It’s got to be one of the most significant milestones to date in the rapid adoption of Robotic Process Automation (RPA), that industry pioneer Blue Prism is now a £1bn ($1.3bn) market cap company. Investors are desperate to find new investment opportunities, and any successful proven business in the enterprise automation and AI space is flavor of the month. However, as the secret sauce spicing up RPA becomes increasingly less secret and easy to replicate, can this valuation explosion sustain itself long-term?

It was only March 2016 that Blue Prism made its initial public offering (IPO) at 78p per share, valuing the company at £48.5m ($65m). It’s proved one of the most successful tech floats since, with the shares going on a pretty constant rise to its current high of 1,684p ($22.43) (See Exhibit 1) – and breaking the £1bn market valuation last week.

Exhibit 1: Blue Prism share price since IPO in March 2016

Source: FT.com

Let’s not forget Blue Prism is trading at this multiple based on its growth potential, not profits.

Blue Prism’s H1 revenues were £9.3m ($12.4m), up 133% yoy. And earlier this month, it said revenues for the year ended 31 October, would beat analyst expectations. Assuming revenues at least double to £20m ($27m), Blue Prism’s value would now be 50x sales – a staggering Price to Sales Ratio (PSR). To put this in perspective, the PSR for the S&P peaked in 2017 at 2.19[1] – and this is the highest it has ever been over the last 15 years!

And the underlying customer numbers are dizzying. This year the company secured 609 new software deals, and took on 324 new customers overall (vs. 189 software deals, and 95 new customers in 2016).

This means new software wins have more than doubled, and new logo customers have more than trebled over the past year. We believe there will still be strong underlying growth from new customers next year. However, inevitably the growth rate of new logos will begin to slow down in the near to medium term.

Consensus forecasts put Blue Prism’s 2018 revenues at £38m ($51m), which would be another 90% increase on this year. To achieve that, Blue Prism will need to sign well over 1,000 software deals in the year (we don’t expect the average RPA deal size to dramatically increase in the next 6 months though there might be some exceptions such as the Sumitomo deal). So there’s no softening of the ambition.

The billion-dollar question – is RPA sustainable?

The literally billion-dollar questions are now whether Blue Prism can continue growing at this rate, and whether the RPA sector valuations are sustainable.

We’ve no doubt that RPA has a lot of life still in it. The sheer scale of poor, often neglected manual business processes in organizations, means RPA will continue to present rich pickings for some time, for both the RPA providers and the broader ecosystem that is now supporting it to deliver better results, and improved customer experience.

One of the big plusses is the RPA providers’ channel partner models, through which they sell via global, regional and local specialists. It’s a great because it keeps the cost of sale down, and gives them access to both local and global customers, leveraging the scale and reach of partners.

To date RPA is still under-penetrated in many of the target organizations. Most are either in pilot phase, or now beginning the scale-up challenge across the organization. Either way it presents more opportunity in the customer accounts for the foreseeable future, and we expect to see compound annual growth of 36%, between now and 2021.

However, while the outlook for growth continues to look optimistic in the near term, there are some very real challenges RPA providers face, and which we believe they need to address to ensure RPA in its current form is sustainable.

Scaling and Customer Experience challenges

One big issue is that customers have been sold RPA licenses because they have bought the vision of it being a silver bullet. Unfortunately, we’re finding in our RPA Customer Experience research, that early pilots have often failed to deliver the outcomes and time to value expected – often because processes are more complex than initially thought, or due to lack of experience or capability among the stakeholders. Many have bought with the sole intention of cutting costs, but failed to realize it’s actually a much bigger challenge to do this in isolation without buy-in across the business.

Our research shows that just 58% of RPA customers are currently satisfied with their implementations. This is why we are now going deep, with RPA customers, to understand what are their pain points and how they see their RPA suppliers performing against specific service experience criteria (see The HfS RPA Customer Experience Survey). The results will begin coming out next month – but we provide a sneak peek at some of the results in our chart below.

