Executive summary

Food and agriculture enterprises are caught in an AI paradox: nearly two-thirds remain in early-stage adoption, yet they are aggressively prioritizing AI-led modernization across manufacturing, sustainability, and customer engagement. The gap between ambition and execution is widening, and the partner ecosystem is failing to close it. Nearly 50% of the respondents in this study said their current partners lack the deep domain expertise that food and agriculture transformation demands. Enterprises are not looking for generic technology providers. They want partners that understand commodity trading floors, traceability chains, and food safety regimes as well as embed AI natively into those workflows.

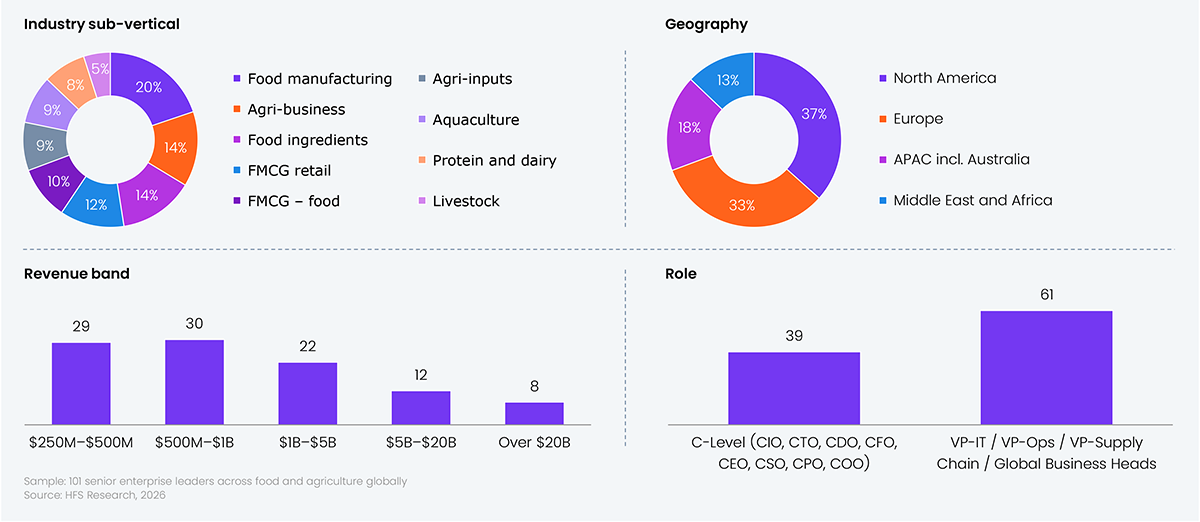

HFS Research, in partnership with Mindsprint, surveyed 101 senior leaders across food and agriculture enterprises to map transformation barriers, AI maturity, investment priorities, and partner ecosystem gaps.

The survey uncovered five key takeaways:

