This claims confidence gap Market Impact Report is for chief claims officers, CFOs, and procurement leaders at P&C insurers redesigning how they buy and govern third-party claims administration.

Property and casualty (P&C) third-party administrator (TPA) spend is increasing rapidly, yet most insurers openly describe the relationship they are leaning on as broken. This report is for the senior leaders who own or influence claims strategy and TPA selection including the chief claims officers (CCOs), CFOs, COOs, vendor-management heads, procurement leads, and program administrators. It shows them why the disconnect persists, what it is costing them in leakage, cycle time, and adjudication quality, and what to change about the procurement and governance of TPA services.

Scope of the study

HFS Research, in partnership with Xceedance, surveyed 302 senior P&C insurance leaders across the US, Canada, and Bermuda in April 2026. Fifty-five percent are primary decision makers on claims strategy and TPA selection, and 34% are key influencers. The sample spans admitted carriers, excess and surplus (E&S) carriers, managing general agents (MGAs), program administrators, self-insured enterprises, and insurtechs. Respondents range from firms with less than $250 million to those exceeding $10 billion in revenue and from lower than 5,000 to over 500,000 in claims volumes annually. The survey is supplemented with qualitative insights and sets out to test one hypothesis: the way insurers buy TPA services has fallen out of step with what they want from those services. The data validates the hypothesis.

Enterprise insurers are spending more on TPA services for a relationship they describe as broken. They want strategic partnerships, AI-driven outcomes, and outcome-aligned commercial structures. Instead, they’re buying processing-vendor relationships, traditional commercial models, and account management that lack deep claims expertise. That gap is the structural problem this report unpacks.

Demand is expanding under structural pressure

The P&C claims TPA market is at an unusual re-contracting point, and most insurers are already navigating it. For 62% percent of insurers, the decision to revisit the TPA relationship is already being made. At the same time, 58% expect to spend more in the same window, and only one in ten plan to stand still.

In a market historically anchored by long-duration relationships, that is an active redrawing of the map. The procurement decisions made in the next twelve months will shape claims operations in the next full renewal cycle, and the insurers redesigning their RFPs around outcomes today will hold an advantage over less-deliberate peers.

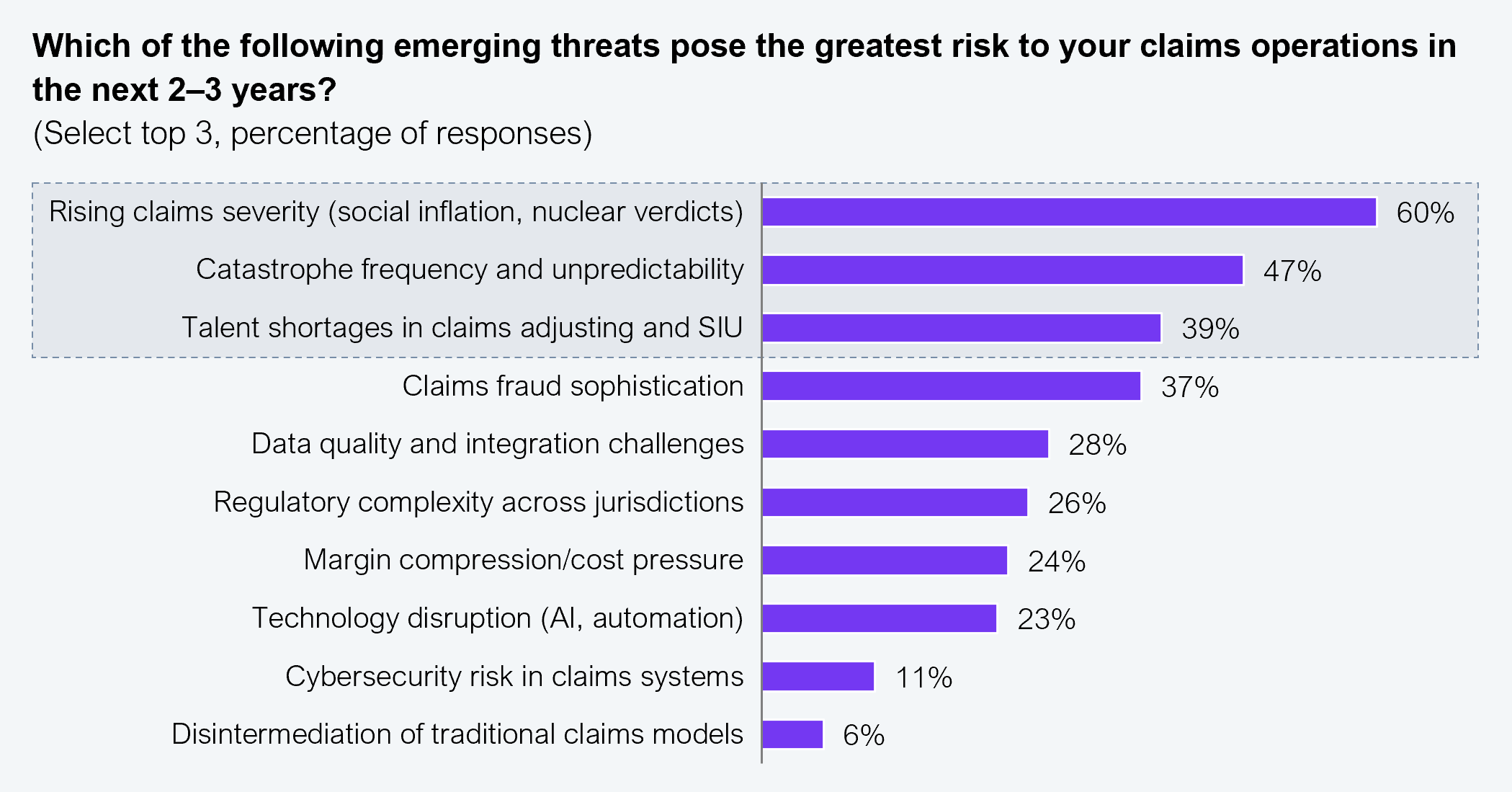

Three external pressures are driving this expansion, all of which lie beyond the control of any single insurer or TPA (see Exhibit 1). These include rising claims severity (60%; driven by social inflation and nuclear verdicts), catastrophe frequency and unpredictability (47%), and talent shortages in claims adjusting and the Special Investigative Unit (SIU; 39%). Talent shortage amplifies every other gap. Fewer experienced adjusters mean slower cycle times and weaker outcomes, and the damage is more pronounced during severity spikes and catastrophe (CAT) events.

Sample size: n=302

Source: HFS Research and Xceedance, 2026

Although the TPA relationship is viewed as transactional, insurers are placing their AI bets on them

Insurers want strategic partners but continue to buy transactional vendors, and they openly know it. Ninety-four percent say their TPA operates more like a processing vendor than a strategic partner, with three out of four strongly agreeing. Yet those same insurers rank AI and automation as the top selection criterion when choosing a TPA. They expect TPAs to play their part but make no effort to move from a transactional to a more strategic relationship.

The explanation sits in the procurement process itself. Insurers are selecting TPA services through a buying framework that doesn’t capture what they want from those services. The next section examines how that gap forms and where it leads.

I want TPAs to stop acting like they’re doing us a favor. We’re the client. When I call about a seven-figure claim, I expect somebody who actually knows the file to pick up.

— A self-insured enterprise ($1 billion–$4.9 billion in gross written premium [GWP])

