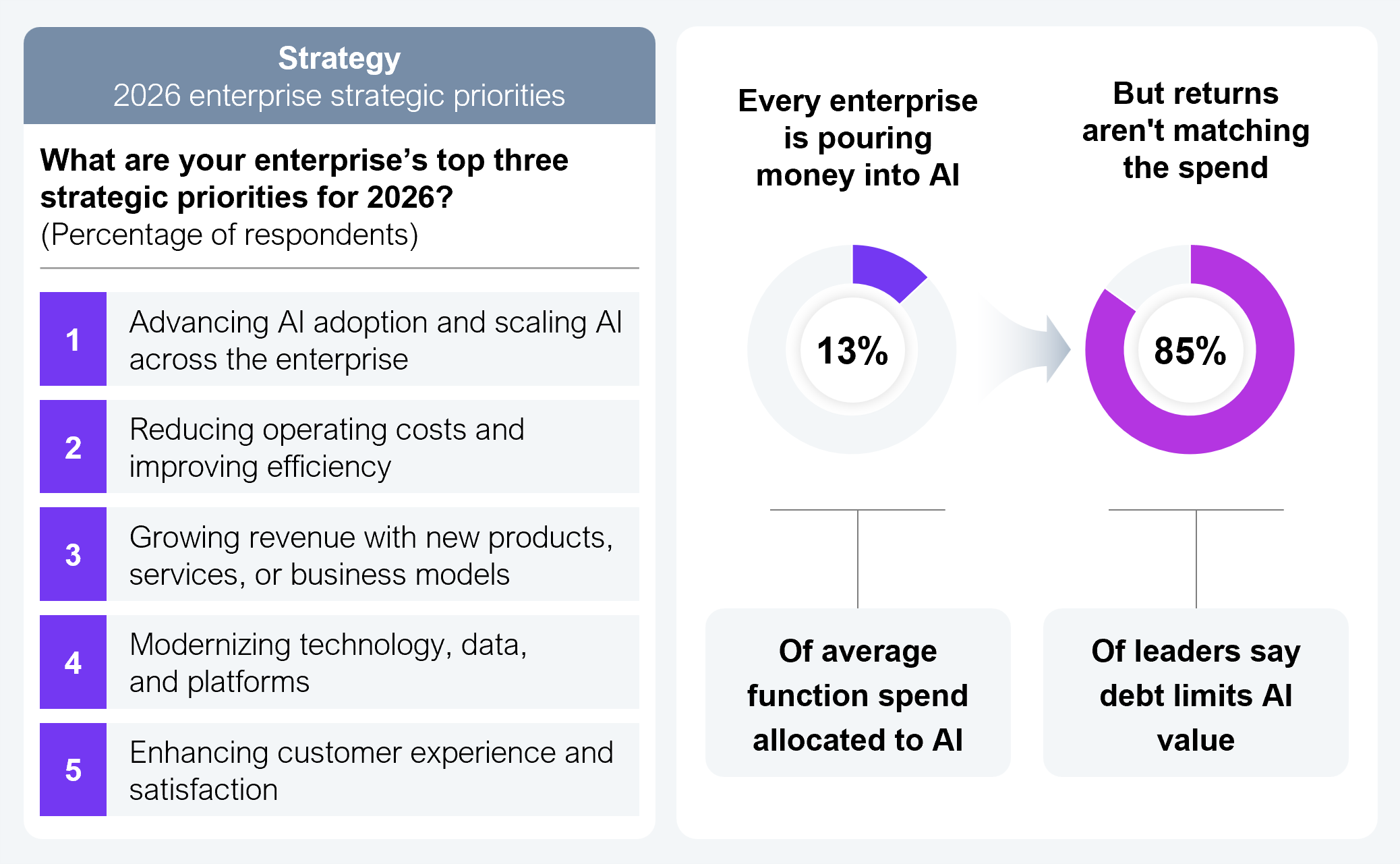

Boardrooms have made their bets. They are clear that AI is expected to drive the next decade of growth, productivity, and competitive advantage, and scaling AI across the enterprise is the number one strategic priority for 2026, as shown in Exhibit 8. But here is the problem. Nearly 13% of enterprise spend is now flowing into AI, while 85% of those same leaders admit that enterprise debts actively inhibit AI value. The money is moving. The foundations are not. Venkat Vagvala, CFA, who leads a large practice at a major global financial institution, is unequivocal about there being no shortcut to fixing what is broken:

Regulations of 50 years ago do not apply to today’s AI world. Hard work has to be done to fix enterprise problems. Hard work has to be done to remedy it.

