Telcos must co-innovate with partners to create new data-driven revenue streams. The global telecommunications sector is struggling to define its next chapter in terms of where new revenue streams will come from to replace declining core communications revenues. It’s an ironic problem, as this sector is powering certain facets of digital transformation but has had trouble picking the best opportunities to monetize, beyond provision of underlying connectivity. As telecommunications firms actively work to shape their future, they are working closely with IT and business process service providers around many emerging areas of technology, such as intelligent automation and the Internet of Things (IoT). However, much of the focus has been on cost optimization efforts rather than anything tied to revenue generation. HfS believes that this is a missed opportunity on both sides of the relationship. This Point of View has a look at major telecommunications industry and global services market trends, with an eye towards encouraging co-innovation. Please refer to Exhibit 1.

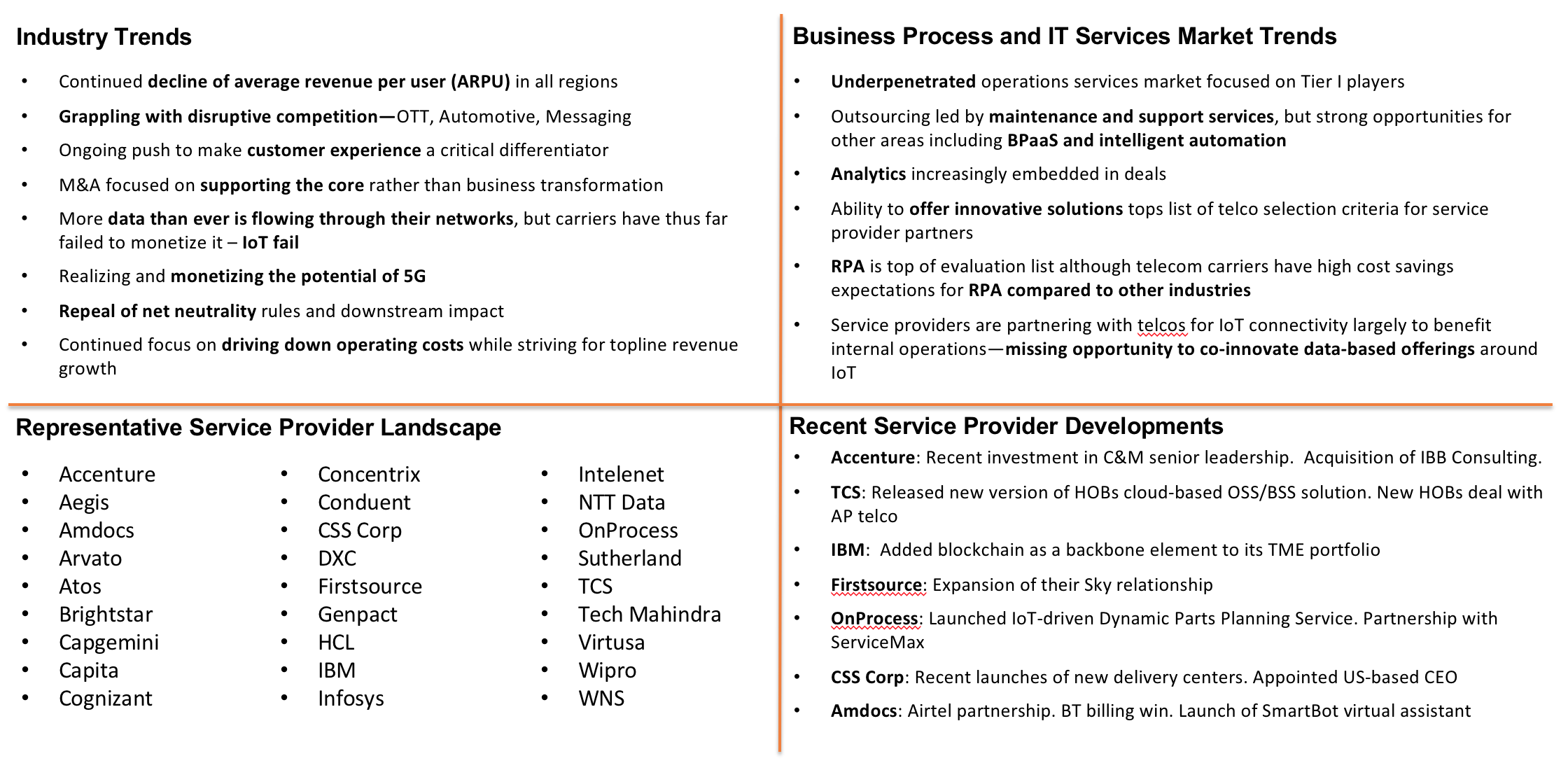

Exhibit 1: The Telecommunications Industry Dashboard

Source: HfS Research 2018

Digital disruption is eroding core carrier revenues

The collection of trends impacting the telecommunications sector is broad as outlined in Exhibit 1, but the pattern is simple – disruption and innovation are eroding core carrier revenues and new opportunities must be created