This HFS Research Take 5 report, produced in partnership with Cognizant, is for US enterprise leaders and BPO buyers evaluating how to close the gap between patchy AI adoption and ambitious productivity expectations by demanding outcome-owned, risk-bearing partnerships from their business services providers.

Executive summary

Enterprises are stuck in islands of AI as most have moved beyond proofs-of-concept. However, only 15% are in the run‑state. Despite this sluggish progression, they’re expecting a 30%+ productivity step‑change across business functions over the next three years. This gap between current patchy adoption and very bold expectations is precisely where enterprises are looking for strategic, risk‑bearing partners. Enterprises are actively reengineering their operating models, deepening synergies with hyperscalers, and increasingly turning to their BPO providers for comprehensive stewardship in this AI-led metamorphosis.

HFS Research, in partnership with Cognizant, surveyed 101 senior enterprise leaders in the US across seven diverse industries to illuminate prevailing AI adoption trends, future imperatives, ecosystem dependencies, and evolving expectations from BPO partnerships.

The survey uncovered five key takeaways:

-

-

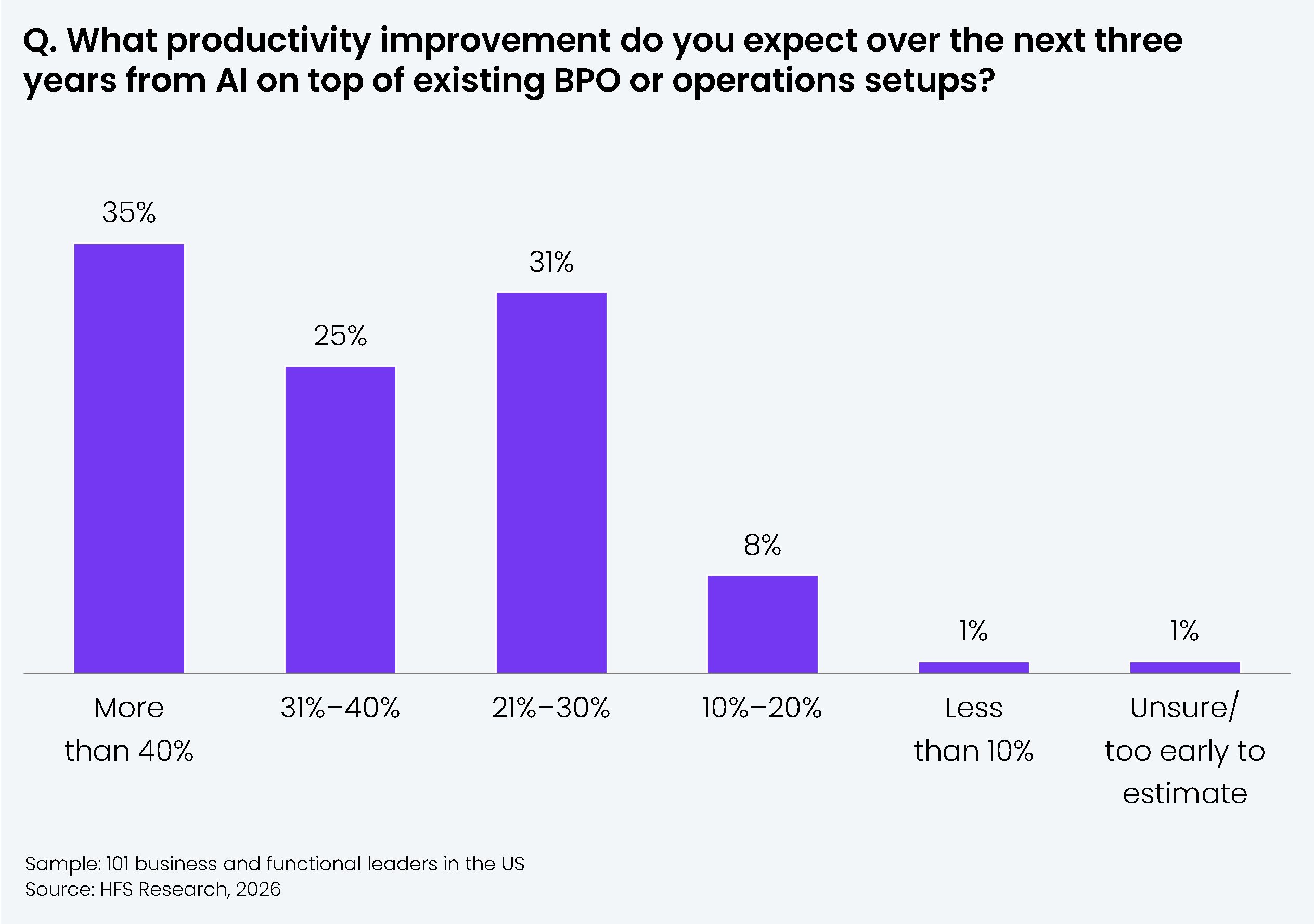

Over the next three years, more than 60% of enterprises anticipate that AI will augment their existing BPO operations with a productivity uplift exceeding 30%.

