Most companies are trying to put the customer at center stage, but there’s too much confusion, and there are too many over-hyped buzz words, especially in the big banks. A holistic front-to-back transformation is the key to unlocking the potential for great customer experiences. At our HFS executive roundtable in London, HFS and Genpact brought together 15 banking leaders and first movers to discuss the challenges and path to using experience innovation to design better experiences.

Disruption will challenge banks in the hyperconnected future state

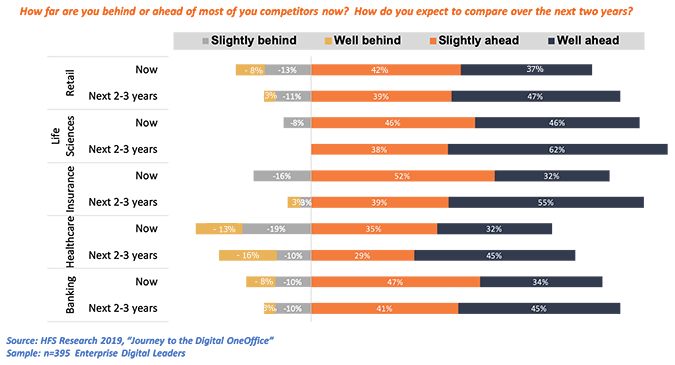

Among many organizations across the board, there’s a sense of complacency about the level of digital disruption that the hyper-connected future state will bring to their industry (Exhibit 1).

Exhibit 1: Banks ooze digital complacency

Source HFS Research

New ways of thinking and operating are helping banks elevate CX

This group of forward thinkers at our London roundtable was ready to discuss the issues potentially keeping banks from being ahead of their competitors and how to change the way they are preparing. “Not reacting and fulfilling CX is a real risk,” as one delegate put it. First is a list of some of the challenges banks face; some examples of how they are attempting to stay ahead of CX follow:

- Think about the customer’s end-to-end view. Don’t think about CX only in the context of individual products. A customer should have a consistent experience across products and interfaces. “Customers don’t think in silos,” as one delegate put it.

- Develop talent into a more innovative workforce. Many banking delegates commented that they have less concern about who the competitors will be and more about developing competitive talent. They mentioned the concept of T-shaped vs. V-shaped employees; that’s the idea of having people with broader expertise (Ts) rather than depth (Vs). Delegates noted that more T-shaped talent might result in both a leaner headcount and broader expertise. Another challenge is successfully recruiting data scientists for days full of unengaging and unfulfilling tasks (e.g., compliance).

- Get out of the big bank comfort zone with new thinking. Some banks are creating “mini-startups” within traditional banks to focus on customer outcomes and new business models, and they are partnering with FinTechs.

- Shed legacy ways of operating that are holding banks back. “We aren’t set up to reward CX” was a popular sentiment. Traditional banks are focused on risk and cost reduction; they need to re-align and improve their methods for holding teams accountable.

Banks are changing how they compete, measure CX, and design experiences:

- Focusing less on the competition and more on the customer. Two delegate quotes sum this up perfectly: “Look at the fringes of industries, look beyond what your competitors are doing, focus on the customer’s goal, and have a broad open mind,” and “You can set all the goals in the world and get something implemented on time and within budget that the customer hates or doesn’t see the value add with. Starting with the customer in mind is a great approach.”

- Developing new ways of measuring CX: There was no consistent approach to measuring CX by delegates. While some considered the Net Promoter score as the gold standard, others used a mixture of KPIs; all agreed that the key is to keep them fluid and look at all angles. “We measure it in several ways—first, KPIs governing the speed of execution, resolution time of queries, transparency of information regarding transaction status, and more process-specific metrics such settlement rate, fail rate, confirmation match rate. Second, we have client relationship management teams who work with clients on a range of satisfaction scores, which are a blend of service metrics, SLA performance, escalations, and client service metrics.Third, we measure internal Manual touchpoints measuring the number of times that a transaction requires human intervention, as potential opportunities to automate a process.”

- Using design thinking to innovate experiences. Most banks are learning how to scale design thinking as a problem solving and implementation framework (including non-CX and design teams) and bringing it together with agile deliveries. Making empathy a key piece of design is critical.

- Organize around customer journeys and each stakeholder’s role therein: “Having a ‘customer-aware’ mindset is key, e.g., ensuring everyone in the chain understands how their part of the process can impact client experience and all working cohesively together to ensure improvements are driven across the whole chain. Understand your client journey; make sure it is well mapped out, articulated, and that it attributes owners to each stage of the journey. Speak to your clients to understand their pain points and how they evaluate good versus bad—don’t just assume.”

The Bottom Line: Banks need to get out of their comfort zones to innovate and continuously deliver on customer experience.

“We’ve become far too cozy,” said one of the delegates about not feeling an incentive to change. In the hyper-connected economy, changes will inevitably become necessary, so banks need to put the pieces in place now to be competitive in the future. These design leaders agreed that you’re never “done” creating customer experiences. CX is constant and evolving—it requires an agile culture mindset to stay in front of customer needs and expectations.