and optimized to succeed. As always seems to be the case for this sector, there is no lack of options or opportunity. It’s the optimization element that is difficult. Telecommunication firms are often the first to get behind new technologies and innovations, such as connected car or IoT – or going back a bit, smart phones – but have trouble getting out of their sweet spot of communications and connectivity to offer anything marginally new or different. In other cases, such as Verizon or AT&T acquiring media firms, there is a clear push to transform the core business, but limited results so far. Telecommunication firms are trying to emanate successful technology firms such as Alphabet and Amazon through logical diversification, but without the fail fast or 10X impact approaches. The result is diversification without dominance, and thus continued anemic performance.

Key findings:

Here are some additional details and examples of the prevailing industry trends for telecommunications.

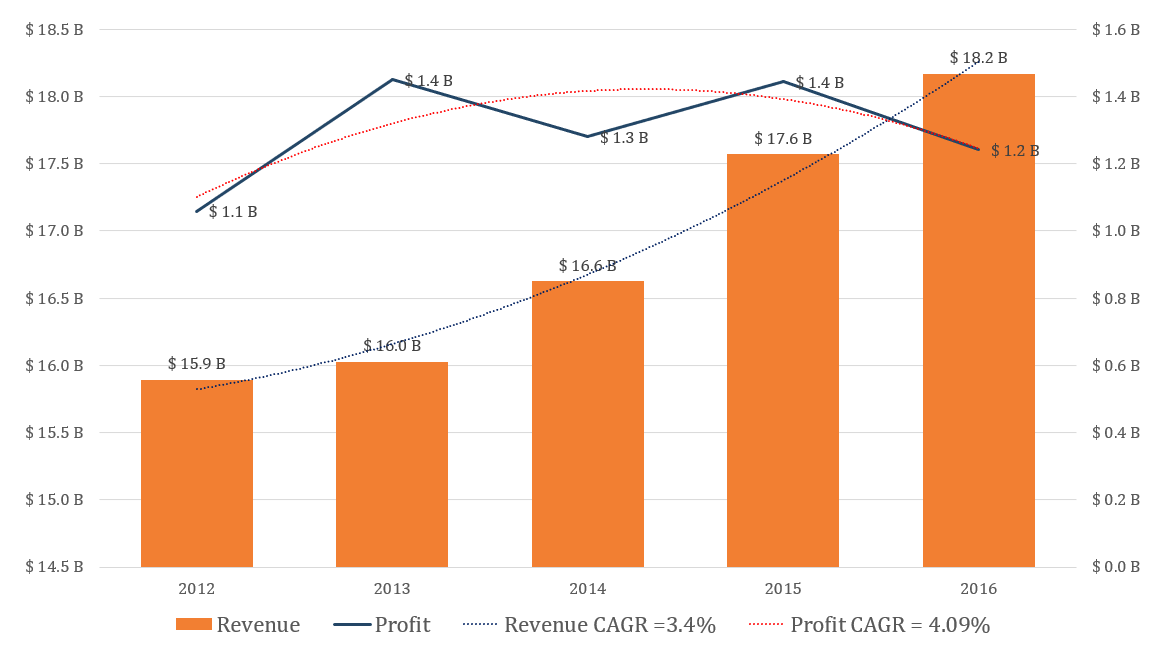

- Revenue and profit roller coaster – HfS revenue analysis of the top 100 telecom players shows a roller coaster of modest growth and decline over the past 5 years. ARPU continues to decline in all regions as core communications revenue decline. The core services of communications and connectivity have become utilities with little to no differentiation. Telecommunication firms need new, focused revenue streams. Please refer to Exhibit 2.