— Venkat Vagvala, CFA, major global financial institution

Sample size: 2,002 global enterprise executives

Source: HFS Research in partnership with Genpact, 2026

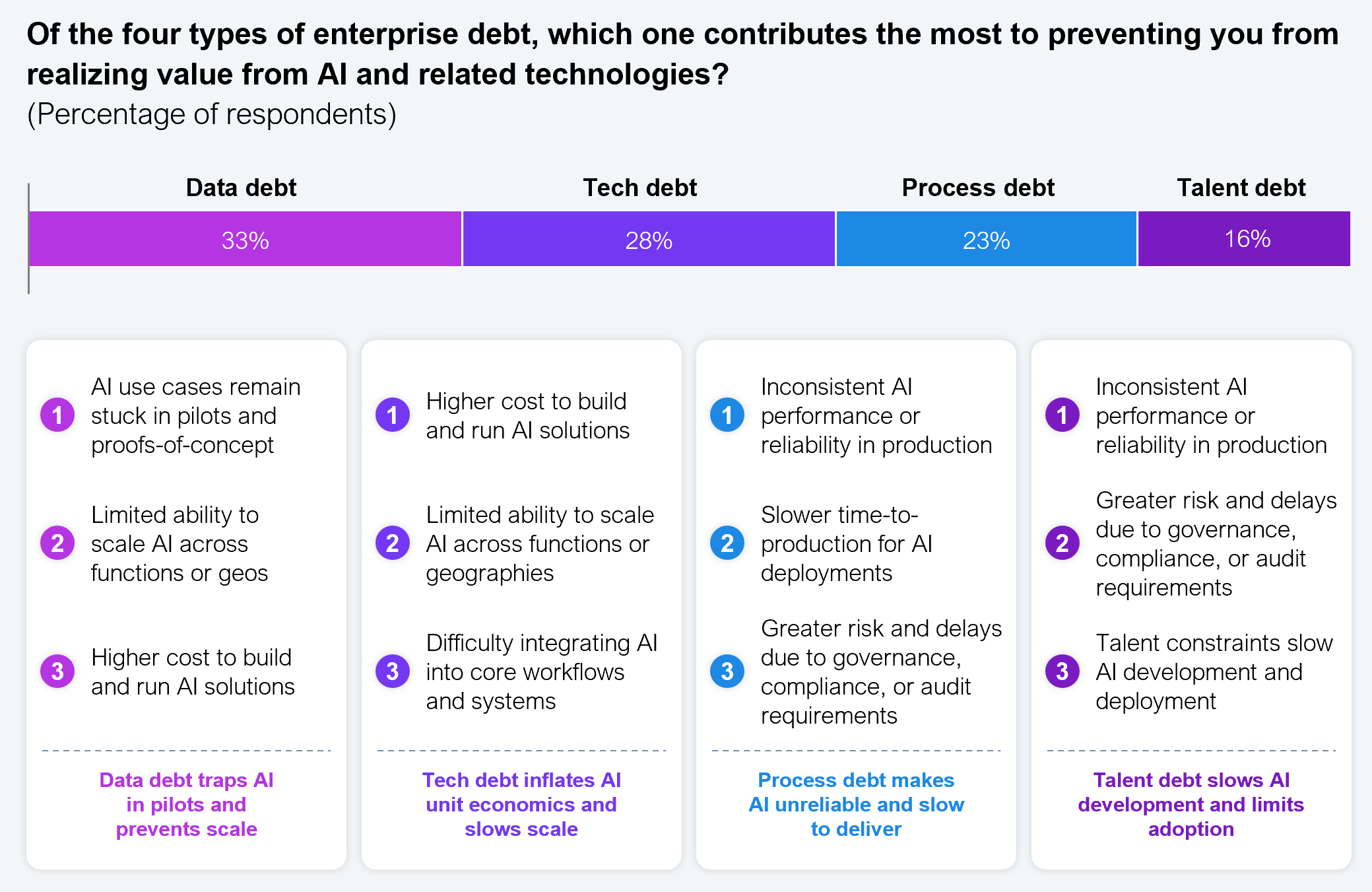

When we turn to the AI-specific debt problem, the picture sharpens considerably, as shown in Exhibit 9. This is a different view of the broader story of enterprise debts: narrower, more urgent, and with consequences already playing out in live deployments.

When enterprises deploy agentic AI before redefining their process workflows, building their data foundations, and preparing their workforce for a human-agent operating model, they are not accelerating transformation. They are encoding their existing inefficiencies into automated systems and running them at speed. A senior AI and data strategy leader at a major global financial institution captures the organizational trap that most enterprises have yet to confront:

You’ve still bolted on to your mess. We have forgotten the ability to unlearn. We are wedded to our rules and ways of working.

— Senior AI and Data Strategy Leader, Major global financial institution

Sample size: 2,002 global enterprise executives

Source: HFS Research in partnership with Genpact, 2026

Data debt emerges as the single biggest AI blocker, cited by 33% of respondents. Without trusted, integrated, AI-ready data, use cases stay in proof-of-concept permanently. Technology debt follows at 28%, inflating unit costs and making integration into core workflows difficult. Process debt (23%) introduces inconsistency and slows time-to-production for every agentic deployment. Talent debt (16%) compounds all three by slowing development and throttling the adoption that would justify the investment.

The consequences are severe. Data debt traps AI in pilots. Technology debt inflates AI unit economics. Process debt makes AI agents unreliable in production because they operate inside broken workflows. Talent debt limits both the adoption and the human judgment at the last mile that agentic operating models depend on. Every dollar spent on AI above a broken foundation is a dollar working against itself.

Lisa Stump, CDIO at Mount Sinai Health System, raises the question many leaders are now asking: Can enterprises use agentic AI to leapfrog parts of the debt problem while the harder foundational work continues underneath? The answer lies in the power of “and”: Use agentic AI where it can create near-term, imperfect wins, and continue the data, workflow, and integration work required for long-term sustainable value.

There are a million projects going on in getting data in shape and changing workflows. But I wonder whether we can take a leapfrog approach instead…Can agentic AI compensate for the messy workflows…at least in the short term…Can it operate across less-than-perfect data, multiple systems, and clunky workflows while we do the hard work to clean the data and streamline the work? In essence, we need to act on both for near-term, albeit not perfect, wins and long-term sustainable value.

