This HFS Point of View is for health system, hospital, ambulatory surgical center, and independent physician practice leaders confronting permanent margin pressure to adopt purposeful AI, escape payer dependency, and build new, higher-margin revenue streams.

The reduction of public health funding worldwide, particularly in the US on the heels of the One Big Beautiful Bill and ACA subsidy expiration, will corrode all four elements of the quadruple aim of care: cost of care, experience of care, health outcomes, and health equity. Both healthcare enterprises and consumers will be hurt. Yet, care delivery enterprises, including health systems, hospitals, Ambulatory Surgical Centers (ASC), and Independent Physician Practices (IPP), will be obliged to care for the community, which is aging with comorbidities, while the cost of care rises faster, 2x–3x that of nominal inflation.

In this context, care delivery enterprises need to partner with a new breed of technology service providers in the age of AI to overcome their structural challenges. In the HFS Horizons: Healthcare Providers (HCP) Service Providers, 2026 study, we evaluated 50 service providers for their ability to address the cost and experience (Horizon 1), health outcomes (Horizon 2), and equity (Horizon 3) for health consumers globally.

Source: HFS Research, 2026

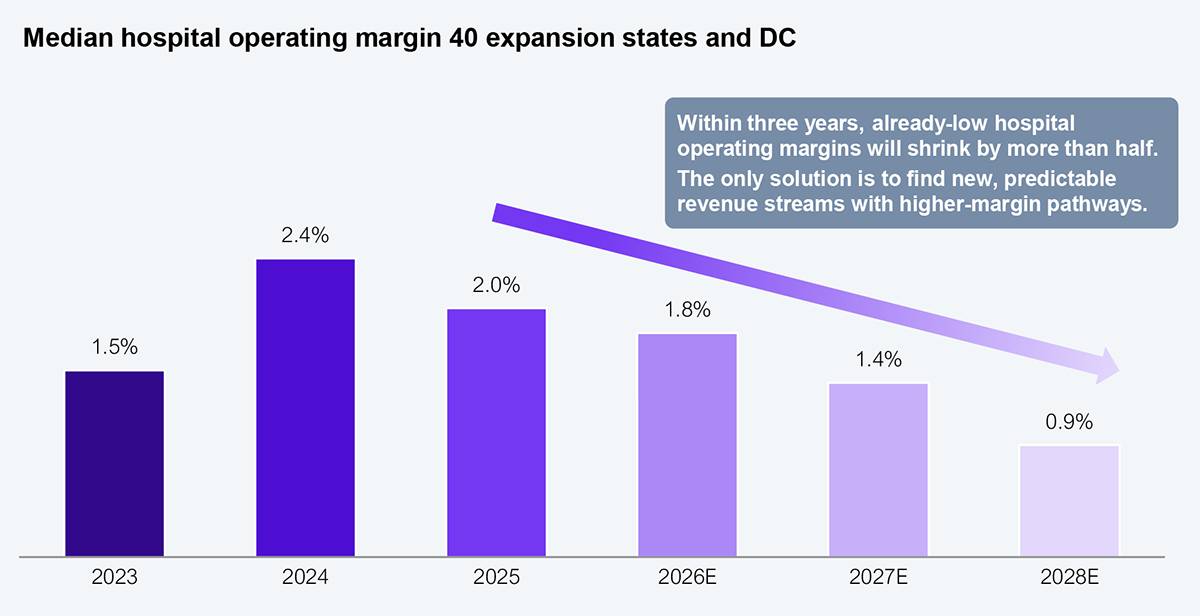

The financial crisis due to public health funding cuts is permanent (see Exhibit 2). Consequently, pricing models built for fee-for-service or value-based care (VBC) will accelerate the path to decline unless health systems find new, predictable revenue streams with higher-margin pathways.

Source: Urban Institute, Commonwealth Fund, Kaufman Hall, HFS Research, 2026

Providers must aggressively build enablement offerings to address self-insured employers. Their strategy must address three key dimensions:

This approach will help providers reduce their dependence on commercial insurance and government programs like Medicare and Medicaid, which will become increasingly administratively burdensome as reimbursements rapidly shrink. Directly addressing self-insured employers will be a win-win for predictable, higher-margin revenues.

Every failed prior authorization is an opportunity for providers to lean into offering self-pay options that improve cash flow at a higher margin (with no administrative burden). In addition, consider that 90% of all consumers enrolled in high-deductible health plans (HDHP) pay 100% of their non-preventive care out of pocket. One third (33%) of US workers, more than 50 million lives, are in HDHPs with an average single deductible of $1,886, up 43% over the past decade.

Given that 60% of insurer-negotiated rates are higher than the hospital’s own cash price for the same service, providers must step up their direct-to-patient game and build a second revenue line. Instrument cash-pay as a discrete P&L line so the shift is visible to the board. That board visibility will find support for atypical RCM (revenue cycle management) investments so that it can build on the paltry 1.8% of gross patient revenue (down from 2.8% in 2019). Thirty to forty percent (30%–40%) of the $1.6 trillion US hospital spend is schedulable in advance and price-comparable, and so provider leaders must create patient-friendly retail practices to reach consumers proactively. It is a generational opportunity for providers to disintermediate payers for non-catastrophic care and build their leverage for future negotiations.

Every year of delay in the onset of diabetes translates into about $16,000 in savings. Similarly, every year of delay in the onset of hypertension is a savings of approximately $3,000, not to mention the increased risk for the world’s biggest killer, coronary artery disease, and other diseases. Estimates of real savings from disease prevention and delayed progression are robust and significantly impact health systems and the communities they serve.

