According to the HfS banking and financial services (BFS) industry Health Rating, BFS enterprises worldwide continue to struggle with revenue and profit growth. Digital transformation has emerged as the panacea to modernize your business processes in order to maximize revenues through digital customer channels.

However, like many firms, yours may be struggling to achieve exponential value from digital transformation strategies because of a fundamental mismatch between your overall objectives and your strategy execution. Establishing this consistency between transformation objectives and desired business outcomes is a critical step in ensuring the success of your digital transformation initiatives. Once this consistency is achieved, it is largely a matter of speed and execution.

This Point of View presents new HfS data from our recent BFS Services Operations Blueprint report that showcases how BFS enterprises like yours are faring with the definition and execution of their digital transformation strategies. Spoiler alert – you are not going fast enough.

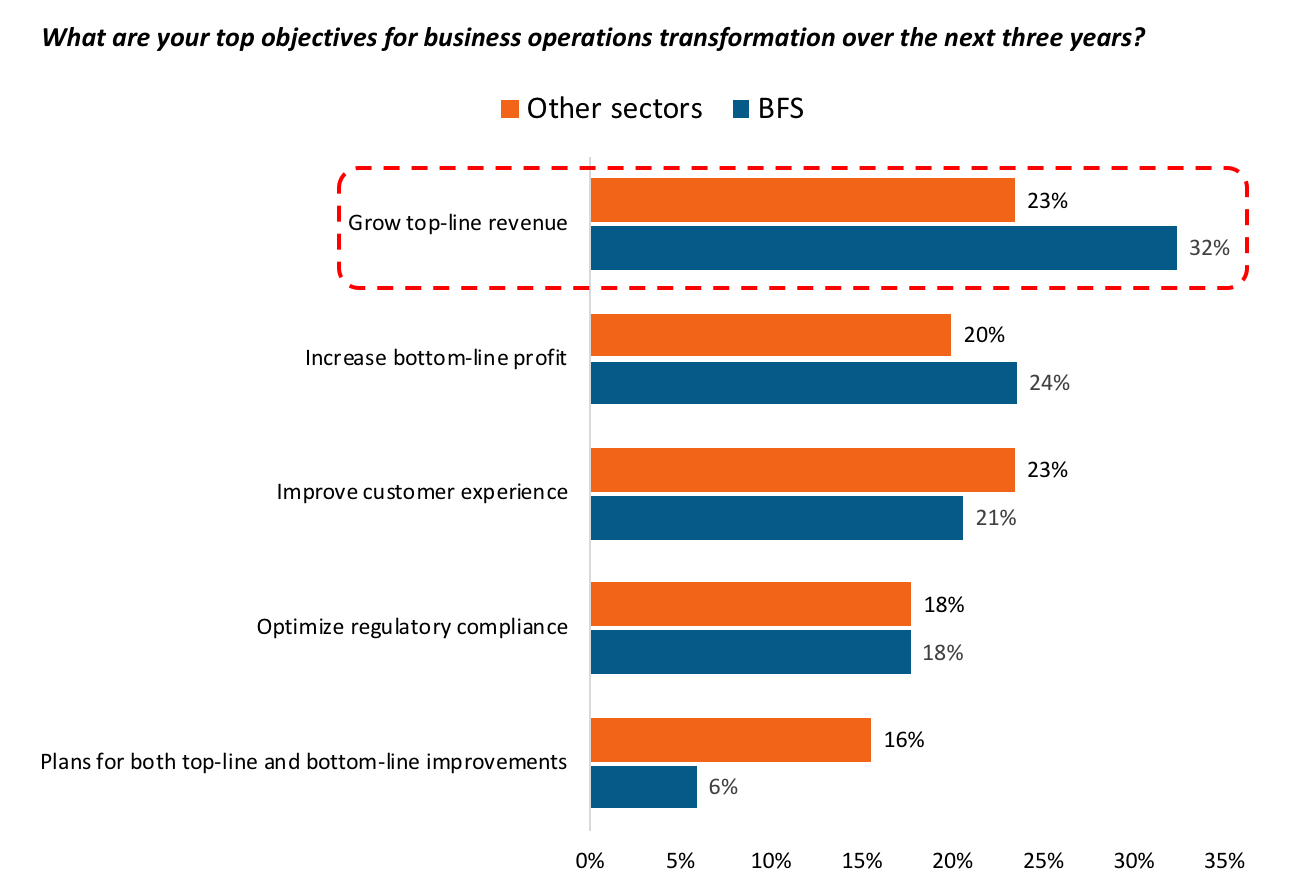

Why transform digitally? BFS enterprises cite revenue growth as their top objective

In a recent survey of IT and business operations leaders within global 2000 firms, HfS queried respondents on the top objectives for business operations transformation over the next three years. The results of the question ultimately pinpoint the big-picture reasons for why enterprises are pursuing digital transformation, as shown in Exhibit 1.