— Lisa Stump, CDIO, Mount Sinai Health System

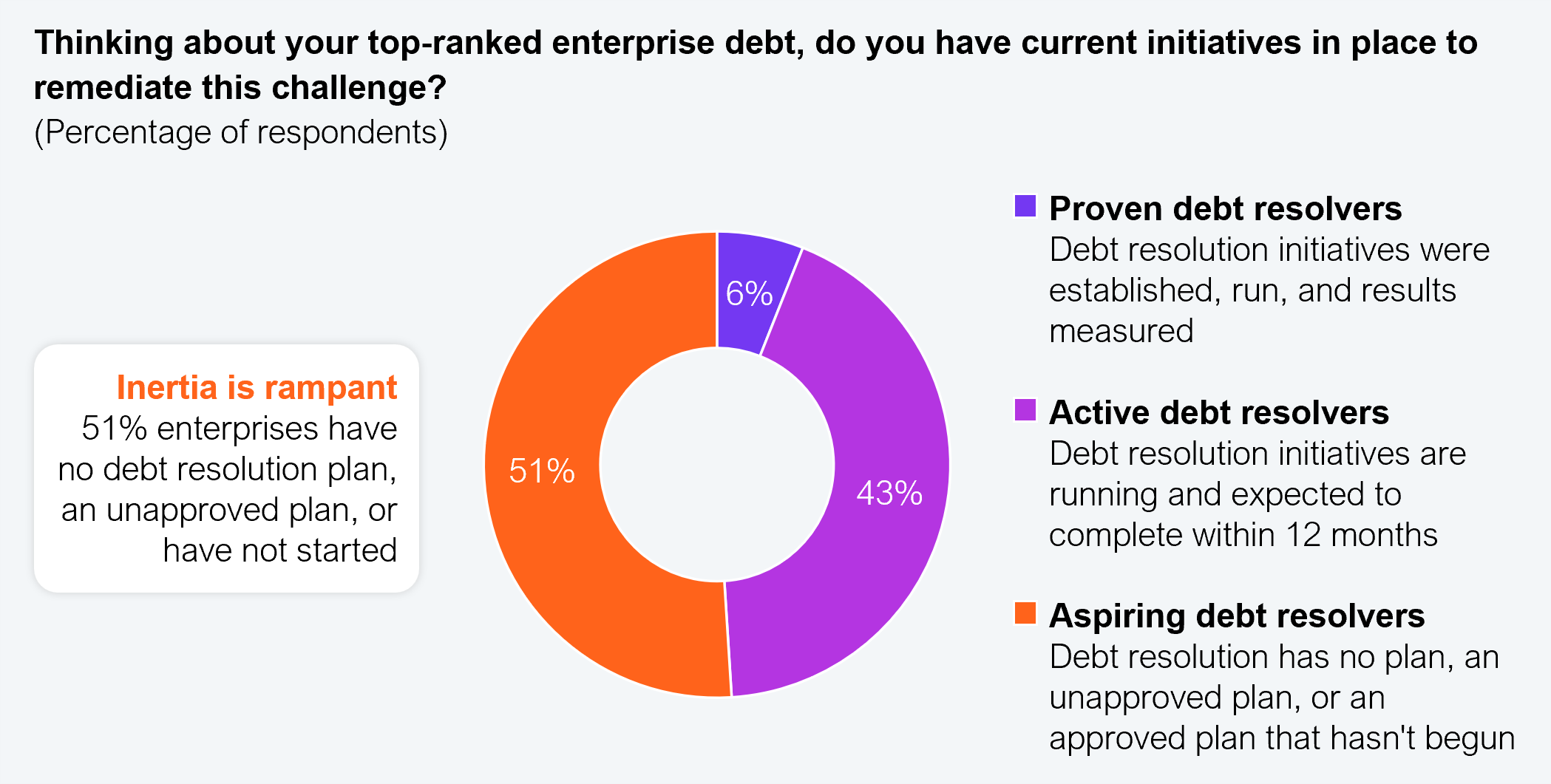

The weight of inaction is compounding the problem. More than half of enterprises have no funded debt resolution plan in place, meaning the foundation that AI depends on is not being built. Every quarter of inaction is another quarter of AI investment landing on ground that cannot support it.

A mere 6% are proven debt resolvers (see Exhibit 10). These are the enterprises that have established, run, and measured results.

Sample size: 2,002 global enterprise executives

Source: HFS Research in partnership with Genpact, 2026

The gap between inertia and action is worth $18 trillion. The AI era has permanently changed the impact of enterprise debt. Before, debts slowed performance. Now, they prevent AI from working. That is a categorical difference. An AI deployment on bad data means wrong decisions at machine speed, at scale, with no human in the loop. Process debt that creates workflow inconsistencies can lead AI agents to behave unpredictably in production. Leaders treating debt resolution as a separate workstream from AI strategy is a compounding liability. The two programs are the same program. Address the debts, and you unlock AI value. Ignore the debts, and you waste the investment.

