This HFS Point of View is for RCPG sourcing, procurement, and commercial leaders renegotiating how services are priced as AI erodes effort-based contracts.

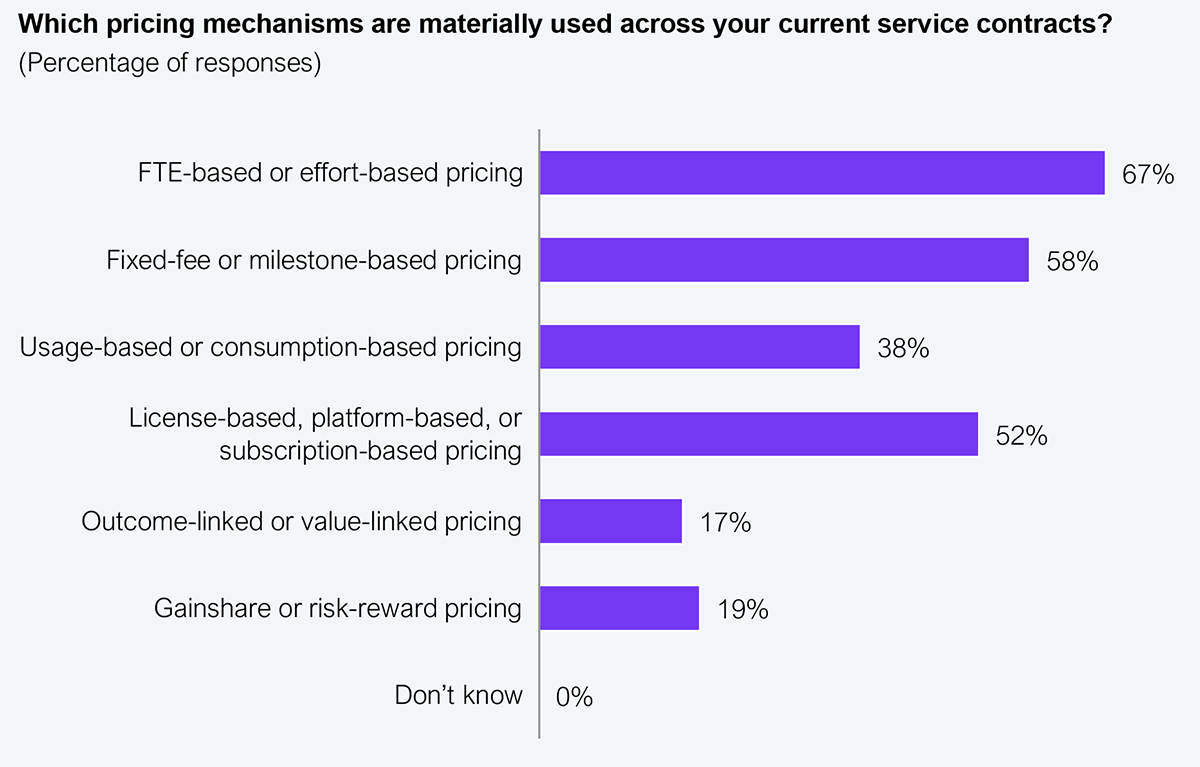

RCPG leaders are signaling a decisive shift in how they want services priced, governed, and evaluated. Directional findings from an initial cohort of 20 RCPG enterprise leaders show an industry mid-pivot; today, 67% of contracts still materially use FTE or effort-based pricing, with fixed-fee close behind at 58%. AI is taking over the manual work that effort-based contracts bill by the hour, yet providers keep the resulting productivity gains in their margins instead of passing them to the buyer’s P&L. The longer leaders price by headcount, the more value they allow providers to capture. RCPG leaders must retire effort-based pricing now and rebuild commercial terms around elasticity, shared risk, and measurable value before AI exposes how little control headcount ever bought.

