This report is for chief procurement officers, sourcing leaders, and category managers redesigning commercial and governance models for AI-led professional services.

Five moves to fix your sourcing model before the next AI-led services deal lands

Within 12 months, 68% of enterprises will sign AI-linked contracts, but only 19% have a procurement model built to govern them. Chief procurement officers (CCPOs) caught in that gap will be signing onto risk they cannot price, measure, or control.

For decades, enterprise sourcing operated on one assumption: more people means more value. AI breaks that. The work that needed eight consultants now runs through a model overnight, with a consulting team to frame the question, check the output, and sign the result. However, the contracts buying that work are still pricing for the eight consultants.

HFS Research, in collaboration with EY, surveyed more than 300 Global 2000 executives and interviewed 8 procurement professionals to understand how enterprises are adapting their sourcing and governance models for AI-led services.

If you keep buying AI through a labor era playbook, you won’t just misprice it. You will sign onto risks you can’t see and inherit governance gaps you may not be able to close.

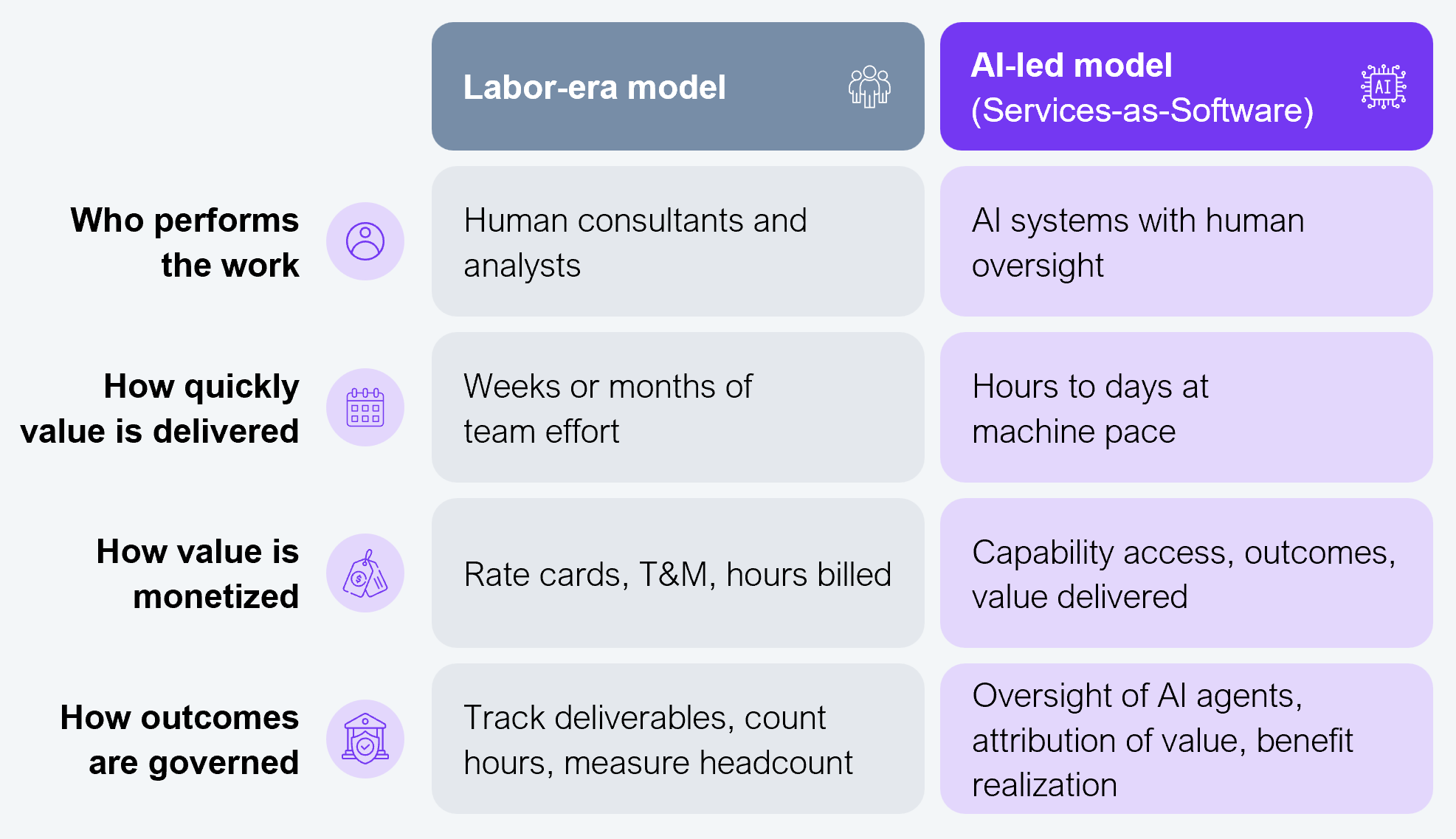

Professional services were built on one commercial assumption: effort was the clearest proxy for value. Team size, billable hours, and delivery timelines shaped how services were priced and governed because labor was the primary constraint on delivery capacity.

AI breaks that. AI-led delivery is a model in which AI systems perform the substantive work of a professional services engagement, i.e., the analysis, drafting, reasoning, and execution. On the other hand, human consultants focus on framing the problem, interpreting the results, and governing the outcomes (see Exhibit 1).

HFS Research describes this shift as Services-as-Software™, where the operating model of professional services moves from labor-intensive consulting toward software-mediated delivery. Work that once required large consulting teams can increasingly be completed with AI-enabled systems operating under fewer layers of human oversight. The problem is that enterprise sourcing models still largely evaluate services through labor-era logic.

Source: HFS Research, 2026

What this looks like in practice

A procurement leader at a global financial services firm receives a proposal for AI-led regulatory reporting. The provider submits familiar rate cards, consultant hours, delivery milestones, and an eight-member project team. In reality, the AI system will complete much of the analysis in hours, while the contract still prices for twelve weeks of human effort.

Neither side has a framework for what “fair” looks like once delivery is no longer primarily human-led. The provider is trying to protect labor-era revenue and margin structures, while the buyer struggles to determine whether they are paying for genuine outcomes or outdated effort-based pricing.

The deal defaults back to T&M because it feels commercially safer for both sides, even though the economics of delivery have fundamentally changed. The AI delivers. The commercial arrangement does not.

AI is changing what procurement even means. We don’t mind paying more if we can clearly see the ROI and how the value is being delivered.