BFS respondents overwhelmingly identified growth of topline revenue as their leading transformation objective. Other sectors such as insurance, healthcare, and telecommunications, are torn between revenue growth and improving customer experience. Given the anemic Health Rating for the BFS sector, this clarity of vision is refreshing. As the BFS industry’s IT and business operations leaders, you need to complement this clarity of vision with succinct definition of what business outcomes will drive transformation and which levers will be utilized to achieve the growth. And you need to do so quickly, as revenue and profit performance continue to deteriorate.

Exhibit 1: Top objectives for digital transformation—Banking and Financial Services

Source: HfS Digital Transformation by Industry 2018; BFS n= 34; Other sectors n= 318; other sectors include manufacturing, energy, utilities, healthcare, pharma, retail and CPG, high-tech, insurance, telecom, and travel.

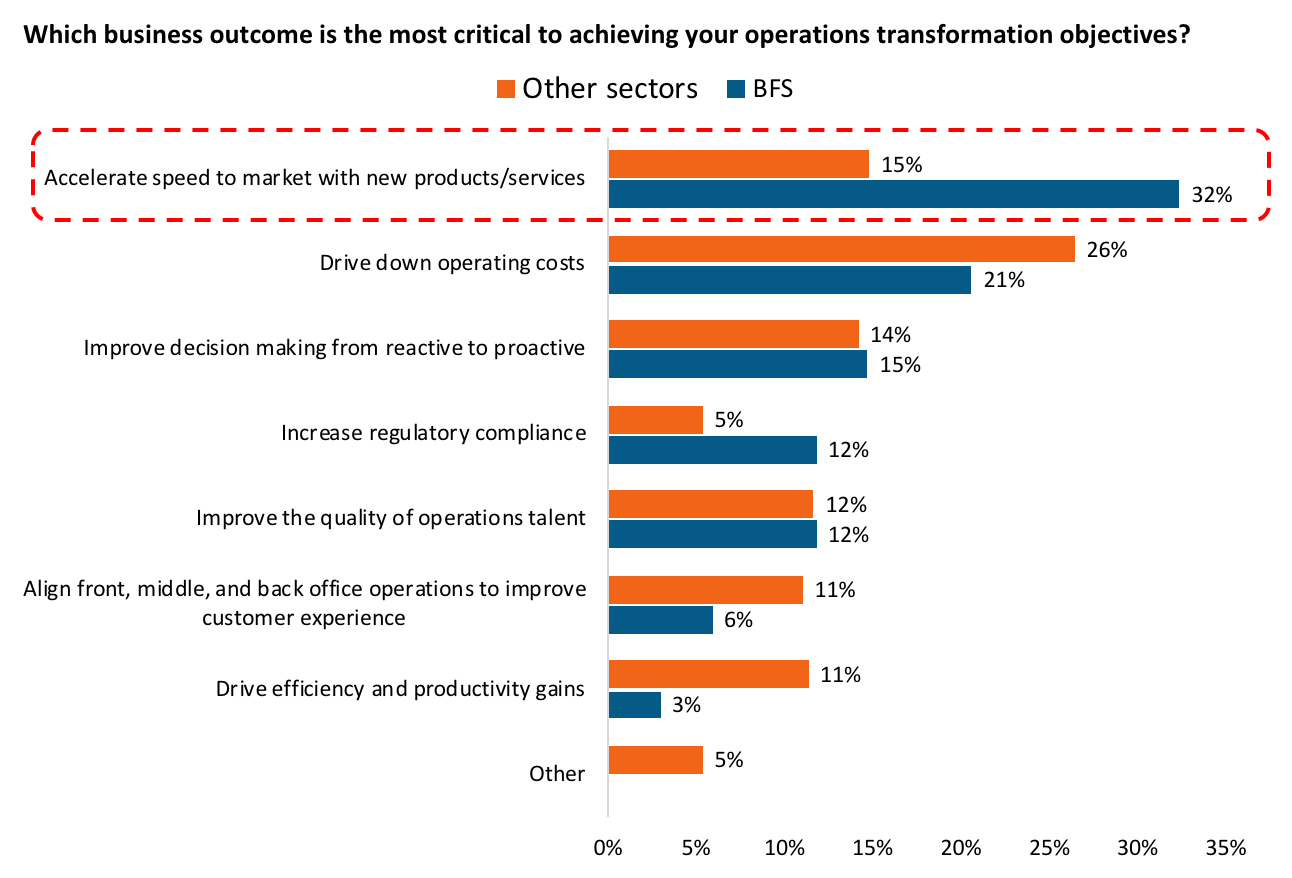

Getting new products and services to market more quickly is the critical business outcome of digital initiatives, BFS firms say

Numerous HfS studies have found a distinct mismatch between overall objectives and strategy execution. Though our data suggests that C-suite mandates for digital transformation are beginning to be operationalized in a more precise manner, with enhanced understanding of the outcomes necessary to fulfill the vision, the jury is still out as balance sheet performance is still forthcoming.

In contrast to BFS, all other sectors cited driving down operating costs as the critical outcome for achieving transformation objectives. Using this approach, these sectors will be hard pressed to achieve either improved customer experience or top-line revenue growth. While driving down operating costs can generate savings, the savings need to be reinvested in digital transformation initiatives to achieve any mid- to long-term value.

Exhibit 2: Top business outcomes needed to achieve digital transformation objectives—Banking and Financial Services

Source: HfS Digital Transformation by Industry 2018; BFS n= 34; Other sectors n= 318; other sectors include manufacturing, energy, utilities, healthcare, pharma, retail and CPG, high-tech, insurance, telecom, and travel.