Sample: HFS Pulse 2026, n=20 RCPG enterprise leaders

Source: HFS Research, 2026

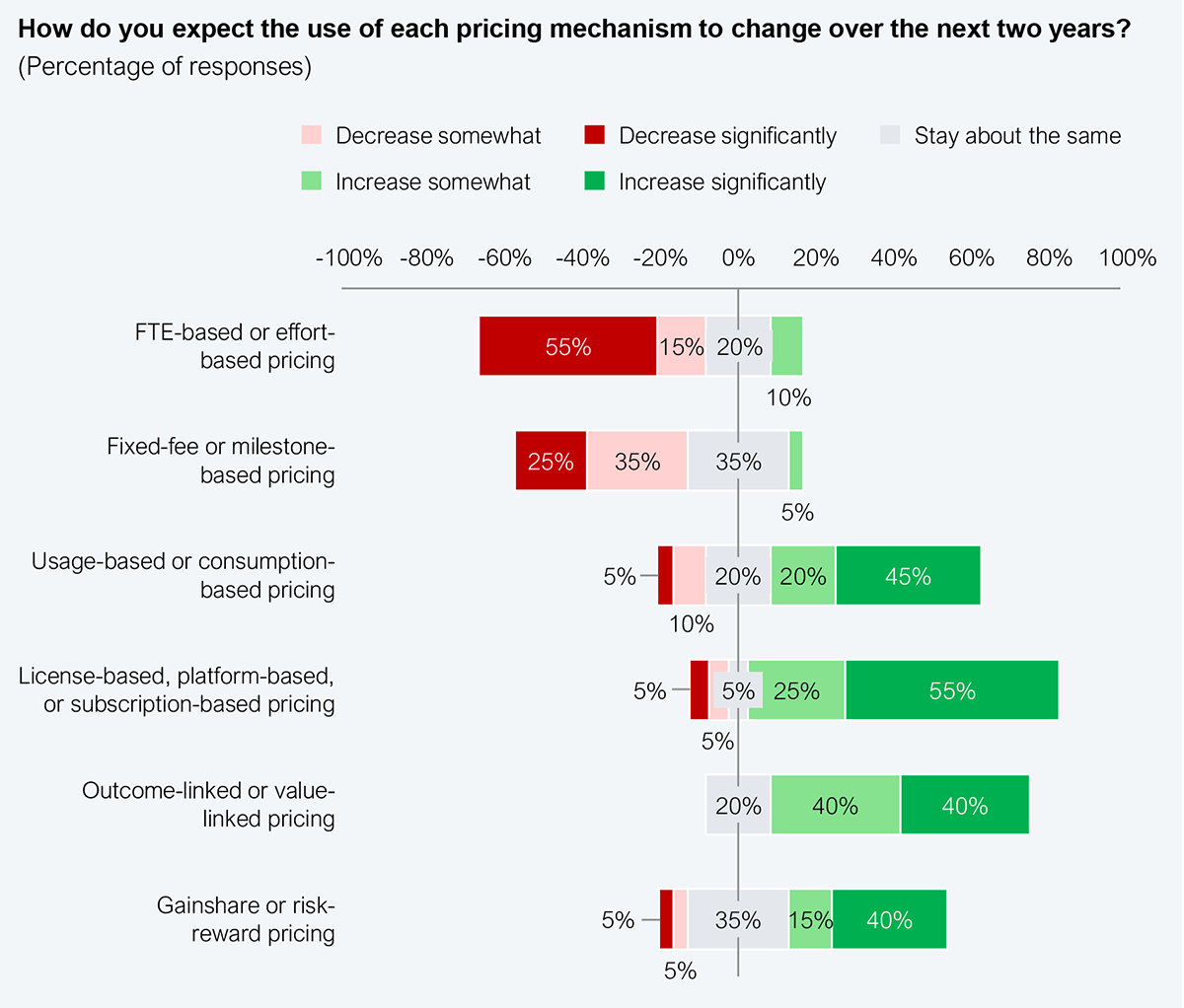

The future signal, however, is moving sharply in the other direction (Exhibit 2). Seventy percent (70%) of RCPG leaders expect FTE pricing to decline over the next two years, with more than half forecasting a significant decrease. The sector is not simply adjusting commercial terms; it is moving away from pricing by headcount. What comes next will not be one replacement model, but a staged move toward elasticity, risk-sharing, and measurable impact.

Sample: HFS Pulse 2026, n=20 RCPG enterprise leaders

Source: HFS Research, 2026

FTE-based pricing has endured because it reduces ambiguity. In complex RCPG environments spanning brands, markets, channels, retailers, and digital platforms, counting people has been the easiest way to control cost and assign responsibility. But effort is only a proxy for work, not proof of value, and AI is now exposing the gap between the two. As automation, analytics, and platforms reduce manual activity, pricing services by labor input becomes harder to defend.