— CFO, global financial services enterprise

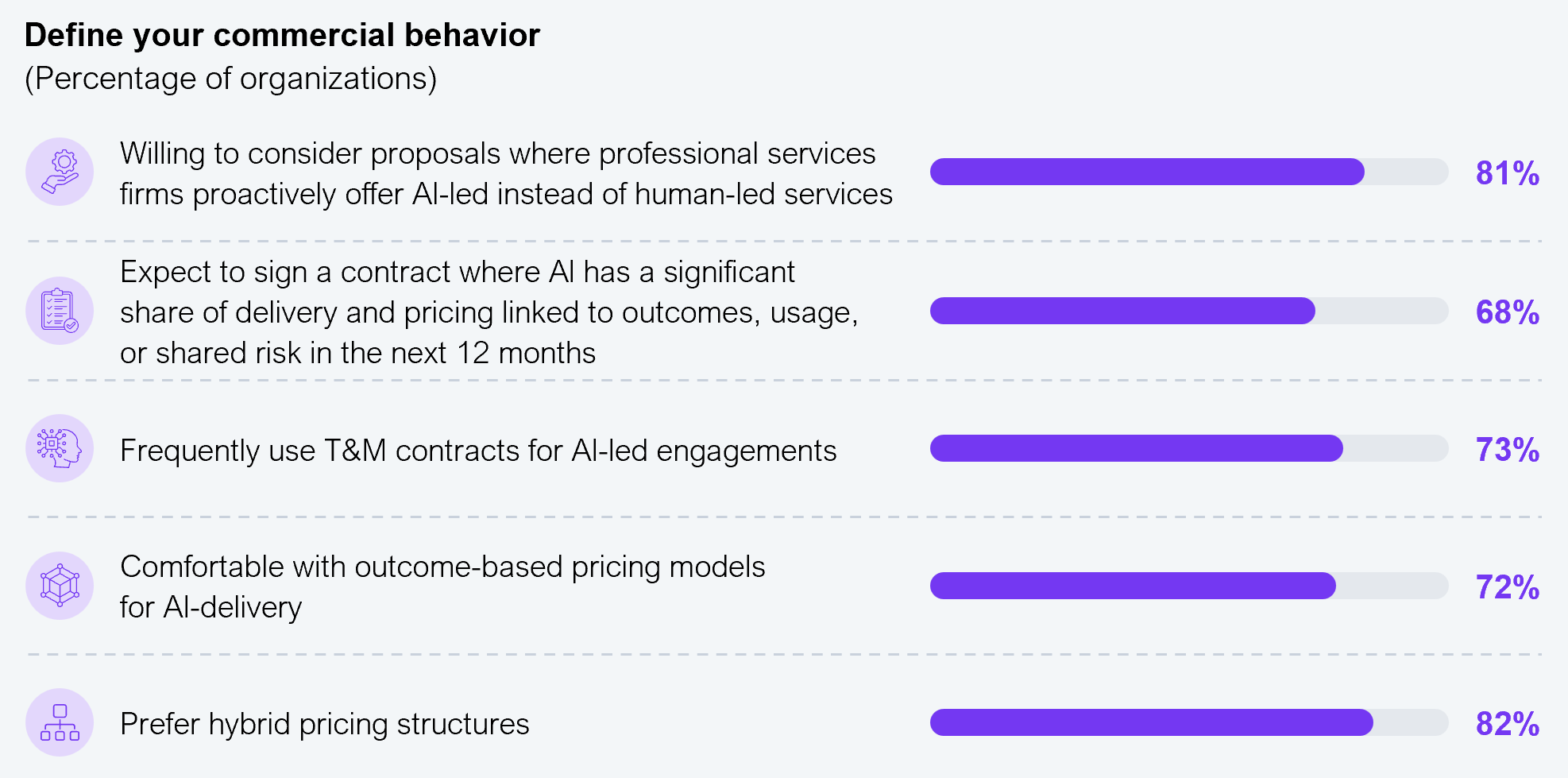

Enterprises are buying AI-led services, but with the old playbook

The disconnect is increasingly visible in enterprise buying behavior itself. Eighty-one percent of enterprises say they are willing to consider AI-led proposals, and 68% expect to sign outcome-linked AI contracts within the next 12 months. Yet traditional T&M contracts remain deeply embedded across enterprise sourcing models, even as buyers express growing comfort with hybrid pricing (blends a fixed fee with outcome- or usage-based components) and outcome-based pricing structures (see Exhibit 2).

Sample size: n=304, Global 2000

Source: HFS Research, 2026

The friction is not that buyers distrust AI-led delivery. It is that labor-era contracts gave them something to benchmark (rate cards, staffing assumptions, delivery effort), and AI-led delivery does not have the same mechanism.