Successes depend on broader change management

Our view is that RPA’s success is going to be absolutely dependent on broader business transformation, process re-engineering and change management services – whether via in house expertise of via external third parties.

These are the traditional service excellence capabilities that have supported organizations through highly disruptive internal change before, like ERP transformation. Scaling RPA is no different. As many early pilots have found, the technology is the enabler, but it’s not the silver bullet. Indeed, without correct engagement from stakeholders, best practice guidance and support, and a deep understanding of the domain and its idiosyncrasies, and support throughout, RPA can in fact add to the problems that already exist.

Will we see other RPAs go public? Unlikely…

Blue Prism’s success inevitably begs the final question – are we now going to see other RPAs go public?

On balance, we think it’s unlikely, however there are strong arguments for and against. On the one hand, they may be put off by the level of scrutiny and public disclosure that they will have to provide. However, this also has a lot to do with personalities and ego, and the desire to make big money while the market’s hot. In our conversations with RPA players and those in the broader Intelligent Automation sector, they have all been keeping a very close eye on Blue Prism’s stock market performance.

Will RPA become a new M&A gold rush? Not really…

There are three primary reasons we don’t think RPA will become the next big M&A gold rush opportunity for one of the big IT/BP services firms.

1. RPAs are too expensive to target and service providers are already building their own bots

Blue Prism and other RPA shops have simply become too expensive to become the targets of acquisitions. Only the likes of IBM, Oracle, SAP, Microsoft etc can really consider it, and only IBM has strategic alignment with RPA. What’s more, IBM, despite being Blue Prism’s largest client, recently signed a mammoth RPA services engagement with SMBC (see link), where UIPath is the prime RPA partner, hence it makes more sense for Big Blue to remain technology agnostic in the RPA space. A PSR of 50 scares away most despite strong growth potential especially given the scalability question. IT/BP Service providers also might find it more lucrative to partner with multiple providers (as they currently do) versus buy one provider and put all eggs in one basket. To offer further choice, providers like TCS, Infosys and LTI have their own RPA tools, and can therefore deploy and support third party RPA vendor products, and their own RPA tools for maximum flexibility.

There is also a real possibility that some of the services firms will develop intelligent bots that are serious alternatives to the software pureplays. Infosys’ AssistEdge RPA product is already being used by several enterprises, as are bots being developed by the likes of Wipro (Holmes) and TCS (ignio). As clients need increasing help managing and customizing bots, ensuring their security, scalability and integration with other applications, analytics and Machine Learning tools, the more they will turn to manage automation offerings from services providers, including multiple RPA offerings.

2. RPA revenues from services outstrip software

As our RPA forecasts show, there is a lot more revenue around advisory and implementation services than pure RPA license revenues. In 2017 it’s 2.9x greater,, and that differential will only extend outwards, to 3.3x by 2021. This means that despite the high valuations around the software today, providers will always make more money from the broader services that wrap around RPA. Providers that are more interested in creating scale and revenue from RPA are therefore better placed to offer the services rather than the software itself.

3. Need for unbiased, third party services

Clients also want objective and unbiased service providers. Hence, they are all pursuing an ecosystem approach.