As generative and agentic AI absorb the manual, repeatable, judgment-light activity that RCPG services have historically billed by the hour, the link between effort and output collapses, even as the headcount on the contract does not. The result is that buyers keep paying for hours providers no longer need to deliver the work, and the productivity dividend AI creates accrues to the provider’s margin rather than the buyer’s P&L. Under FTE pricing, the better the provider’s AI, the less of the gain the buyer ever sees.

Consumption pricing flexes where FTE pricing cannot

The “control” the model promises becomes control over an input that has been hollowed out, a headcount that no longer maps to the work being done. This hollowing out of control is why the rise of elastic pricing matters. Usage- and consumption-based pricing is expected to increase by 65% of respondents, while license, platform, and subscription-based pricing is expected to increase by 80% of respondents. These align better with how RCPG actually operates and with demand shifts by season, category, retailer, promotion, channel, and geography.

Consumption pricing allows services to flex with transaction volumes, campaign intensity, digital shelf activity, customer contact demand, and analytics usage. Subscription and platform pricing create access to reusable capabilities that can scale across functions and markets. The new risk is no longer just overpaying for labor; instead, it is overpaying for underused platforms, unmanaged consumption, or capabilities that fail to change business behavior.

Outcome and value-linked pricing show the clearest aspiration gap. Only 17% of current contracts materially use it, yet around 80% of leaders expect it to grow. Outcome pricing is the model RCPG wants because it speaks the language of executive value, margin, growth, speed, working capital, resilience, and customer experience. But wanting outcome pricing is not the same as being ready for it. Outcomes are rarely produced by one party alone, and value attribution becomes difficult when results depend on provider performance, enterprise adoption, data quality, retailer behavior, and market conditions. Pure outcome pricing demands measurement infrastructure, governance maturity, and trust that most contracts cannot yet support. The 80% growth signal reads less as readiness and more as direction of travel.

Gainshare separates aspiration from intent

Gainshare becomes pivotal when ambition must translate into measurable and payable outcomes. It is currently used in only 19% of contracts, but 55% of respondents expect it to grow. Gainshare requires what outcome pricing only implies: defined value pools, joint accountability, auditable baselines, and a willingness on both sides to share upside and downside. The lower growth expectation is not lack of interest; it is the distance between leaders who want outcomes in principle and leaders ready to commit to the mechanics that make outcomes payable. Read together, the two numbers separate aspiration from intent.

The ability to make outcomes payable is why gainshare is the practical bridge. It is also where the AI dividend changes hands. The productivity gain that silently accrues to the provider under FTE pricing becomes, under gainshare, a value pool both sides can see, size, and split, which is why the model matters more as AI matures, not less. It preserves a service-fee floor while allowing upside participation, but only if the value pools are designed correctly, narrow enough to measure, material enough to matter, and attributable enough to defend.

The right value pools already exist

Trade promotion claims automation, deduction reduction, forecast accuracy, digital shelf compliance, contact deflection, finance close acceleration, and working-capital release are gainshare-grade value pools because performance can be observed, baselines can be audited, and provider contribution can be isolated from market noise. The strongest commercial conversations of the next two years will not be about whether to move to outcomes. They will be about which value pools are gainshare-ready now, and what infrastructure must be built to make the rest measurable.

RCPG services pricing is migrating from inputs to impact, but not in a straight line. Buyers should not accept outcome-based pricing as a slogan or an end-state promise. They must demand pricing constructs that clearly map the journey from labor certainty to elastic capability, from elastic capability to shared risk, and from shared risk to trusted business value.

At your next negotiation, ask the provider to name a gainshare-ready value pool, baseline it, agree how to measure it, and propose a split. If they cannot do that, the AI productivity dividend stays on their margin instead of yours.

Register now for immediate access of HFS' research, data and forward looking trends.

Get Started

If you don't have an account, Register here |

With the exception of our Horizons reports, most of our research is available for free on our website. Sign up for a free account and start realizing the power of insights now.

Our premium subscription gives enterprise clients access to our complete library of proprietary research, direct access to our industry analysts, and other benefits.

Contact us at [email protected] for more information on premium access.

If you are looking for help getting in touch with someone from HFS, please click the chat button to the bottom right of your screen to start a conversation with a member of our team.