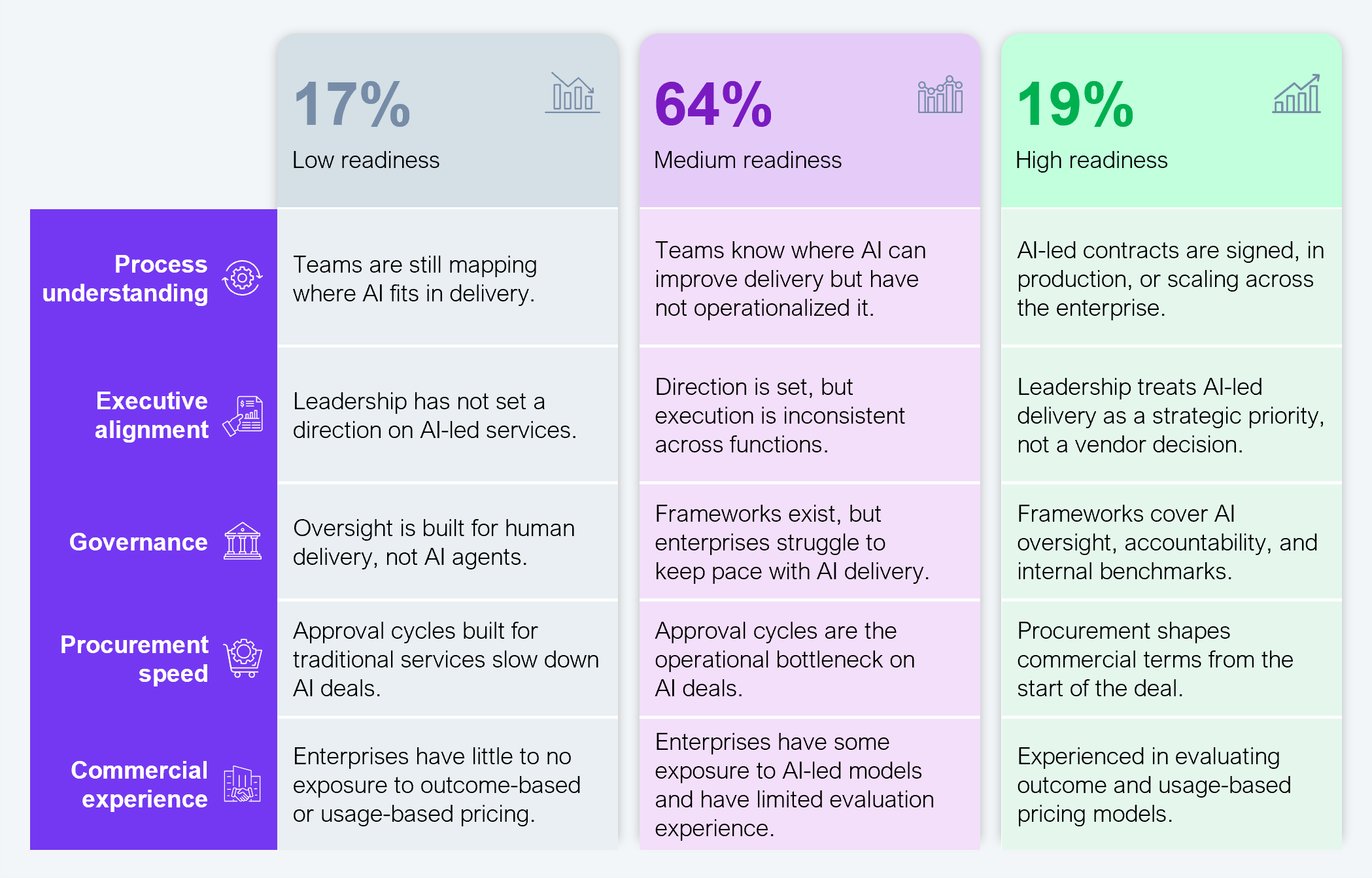

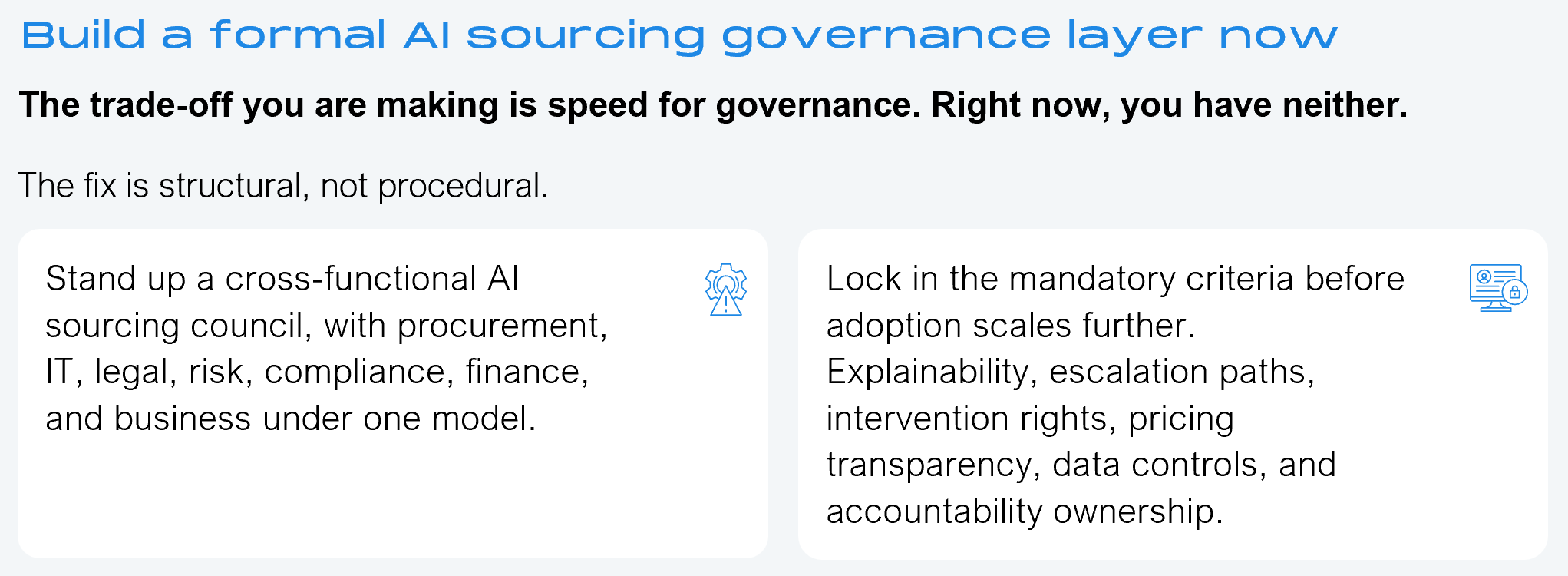

Most enterprises are stuck between yesterday’s governance and today’s delivery

Only 19% of enterprises have redesigned procurement, governance, and commercial structures to support AI-led delivery at scale. The other 81% are running AI deals through sourcing models built for labor (see Exhibit 3).

Sample size: n=304, Global 2000

Source: HFS Research, 2026

The gap is not a pricing problem waiting for a pricing fix. It is a governance and operating model problem that pricing alone will not solve.

Knowing the labor model is wrong is the easy part. Deciding what replaces it is where every AI deal now hits friction. Faster execution, smaller teams, and software-mediated workflows have broken the link between hours billed and value delivered. Nothing has taken its place.

What remains unresolved is how the economic upside from AI should be shared. Organizations increasingly expect AI-driven efficiency gains reflected in pricing, while providers still want upside tied to innovation, execution performance, and new capability creation. The result is a market operating between two economic models at once: one built around labor visibility and the other still being negotiated in real time.

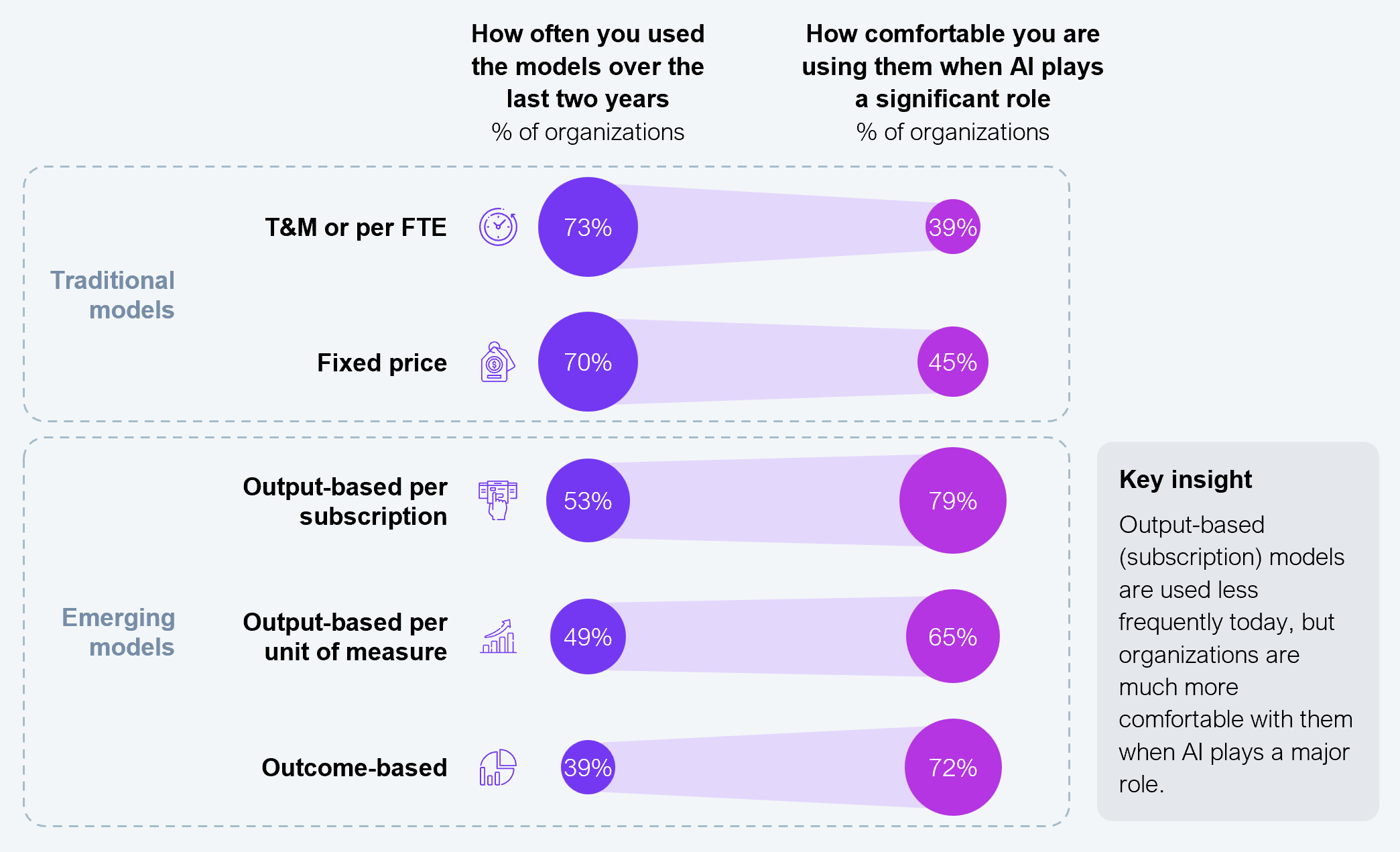

The old pricing model no longer fits AI-led delivery

Traditional pricing structures still dominate most service engagements today. T&M and fixed-price contracts remain operational defaults across much of the market, while outcome-based pricing continues to see lower real-world adoption.

At the same time, comfort with AI-native pricing models has advanced far beyond current usage patterns. Subscription-, output-, and outcome-based commercial structures all receive substantially stronger support when AI plays a major role in delivery (see Exhibit 4).

Sample size: n=304, Global 2000

Source: HFS Research, 2026

AI should be more efficient, but pricing rarely shows where the efficiency goes.