-

-

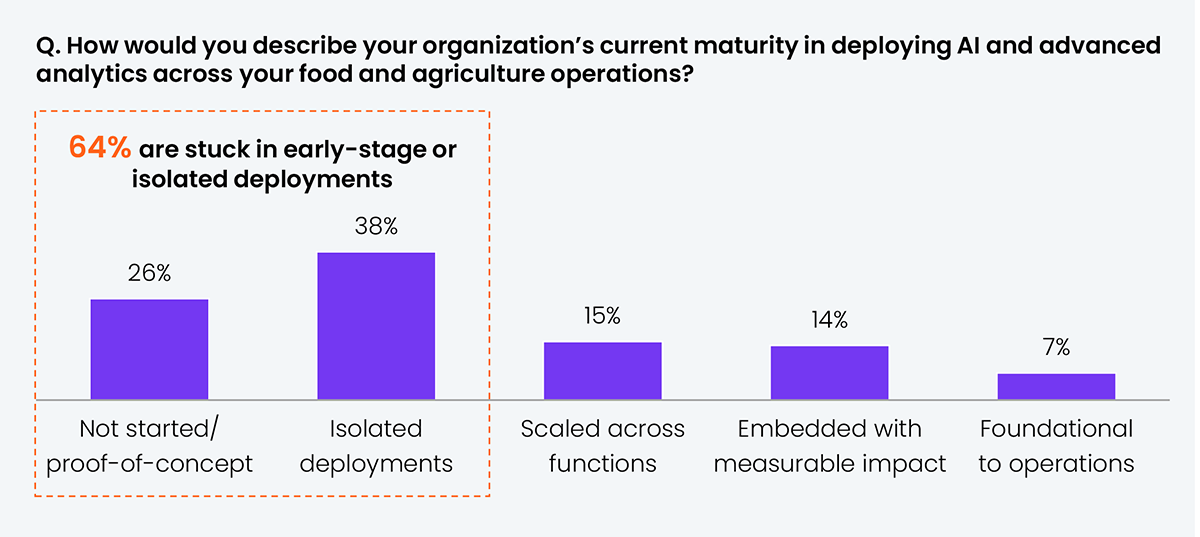

Nearly two-thirds of food and agri enterprises remain stuck in early-stage AI; half of them aren’t even measuring or seeing returns

-

Legacy ERP and data silos dwarf every other barrier, so fix the data estate before scaling AI

-

The upstream blind spot: AI investment clusters in post-harvest, while the origin of traceability is starved

-

What enterprises demand from partners: Domain expertise leads, followed by proven AI capability

-

Where partners are failing: 47% say domain expertise is the biggest need unmet

The Bottom Line: Stop bankrolling your food and agri partner’s learning curve. Roughly 82% of enterprises rate domain expertise as critical, 47% say their partners lack it, and 40% say partners can’t deliver productized AI. The data is unambiguous. Demand expertise or keep paying for someone else’s education.

- The industry is in an “AI holding pattern.” Sixty-four percent of food and agriculture enterprises are either still exploring AI or have only isolated deployments. Only 7% have reached a state where AI drives most operational and strategic decisions.

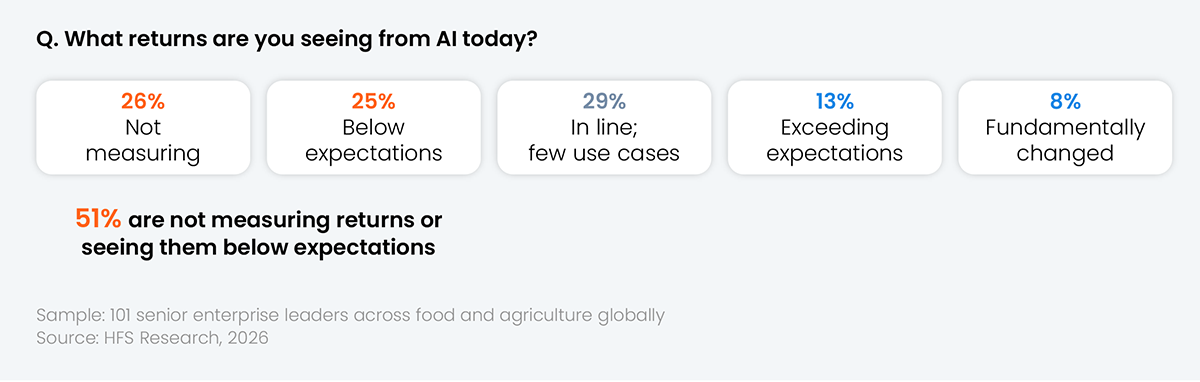

- The returns picture is equally sobering: 51% are either not measuring AI returns at all (26%) or seeing returns below expectations (25%). Only 21% report returns exceeding expectations.

- This gap between aggressive AI prioritization and anemic execution points to a structural problem. Enterprises are not short of tools; they lack the organizational readiness and domain-specific implementation capability to make those tools productive.

Fewer pilots. More scale. We have 47 proofs of concept and maybe 4 things actually running in production.