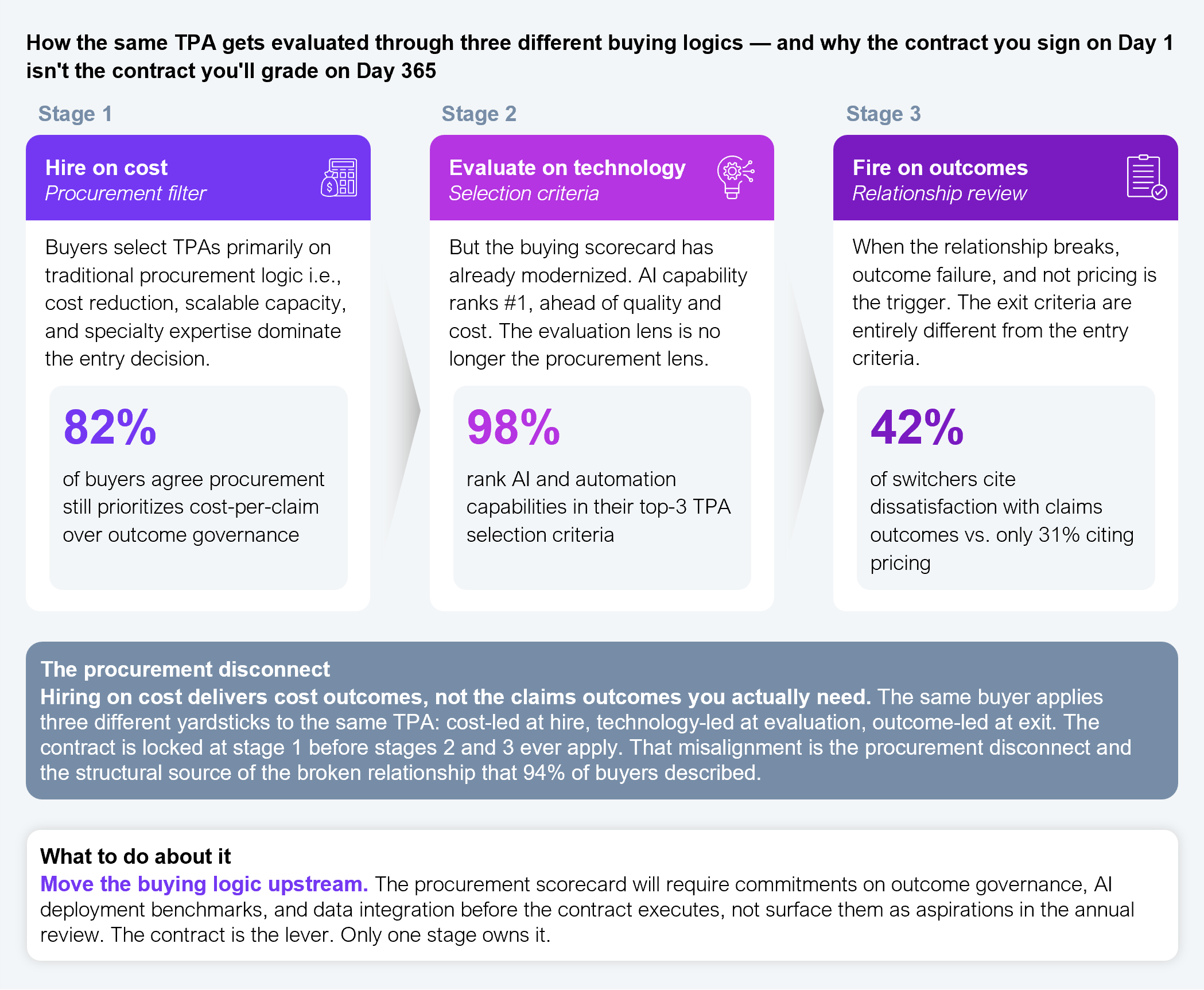

Enterprise insurance buyers operate on three different evaluation logics across the TPA lifecycle, and those logics don’t talk to each other. Each logic optimizes against a different metric, and no part of the buying organization is accountable for connecting these logics (see Exhibit 2).

Sample size: n=302

Source: HFS Research and Xceedance, 2026

Insurers hire on cost

Procurement still buys TPA services on cost, and the contract signed at that stage shapes every outcome the relationship can deliver afterward. The top two reasons insurers hire TPAs are scalable claims capacity (49%) and cost reduction versus in-house operations (40%). Procurement treats TPA services as a make-or-buy economics question, resolved by pricing per claim, FTE rates, and capacity hedging.