Exhibit 2: Telecommunications – Average Revenue and Profit 2012- 2016

Source: HfS Research 2018

- Disruptive competition – Over the Top (OTT) providers such as Netflix, messaging apps such as WhatsApp, and even the automotive industry, are all eroding the revenue and opportunity of telecom providers – and leveraging telco networks to do it. IBM recently inked a deal with BMW that will enable BMW customers to share telematics data from their vehicles with third-parties of their choice, such as insurance companies or repair shops, to create new user experiences. Telco connectivity enables the data-sharing but stops there. These data-driven new services are exactly the type of opportunities telcos need to cultivate.

- Customer experience as a differentiator – With declining ARPU and disruptors co-opting current and potential revenue streams, telcos are looking for new ways to differentiate. Customer experience has emerged as a contender for differentiation, as companies pay more attention to changing consumer expectations and trying to lever emerging technology to deliver personalized and increasingly proactive customer service. While many consumers prefer intuitive self-service apps, there is a growing question about whether telco investment in self-service and intelligent automation are truly intended to boost customer experience or to lower costs through less expensive channels. It’s a boon for telecommunication firms if they can achieve both, but we’ve observed that the focus is on shiny front-office user interfaces, with limited back office integration. The lack of movement to the Digital OneOffice perpetuates customer frustration through lack of a true 360 degree, omni-channel view of customers. That stated, examples from sectors such as travel, have proven that customer experience can foster loyalty. If telcos can understand their customers across channels and leverage their vast data stores to deliver useful and proactive value, customer experience can become a differentiator. But not for long.

- M&A focused on supporting the core – M&A is always interesting to track; it can provide a very clear picture of companies’ growth strategies. As we examine the past couple of years of telecommunications M&A, we see that the prevailing theme has been shoring up and expanding their core businesses, rather than business transformation (although there are exceptions, such as AT&T with Time Warner, Verizon with Yahoo). Examples include:

- CenturyLink’s acquisition of Level 3, enabling network services portfolio expansion.

- Verizon’s pick up of Straight Path, enabling 5G network development. XO brings fiber network expansion in 45 cities, and its acquisition of Yahoo will work with its prior AOL acquisition to round out a media and advertising push.

- Windstream and Earthlink merger expanded national fiber footprint and enables costs savings.

- T-Mobile (Deutsche Telekom) works on regional plays with acquisitions of UPC Austria, a leading cable provider, and Tele2 Netherlands.

- The merger of Vodafone India and Idea created the largest telecoms operator in India.

- AT&T and Time Warner – although held up by anti-trust concerns, if it proceeds, it would be massively transformative to AT&T, propelling them firmly into the media and entertainment space.

- So much potential with data, so many missed opportunities to do more – While telecommunications firms have had a strong focus on leveraging data and investing in analytics to help to optimize their business operations, there has been limited focus on creating or developing services that leverage the data. IoT is a prime example. Telcos are providing the connectivity but could be developing services such as automotive telematics, enabling location-based services and advanced safety features. #IoTfail

- Realizing and monetizing the potential of 5G – 5G is in many ways the ultimate enabler of ubiquitous data-based services. The telcos are doing their part in bringing these networks to life, thus actively ensuring a role in future ecosystems. However, what the role becomes is the pivotal question. Commoditized utility or purveyor of value-added analytics-led services?

- Repeal of net neutrality – With the repeal, US consumers and businesses are worried about blocking, throttling, and steep fees for prioritization of content. Given the struggles of telecommunication firms to secure new revenue streams, potential scenarios include bundling based on content types (a la the Portuguese telecommunications firm MEO), or simply higher premiums for preferred access. As telecommunications and media sectors become more intertwined, the prioritization of content will continue to be a thorny issue.