— VP of operations at a livestock and animal protein company in North America

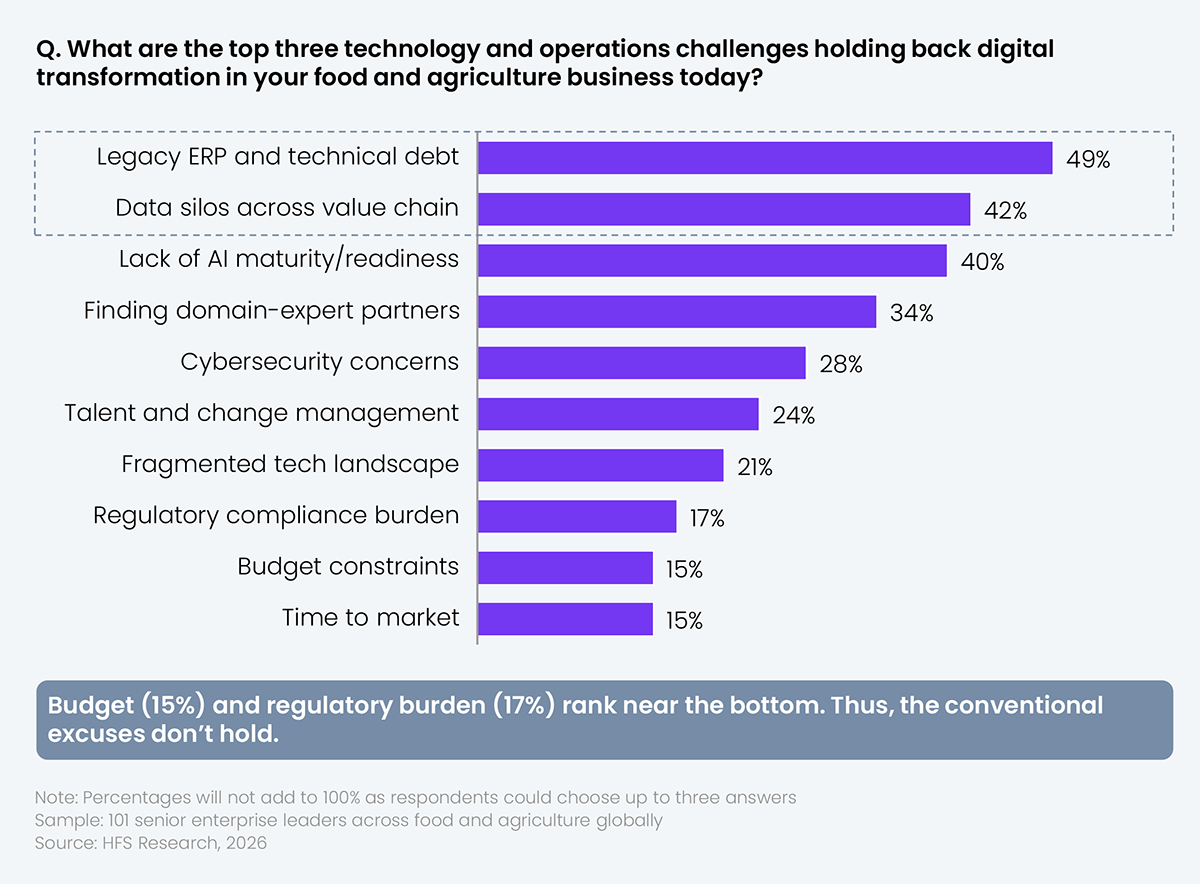

- The top two barriers are structural: legacy ERP (49%) and data silos (42%). These are the foundational debts that make AI scaling impossible without first modernizing the data estate.

- Budget constraints (15%) and regulatory burden (17%) rank near the bottom. The conventional excuse that “we don’t have the budget” is not what enterprise leaders are saying. They have the money. What they lack is a coherent data layer and modern ERP infrastructure to deploy AI against.

- The implication for enterprise leaders is clear: AI transformation programs that start with use cases instead of data modernization are building on sand.

We’ve spent more on consulting fees than on people who can actually sustain the systems once they’re live.