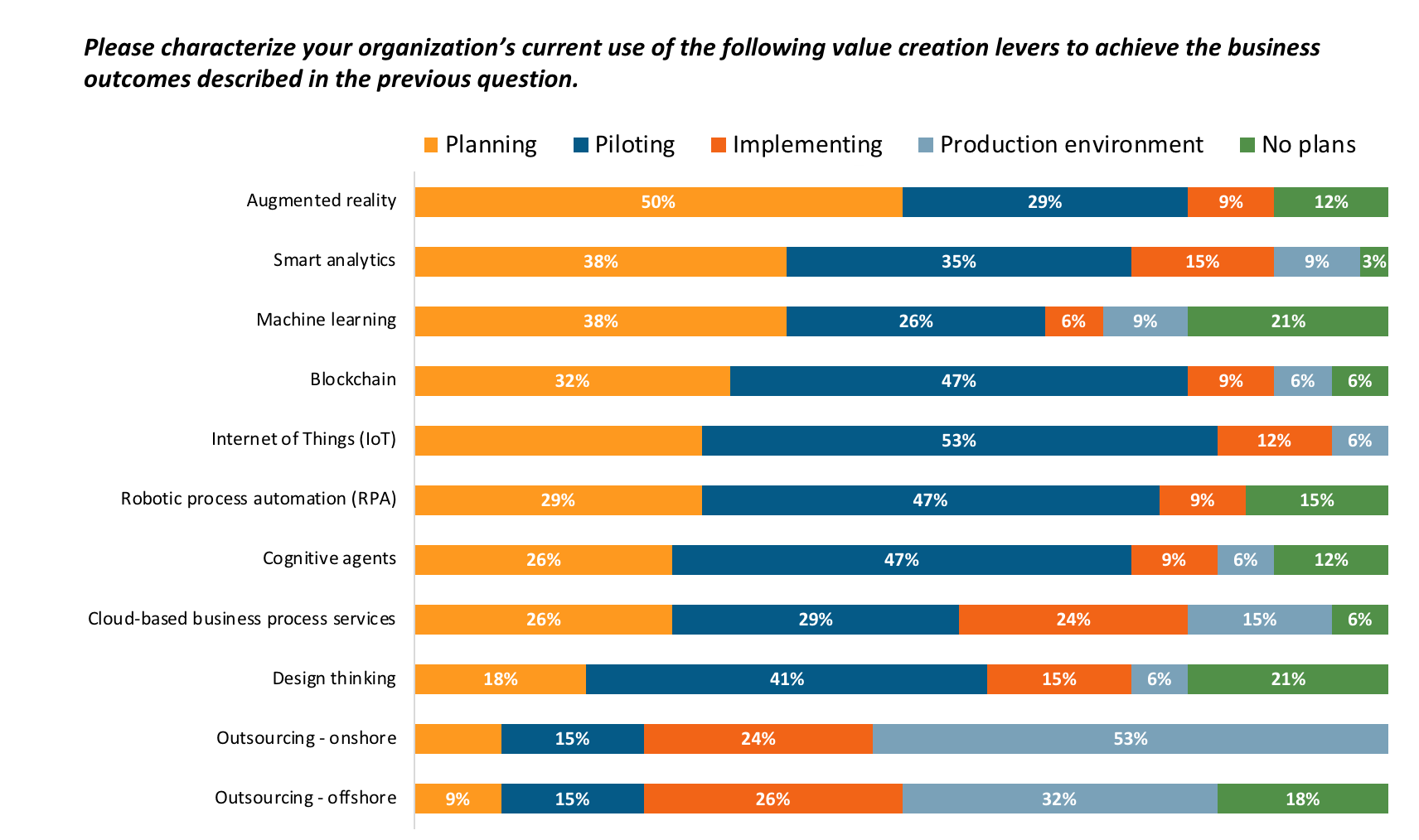

BFS enterprises are leveraging a range of critical change agents – albeit slowly – to achieve digital transformation

In the BFS space, you and your peers are focused on using the latest change agents, such as blockchain and robotic process automation (RPA), to drive digital transformation and achieve tangible business benefits. While the focus is there, the actual progress and results are not as far along as market hype might suggest. In reality, many of the change agents you are employing are still in the planning, pilot, or early-implementation stages. Our study’s findings are summarized below and in Exhibit 3:

Ultimately, you must guide your enterprise through its own unique process of planning, piloting, and implementation, to achieve its business objectives. The reality is that the BFS industry is in flux and, as such time is of the essence. All of your focus needs to be placed on executing the investments that will deliver maximum benefits in line with your overarching business objectives.

Exhibit 3: Use of change agents to drive digital transformation—Banking and Financial Services

Source: HfS Digital Transformation by Industry 2018; BFS n= 34

What do focus, speed and execution yield when it comes to digital?

For a European bank: topline results!

Customer satisfaction was at an all-time low, for one European bank, and its revenue and profitability were also down. In 2015, its leadership team defined and set course on a digital transformation journey. It was very clear what they needed to achieve because, literally, their future depended on it. Their mission was to redefine and remake customer experience across a targeted set of customer journeys. Through a mix of design thinking, use of DevOps disciplines, strategic