-

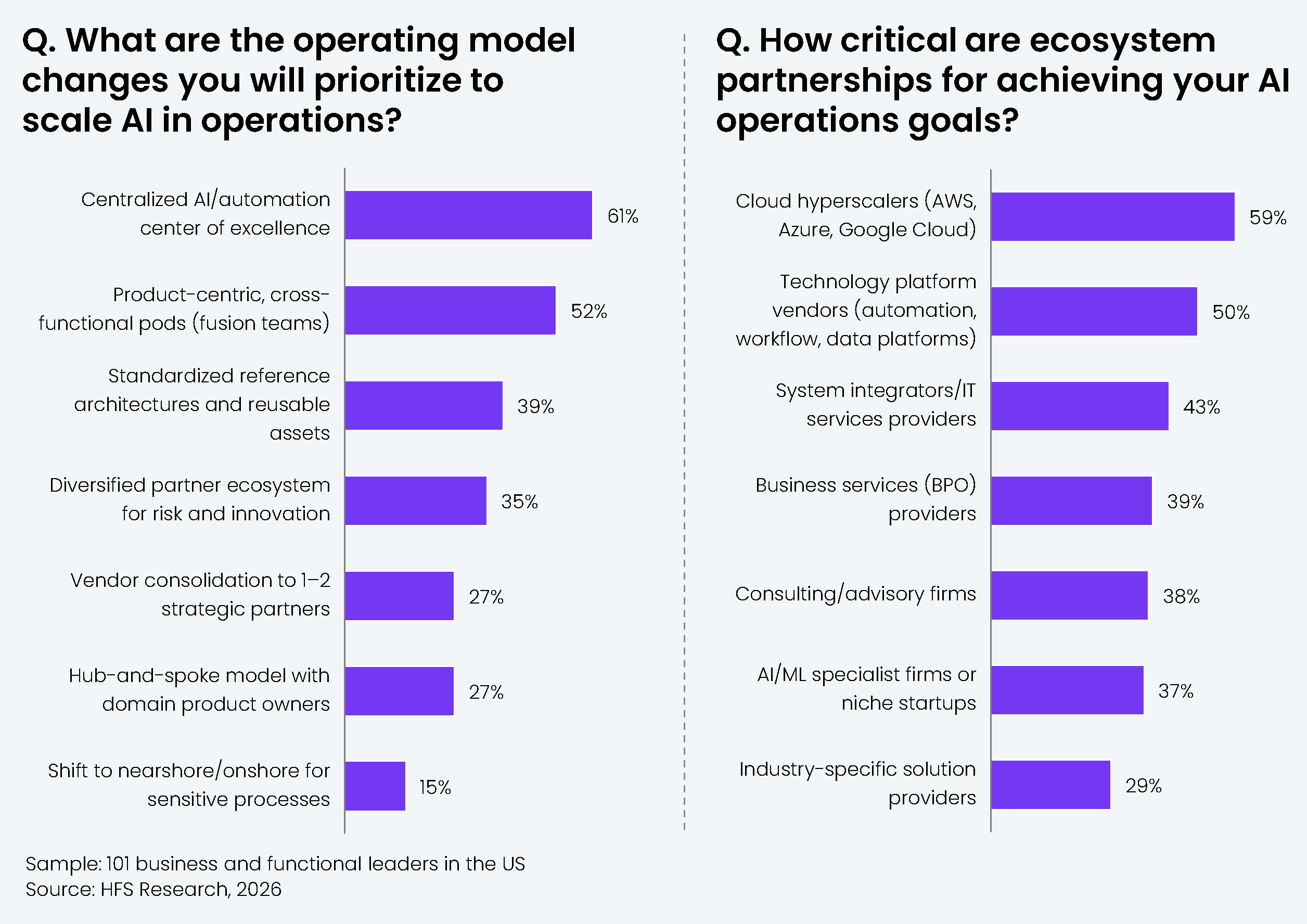

To scale AI from isolated endeavors to enterprise-wide transformation, enterprises are rewiring their operating models and deepening reliance on strategic alliances with hyperscalers