Atos raised a few eyebrows in late 2018 when it stumped up $4 billion to acquire Syntel to add some major strengths to its US financial services business and expand its global footprint. These eyebrows are raised because this acquisition is very unlike previous moves from Atos, with its motives driven by changing the very culture and nature of how the firm delivers services.

At first glance, this looked like a play from Atos primarily to strengthen its foothold in the US, where Syntel has strengths, while also tapping into some lucrative long-term relationships that Syntel has nurtured for many years. As this acquisition has unfolded, the narrative has shifted from top line growth to optimization of existing revenues, making it a potential game-changer for the newco.

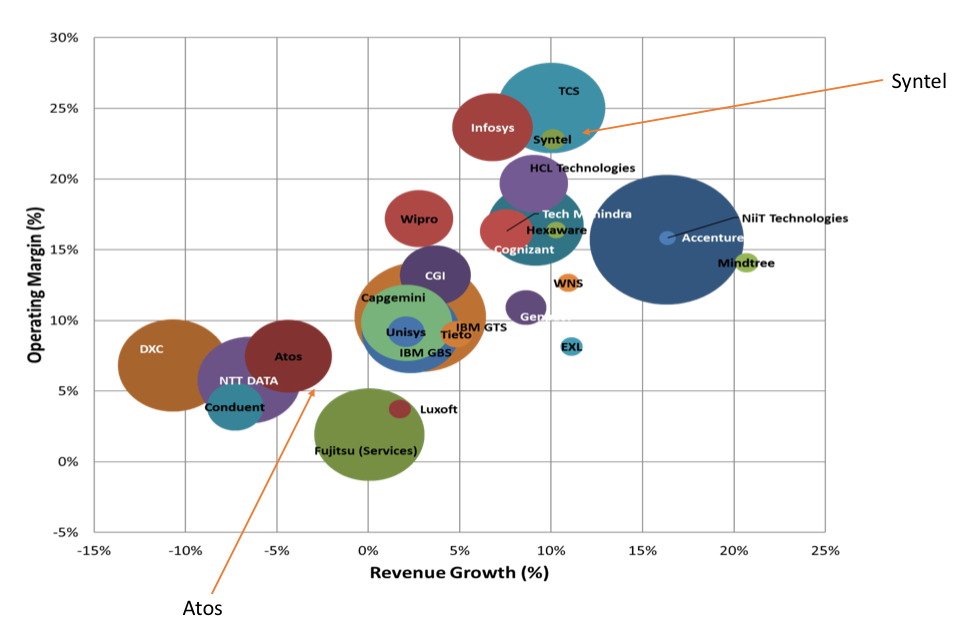

To many, Syntel’s high operating margin seems anomalous rather than ingenious. When you package all of the firms together on a single graph, the firm is an outlier, joined only by a few of the other major offshore firms, yet to trade margin for growth. (Exhibit 1 shows pre-merger margin versus growth performance from Q2 2018.)

The reality is that Syntel has perfected a model that drives out costs for both customers and the finance department. The firm’s commitment to long-term partnerships, automation, and a blend of nearshore and offshore has enabled the firm to push margins much higher than other firms of its scale. Atos executives, at its recent investor day in Paris, excitedly pushed plans to leverage the Syntel model for the majority of their corporate clients—to boost Atos’ margins. Atos is looking at the broader opportunity presented by its acquisition as a lever to drive change and increased profitability within its business, rather than additional revenues, market, or client acquisitions.

Exhibit 1: Provider performance overview, 2018 Q2

Like most of its contemporaries, Atos’ main stated strategic drive is to move away from its low-yield, traditional IT services business, and aim for high-value, higher-growth and higher-margin digital services. As this is swiftly becoming a hygiene requirement for a Tier 1 provider, rather than a differentiator, we don’t need to dig into this too much.

Things get interesting, though, when Atos adds in the extra dimension from this particular acquisition. Recent experiences in the M&A space have followed a basic formula: a major IT services firm acquires a company and rebrands the acquisition as the parent company. Talent leaves. The acquisition is over. However, Atos is taking a different approach; the firm genuinely wants to embrace Syntel’s service delivery model pledging to transition many of its existing commercial clients over to the Syntel model.