— VP Procurement, global industrial manufacturer

Seventy-four percent of buyers now expect AI-led services to cost less; it’s time for pricing structures to catch up

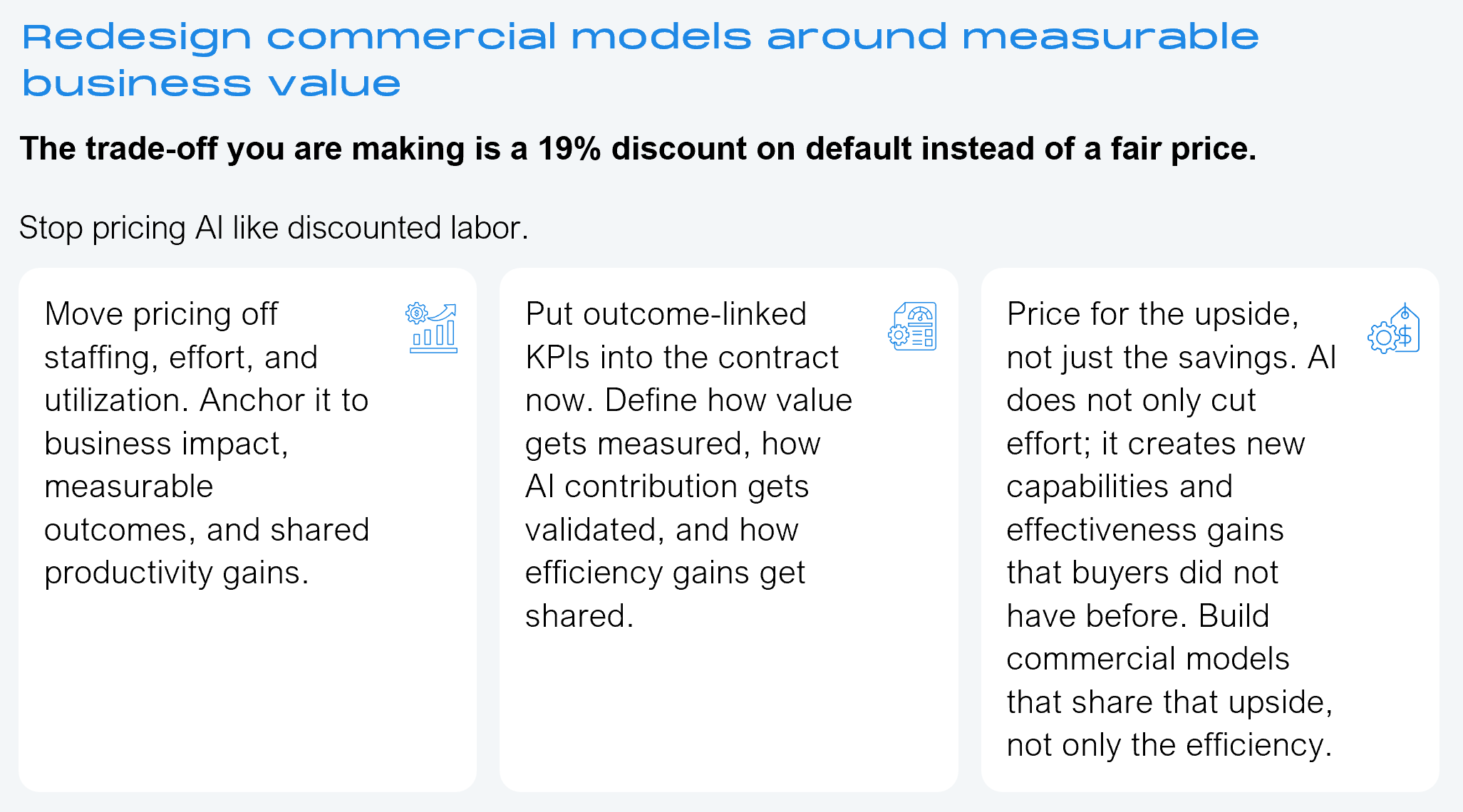

Once delivery becomes less dependent on large pools of human effort, pricing expectations begin to shift quickly. Most organizations now expect AI-led professional services to cost materially less than human-led equivalents. Roughly 40% expect pricing reductions of 10% to 30%, while another 34% expect more than 30%. Average expected pricing declines now approach 20% (see Exhibit 5).

What this looks like in the room: a sourcing lead at a North American bank opens an AI-led advisory proposal and finds the same rate card that came in last year, even though the provider’s own pitch deck acknowledges three pages later that AI is doing the modeling overnight. The sourcing lead sends it back. Two weeks later, the provider returns with a different number. Nothing in the work has changed, only how it was priced. That kind of pushback is starting to define how AI-led proposals get evaluated.

Sample size: n=304, Global 2000

Source: HFS Research, 2026

These expectations create growing pressure on commercial models built around labor expansion and utilization-based pricing. As AI compresses delivery effort, organizations increasingly expect service economics to compress alongside it.

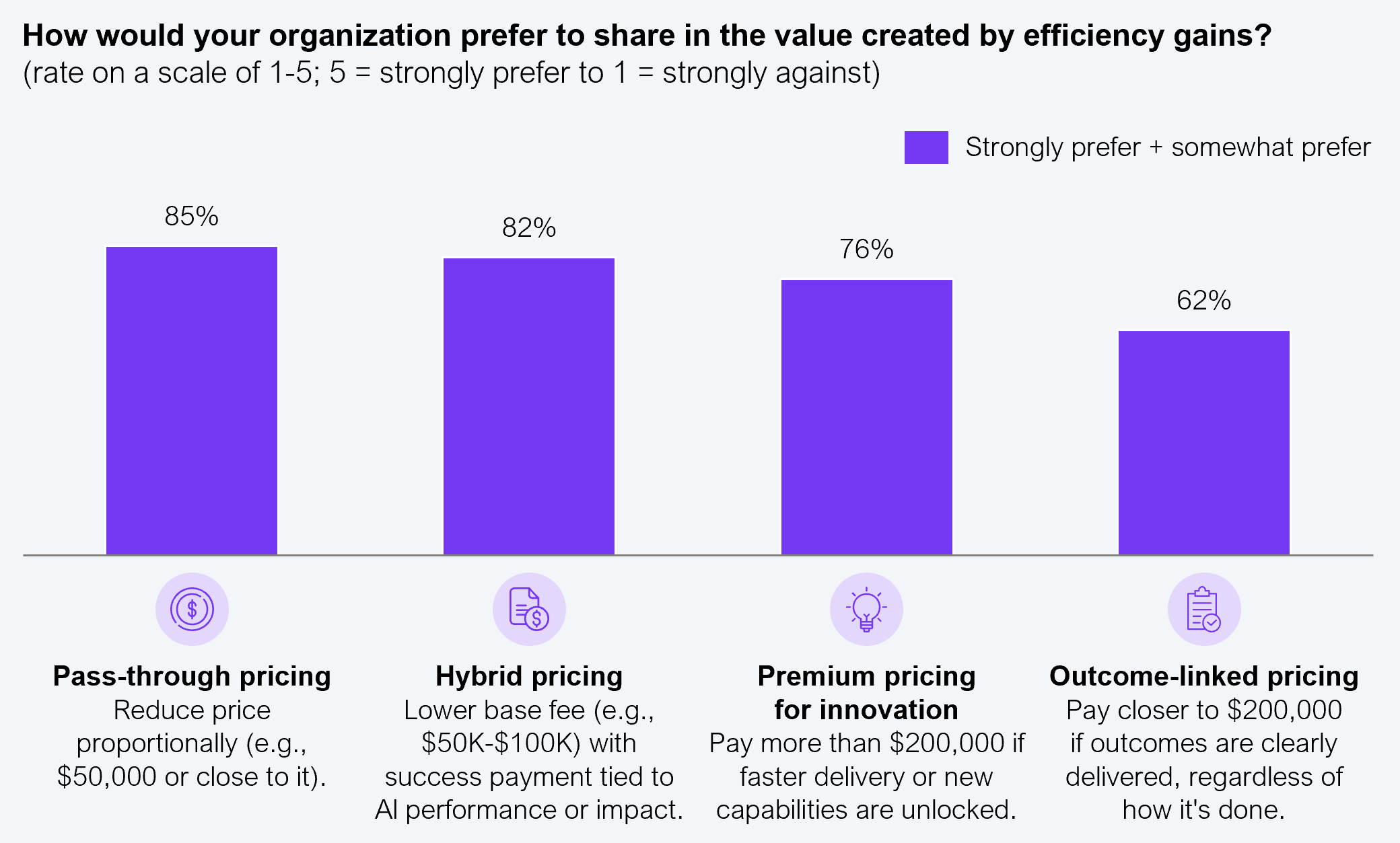

Nobody has agreed what AI is worth, and every contract is paying the price

AI is changing the economics of service delivery. The market has not agreed on how those gains get priced, shared, or justified.