and technology platform providers.

-

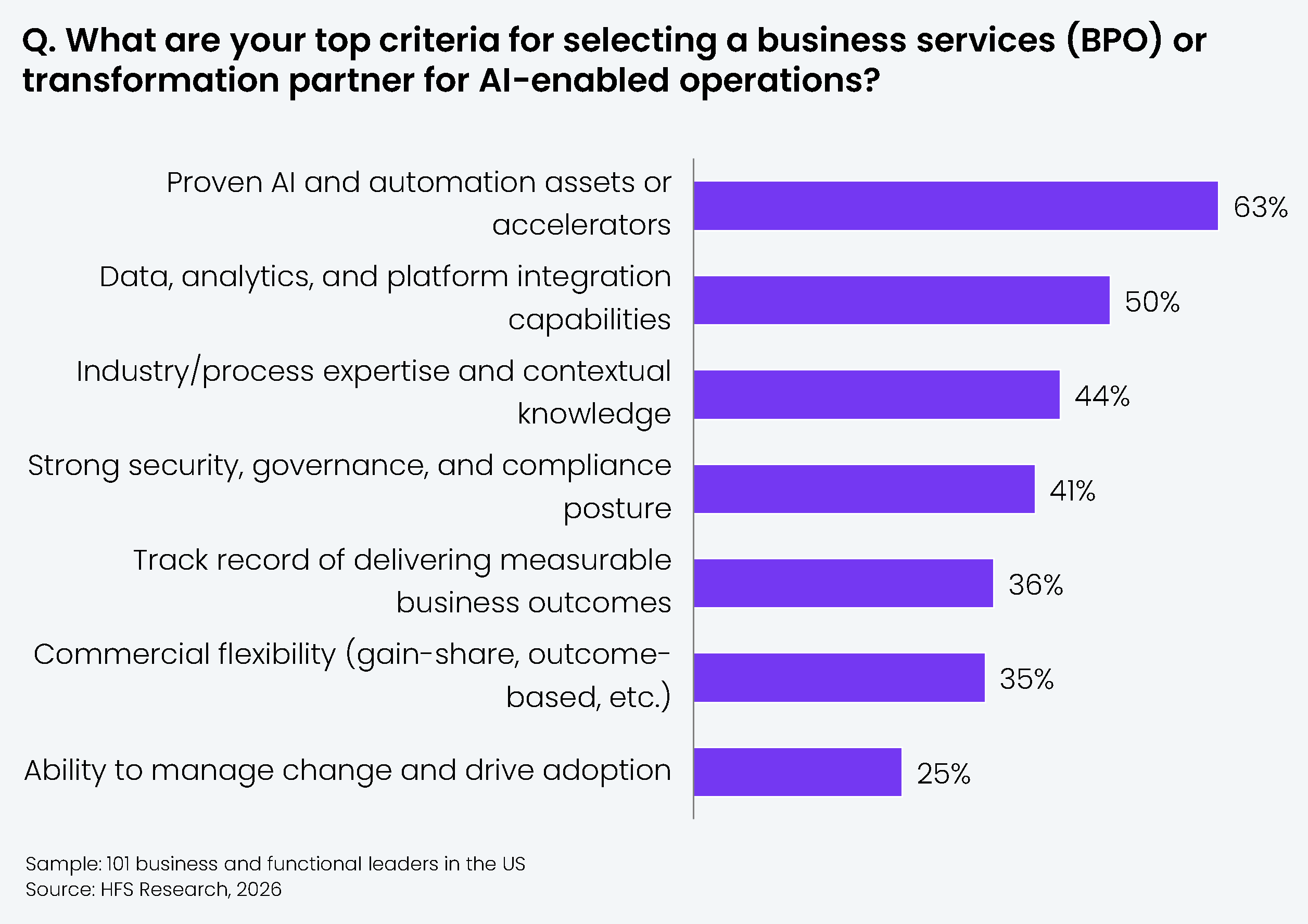

While selecting BPO providers, enterprises are looking for proven IP, platform integration capabilities, and industry/process expertise.