use of outsourcing partners, BPM, artificial intelligence and RPA, as well as a very transparent and inclusive engagement process with customers, the bank has returned to sustained profitability and has vastly improved customer experience. The journey is by no means over – on the contrary, now the leaders have seen what’s possible, they are continuing to drive performance improvement through innovation. New blockchain and cognitive projects are currently cycling through proof-of-concept and proof-of-value.

The bottom line:

BFS IT and Business Ops leaders – you must align your firms’ objectives and execution, and proceed with a sense of urgency

Why are you digitally transforming? What are you going to achieve? How are you going to do it? The answers to these questions must always be clearly communicated to every level of the organization. BFS firms, suffering from anemic growth and profit performance, are developing strong clarity around their core objective for digital transformation – driving top-line revenue. As this vision becomes clear, there is no time to waste: put it into action, now!

BFS executives – if you are, or want to be, on the fast track to digital transformation, HfS recommends the following:

Register now for immediate access of HFS' research, data and forward looking trends.

Get Started

If you don't have an account, Register here |

With the exception of our Horizons reports, most of our research is available for free on our website. Sign up for a free account and start realizing the power of insights now.

Our premium subscription gives enterprise clients access to our complete library of proprietary research, direct access to our industry analysts, and other benefits.

Contact us at [email protected] for more information on premium access.