Buyers back pass-through pricing, hybrid structures, and premium pricing when AI improves business outcomes. They also back outcome-linked pricing, even though no one has settled on how AI-generated value should be measured (see Exhibit 6).

Sample size: n=304, Global 2000

Source: HFS Research, 2026

Buyers are not simply demanding cheaper services, even though their backing for pass-through pricing shows they expect AI efficiency to be reflected in cost. They are demanding new economic rules.

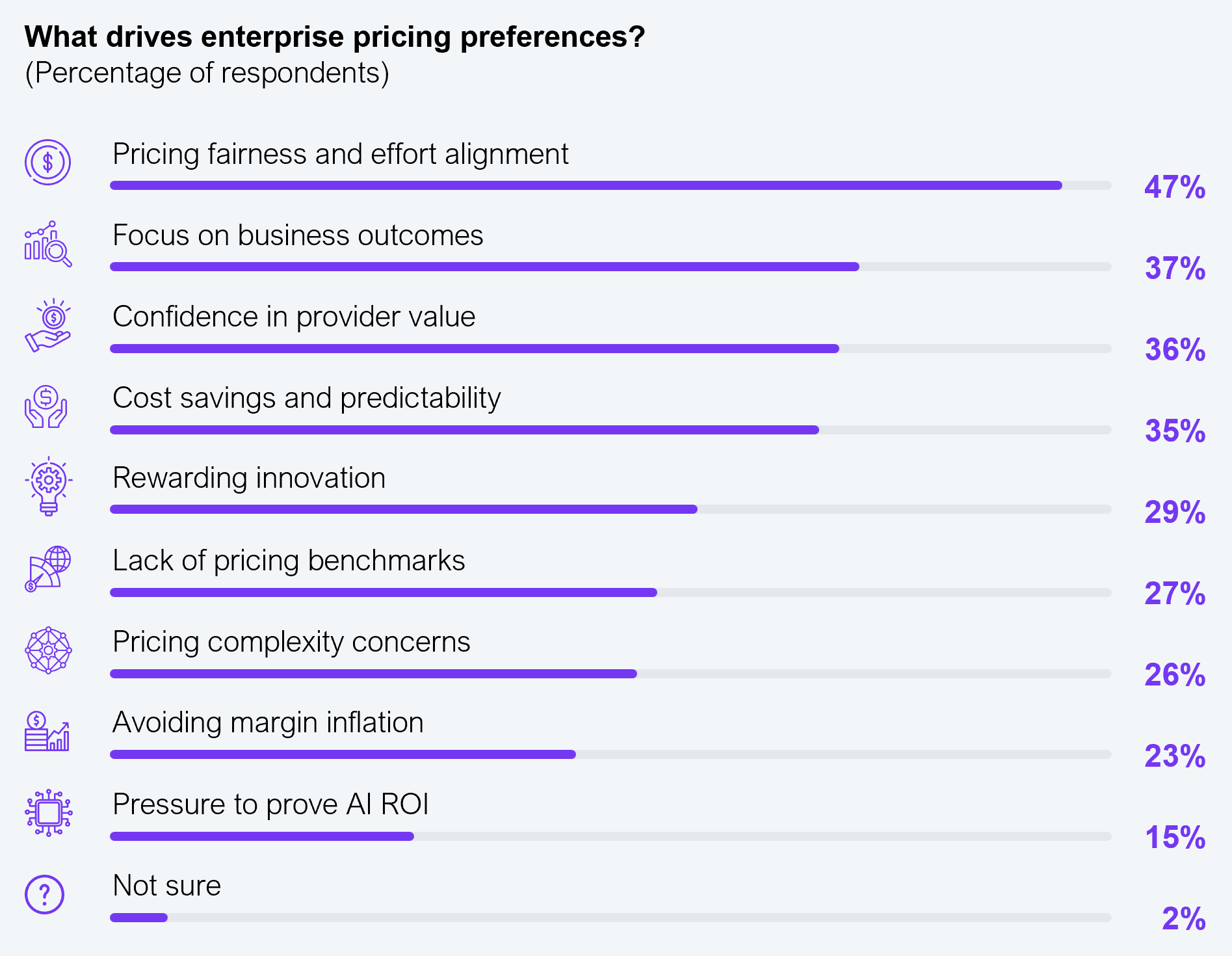

What matters is whether the pricing is commercially justified. That becomes clearer when organizations explain what drives their commercial preferences. Pricing fairness and alignment with effort rank highest overall, followed closely by business outcomes, confidence in provider value delivery, and cost predictability (see Exhibit 7).

Sample size: n=304, Global 2000

Source: HFS Research, 2026

Outcome pricing sounds great, until no one agrees on what success looks like.

— Strategic Sourcing Lead, global financial services enterprise

The market is not rejecting premium or outcome-based pricing. It is trying to define fair exchange when delivery is no longer measured in human effort. That makes pricing discussions harder, not simpler. They now turn on value attribution, measurable outcomes, accountability, and shared upside, not staffing levels and billable hours.

We don’t mind paying more if we know exactly what’s human, what’s machine, and what’s shared.

— Head of Sourcing, global energy company

Fair pricing cannot be settled inside a procurement function alone. Once a contract defines how AI value is measured, where accountability sits, and which humans stay on the hook, the conversation stops being commercial and becomes governance. That is where most enterprises are exposed: they moved from sourcing AI-led services to deploying them. The governance to evaluate AI-led delivery across procurement, legal, IT, compliance, finance, and the business has not kept pace.