-

Enterprises are gravitating towards an evolved engagement model where:

1. BPO providers accept end-to-end ownership and accountability

2. AI is embedded into existing workflows offering platform-as-a-service and anchored in vertical use cases.

-

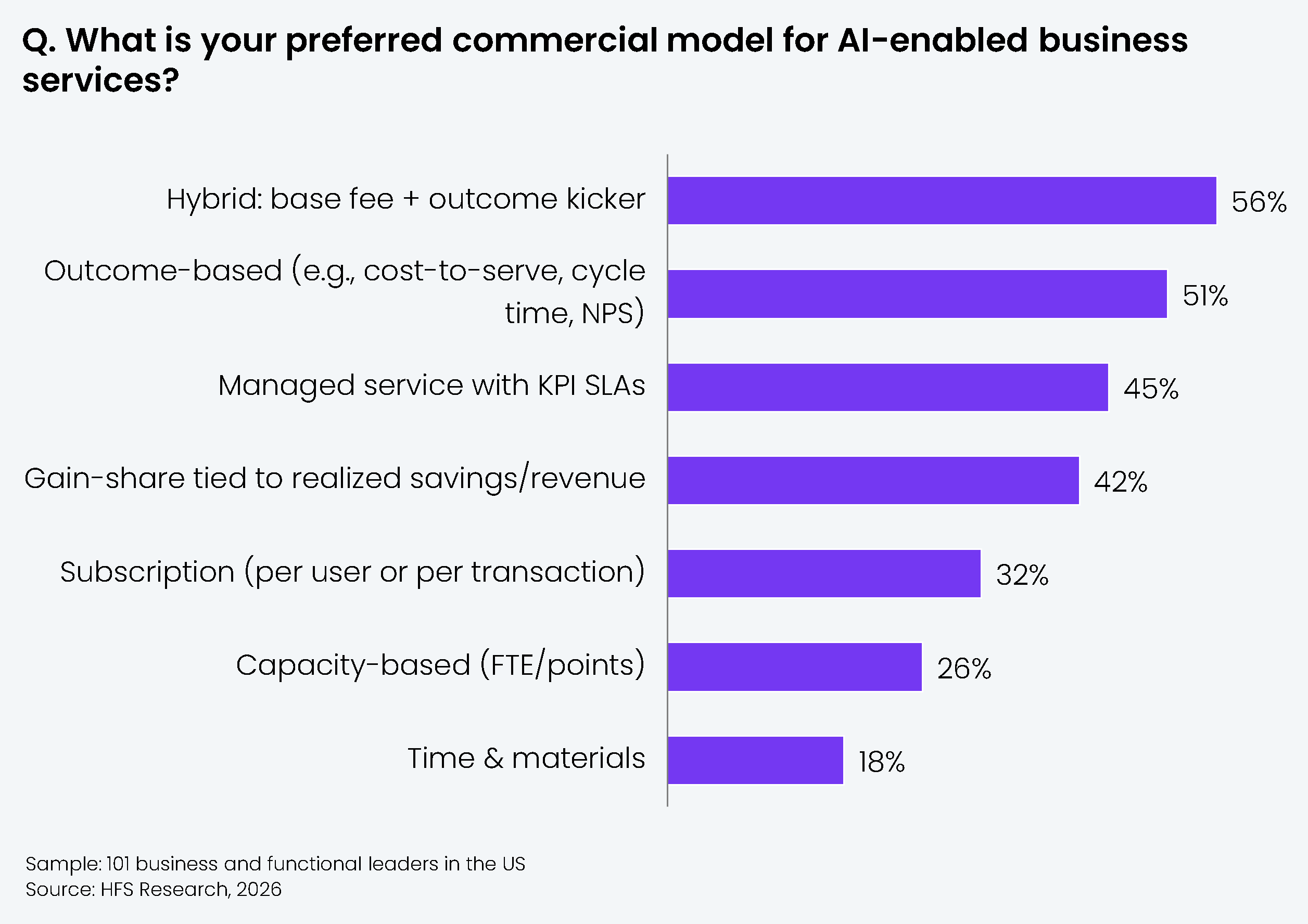

Risk alignment is fast becoming the lodestar of next-generation commercial models. Enterprises are increasingly favoring a “hybrid” construct, anchored in a foundational base fee, augmented by an outcome-linked “kicker.”