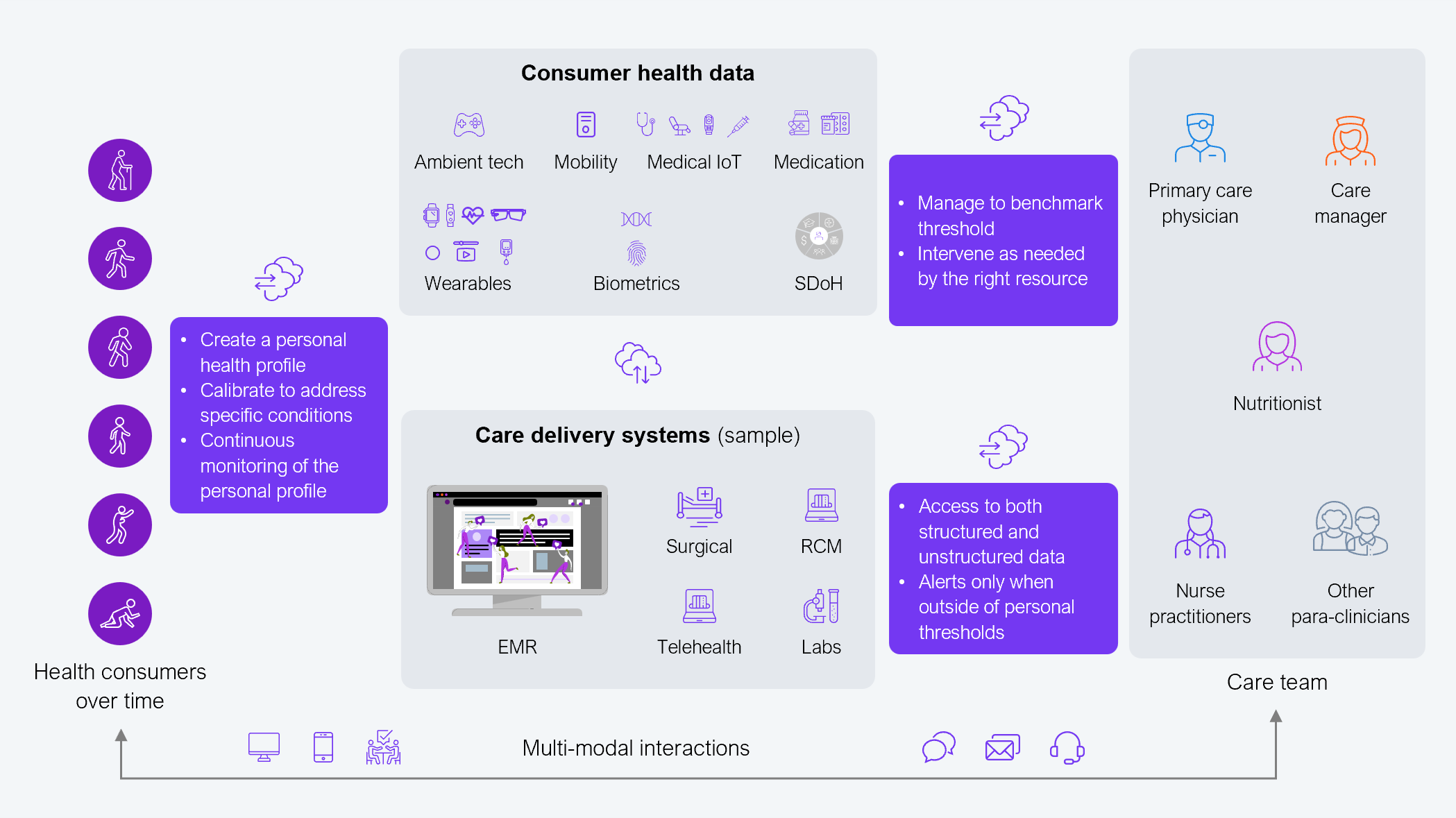

Consider then that there are a variety of technologies and devices on the market, at scale, and increasingly AI-enabled to be truly intelligent, capable of preventing disease, delaying its progression, and better managing it. A Wi-Fi-enabled intelligent toothbrush can help identify the risk for periodontitis, which can flag coronary disease risk. Wearables like continuous glucose monitors and smart watches can help monitor glucose levels and blood pressure in real time, flag activity (or lack of), and report a variety of other health attributes. When these devices are connected (see Exhibit 3), they begin to create the framework for a new paradigm: need-based intervention vs. demand-based.

Source: HFS Research, 2026

Historically, health systems have ignored the potential of connected health amid regressive payment models. However, the times are changing. Providers who don’t embrace technology are doomed to fail their patients and their communities.

The provider margin crisis will expose who can bend the cost curve, create new revenue streams, and shift care from sickcare to wellness management. The winners won’t be the ones with the biggest logos or slickest GenAI demos, but rather those who can escape payer dependency and industrialize direct-to-employer and self-pay models.

Register now for immediate access of HFS' research, data and forward looking trends.

Get StartedIf you don't have an account, Register here |

With the exception of our Horizons reports, most of our research is available for free on our website. Sign up for a free account and start realizing the power of insights now.

Our premium subscription gives enterprise clients access to our complete library of proprietary research, direct access to our industry analysts, and other benefits.

Contact us at [email protected] for more information on premium access.

If you are looking for help getting in touch with someone from HFS, please click the chat button to the bottom right of your screen to start a conversation with a member of our team.