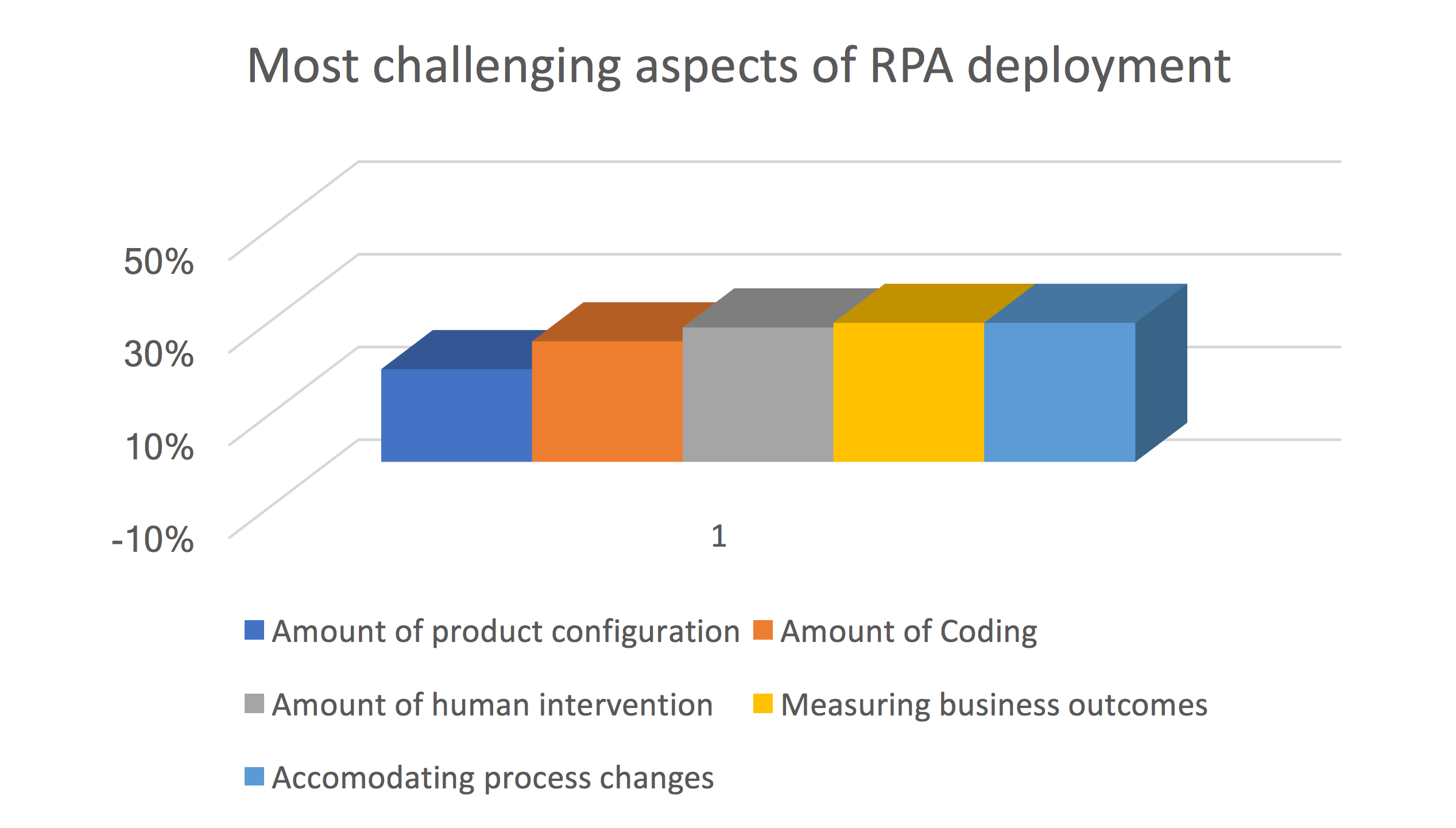

While many RPAs talk about plug-and-play capabilities, the reality is very far from this. Through our RPA CX research, it’s clear that the number one challenge relating to poor CX (see Exhibit 2), is the amount of additional work like coding and configuration needed to get RPA ‘production ready’. All top 5 challenges we have found relate to broader change management issues, which underlines how RPA CX is dependent on many more factors than product function alone. And this underpins the necessity for independent, unbiased services that can advise on products, delivery approaches and support RPA deployments.

Exhibit 2. Top 5 challenges of RPA deployment

Source: The HfS RPA Customer Experiences Survey

M&A consolidation between RPAs unlikely

Mergers between RPA providers are also not likely to happen. Beyond the expense factor, there are not enough complementary features to justify mergers, which is another nod to the risk of commoditization. As things stand today, we’re clear that the market continues to have room for everyone – so consolidation is not really required. Plus, most RPA providers are not really pals – and hostile takeovers are not what we are expecting.