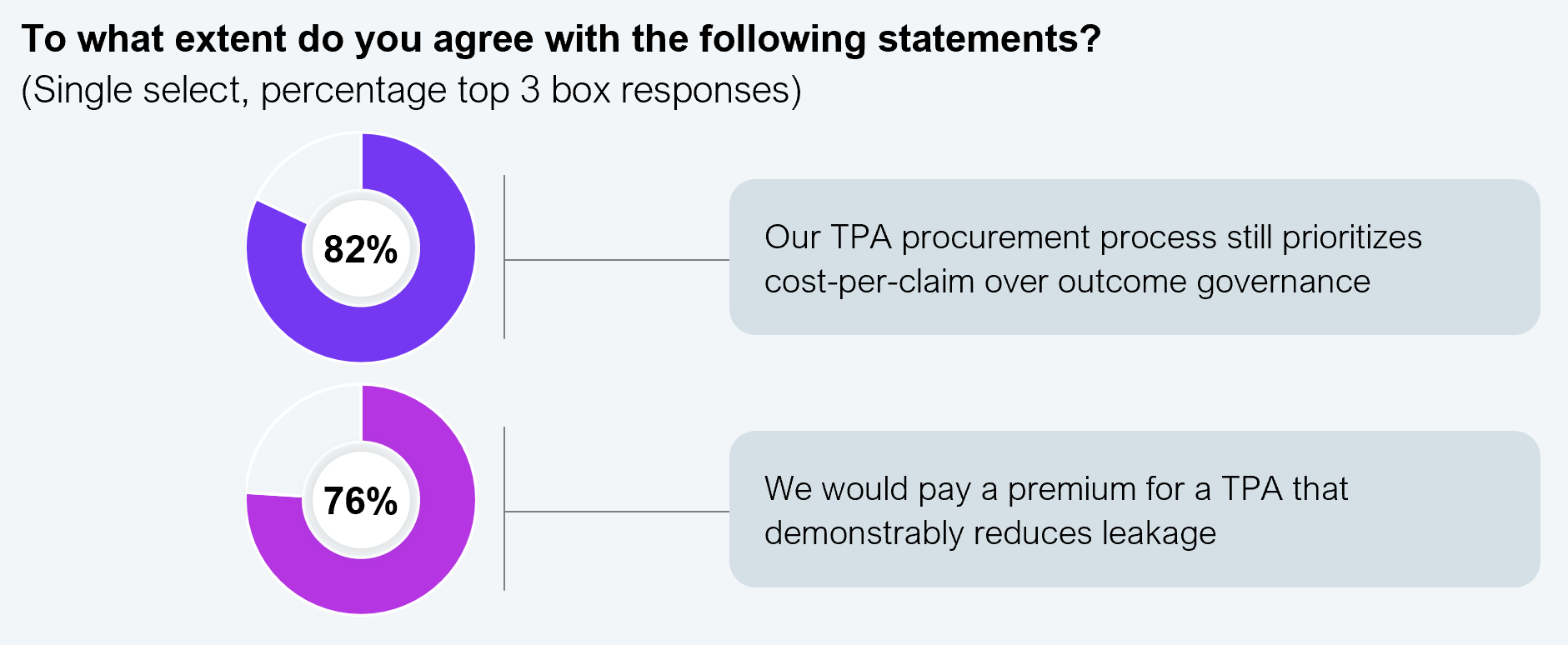

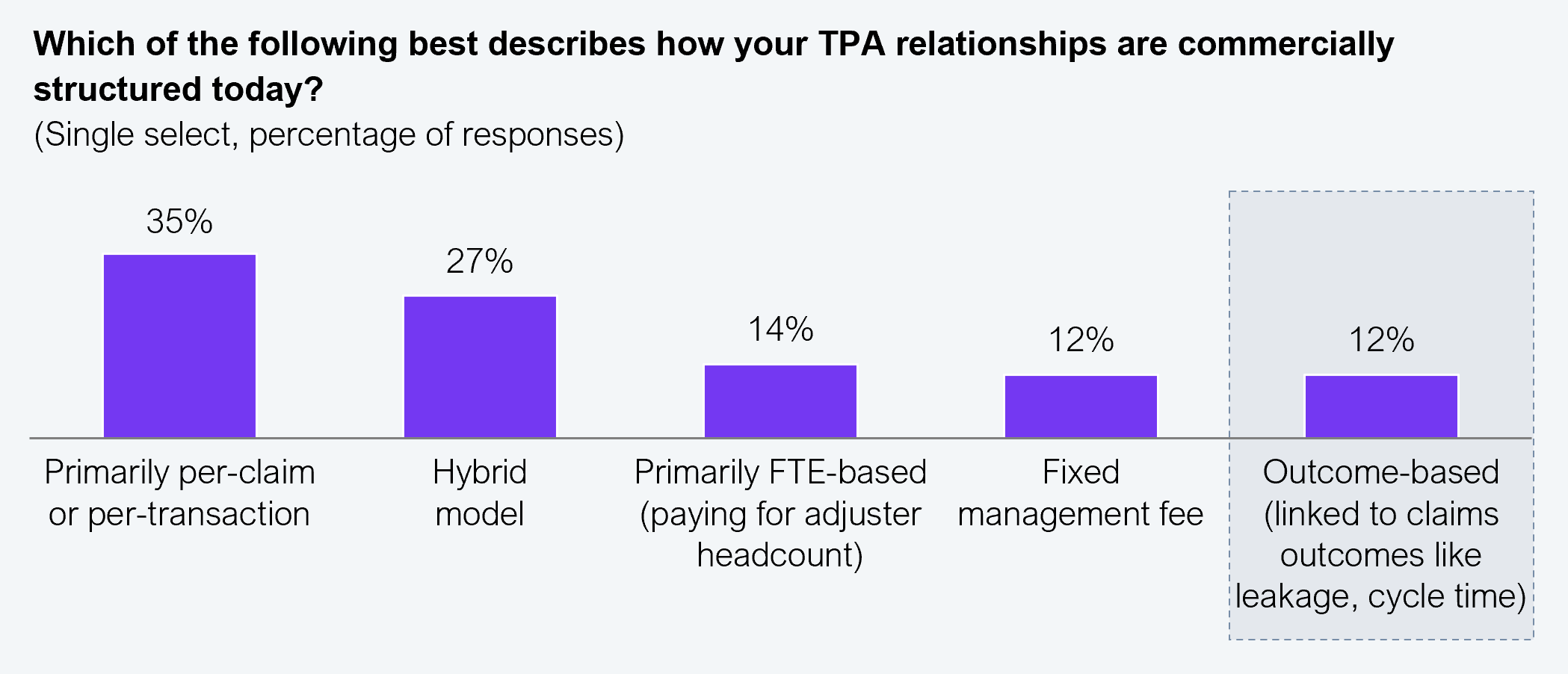

Eighty-two percent of insurers admit that their procurement process still prioritizes cost-per-claim over outcome governance (see Exhibit 3a). The contracting language reinforces it. Forty-nine percent of TPA relationships are structured on traditional pricing, including 35% on per-claim or per-transaction, 14% FTE-based. Another 12% are tied to fixed management fees. Hybrid models account for another 27%, whereas only 12% are structured around outcomes (see Exhibit 3b).

Eliminate the hidden fees. By the time you add up implementation charges, system access fees, per-user licensing costs, and report customization surcharges, the actual cost is 30%–40% higher than what they quoted.

— P&C carrier (admitted)

Sample size: n=302

Source: HFS Research and Xceedance, 2026

Sample size: n=302

Source: HFS Research and Xceedance, 2026

Insurers evaluate on technology

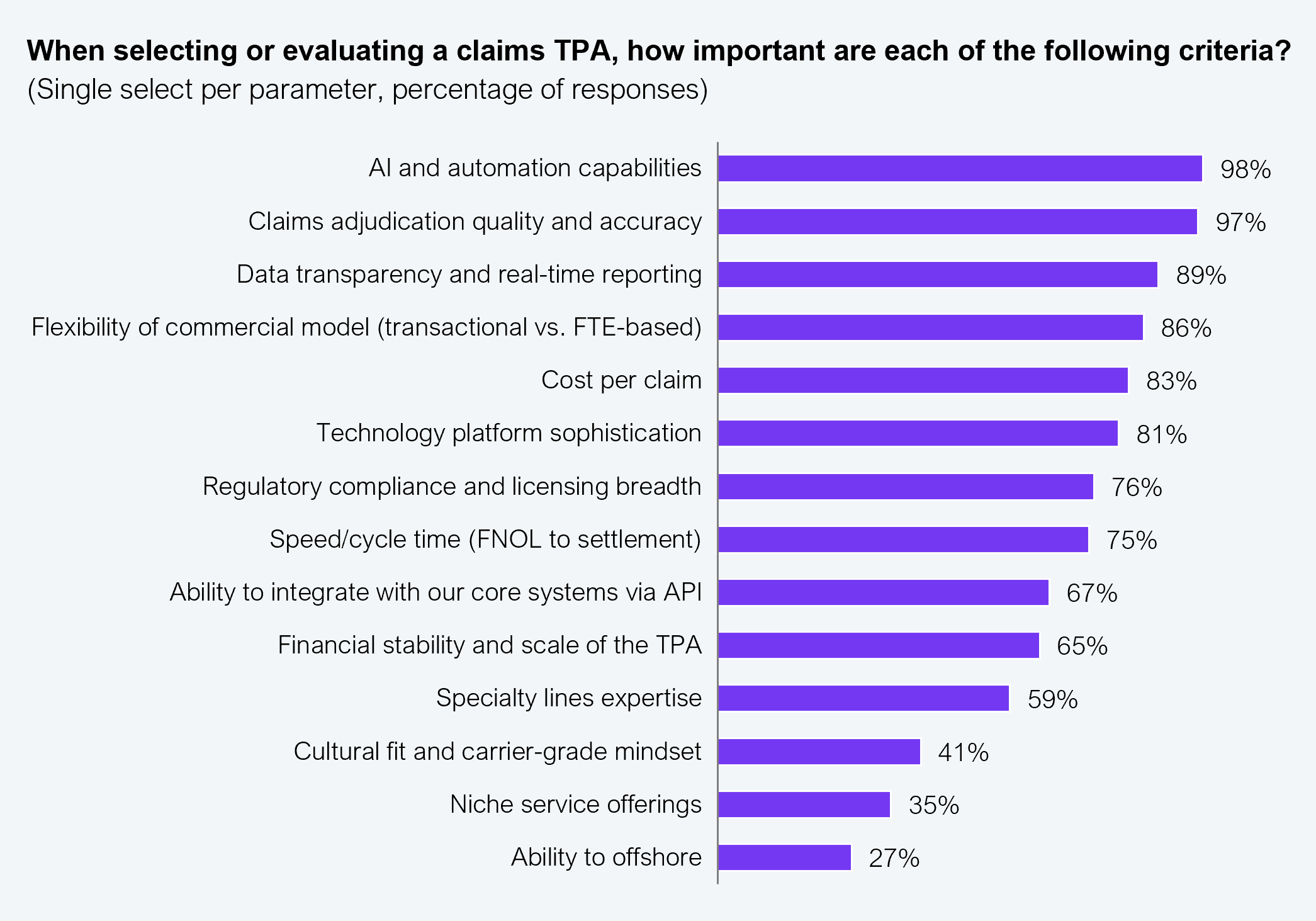

Once a procurement shortlist forms, the evaluation logic flips. When asked which capabilities most influence the final TPA selection, 98% rank AI and automation among their top three, ahead of claims adjudication quality, data transparency, and cost per claim (see Exhibit 4). Technology has displaced cost as the differentiator, but outcomes still don’t appear on the scorecard.

I keep hearing about AI and machine learning at every conference, but when I look at how our TPA is actually handling claims, they’re still using the same triage process from 2010.