Only 6% of enterprises are proven debt resolvers. They are the organizations that have not only initiated resolution programs but have also seen them through to measurable outcomes. They are a small cohort, but the most instructive one in this research. They have done what the majority are still planning to do and done it at a sufficient scale to know what works and what does not.

What separates the proven debt resolvers from the aspiring majority is not resources or ambition; it is the decisions they made differently across five dimensions that define how resolution gets done.

Among the small group of proven debt resolvers, ownership is unambiguous. Resolving enterprise debts sits with the CEO and board, not within a single function. These leaders treat data, processes, technology, and talent as a single system and fund, govern, and measure it accordingly. Adi Shetty, SVP, Global Head of People Operations and Systems, Visa, captures why clear accountability is the difference between progress and paralysis:

The moment the solution is ‘IT will solve it,’ we have lost the plot.

— Adi Shetty, SVP, Global Head of People Operations and Systems, Visa

Debt spans all four domains simultaneously, and no single C-suite leader holds authority over more than a slice. The CHRO cannot fix the data. The CTO cannot fix the process. The CDO cannot fix the talent. Without CEO-level ownership, programs get scoped to whatever one function can control, funded at whatever survives the budget cycle, and abandoned when the next priority lands.

Agentic transformation is a board, executive, and front-line imperative. It is not an IT initiative. Nan Li, SVP Transformation, Condé Nast, makes clear what effective governance requires:

Governance needs the golden triangle—people, process, and technology—and the CEO has to lean in and champion it.

— Nan Li, SVP Transformation, Condé Nast

Proven resolvers avoid this failure mode by treating enterprise debts and AI transformation as a single, enterprise‑wide mandate with shared accountability from the boardroom to the front line. Steve Taylor, EVP & CIO, Cenlar, reflects on what separates initiatives that succeed from those that stall:

There is one defining force behind the success of every major initiative in an organization: someone who truly champions it. Every successful project I have been part of shared this in common: a senior leader who owned the vision and an executive team that supports the vision to ensure it is carried forward. Technology may enable the outcome, but momentum comes from executive leadership. Success is ultimately determined by who steps up to drive it, believes in it, and takes responsibility for making it real.

— Steve Taylor, EVP & CIO, Cenlar

Aspiring debt resolvers tend to focus their bets on one or two debt types. Proven resolvers, by contrast, deliberately address all four.

Sample size: 120 (6%) proven debt resolvers across the 2,002 global enterprise executives