RPA at risk of commoditization

The other very real risk facing RPAs, is the commoditization of RPA itself. At a core level, robots are ‘dumb’ in that they follow rules and logic, to execute a particular process, whether that’s opening and closing a file, extracting and inputting data, or logging tickets. They don’t use ‘intelligence’ to make judgements or learn from their actions.

The mega technology providers (Google, Microsoft, Amazon) are betting big on Artificial Intelligence (AI) versus RPA. The underlying RPA IP is not rocket science that these providers can’t figure on their own, and by offering the execution only layer, the RPA players are not really threatening to take away the broader and much bigger AI market opportunity from these mega providers.

The risk of RPA commoditizing fast is a real one if providers don’t continue to innovate and move up the value chain. Blue Prism and the other RPAs have an expanding set of AI/ML partners to augment the technology stack and value proposition. This is critical to overcoming some of the user experience gaps exposed in the early pilot programs.

The ecosystem approach only goes so far though, because it means all the competitor RPAs will also have access to the same ecosystem. Only by owning differentiating tech in these areas will RPAs be able to truly distinguish from the pack, so bolt-on M&A could become a possibility. Small tuck in deals wouldn’t in our view undo their ecosystem model.

It’s for this reason we think RPAs have to invest in AI/ML to differentiate at the core. AI tools to extract and catalog unstructured data, data mining and modelling to assess, streamline and improve the business process, and advanced analytics to learn, predict and even self-remediate, are going to deliver the added value customers desperately need for improved CX.

Baking in AI/ML techniques so that they can be deployed rapidly to accelerate time to value could become a powerful differentiator, and part of a vision for delivering autonomous robotic operations. It would also help RPA align closely with the broader Intelligent Automation opportunity.

Table 1. Summary of arguments ‘for’ and ‘against’ sustainability of current RPA valuations

|

For |

Against |

|

A huge untapped opportunity still remains to automate manual rules-based tasks across the enterprise |

RPA is low level, compared to AI and cognitive automation techniques, and will commoditize |

|

Partnering with global SIs and consultancies provides ready access for RPA to markets and customers globally |

Major BPOs and SIs unlikely to buy an enterprise RPA platform at current values, many now building their own competing RPA products |

|

Major RPA deal values are being openly discussed now, as part of wider business transformation initiatives |

Smoke and mirrors continue around deals and what’s been achieved to date with many disappointing pilot programs |

|

Truly game-changing potential to reduce costs, and dramatically improve productivity across operations |

Services revenues far outstrip RPA revenues and will be where the biggest dollar opportunities lie for players in the RPA ecosystem |

|

RPA really helps putting a band aid on legacy IT and increases its life. The relatively low investment and fast implementations make it inherently attractive |

Questions remain over the scaling potential of RPA. A lot more needs to be done on broader change management and delivering a better customer experience |

Bottom line: 2018 will be about making an impact

RPA providers of all shapes and sizes need to focus on the challenges identified. RPA is a nascent market, and evolving fast, so only by staying one or two steps ahead are they really going to be sure of capitalizing on their current run. We think evolving is essential to ensure the longevity of RPA.

2018 will therefore be an important year as RPA transitions from a shiny new object to a proper business value driver. That is why we think 2018 will be the year of making an impact.

[1] http://www.multpl.com/s-p-500-price-to-sales

Register now for immediate access of HFS' research, data and forward looking trends.

Get StartedIf you don't have an account, Register here |

With the exception of our Horizons reports, most of our research is available for free on our website. Sign up for a free account and start realizing the power of insights now.

Our premium subscription gives enterprise clients access to our complete library of proprietary research, direct access to our industry analysts, and other benefits.

Contact us at [email protected] for more information on premium access.