— MGA and program administrator

Sample size: n=302

Source: HFS Research and Xceedance, 2026

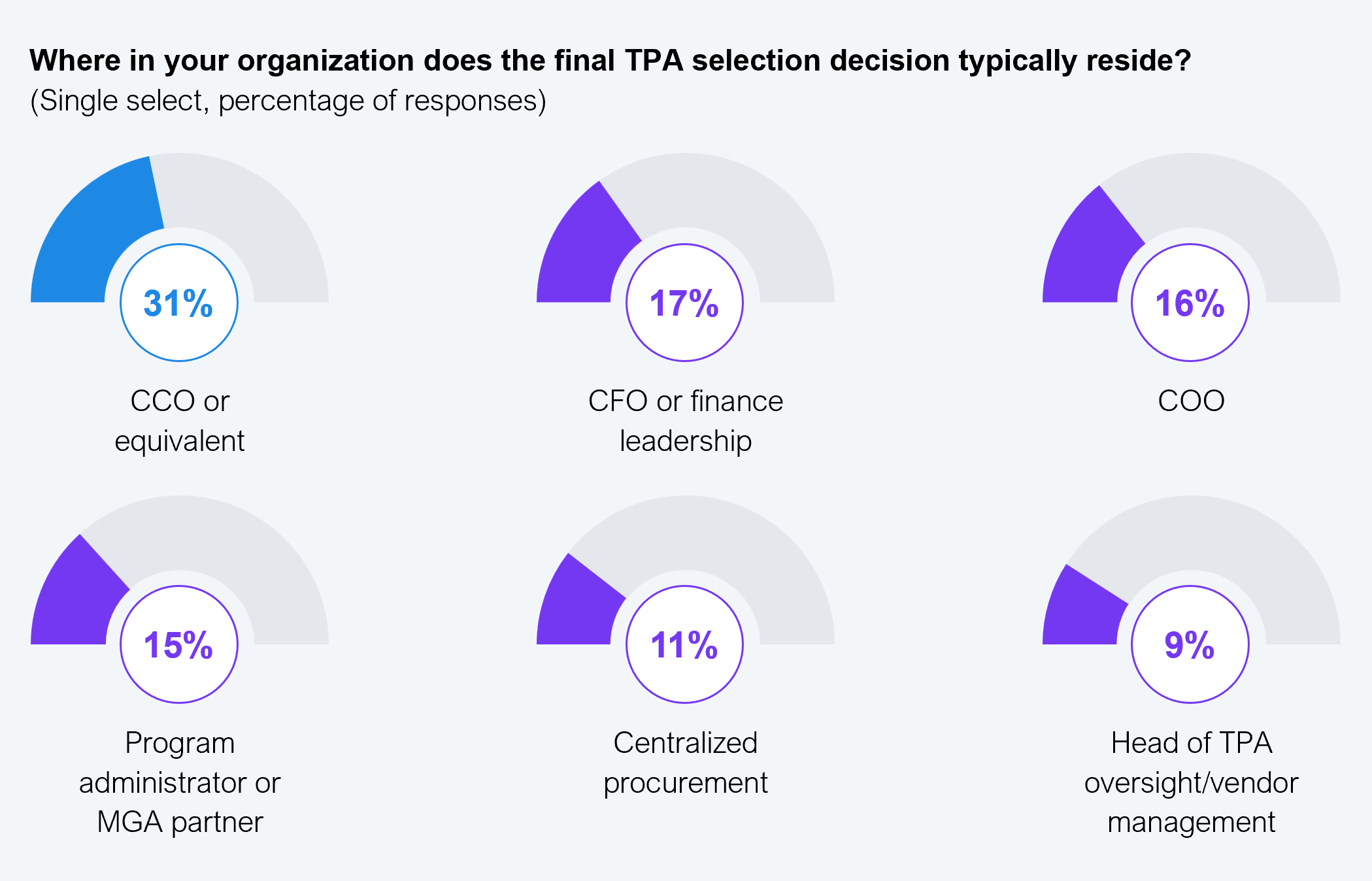

The mismatch is structural, and the buying committee fragments it further. Only 31% of insurers say that the CCO is the primary final decision maker for TPA selection. The remaining decisions are split across CFOs, COOs, MGA partners, and procurement leaders, each evaluating through a different lens. The CFO sees price-per-unit, the CCO sees outcomes, and the COO sees vendor management. There is no single accountable owner for the trade-offs between them.

Sample size: n=302

Source: HFS Research and Xceedance, 2026

Insurers fire on outcomes

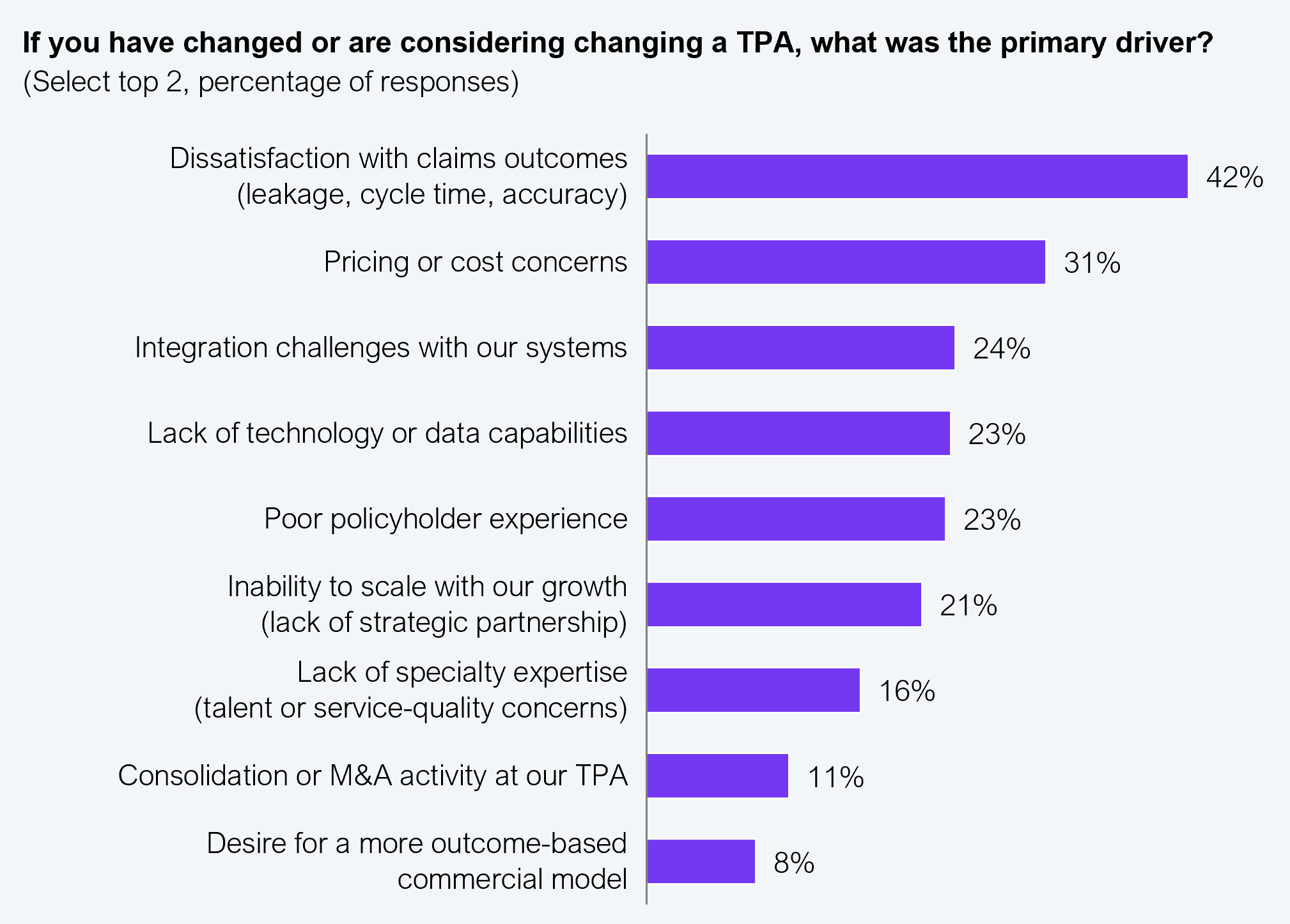

The third logic surfaces only when insurers leave their TPAs (see Exhibit 6). The exit logic is unrelated to the entry logic. It’s the outcome failure, not pricing, that breaks the relationship. Forty-two percent of those changing or considering changing TPAs cite dissatisfaction with claims outcomes, including leakage, cycle time, and accuracy as the primary drivers. Pricing concerns stood at a distant second at 31%. Lack of technology capabilities and integration challenges follow at 23% and 24%, respectively. The procurement factor, heavily weighted at the front end (82%; as shown in Exhibit 3a), is not the most common reason insurers leave.

Sample size: n=273 (subset reporting active or planned switching)

Source: HFS Research and Xceedance, 2026

How the disconnect compounds

The disconnect compounds because of three characteristics of the procurement design itself:

I’d make it so switching TPAs wasn’t such a nightmare. The data migration alone takes six to nine months, and half the historical claim information gets lost or corrupted in the process. It creates an artificial lock-in.

— Self-insured enterprise

The problem is not that TPAs lack technology, but that the procurement design leads to misalignment. This misalignment appears in leakage for which no one is held accountable and in the structural lock-in that keeps insurers in relationships they would otherwise exit. Both are solvable, and many fixes can be implemented during the procurement and contracting stages.