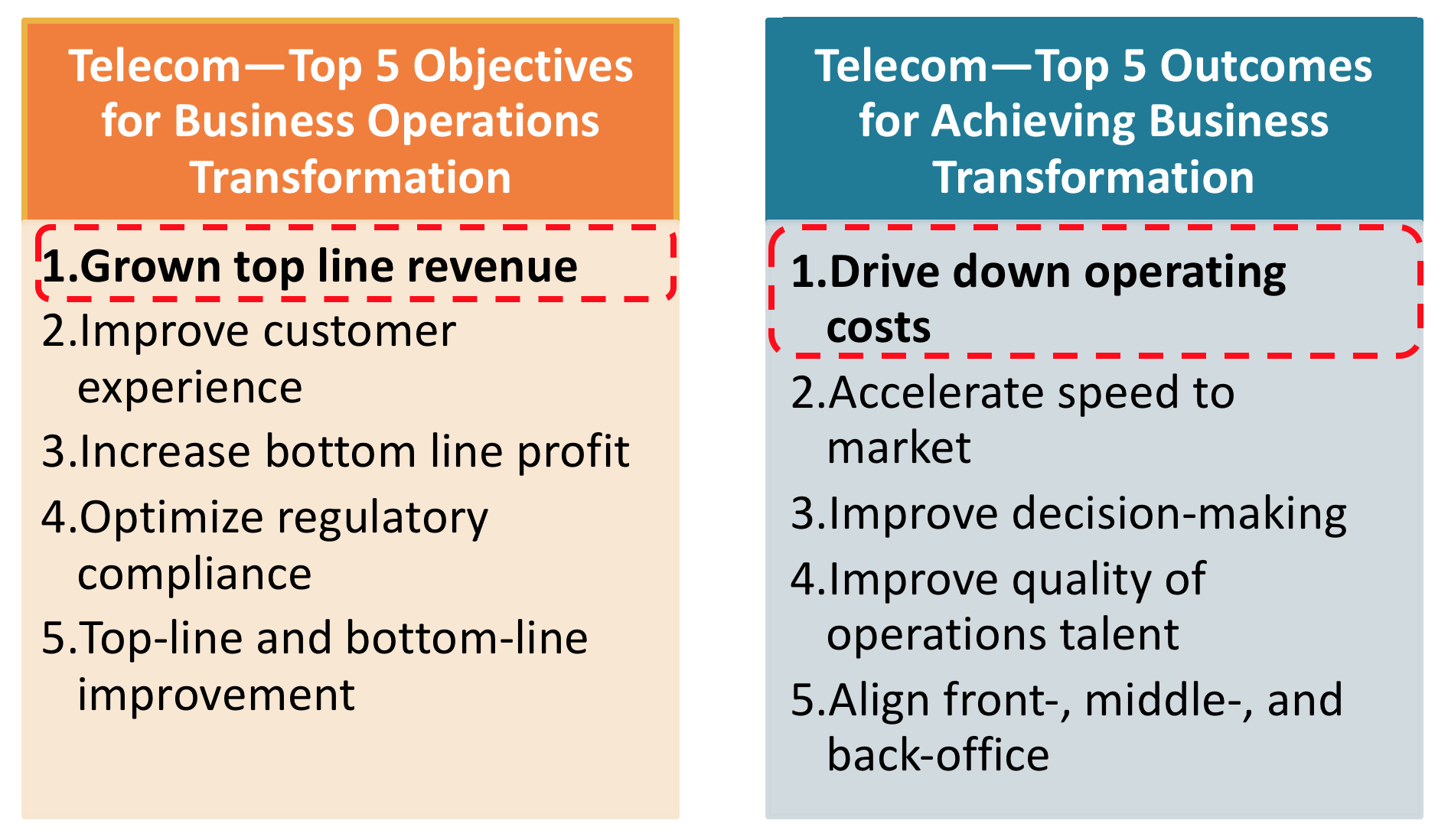

- Striving for topline revenue growth while focused on cost savings – A recent HfS study illustrates an ongoing challenge for the telecommunications sector (really all sectors in transition) – the top reason for engaging in digital transformation is to achieve better topline revenue, but the most critical outcome to achieve this is reducing operating costs, as depicted in Exhibit 3. While cost take -out as a funding strategy for innovation can work, it is a short-term strategy. And far too often, the savings just flow to the bottom line and are not reinvested in areas that can stimulate growth.

Exhbit 3: The Telecommunications Topline Revenue Generation Through Cost Savings Catch-22

Source: HfS Research 2018

The singular focus of telecommunications business process and IT services on cost-savings is a missed opportunity

As telecommunications firms actively work to shape their future, they are working closely with IT and business process service providers around many emerging areas of technology such as intelligent automation and internet of things. However much of the focus has been on cost-optimization efforts, rather than anything tied to revenue generation. HfS believes that this is a missed opportunity on both sides of the relationship. The following points provide some analysis on the current trends in the provision of IT and business process services to telecommunications firms.