— C-suite executive at a protein and dairy company in North America

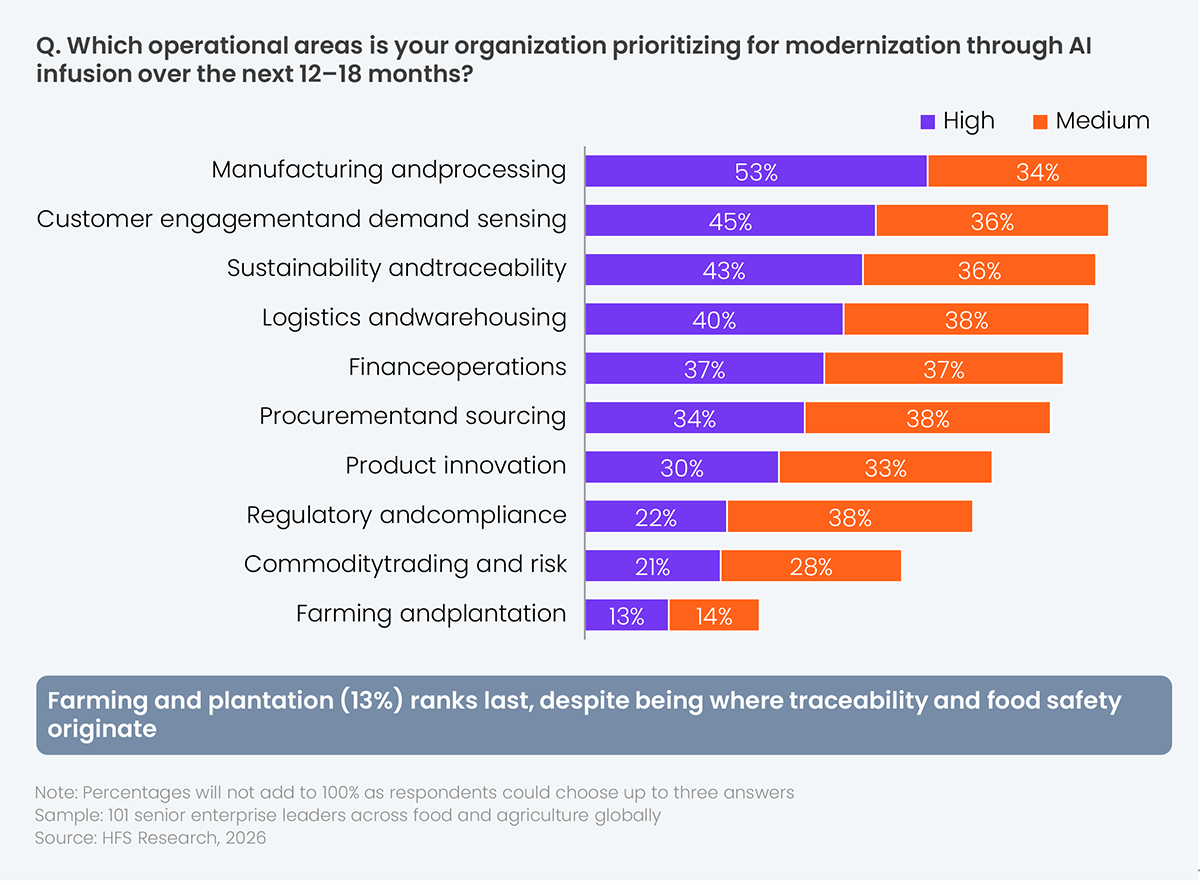

- The post-harvest cluster tells where the AI budget is going today: manufacturing and processing (53%), customer engagement and demand sensing (45%), and sustainability and traceability (43%). These are the functions closest to revenue and cost optimization, and where AI delivers the most immediate, measurable impact.

- Farming and plantation ranks dead last at 13% high priority, yet it is where traceability, food safety, and sustainability compliance originate. The regulatory imperatives that are existential for market access in Europe and increasingly in APAC start upstream. Enterprises are investing in the middle and end of the value chain while leaving the origin underserved.

Stop calling it transformation. Just fix the basic workflows.

