The move toward platforms and away from functionality is radically changing the game for the IT and BPO services providers, which have feasted on complexity for decades. IT services firms have relied on complex apps that require constant workarounds and human intervention, while BPOs have grown up on processing work that couldn’t be standardized within an ERP suite. The recent Salesforce acquisition of integration firm MuleSoft is a further move in this trend that enterprise clients want greater simplicity and less need for constant human intervention from their software investments.

Salesforce adds MuleSoft with the aspiration to be de facto one-stop customer enterprise management suite

Salesforce has made its largest-ever acquisition, splashing out a huge (reported) $6.5 billion to add the data integration capabilities of MuleSoft as it takes aim to become the de facto one-stop-shop customer enterprise management suite.

While the addition makes complete sense strategically and, if nothing else, adds new revenues to the Salesforce empire, the biggest question mark is around the price tag—especially when you consider that just a few years ago Cast Iron, which has comparative products, was snapped up by IBM for about $100 million and Cape Clear by Workday for a similar sum. Has Salesforce blown the last of its available cash? Or is this a near-final move from the firm to shore up its CRM dominance and cement its position as the only enterprise show in town?

The shift from apps and functionality to platforms is well underway

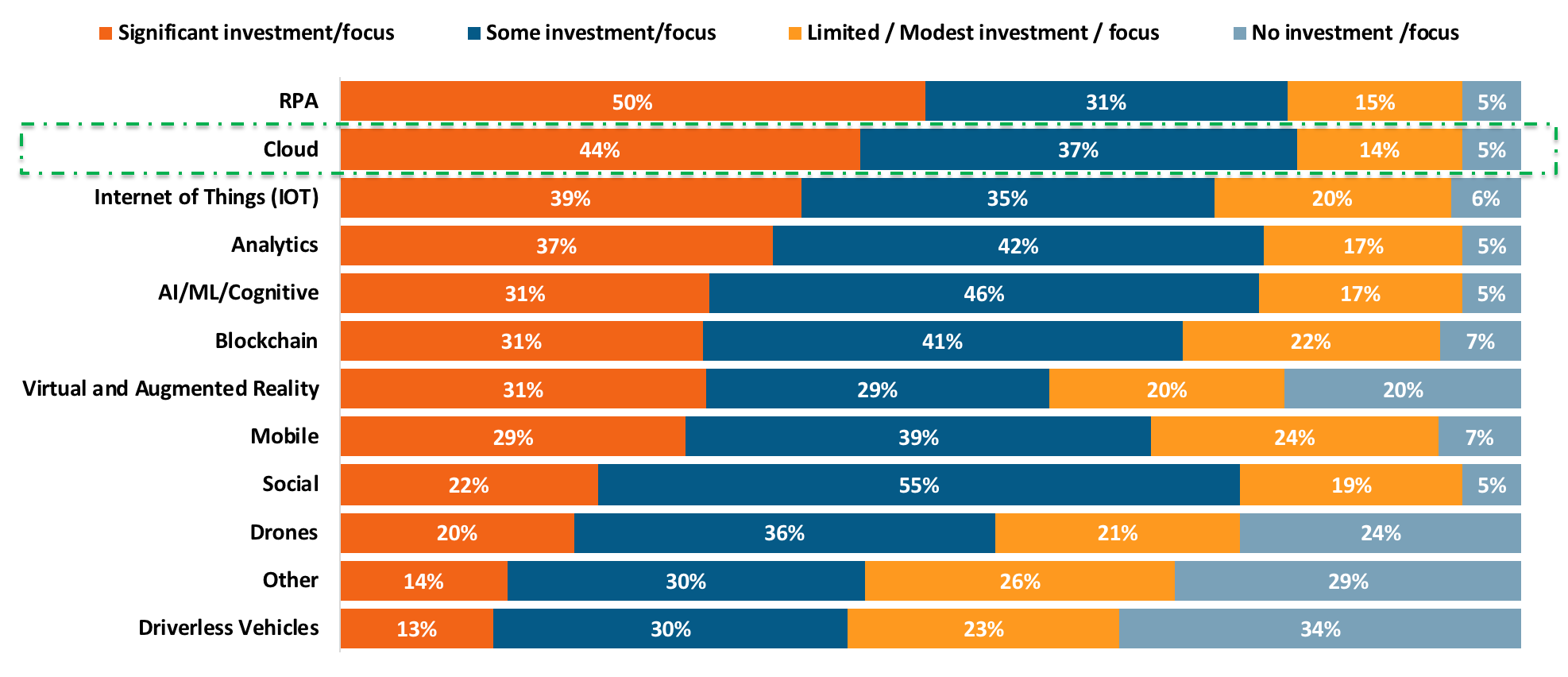

Exhibit 1 shows the investment focus that Global 2000 operations leaders have for next year; cloud is number 2. We see cloud representing more than just As-a-Service and virtual machine computing, but as an analogy for more flexible and agile computing, which provides enterprises a technology platform to adapt to the way they operate their businesses. RPA’s dominant position in the list reflects another aspect of this—organizations expect software to do more of the task, without the slack being taken up by human processing. This means that enterprises expect software to be much more flexible and able to fit their business purpose. So, a platform that helps to integrate software across a business or process without the need for costly and resource-intensive workarounds and recoding is dynamite.