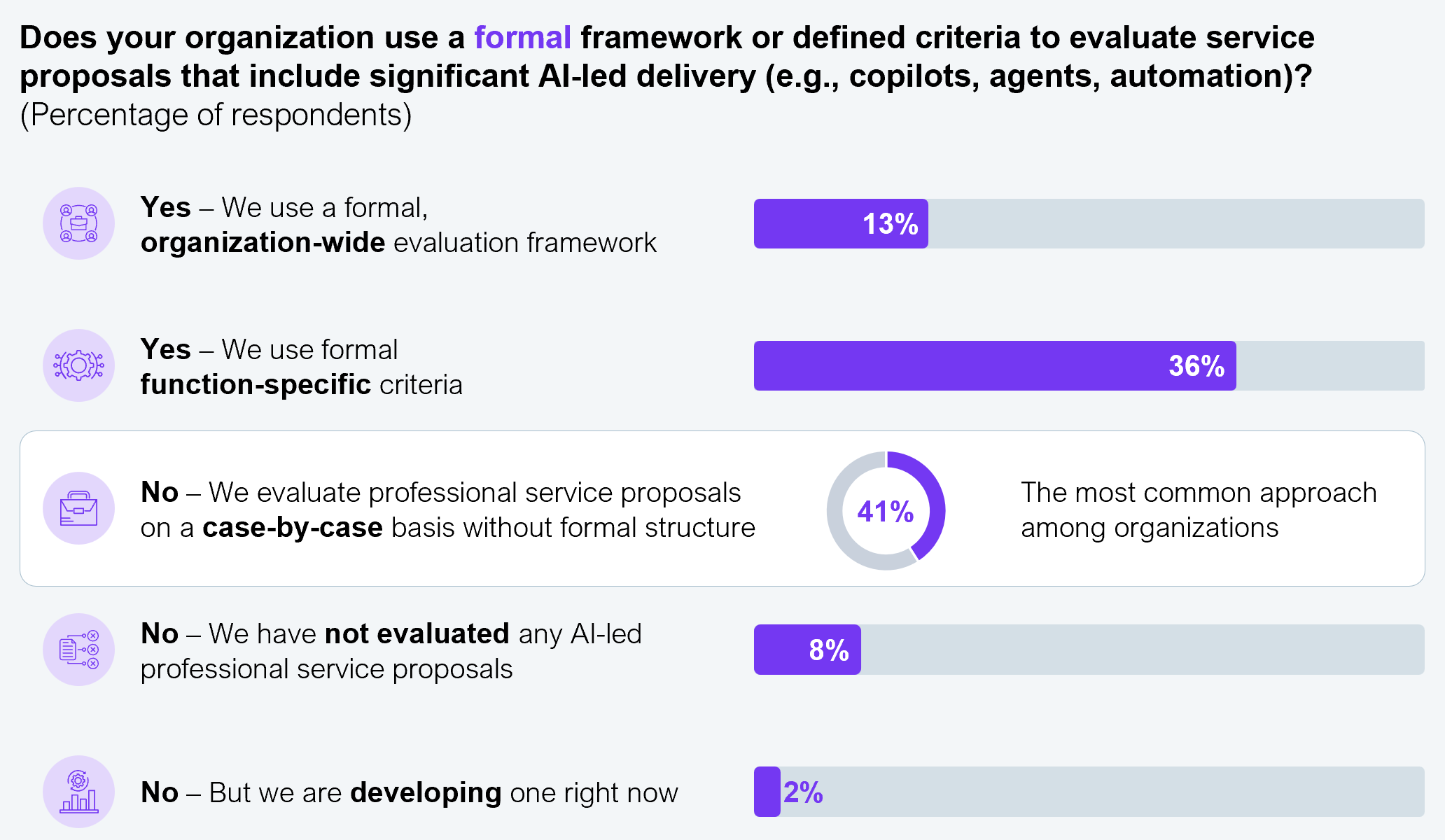

Most organizations still govern AI-led services case by case

Only 13% of organizations use a formal, enterprise-wide framework to evaluate AI-led professional services proposals. Most either rely on function-specific criteria or assess proposals on a case-by-case basis without formal governance structures (see Exhibit 8).

Sample size: n=304, Global 2000

Source: HFS Research, 2026

Organizations have moved quickly to evaluate and procure AI-led services, but far fewer have established consistent mechanisms for assessing, approving, and governing those engagements. That gap creates fragmented sourcing decisions, inconsistent accountability models, and uneven risk oversight across the enterprise.