The Bottom Line: Enterprises are demanding AI‑embedded, outcome‑owned operations from their BPO partners. Their overall partner ecosystem strategy and internal organizational readiness are the key prerequisites for success.

- While most enterprises have progressed beyond AI proof-of-concepts, a mere 15% have reached a sustained run-state. They find themselves in what one might call an “AI holding pattern.”

- Despite this disconcerting lack of scaled success, optimism abounds: a striking 91% anticipate minimum productivity uplift of >20% from AI layered atop their existing BPO ecosystems.

- This gap between current patchy adoption and very bold expectations is precisely where enterprises are:

- Rethinking and reengineering their operating models in pursuit of structural reinvention

- Deepening partnerships with hyperscalers, followed closely by technology vendors, to modernise their digital core

- Seeking BPO partners with the strategic mettle and risk appetite to shoulder end-to-end accountability.

- Enterprises prioritize setting up AI/automation centers of excellence (COEs) and cross-functional PODs to ensure:

- There’s a dedicated unit so pilots don’t die midway

- Every business function becomes a stakeholder and owns the pilot-to-production journey

- Hyperscaler relationships (including AWS, Microsoft Azure, and GCP) are considered most mission critical in achieving AI goals.

- Beyond hyperscalers, enterprises are turning to primary platform vendors such as SAP, Microsoft, Oracle, Salesforce to upgrade to the latest versions of these platforms with embedded AI capabilities.

- Enterprises prioritize pre‑built AI assets (63%), data/platform integration (50%), and deep domain understanding (44%) plus the ability to manage security and deliver measurable outcomes.

- When picking partners, they are betting on the builders (context-specific solutions) Show, don’t tell!

- The “wow” factor of basic agent assist (summarization, email drafting, knowledge search) has already become table stakes. Clients now want context‑driven, probabilistic AI that can, for example, use multi‑source data to distinguish between genuine write‑off requests and leakage in a US$70M revenue leakage scenario.