Source: HFS Research in partnership with Genpact, 2026

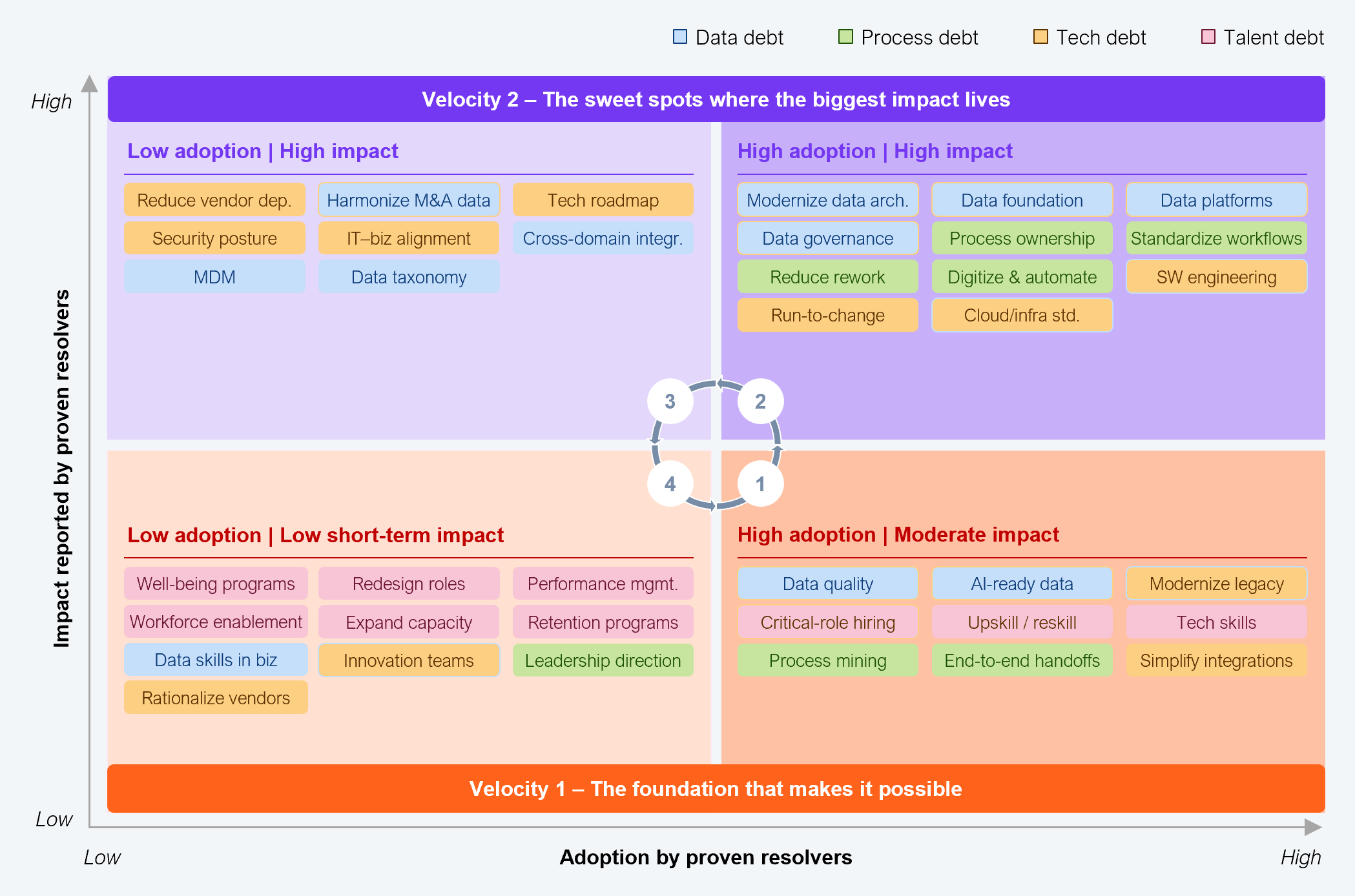

Exhibit 11 maps resolution initiatives of proven debt resolvers across two dimensions: how widely adopted each is among proven resolvers, and how much impact it delivers, resulting in four zones:

Proven resolvers do not work through these quadrants in a single sequence. They operate at dual velocities.

Velocity 1: Fix the foundations, place the long-term bets (Zones 1 and 4). Invest now in data quality, workforce upskilling, and targeted talent acquisition, the high-adoption foundation everything else runs on. Simultaneously, commit to the longer-horizon plays: role redesign, well-being programs, and performance management reform. These do not generate headlines in a quarter. They generate the organizational muscle that makes every other initiative compound.

Velocity 2: Capture the sweet spots and unlock the hidden gems (Zones 2 and 3). Zone 2 is where high adoption meets high impact; standardizing workflows, establishing process ownership, and digitizing and automating remove friction fastest. Zone 3 is where the hidden gems live; initiatives like IT-business alignment, a strong security posture, and cross-domain integration that deliver outsized impact in the right context, but only once the foundational layer is in place.

These two velocities run in parallel, not in sequence. Enterprises that wait for the foundation to be “complete” before moving on to sweet spots will wait forever. Enterprises that chase hidden gems without a foundation underway will fail, as most aspiring resolvers do. The dual velocity model enables proven resolvers to show short-term progress while building long-term resilience, satisfying both the CFO’s quarterly lens and the CEO’s transformation mandate simultaneously.