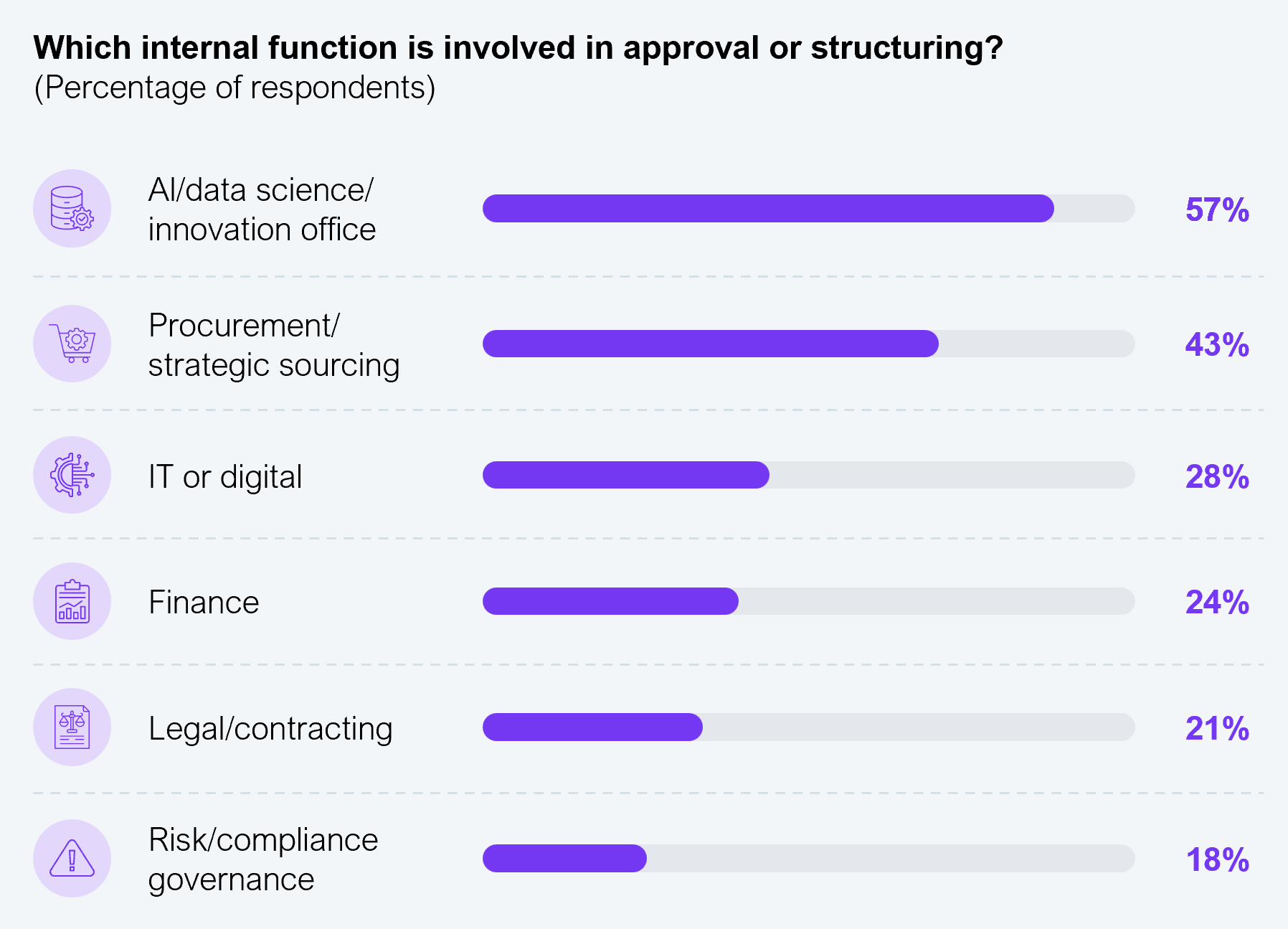

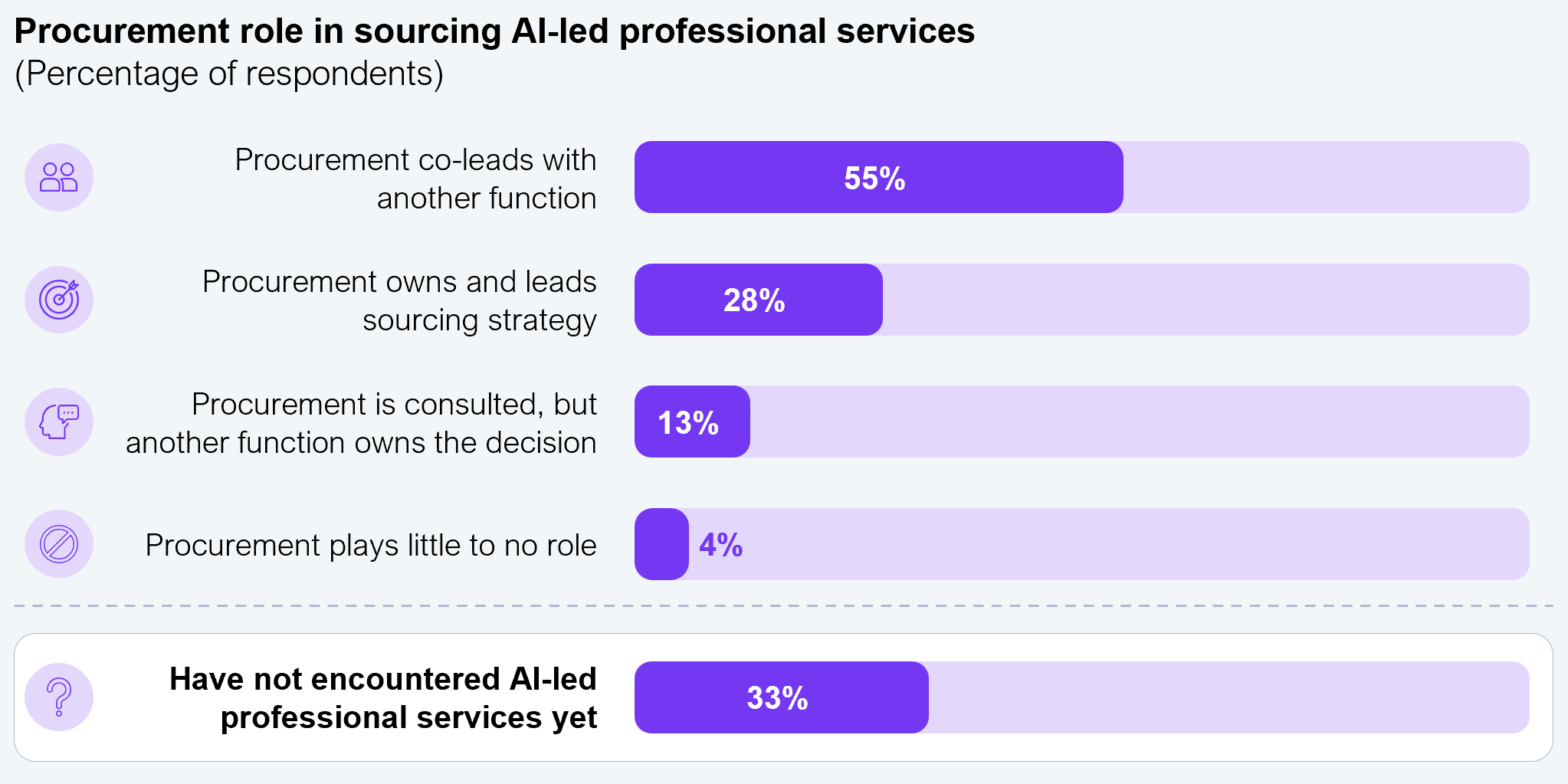

Procurement can no longer sign an AI deal alone, and the buying team has not caught up

Procurement alone cannot evaluate an AI-led deal anymore. Commercial structures, model behavior, operational risk, compliance, and accountability now cut across multiple functions in the same contract (see Exhibit 9).

Sample size: n=304, Global 2000

Source: HFS Research, 2026

In practice, procurement is already co-leading with IT, finance, legal, and risk on AI deals, even where the formal mandate has not caught up. Sourcing is collaborative by necessity: model accountability, intervention rights, compliance exposure, and operational oversight all sit in the contract, and none of them are pricing decisions (see Exhibit 10).

Sample size: n=304, Global 2000

Source: HFS Research, 2026

As AI moves deeper into service delivery, sourcing decisions look more like governance exercises than procurement events.