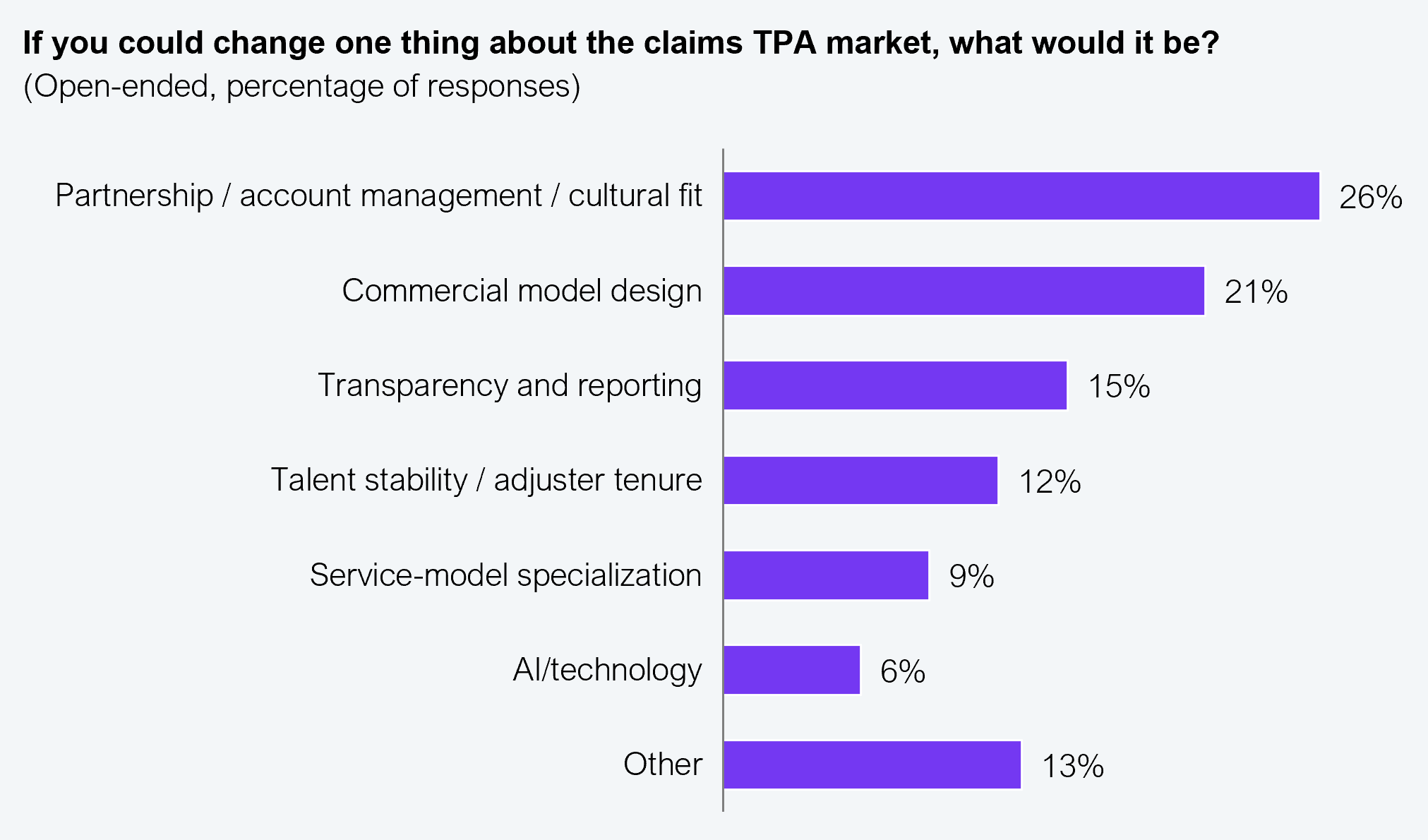

AI is not what insurers say is broken about their TPA. It shows up in just 6% of responses when enterprise insurance leaders describe unmet market needs. Data shows that it ranks top among the TPA selection criteria and anchors nearly every modern TPA pitch. Insurers expect it, but what they are not getting is something different entirely.

When asked what is actually broken about their TPA experience today, insurers cite partnership quality, account management depth, and cultural fit far more than any technology gap (see Exhibit 7). That pattern holds across every buyer segment: admitted carriers, E&S, MGAs, self-insured enterprises, and insurtechs. AI is the price of entry, and the relationship is where TPAs are actually failing.

Sample size: n=302; analysis of open-end responses

Source: HFS Research and Xceedance, 2026

Account management depth

Insurers want substantive engagement from claims domain experts, not generic client success managers. Three out of every four frustrations cluster around this layer. The complaint is consistent: senior people show up for the pitch, while daily contact is three levels below.

The senior team shows up for the pitch, then you never see them again. Your day-to-day contact is someone three levels below the person who sold you the program.

— P&C carrier (admitted)

Cultural fit and operational accountability

Insurers want TPAs that operate as extensions of their own claims’ teams, not as black-box vendors with proprietary playbooks. The desire isn’t TPA passivity, but genuine collaboration on operating decisions. Insurers call out the lecture-on-best-practices dynamic, the this-is-our-way inflexibility, and the absence of TPAs willing to challenge their own operating assumptions.

Transparency and proactive communication

Real-time dashboards top the list of must-have technology capabilities (76%), but the underlying complaint surfaced is relational, not technical. Insurers want TPAs to proactively flag emerging issues, not waiting to be asked.

I don’t want to hear about a problem claim for the first time when it shows up on a reserve report. Proactive escalation of emerging issues should be table stakes.

— MGA and program administrator

The themes vary modestly by segment. Admitted carriers emphasize transparency and reporting. E&S buyers stress service-model specialization. MGAs talk about talent and stability. Self-insured enterprises want technology modernization and visibility. Insurtechs lean toward pricing and incentive alignment. The partnership and account management theme threads through every group as the dominant unmet need.

Talent stability

Adjuster turnover is the leading source of frustration, particularly among MGAs and self-insured buyers. Each turnover event is a retraining cost that insurers absorb in cycle time and outcome quality, one that never appears on the invoice. The broader talent shortage, cited by 39% of respondents as a top external threat, narrows the available adjuster pool and makes retention harder to sustain across the industry. A TPA’s retention strategy and bench depth should be standard due diligence items before the contract is executed.

We’re on our fourth dedicated adjuster in two years. Every time we get someone trained on our program, they leave. The institutional knowledge loss is enormous.

— MGA and program administrator

Additionally, they want the following overhauled:

Commercial model design

Insurers want commercial structures that put TPAs in the game with them, not pricing that rewards execution and ignores improvement. Only 12% of contracts are structured around outcomes today, while 76% of buyers would pay a premium for a TPA that demonstrably reduces leakage. Skin in the game is what turns a TPA from a vendor executing the brief into a partner that meaningfully improves it over time.

More willingness to put skin in the game. If a TPA truly believes their approach reduces loss costs, they should be willing to accept a fee structure that rewards them for outperformance and penalizes them for missing targets.

— P&C insurance carrier (admitted)

Data quality and transparency

Insurers want capability-grade reporting infrastructure, not scheduled monthly summaries that arrive after decisions are made. Only 44% are satisfied with their TPA’s real-time visibility, and 85% agree that the biggest gap in TPA performance is data quality and reporting, not claims handling itself. They want the data layer itself, i.e., claim-level access, API integration, and reporting, that connects to their own analytics estate.

I shouldn’t have to chase down my own TPA for basic loss data that I’m paying them to manage. Give me real-time dashboards.

— P&C insurance carrier (admitted)

Most TPAs lead with AI and technology in their pitch decks, RFP responses, and public marketing. They are responding to insurers’ selection criteria, which puts AI in the top three for 98% of buyers.

However, the market is solving the wrong differentiator at the wrong stage of the decision. Buyers award contracts on AI, leave them on outcomes, and become loyal to TPAs that fix the partnership. AI is necessary but not sufficient. The partnership layer is where value builds over time. The selection process should diagnose the partnership layer with the same rigor applied to technology demos.

More accountability on outcomes. TPAs are great at reporting activity, but nobody’s tying compensation to whether they actually reduced our total cost of risk

— P&C insurance carrier (admitted)

The big TPAs have the scale; the small ones have the agility. What the market needs is more firms that have figured out how to have both.”

— MGA and program administrator (admitted)