Aspiring resolvers gravitate toward what is obviously broken: digitize the manual work, write the technology roadmap, and standardize the workflows. These are the natural first instincts when a leader is staring at operational pain. Proven resolvers make a different choice. They invest in the capabilities that prevent debt from recurring, not just the symptoms that make it visible.

Companies that have completed debt resolution initiatives spend disproportionately on talent and data foundations, like hiring critical roles, upgrading data platforms, fixing performance incentives, governance, AI-readiness, and well-being. These are the “boring” investments that make subsequent change stick.

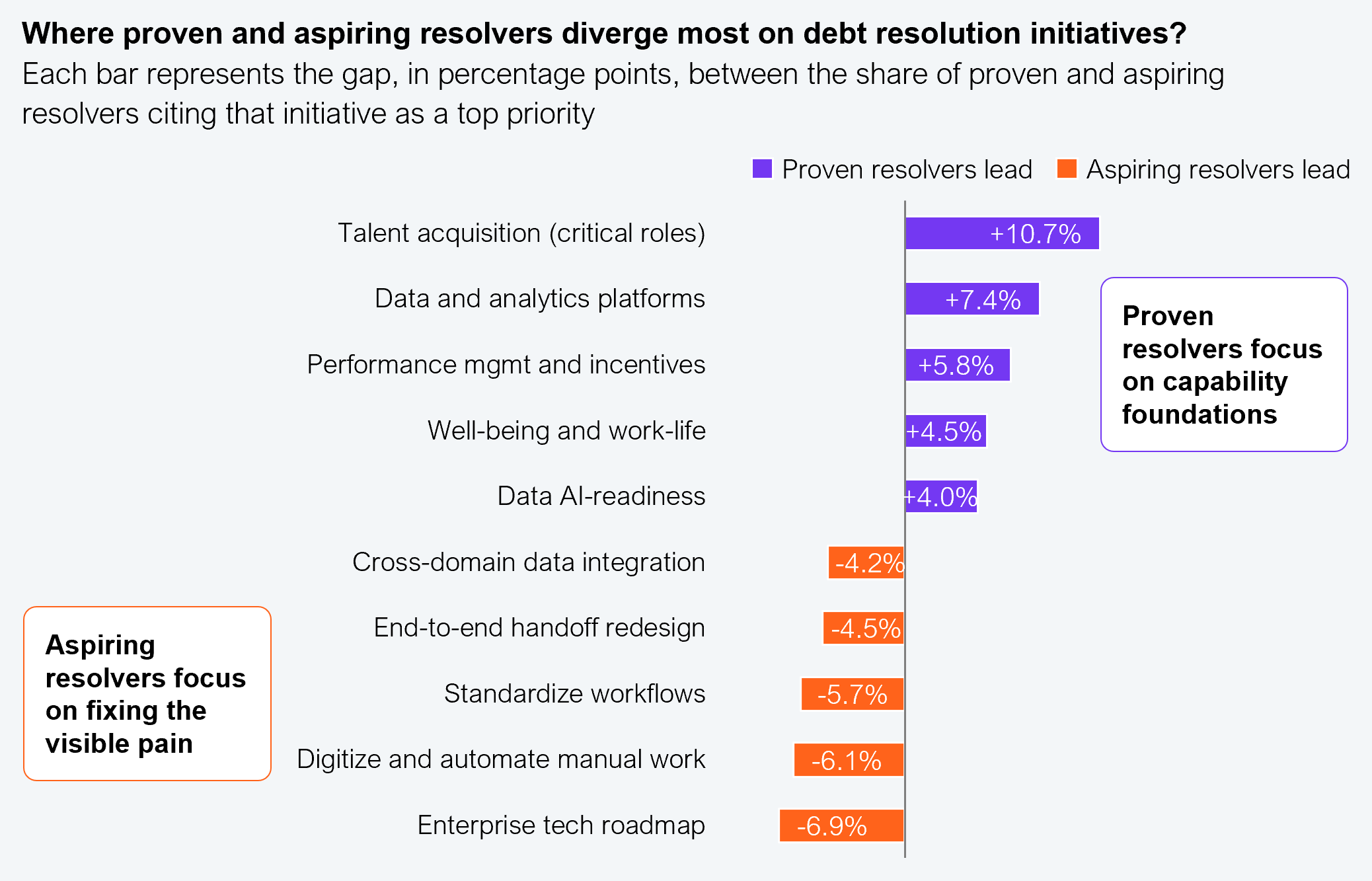

The data is unambiguous on where the divergence shows up across four dimensions.