Exhibit 1: Operations leaders focus on cloud platforms and software that simplifies processes

Q: How much investment/focus is your organization making in the following in the next year to help you achieve operational cost saving goals?

Source: HfS Research in conjunction with KPMG, “State of Operations and Outsourcing 2018”, March 2018. Sample: interim enterprise buyers = 250

Salesforce now boasts a complete customer engagement platform

In recent years, Salesforce has ambitiously repositioned from providing a set of separate CRM tools to delivering a complete customer engagement platform. Central to this is the company’s AI engine, Einstein. For clients to get the maximum benefit of this complete CRM solution with all customer data to hand, enterprises need effective integration tools that connect Salesforce with their other business application systems. Cue MuleSoft, which enables connectivity with other CRM systems such as Siebel and Microsoft Dynamics; other ERP systems such as SAP, NetSuite, and Oracle EBS; and even other HR systems including Workday.

It’s no surprise that many Salesforce service providers, including Appirio (a Wipro company), Capgemini and PwC, have partnered with MuleSoft to deliver this enterprise-wide data capability to clients.

The market is ready for a holistic CRM solution, but does this render service providers useless?

The market is ready. Enterprise clients are starting look at Salesforce deployments more strategically. Although most buyers continue to focus on achieving fast implementations, some are starting to realize the importance of aligning their Salesforce strategies with their overall business strategy. In other cases, Salesforce services providers are demonstrating the need to use Salesforce as a platform to bring business solutions rather than to consider Salesforce as individual technical cloud implementations. In addition, Salesforce customers want Salesforce to integrate the applications it provides them. Their clouds and products need to work together and having “one throat to choke” should play in their favour, provided Salesforce provides the integration for free (or at a reasonable cost). Owning an integration platform such as MuleSoft will make the whole integration process easier and more cost effective.

Enterprises should adopt a holistic and strategic view of their Salesforce deployment, one that aligns with the overall CRM strategy. Clients like Salesforce because of the flexibility it provides for building on the platform and its ease of use. The additional capabilities of MuleSoft offers a whole new value proposition of an enterprise-wide strategic solution. Having access to all customer data enables quick insights leading to better-informed decisions. It also potentially facilitates data regulations and privacy law enforcement, such as GDPR.

So, what does this mean for the Salesforce service providers?

While the addition of the MuleSoft technology brings important integration capabilities, there are still many opportunities for service partners to deliver value. The definition of value, however, is shifting. To survive in this market, Salesforce service providers must be able to deliver the following:

Service providers offering Salesforce services must invest in business partnering capabilities as platformization reduces the need for complex technical services

In short, successful service providers have no choice but to keep moving up the value chain from simply integrating and managing technology to becoming a business partner that delivers consulting and advice throughout deployments.

Having a deep understanding of a client’s culture, business, and technical requirements, as well as the industry sector specifics, is emerging as the differentiating service provider skill.