— C-suite executive for a protein and dairy company in Asia-Pacific

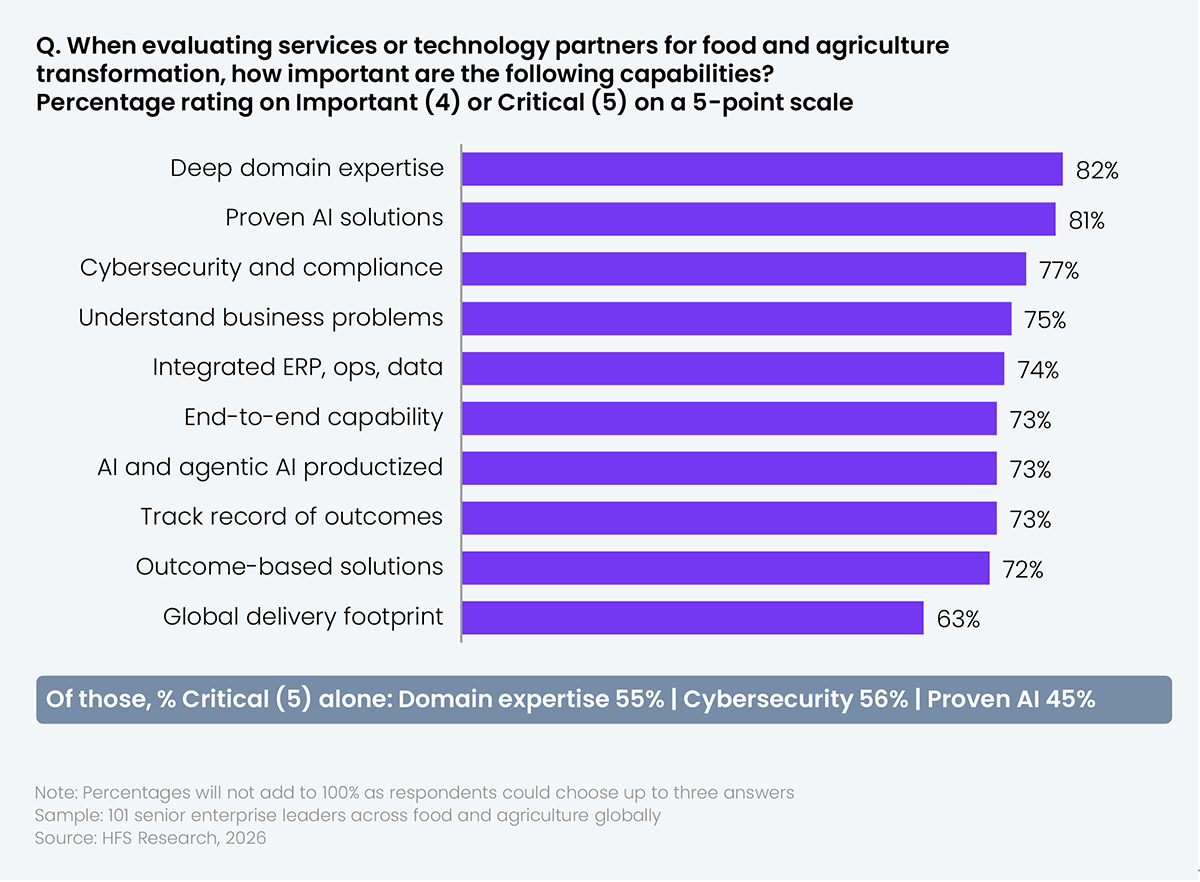

- Domain expertise leads the pack: 82% rate deep food and agriculture domain expertise as critical or important, with 55% at “critical” alone. This is the single strongest signal in the survey.

- Cybersecurity and compliance (77%) reflects the regulated nature of food and agriculture. FSMA, EU traceability mandates, and emerging sustainability reporting requirements make this non-negotiable.

- The demand for AI and agentic AI productized offerings (73%) and outcome-based solutions (72%) confirms that enterprises are past the experimentation phase. They want partners that can show a working product, not a roadmap.