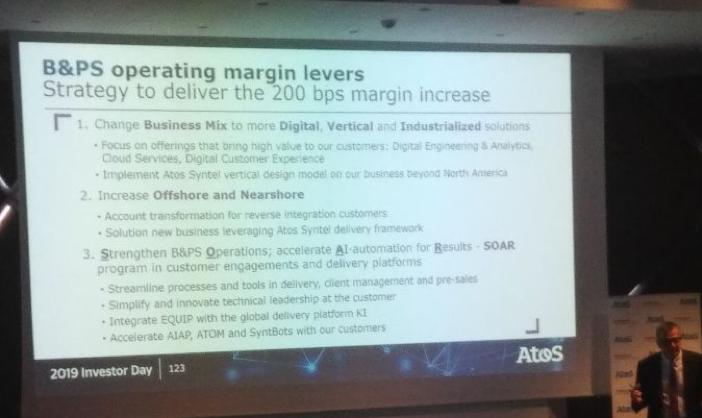

Atos also plans to change the offshore and nearshore blend of capability—shifting existing engagements to a more efficient blend that includes Syntel’s significant offshore capabilities and ensures all new client engagements are spread across the most efficient areas of the Atos-Syntel delivery framework (see Exhibit 2).

Exhibit 2: Operating margin levers for the Atos-Syntel delivery model

Another tool in Syntel’s toolbox is Syntbots, a proprietary process automation platform that the firm leverages to automate as many processes as possible, keeping costs low and margins high. In its push to boost margins and drive efficiency, Atos is keen to leverage a similar enthusiasm for bots across the firm as part of its SOAR initiative (“strengthen B&PS operations, accelerate AI-automation for results.” The SOAR initiative and Syntel’s enthusiasm for bots mean we can expect greater cross-fertilization of Syntel’s aptitude for automating away low-value activities with Atos’ predilection for data management—the former most likely to precede the latter.

This approach from Atos means clients can expect some changes to creep into existing engagements over the first half of 2019. Processes that weren’t in scope for automation might now find themselves swarmed with Syntbots. The delivery blend may also change, with some work pushed offshore to keep costs down—and clients can expect engagements to become more aligned with Syntel’s vertical-oriented structure. If you’re an executive in a bank, in particular, you’re likely to find solutions relevant to your industry pushed toward you and ex-finance CIOs taking the lead from Atos’s sales engine.

As one would expect from an investor day, the focus was primarily on how Atos was becoming more financially attractive, so when they discussed margins and efficiencies, they geared the pitch toward shareholders wanting more value from their assets. But as industry analysts, our thoughts strayed to how clients could get in on the action, make the most out of this deal, and pick up their fair share of any cost reduction.

Bottom Line: Atos leverage Syntel’s high profitability is good news, but existing clients must ensure they get in on the action.

The reality is that this move is in many ways a vital step for Atos to push a better price point into a highly competitive market. The quagmire clients in which many clients will find themselves is how they are expected to pay for services in future.

Providers love to push “non-linear” pricing, where their clients “shouldn’t concern themselves” with the number of delivery personnel devoted to their service contract. However, as a canny provider figures out how to deliver the same work with fewer people (or with lower-wage people), their clients need to share in those efficiency gains. And this is in the interests of the providers also, as they will be exposed to competitors who can clearly undercut prices upon renewal. The key is for clients to demand transparency and use this as an opportunity to reinvest some of the savings into co-innovation initiatives which add value to both parties and strengthen the relationship.

Register now for immediate access of HFS' research, data and forward looking trends.

Get StartedIf you don't have an account, Register here |

With the exception of our Horizons reports, most of our research is available for free on our website. Sign up for a free account and start realizing the power of insights now.

Our premium subscription gives enterprise clients access to our complete library of proprietary research, direct access to our industry analysts, and other benefits.

Contact us at [email protected] for more information on premium access.