- Service opportunities exist beyond Tier I telco players – Tier one telcos tend to dominate the market for operations services such as maintenance and support, fulfillment, billing and network support services. HfS research suggests that there is a strong potential opportunity for regional players to help them optimize their operations and transition to digital platform-based models. Regional and value-chain telcos can also benefit from service partnerships, particularly for digital operations and the co-innovation of new service offerings.

- Outsourcing is currently led by maintenance and support services, but there is so much more – Services under this umbrella, such as technical support and field service management, account for the lion’s share of outsourcing for telecommunications firms today. But strong opportunities exist for other areas, including BPaaS and intelligent automation, that are much more closely tied to helping firms digitally reinvent their businesses. Even within maintenance and support services, strong opportunities for service enhancement exist, such as leveraging artificial intelligence and machine learning to support technical support, and IoT-enabled analytics to optimize field

service management.

- Embed analytics in deals – Providers of IT and business process services are becoming increasingly savvy at brokering a broad array of capabilities beyond labor arbitrage and human capital. Analytics is a logical complement and value-add to many services such as network optimization, fall-out management, service failure prediction and prevention, and technical support. Increasingly, HfS is seeing analytics elements, in various forms, embedded into outsourcing engagements.

- Telcos want to leverage partners for emerging technologies – As telecommunication firms consider their future, they are increasingly looking to their service partners to step up their game, so that they can help them transform and transition to digital businesses. Offering knowledge, talent and experience in change agents, such as smart analytics, intelligent automation, internet of things, blockchain and cloud-based solutions, is essential to meeting telcos’ changing needs. Thus, it’s not surprising that innovation tops their list of criteria for selecting service partners.

- The top area of intelligent automation currently under consideration for telecom firms is RPA –

A recent HfS report found that RPA is at the top of the evaluation list. However, telcos need to be careful not to view RPA as a cost-saving panacea, as the same study found that telcos have high cost-reduction expectations for RPA, compared to other industries.

- Opportunities for IoT go well beyond optimizing internal telco operations – As consumers for IoT, along with industrial use cases, start to multiply, the play in telecommunications seems strongly focused on optimizing business operations, such as connected parts and inventory management, tower monitoring with drones, and set-top box validation and testing. While this innovation is applause-worthy, there is likely a missed opportunity to focus IoT efforts on creating new data and analytics-driven services that leverage IoT data and could contribute to the topline growth that telcos are so hungry for. Interesting co-innovation partnerships continue to be established, such as Cubic Telecom (an IoT software provider) with Microsoft, and Qualcomm focused on software and cloud services that connect cars to any network globally. At the recent 2018 Mobile World Congress, Cubic announced that is has achieved the milestone of enabling one million connected cars in the past 15 months. It is this type of creative partnering that could benefit the telecommunications sector. And IT and business process services firms are equally ready for some ground-breaking collaboration.

Representative service provider landscape and recent developments in the telecommunications industry

Exhibit 1 provides a representative sample of IT and business process service providers that support the telecommunications sector today. The list is not exhaustive, and it is not a ranking. It represents an ecosystem of players supporting the telecommunications sector with industry-specific solutions. HfS will release an Industry Blueprint focused on telecommunications in Q2 2018 which will include an updated service provider ranking grid.