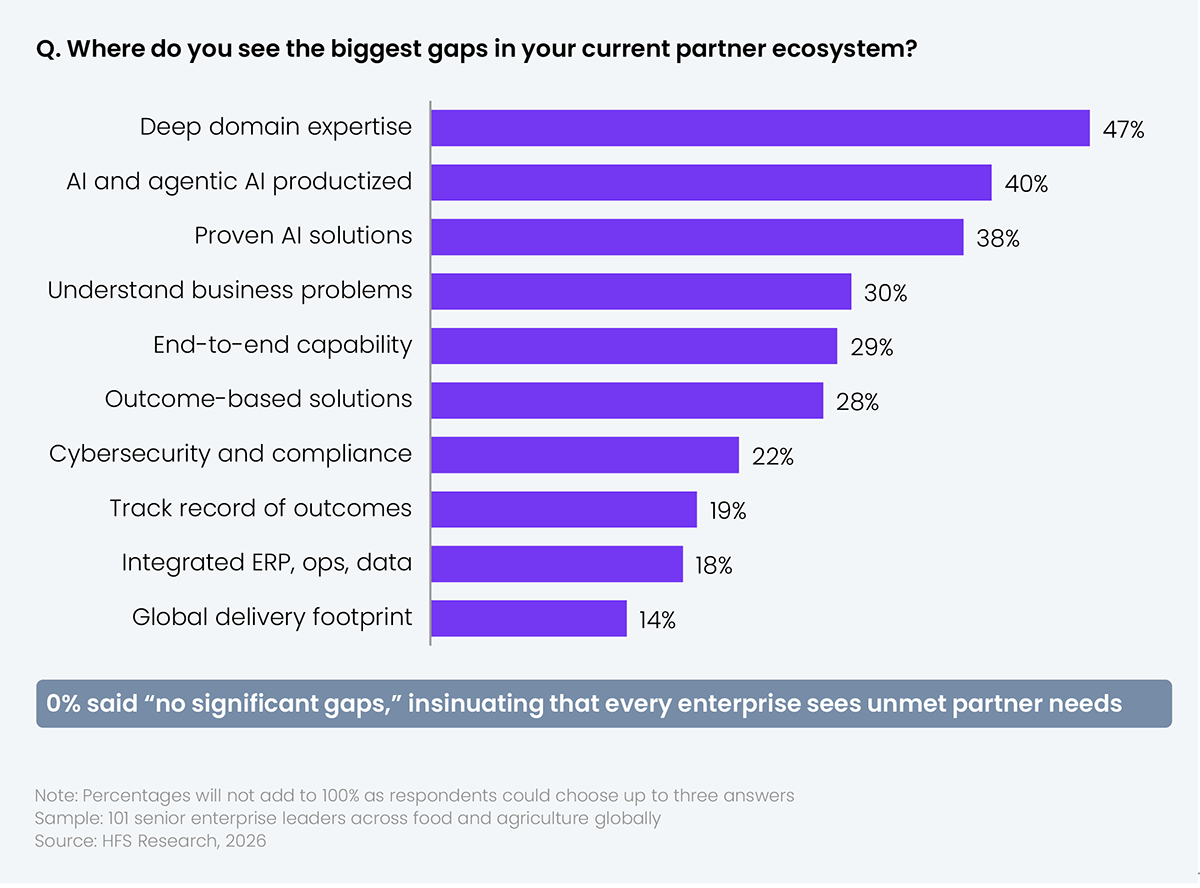

- Forty-seven percent of enterprises identify deep domain expertise as their single biggest partner ecosystem gap. This is the defining constraint, meaning that the most demanded capability (on the previous slide) is also the most absent.

- The second and third gaps: AI and agentic AI productized offerings (40%) and proven AI solutions for agri-food (38%) tell a complementary story. Enterprises don’t just want domain knowledge; they want it embedded into ready-to-deploy, AI-native product constructs.

Our biggest mistake was letting procurement lead vendor selection. They optimized for price. We now have six incompatible systems.

— VP of operations at a food manufacturing company, Asia-Pacific

The Bottom Line: Stop bankrolling your food and agri partner’s learning curve. Around 82% demand domain expertise, 47% say their partners lack it, and 51% are not even seeing measurable returns from AI. Demand expertise or keep paying for someone else’s education.

-

-

Fix the data estate before chasing AI use cases

The “AI holding pattern” (64% early-stage) will not break with more pilots. Forty-nine percent cite legacy ERP as the top barrier. Enterprise leaders should sequence data modernization before AI scaling, not alongside it.

-

Audit your partner roster against domain expertise

Eighty-two percent of your peers rate domain expertise as critical, and 47% say their current partners fall short. If your transformation partner can’t demonstrate specific knowledge of this value chain, replace them. DO NOT wait for them to learn on your budget.

-

Demand productized AI with outcome accountability

Seventy-three percent of enterprises want productized AI and agentic AI offerings, but 40% say their partners can’t deliver them. Stop accepting roadmaps and proofs of concept as progress. Ask for deployable products with measurable outcome commitments before signing.

Survey demographics