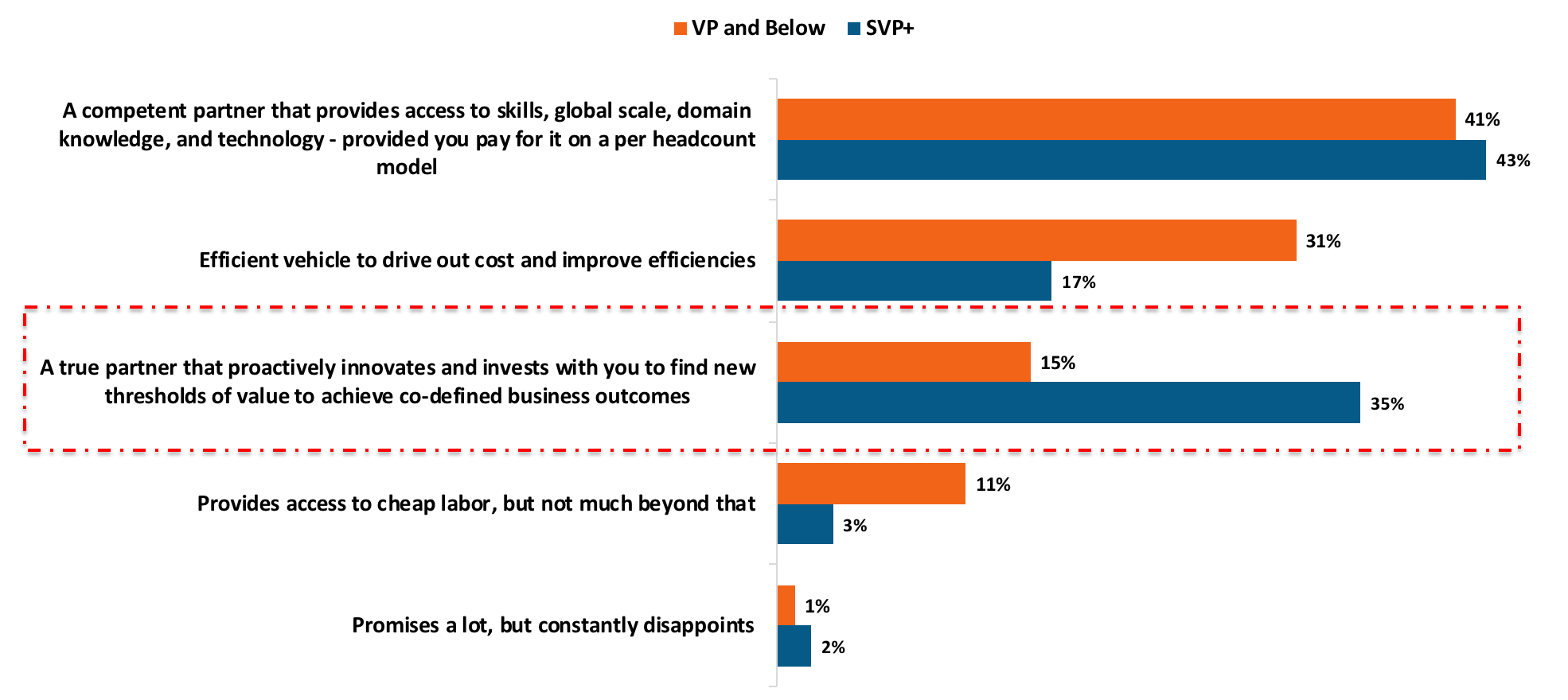

One of the key reasons for enterprises investing in broader platforms is to reduce their reliance on costly integration services. Our recent study clearly shows that well over a third of senior leaders (SVPs and above) view their primary service provider as a partner that proactively innovates with them to achieve jointly defined business outcomes:

Exhibit 2: Many senior leaders believe their service partner can evolve with them

Q: How would you best describe your current primary service provider?

Source: HfS Research in conjunction with KPMG, “State of Operations and Outsourcing 2017”, sample: global 2000 enterprise buyers = 464

What’s encouraging here is that enterprise services clients, by and large, do not view their service providers as mere efficient cost take-out vehicles, which was how well over half viewed them a couple of years ago. While 43% of SVPs and above see service providers as competent partners who can deliver the goods, another 35% view them as innovation partners that can work with them to achieve co-defined business outcomes. This is a breakthrough for the services industry.

The bottom line: The door is wide open for ambitious providers willing to invest in developing their talent, but closing firmly shut for those perpetuating what worked in the past

There has never been a time in the history of services where we’ve arrived at such a pivotal turning point—what used to work for clients is now commodity—such as bread and butter Salesforce implementations—and those service providers wanting to avoid this drain-circling spiral into insignificance must make serious investments in their internal capabilities to partner with their clients.

This means that more people can work in close proximity to their clients with real capabilities rolling out automation roadmaps, designing digital business models, and working with clients to develop predictive data models and smart cognitive strategies. Sadly, there isn’t much of an available pool of eager college graduates ready to leap into these roles at low wage rates, so providers need to reinvent themselves radically as true learning establishments and universities for their emerging talent.

Ambitious staff increasingly want to invest their careers with firms that are prepared to invest in their talent, especially a large proportion of millennials who prefer to have more on-the-job training and a longer trajectory of development than merely an attractive wage. The future isn’t about buying packaged consulting; it’s about partnering with services firms whose stakeholders want to co-invest in themselves and their clients with a long-term vision and definitive plan. The model has changed forever, and we can only watch, learn, and work with it as it unravels piece by piece.

Register now for immediate access of HFS' research, data and forward looking trends.

Get StartedIf you don't have an account, Register here |

With the exception of our Horizons reports, most of our research is available for free on our website. Sign up for a free account and start realizing the power of insights now.

Our premium subscription gives enterprise clients access to our complete library of proprietary research, direct access to our industry analysts, and other benefits.

Contact us at [email protected] for more information on premium access.