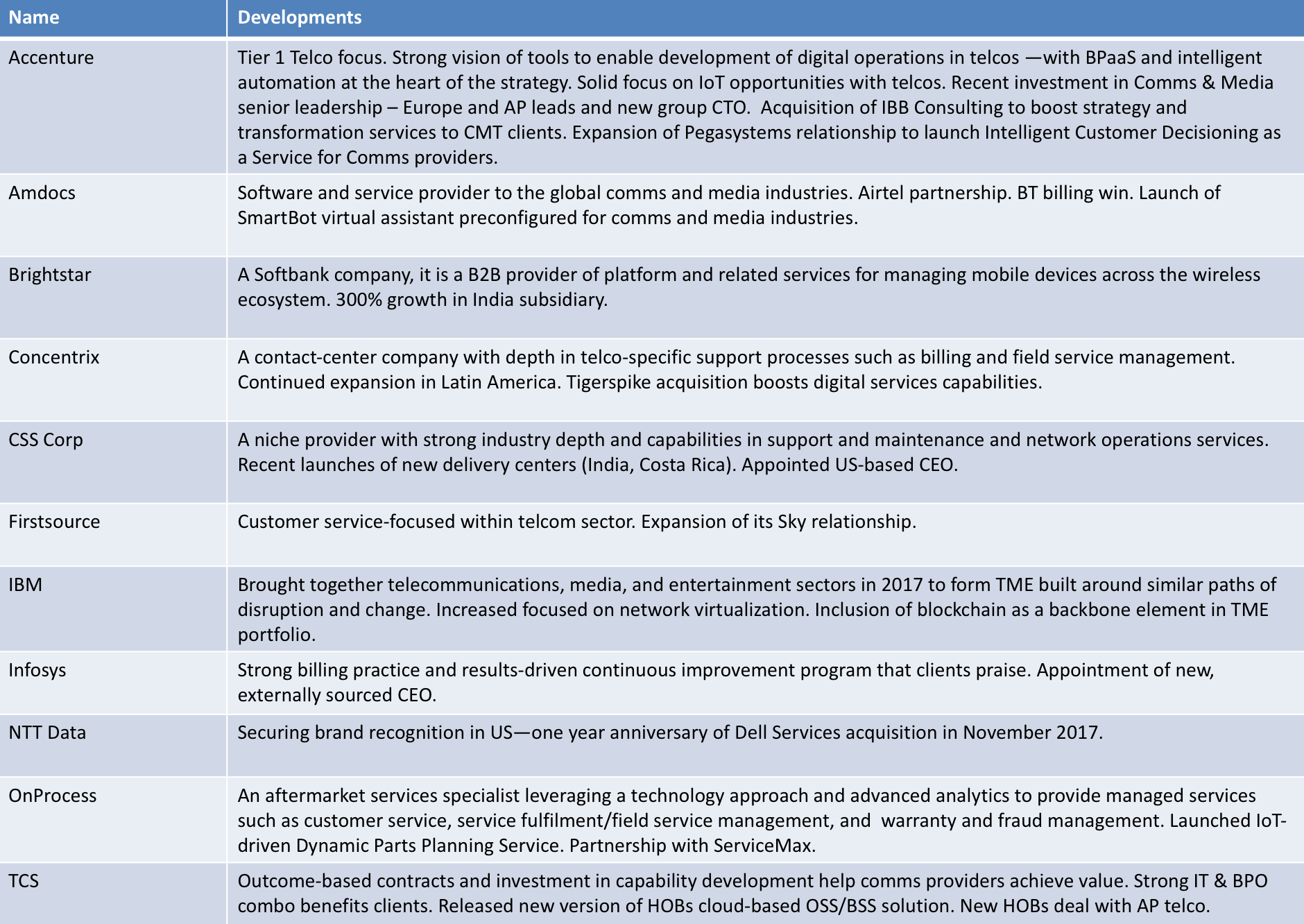

As these providers go through their own evolution in focus, from labor arbitrage to technology and platform-based businesses driving digital transformation, the critical ability is that of updating their portfolios to ensure that they are as relevant as possible to the needs of their clients. In the last year, some of the identified service providers have publicly announced investments, new wins or other advancements, to support their offerings in the telecommunications sector. Exhibit 4 presents a range of these recent developments.

Exhibit 4 – Service Provider Developments in Support of the Telecommunications Sector

Source: HfS Research 2018

Bottom Line: A call to telcos and service providers for them to co-innovate

As we review the dashboard of trends impacting the telecommunications industry, it is clear that focused change is needed, to help this sector chart a profitable future beyond its eroding communications and connectivity base. Service providers, who are also grappling with a similar need for redefinition and transformation, are supporting the telecommunications industry largely with cost optimization and business operations transformation. Telcos and service providers should work together to help enable new data-driven revenue streams.

Telecommunication firms and IT and business process service providers are both at the cross-roads where their core businesses are being substantially eroded. However, each has great future potential with the change agents of digital transformation. The potential for reinvention is strong, so long as each sector adequately focuses and optimizes its opportunities. This optimization may well come in the form of enhanced collaboration, whereby the communications and connectivity strength of the telecommunications sector is melded with the analytics, industry, and fundamental value-added services expertise of the IT and business process services sector. Together, these sectors could co-innovate some of the services of the future, to be built on 5G and leveraging technology change agents.