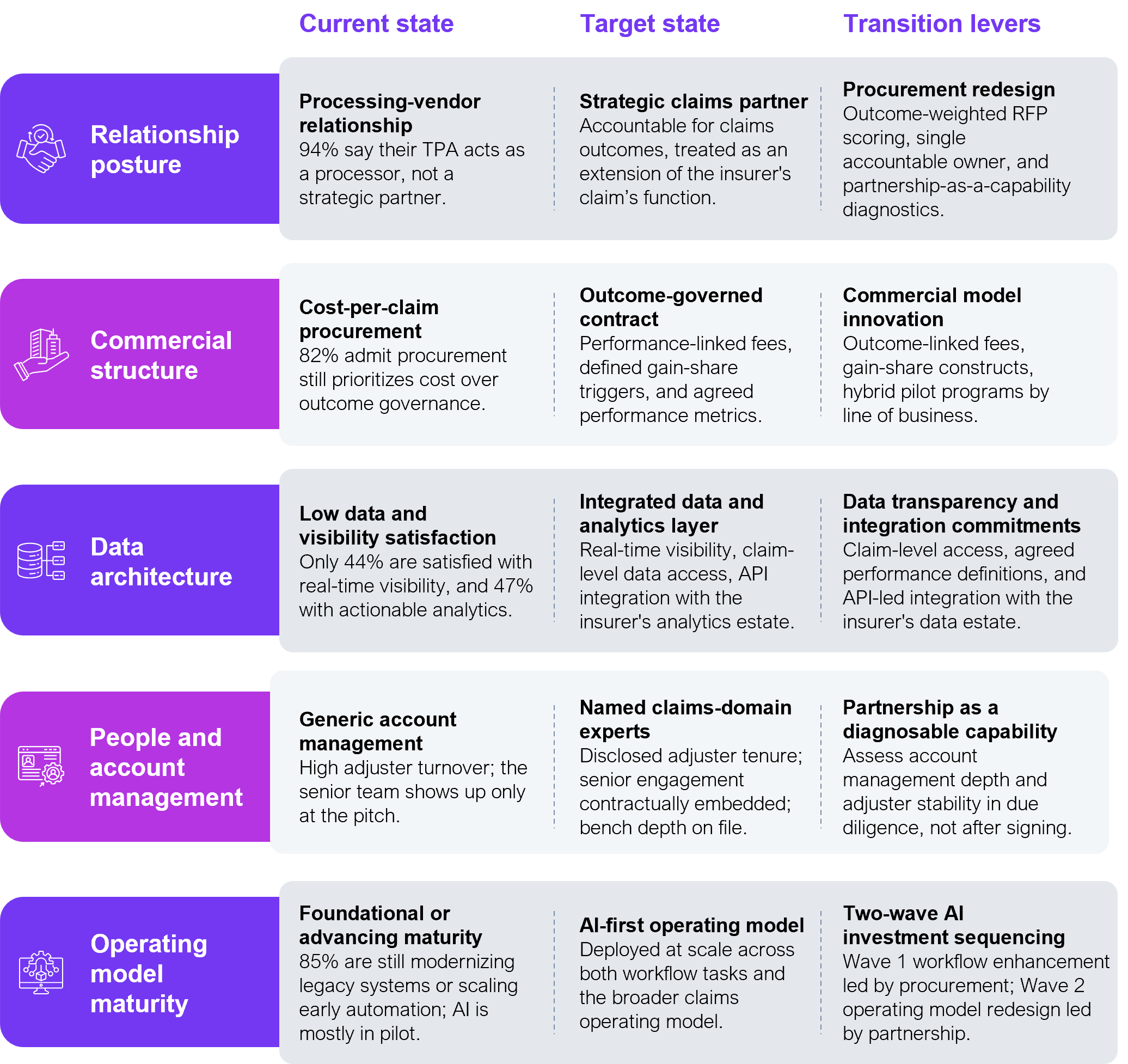

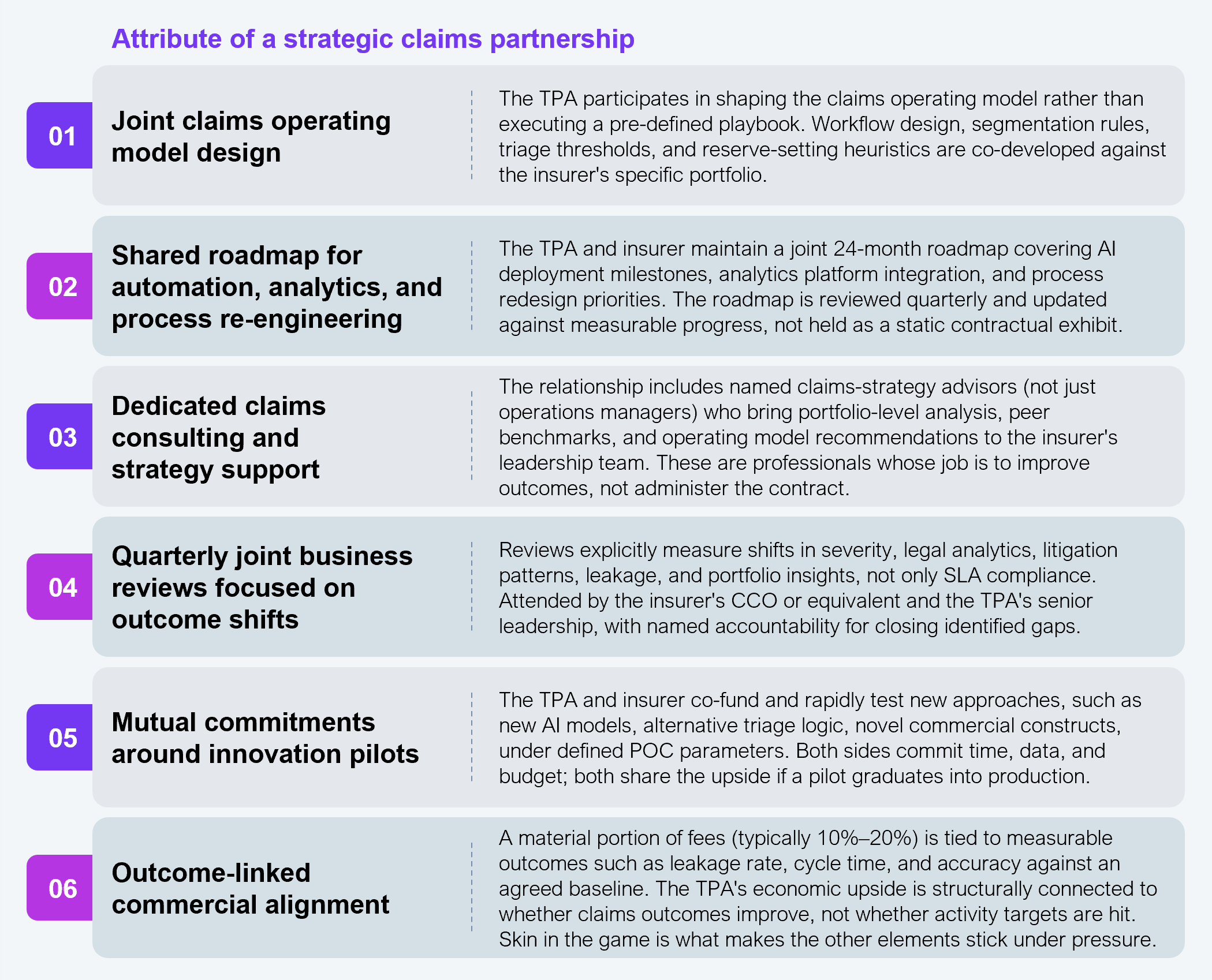

The four unmet needs that insurers describe are symptoms of a single structural absence: most TPA relationships are not designed to operate as strategic partnerships in the first place. A genuinely strategic partnership is a set of contractual and operating commitments insurers need during selection, not hope for after signing.

*Note: Not all six are equally achievable today. Elements 4 and 6, i.e., quarterly outcome reviews and outcome-linked commercial alignment, are within reach for most insurers in the current renewal cycle. The other four need negotiating leverage, typically available only to larger or more sophisticated buyers. They mark the difference between a top-quartile TPA relationship and the median one.

Source: HFS Research and Xceedance, 2026

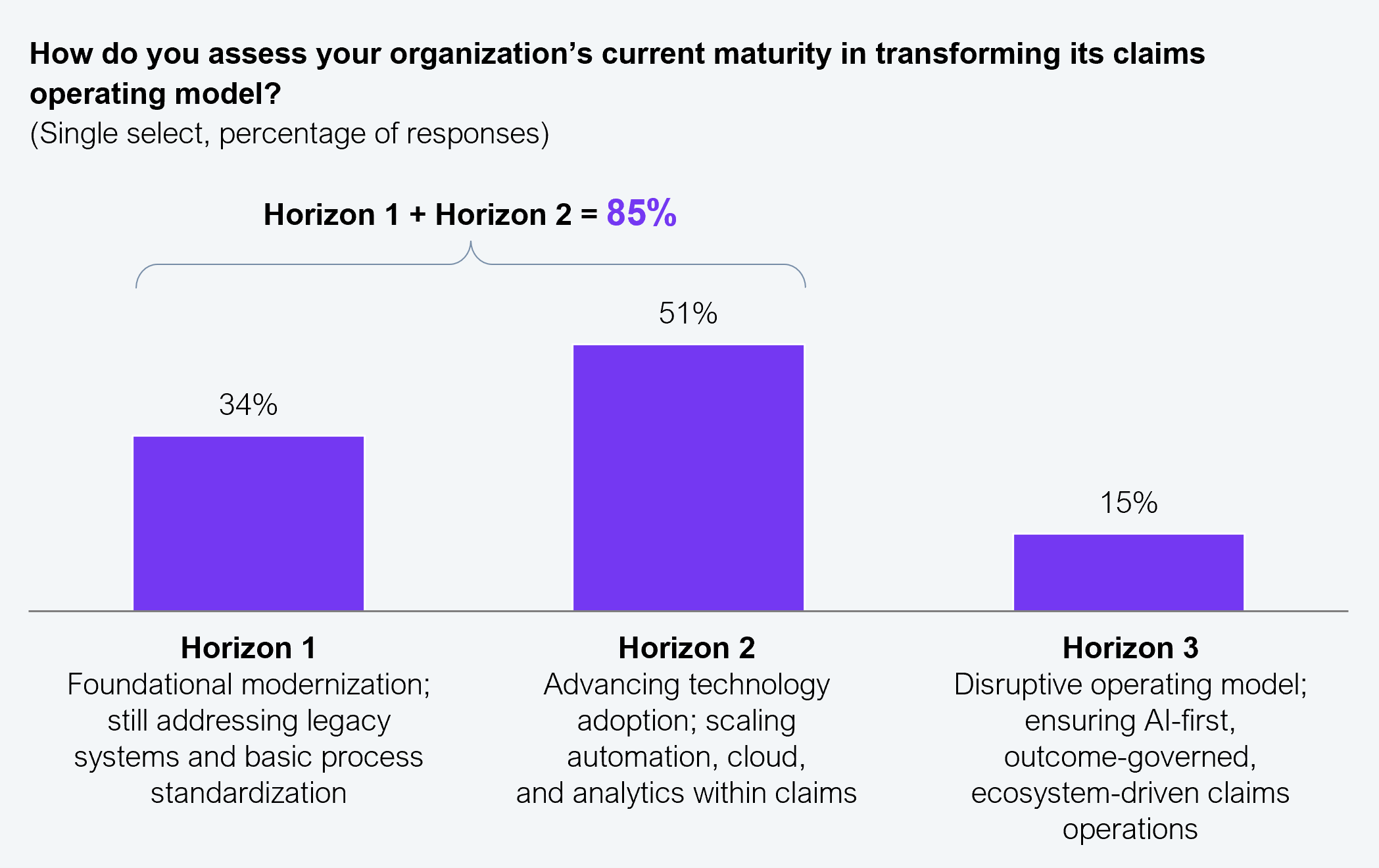

Demand is rising, the relationship is broken, and procurement is misaligned. Underneath it all, the operating model itself is still a work in progress for almost every player in the market.