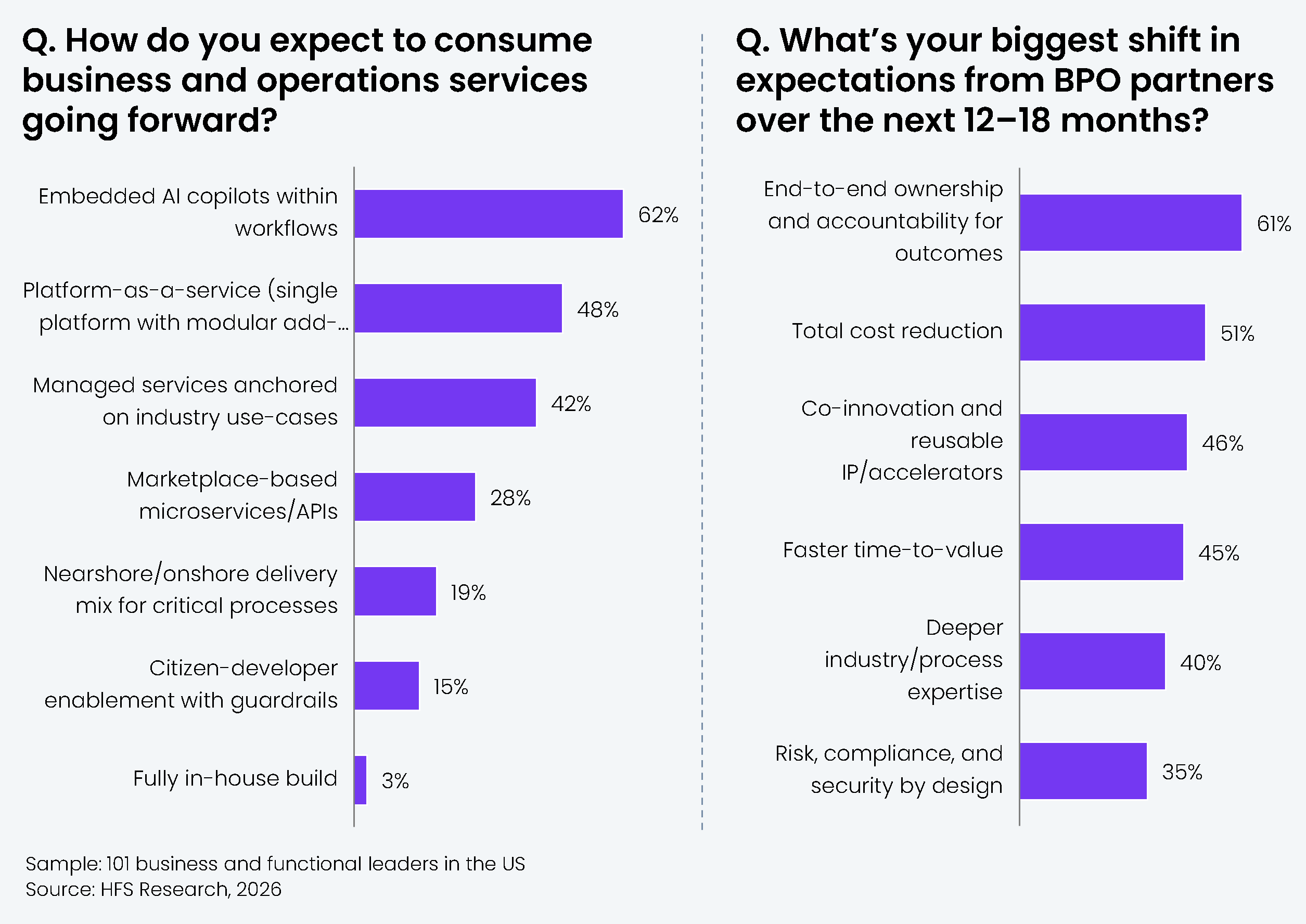

- Enterprises are fast acquiring greater lucidity on the elusive question of “how to AI.” They are poised to implement two immediate transformations: first, in the way they consume business services; and second, in the evolving nature of their engagements with service providers.

- The emerging model of engagement is one wherein AI is getting manifested through copilots woven into existing workflows, platform-as-a-service offerings, and managed services tailored to vertical-specific use cases.

- Over the next 12 to 18 months, the most pronounced shift in enterprise expectations from their BPO partners will be a clarion call for ownership and accountability of outcomes. This demand is voiced by 61% of the respondents, eclipsing even traditional imperatives of cost reduction.

- Traditional constructs such as time-and-materials and capacity-based pricing are rapidly falling out of favor. Only 18% of respondents still cling to the T&M model, signaling a decisive shift away from remuneration based on input effort.

- A hybrid model combining a base fee to assure provider sustainability with outcome-based incentives to drive performance is emerging as the most preferred paradigm (56%), offering a judicious balance between risk and reward.

- Nearly one in two enterprises (51%) are ready to embrace pure outcome-based models, indicating a growing appetite for accountability and value realization over mere transactional delivery.

The Bottom Line: Enterprises are demanding AI‑embedded, outcome‑owned operations from their BPO partners.

Their overall partner ecosystem strategy and internal organizational readiness are the key prerequisites for success.

The era of isolated pilots and legacy service models is waning. To unlock the full transformative potential of AI, enterprises must pivot to outcome-centric partnerships, invest in robust data and governance foundations, and institutionalize AI through centralized operating models.

- Prioritize BPO partners that embrace end-to-end ownership of outcomes. Embed commercial models such as hybrid or pure outcome-based contracts to align incentives and share risk.

- Establish CoEs and fusion teams under a unified governance model to ensure standardization.

- Invest in data estate modernization, MLOps, and privacy/security infrastructure to de-risk GenAI deployment and maximize ROI.

-

-

Restructure partnerships around accountability

-

Institutionalize centralized AI governance for scaling

-

Double down on data and MLOps foundations for embedded intelligence