Sample size: 2,002 global enterprise executives

Source: HFS Research in partnership with Genpact, 2026

Capability investments don’t show up immediately on a dashboard. All of them compound over time. Debt resolution is not a one-time clean-up. If you fix the surface without redesigning the underlying operating model, the debt comes back. The goal is not to reach zero debt; the goal is to build an organization capable of continuous, value-led transformation as technologies evolve and organizational learning improves.

Proven debt resolvers are not waiting for clean data, governed processes, and AI-ready talent before deploying AI. They are using AI to accelerate the resolution:

Debt resolution enables better AI. Better AI accelerates debt resolution. Proven resolvers are already running this loop.

Both proven and aspiring resolvers identify broadly the same problems. The diagnostic gap between them is small, but the execution gap is enormous. This is a choice. Proven resolvers ship, measure, and iterate. Aspiring resolvers remain stuck in analysis and planning.

Speed of execution beats precision of strategy every time.

The lesson from the 6% proven resolvers is not about having a clever framework. It is about organizational character. Enterprise debt resolution and AI transformation are the same program, just seen from different angles. One looks at the liability on the balance sheet, the other at the opportunity in the AI roadmap. The enterprises that close the gap will be the ones that build the data estates, process architectures, workforce capabilities, and technology foundations to enable AI to perform sustainably at scale, with humans firmly at the center. The gap between proven and aspiring resolvers is a courage gap, not a planning lapse. As Maharaj Mukherjee, PhD, Senior Vice President at a leading US-headquartered global bank, points out, the biggest barrier is not the technology itself but the fear, reluctance, and inertia that prevent organizations from embracing new ways of working:

The main thing that is holding back the full promise of AI is the fear and the reluctance to adopt AI because it’s something new. And once people can get over that inertia, I think we should be able to all fully realize the capacity of AI.

— Maharaj Mukherjee, PhD, Senior Vice President, leading US-headquartered global bank

Every dollar spent on AI without resolving debts is a dollar working against itself. Every quarter spent planning debt resolution without acting is a quarter the 6% are using to pull further ahead.

The numbers are unambiguous:

That gap between acknowledgment and action is not a strategy problem. It is a courage problem, and enterprise value is eroding inside it, quietly, quarter by quarter.

The root cause of inaction is structural. Enterprise debts span all four domains simultaneously, yet no single C-suite leader holds authority over more than a slice. The result is a collective action failure: everyone knows it is a problem, but no one has the mandate to treat it as a whole-system problem. This is why CEO ownership is not a best practice; it is the precondition.

Every enterprise carries a different mix of debt across technology, process, data, and talent, and the value lies in clearly diagnosing that mix. Proven resolvers treat debt resolution and agentic transformation as one program, owned at the top, funded as a portfolio, and sequenced to build capability, not just fix visible pain. Leadership needs to understand it holistically, solve for it deliberately, and move before every answer is perfect.

Do the diagnosis for your industry and function to assess where the debt sits, what it is costing you, and how to sequence resolution to unlock your share of the trillions on the table.

Know where your debt is heaviest. Know what the opportunity is. Know what to fix first. That is the whole plan.

Register now for immediate access of HFS' research, data and forward looking trends.

Get Started

If you don't have an account, Register here |

With the exception of our Horizons reports, most of our research is available for free on our website. Sign up for a free account and start realizing the power of insights now.

Our premium subscription gives enterprise clients access to our complete library of proprietary research, direct access to our industry analysts, and other benefits.

Contact us at [email protected] for more information on premium access.