Insurers skew early when asked to self-assess claims transformation maturity against a three-horizon framework: Horizon 1 (foundational legacy modernization), Horizon 2 (advancing through automation, cloud, integrated platforms), and Horizon 3 (disruptive, AI-first claims operating model). Thirty-four percent sit in Horizon 1, and 51% are in Horizon 2. Only 15% report a Horizon 3 disruptive operating model. In other words, five out of every six insurers are still building foundations rather than disrupting (see Exhibit 9).

Sample size: n=302

Source: HFS Research and Xceedance, 2026

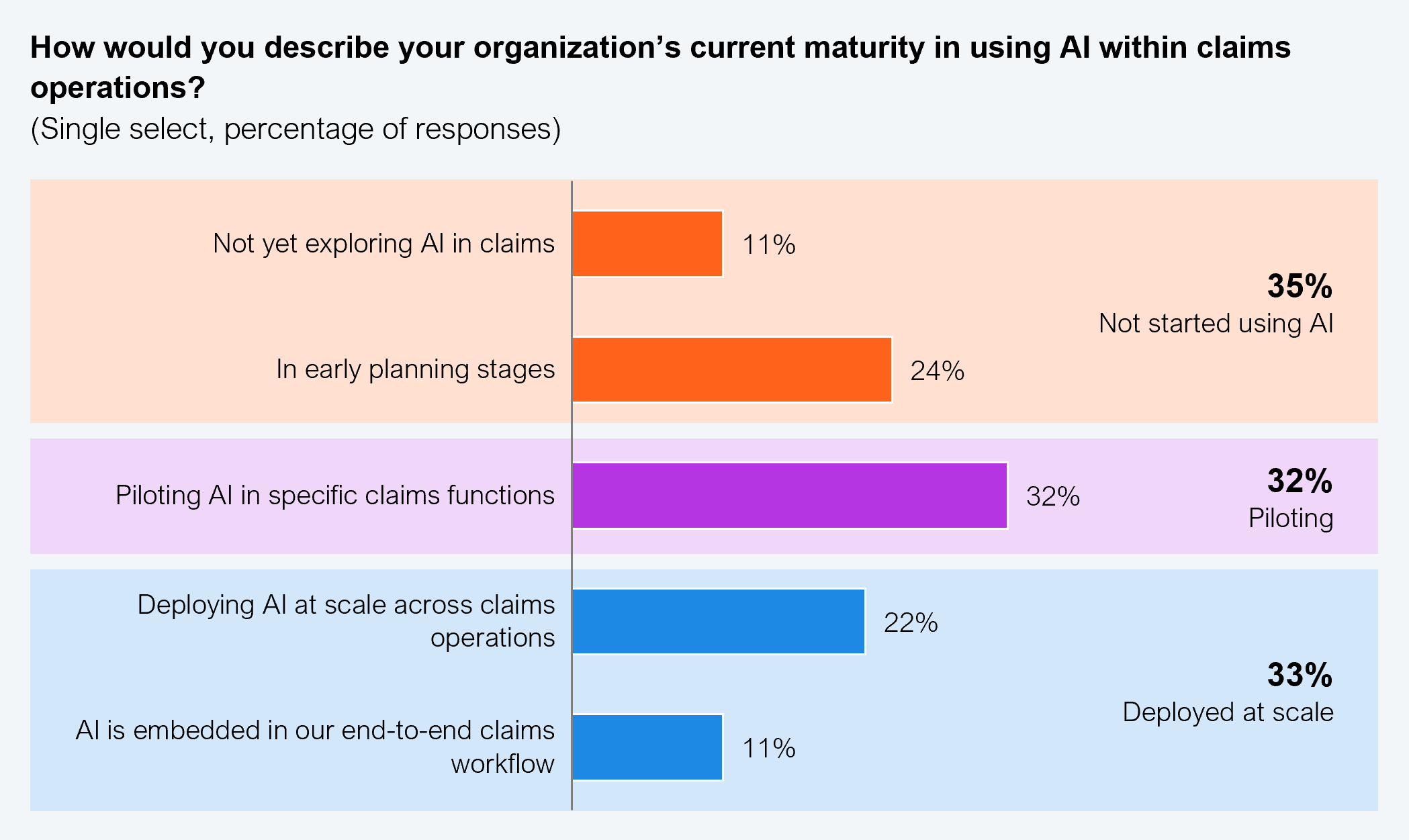

The AI deployment data tells the same story with sharper numbers. AI in claims is operating at three speeds at once and sits roughly evenly in thirds. About one-third of insurers (33%) have AI deployed at scale or end-to-end. A second third (32%) is piloting in specific claims functions. The final third (35%) is still in pre-production, either not exploring or in early planning. For buyers selecting a TPA today, the implication is direct: align with the cohort already operating with AI at scale or default to the two thirds still building the foundation.

Sample size: n=302

Source: HFS Research and Xceedance, 2026

It’s important to note that “end-to-end embedding” can refer to varying levels of AI integration. For some TPAs, it can mean deeply integrating it into one workflow, like a glass damage triage. Others describe it as woven into every step of the claims lifecycle. The directional finding holds.

Where the market sees AI working

Insurers described gains where AI has been deployed: time-to-acknowledge improvements after AI-assisted coverage verification, fraud analytics programs surfacing significant suspicious-claim volume, and document-intelligence tooling reducing adjuster admin time. The pattern is consistent. Wherever AI has been deployed at single carriers, the outcomes those respondents describe are material to their economics.

Our TPA recently deployed an AI-assisted coverage verification tool and our time-to-acknowledge metric improved by nearly 30%. That’s the kind of change I’m talking about.

— P&C insurer

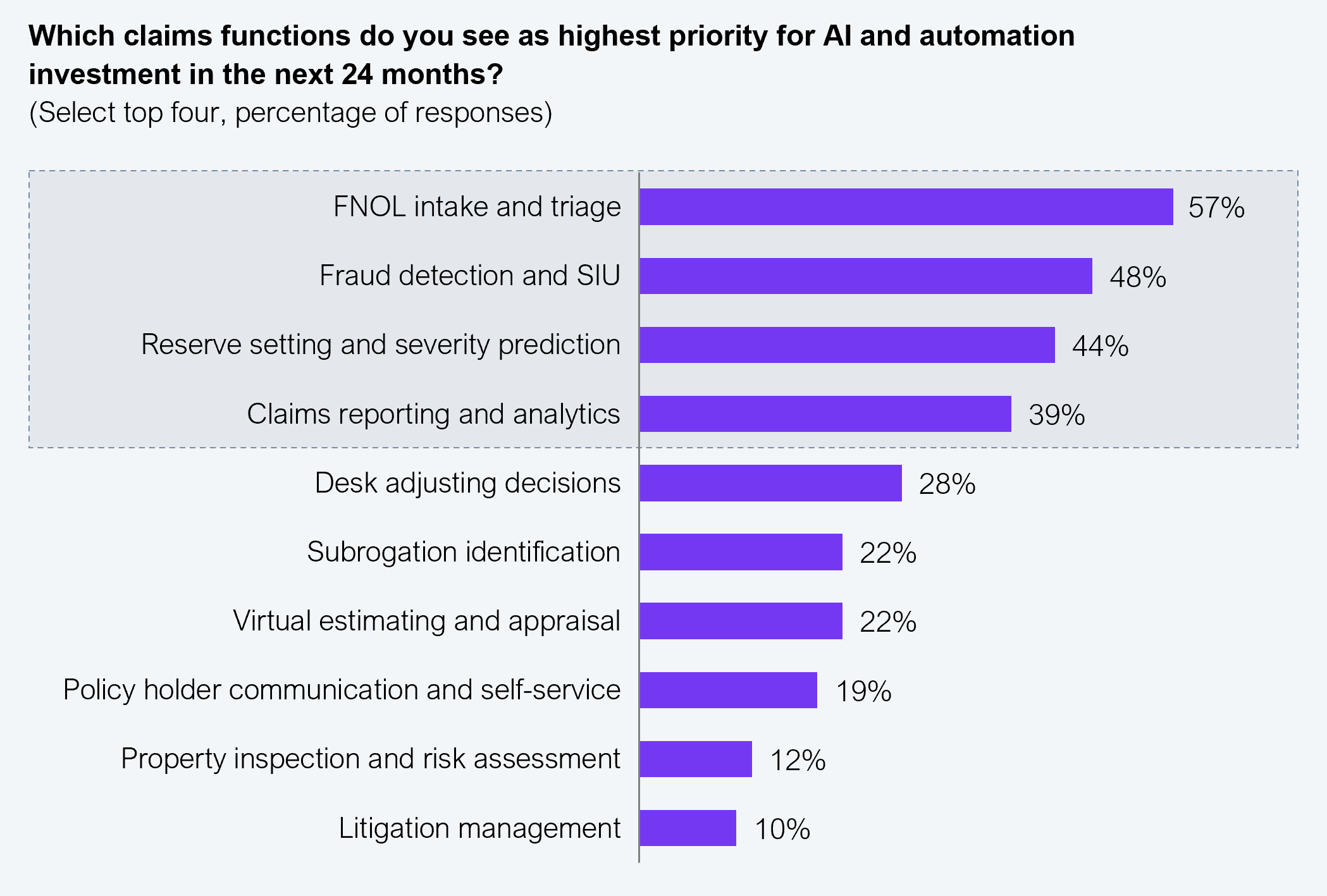

Where AI is going next

Insurers are prioritizing AI investment to attack loss-ratio economics first and customer-facing or judgement-heavy work last. The top three priorities are: FNOL intake and triage (57%), fraud detection and SIU (48%), and reserve setting and severity prediction (44%), all directly affect leakage and cycle time. The market is least willing to deploy AI in areas like., litigation management, property inspection, and policyholder communication). Insurers are not prepared to put AI between those decisions and their customers until the technology has demonstrated it belongs there.

Sample size: n=302

Source: HFS Research and Xceedance, 2026

There are two waves of AI surfacing in claims

AI in claims is unfolding in two distinct waves, and they require different operating logics, different vendor relationships, and different success metrics.

Wave 1: Reduce existing problems, enhance current workflows

This is where the market is now: AI applied to intake and triage to compress cycle times, AI for first-pass fraud screening, and AI-assisted reserve setting that flags severity outliers. The success metric is operational efficiency comprising hours saved, cycle days compressed, and leakage reduced incrementally. Most TPAs’ marketing AI capabilities are selling Wave 1 outcomes today.

Wave 2: Reorganize the claims operating model

This is where the market is heading and where Horizon 3 actually sits. AI doesn’t enhance the existing claim workflow; it changes what a claim workflow is. Subrogation becomes continuous and model driven. The litigation strategy becomes data-anchored from FNOL forward. The reserve setting becomes a learning loop, not a checkpoint. The emerging operating model has different roles, vendor topologies, and commercial structures. Almost no TPA delivers Wave 2 at scale today. The 15% of Horizon 3 insurers are mostly buying Wave 2 capabilities piecemeal from specialty providers.

The strategic implication is direct. Wave 1 is a procurement and execution problem; buy it, deploy it, and measure it on operational metrics. Wave 2 is an operating model design problem and one that requires a partnership that the TPA market is only just learning to deliver.

Conflating the two, buying Wave 2 outcomes from a Wave 1 vendor relationship is one of the most common patterns producing frustration in this market.

Automation without oversight is just faster mistakes. I want smart automation with human review at the decision points that matter.

— MGA and program administrator

The disconnect this study surfaces can be corrected within the buyer organization. They don’t require new technology, new regulations, or new market structures. They want insurers to redesign how they engage with the TPA market across procurement, contracting, performance management, and the operating model design. Four procurement and operating model moves address the core of it:

Our first HFS POV on this topic identified four pillars of digital sovereignty: jurisdictional control, operational portability, governance ownership, and infrastructure resilience. The four pillars are now five with the addition of stack interoperability: the ability to quickly swap vendors out, eliminating as far as possible vendor lock-in, is now an essential property of any sovereign stack. Together, these five suggested stress tests form the diagnostic that translates sovereignty from marketing hype to strong procurement and tests that vendors selling sovereign AI capability must answer.

Insurers fire TPAs on outcomes but buy them on cost. Closing this gap is the highest-leverage move available and doesn’t require an overnight shift to outcome-based contracts.

The sequencing is practical and deliberate. First, rebuild the TPA RFP scoring matrix so outcome metrics such as leakage reduction, cycle time, accuracy of reserves, and NPS are weighted on equal footing with cost. The 12% of the market on outcome-based contracts started here. Second, use the two-year renewal window to insert outcome-tied performance bonuses and penalties before the next contract cycle locks in. Renewals are the only moment where commercial terms are genuinely in play. Third, transition at least one significant program, a single line of business, a regional book, or a specific claims category to a hybrid outcome-based model within 12–18 months. The 27% of the market on hybrid commercials is not a fundamentally different type of buyer. They are insurers that decided to build the muscle one program at a time.

Three contract elements are worth negotiating explicitly. First, tie 10%–20% of the fee to a measurable outcome basket the TPA agrees within their control (typically cycle time and leakage rate against an agreed baseline) with a quarterly true-up. Second, negotiate explicit definitions for cycle time, severity, and leakage at the contract drafting stage. One of the most consistently cited frustrations in this study is that every TPA defines these terms differently, making apples-to-apples evaluation impossible. Third, reserve a contractual right to switch the TPA if outcome metrics miss targets for two consecutive quarters.

No single stakeholder owns the TPA relationship today, and that fragmentation can’t be solved downstream. CCOs hold 31% of final TPA selection decisions, with the balance fragmented across CFOs, COOs, and procurement. That fragmentation produces a TPA relationship that no single stakeholder owns. It can’t be solved through better performance management downstream because the misalignment originates in the selection process upstream.

Before the next RFP, build a single, weighted scorecard that captures cost, technology and AI capability, and outcomes and partnership quality with each dimension owned by the stakeholder best positioned to evaluate it. CFOs own cost, and CCOs and innovation leads own the technology. Outcomes and partnership require all parties at the table.

Assign one accountable owner, typically the CCO or a dedicated TPA program lead who signs both the selection recommendation and the ongoing performance reviews. Without that accountability, every TPA conversation will optimize against whichever stakeholder is most vocal in the moment, and the TPA will simply mirror that volatility.

Most insurers treat partnership as a soft, post-contract afterthought that the account manager handles. Treat it instead as a measurable capability that due diligence diagnoses during selection.

This calls for three requirements from every prospective TPA before the RFP scores. First, disclosed adjuster tenure data on accounts the TPA currently serves. Second, named claims-domain experts available by line of business, with bios and tenure on file. Third, an executive engagement cadence written into the contract: quarterly business reviews, named senior accountabilities, and escalation paths that bypass account management when needed.

Score these requirements against the technology demos in the same RFP. Partnership capability is not a soft credential. The data in this study is direct on the point: partnership underdelivery costs more in outcome quality than technology underdelivery costs in capability gaps. Three out of four frustrations respondents cite cluster around exactly this layer.

Wave 1 focuses on workflow enhancement and is procurement-led.

Buy it, deploy it, and measure it on operational metrics: hours saved, cycle time reduced, and incremental leakage reduction. FNOL automation, triage, fraud screening, and first-pass reserve setting all live here. Treat it with the pace and rigor of any other technology investment.

Wave 2 focuses on operating model redesign and is partnership-led.

The distinction is important because Wave 2 AI does not make the existing claims workflow faster. It makes the existing claims workflow obsolete. Subrogation becomes continuous. Litigation strategy becomes data-anchored from FNOL. Reserve setting becomes a learning loop. The vendor relationship that delivers Wave 2 looks more like a co-design engagement than a procurement transaction. The commercial structure looks more like outcome-sharing than per-claim pricing.

The TPA disconnect insurers are living through is not because TPAs are underdelivering on AI, but because the buying process fails to match what insurers actually want from those services. Insurers hire on cost, evaluate on technology, and fire on outcomes. The TPAs they ultimately work with can’t resolve that contradiction because it lives in selection, not delivery.

For insurers, the next action is to redesign procurement before the next contract. They must write outcome-aligned commercial terms, name a single accountable owner across CCO/CFO/COO/vendor management, and gate the RFP on AI deployment maturity, not AI pitch quality. TPAs, on the other hand, should lead with partnership and outcome economics before AI capability. Buyers reward depth of relationship in renewal, not pitch quality at the selection stage.

Register now for immediate access of HFS' research, data and forward looking trends.

Get Started

If you don't have an account, Register here |

With the exception of our Horizons reports, most of our research is available for free on our website. Sign up for a free account and start realizing the power of insights now.

Our premium subscription gives enterprise clients access to our complete library of proprietary research, direct access to our industry analysts, and other benefits.

Contact us at [email protected] for more information on premium access.

If you are looking for help getting in touch with someone from HFS, please click the chat button to the bottom right of your screen to start a conversation with a member of our team.