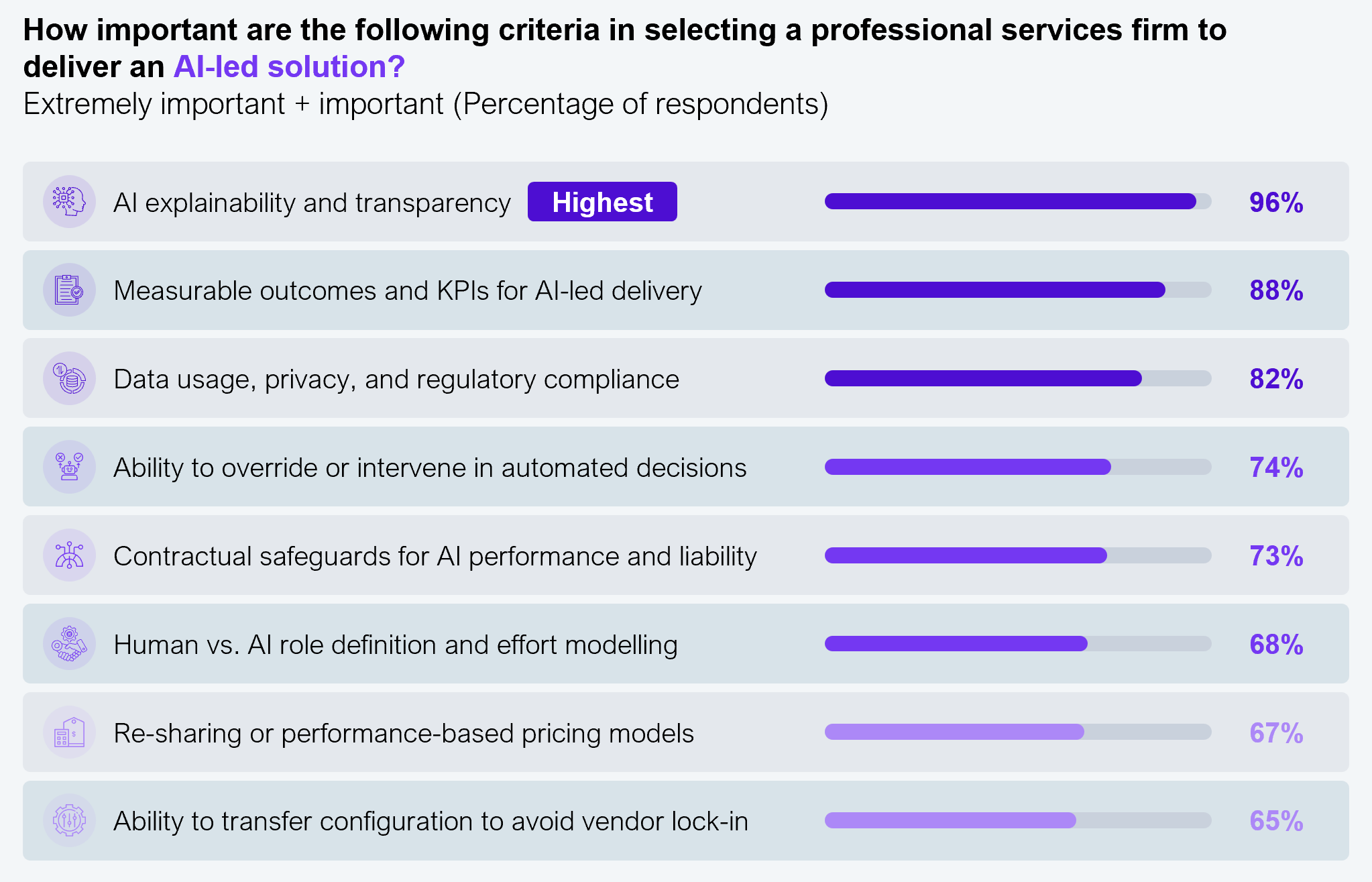

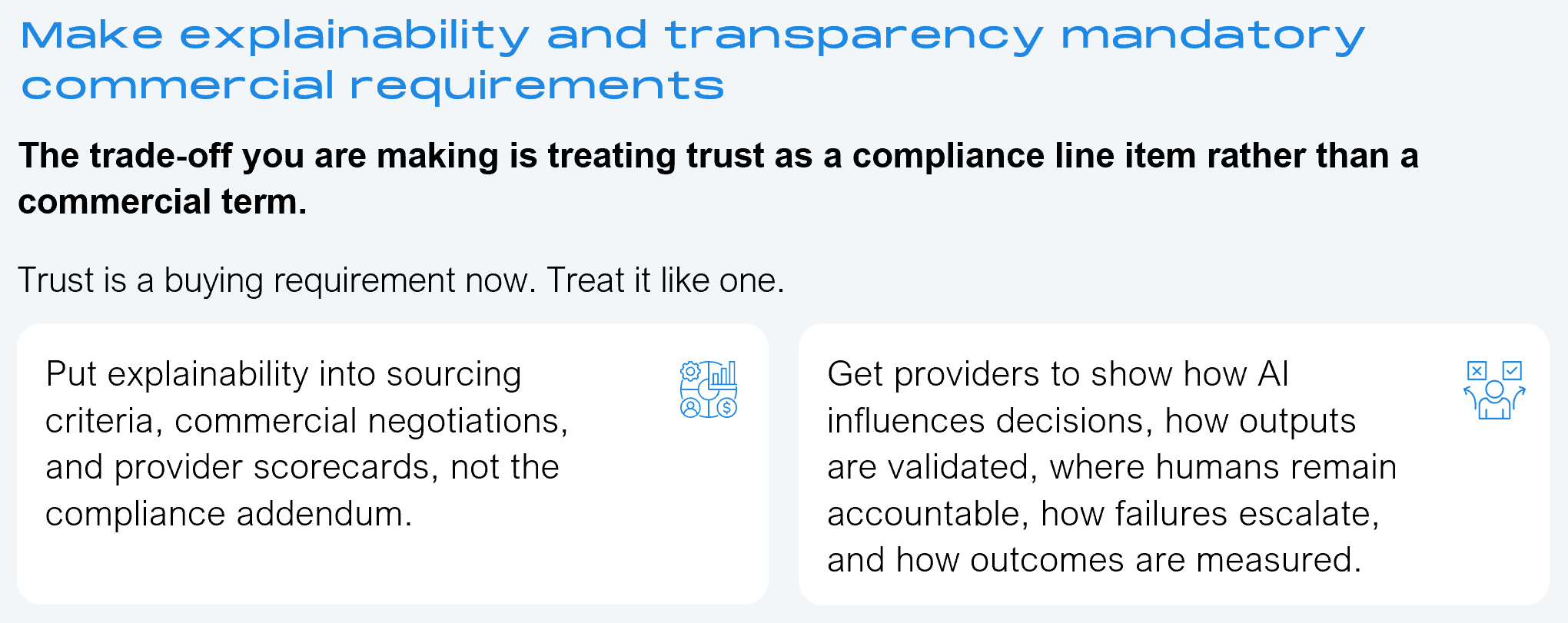

Ninety-six percent of buyers rank explainability as a top selection criterion

As AI-led services move from experimentation into active sourcing, trust is no longer a governance consideration sitting behind the contract. It is part of the commercial decision itself.

AI explainability and transparency now rank as the single most important factor in selecting AI-led providers, followed closely by measurable outcomes, regulatory compliance, intervention rights, and contractual safeguards (see Exhibit 11). The selection moment increasingly turns on it. What separates the providers is whether each one can show on a single page how a model decision moves through their delivery process, where the human signs, and what gets logged for the auditor. For example, two providers can and two cannot. The shortlist writes itself. That kind of single-page test is starting to replace longer technical evaluations as the moment AI-led decisions actually

get made.

We’d pay a premium for partners who make compliance invisible.

— Chief Risk Officer, global banking enterprise

Sample size: n=304, Global 2000

Source: HFS Research, 2026

Explainability alone is not enough once AI is embedded in delivery and commercial models that pay on outcomes.

Buyers need to see the math, the metrics, and the guardrails to sign confidently

As AI-linked engagements get bigger, confidence depends on whether the provider can show how value is measured, how accountability is shared, how pricing aligns to outcomes, and where human oversight remains visible. Buyers are not asking whether AI works. They are asking whether AI-led delivery can be governed, trusted, and priced on terms that make sense as it scales (see Exhibit 12).

Sample size: n=304, Global 2000

Source: HFS Research survey data, 2024

That has changed how providers get evaluated. Technical capability is no longer enough. Buyers prioritize providers that operationalize trust through transparent metrics, clear AI-human accountability boundaries, measurable outcomes, governance safeguards, and commercially understandable delivery models (see Exhibit 13).

Sample size: n=304, Global 2000

Source: HFS Research, 2026

We sign faster when we can see the math, the metrics, and the guardrails.

— Head of Strategic Sourcing, global banking group

Most procurement organizations are running operating models built for labor-heavy services in an AI-led market. The next phase of advantage will not come from buying more AI. It will come from redesigning how AI is bought to ensure it delivers on its promise. Five moves will separate the procurement teams that will be ready from the ones that will not.

Move 01

Move 02

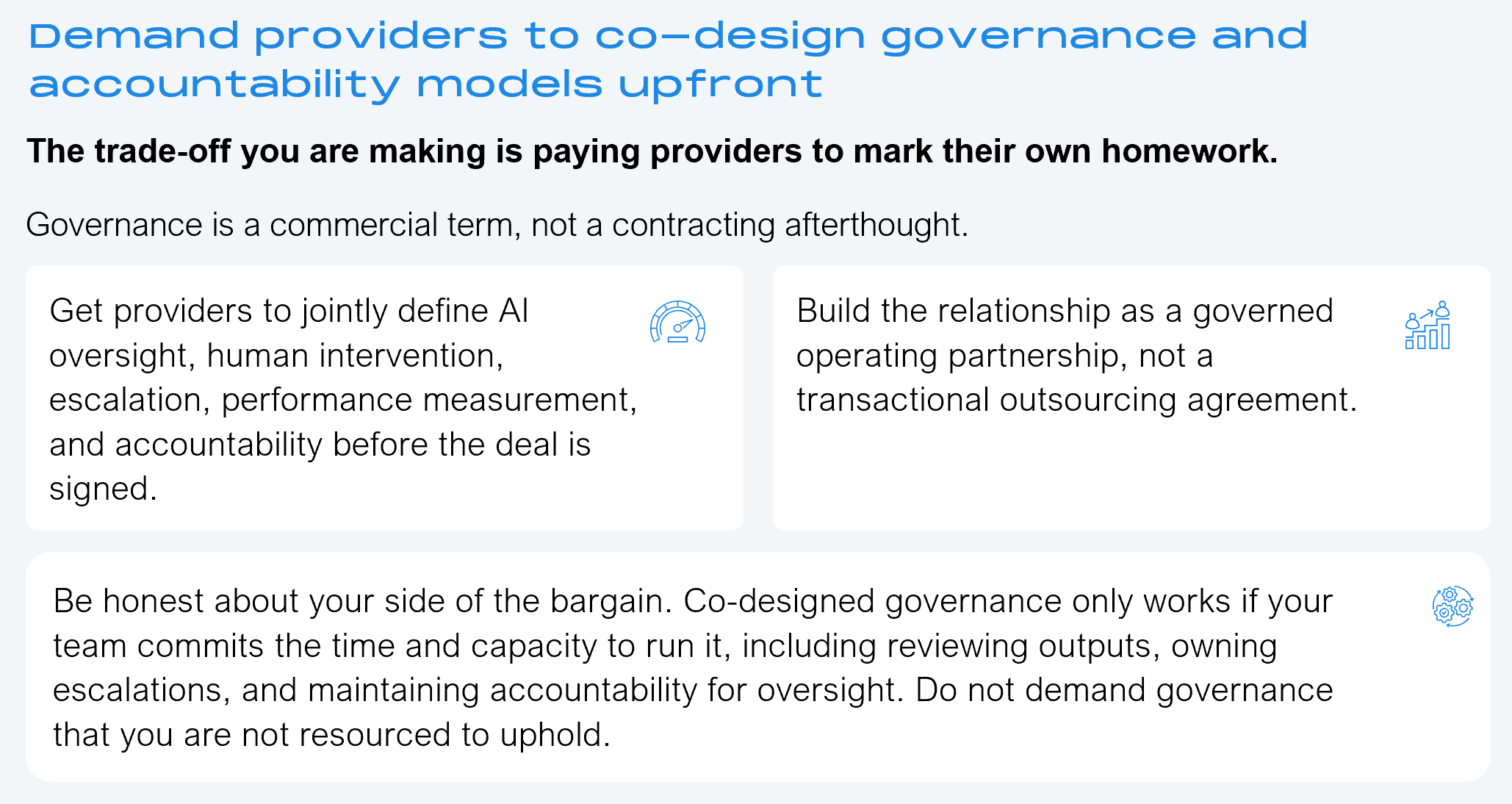

Move 03

Move 04

Move 05

The five moves above are not a checklist. They are the minimum operating model for buying AI-led services without absorbing the risk that the contract no longer prices. Procurement teams that make them will spend the next 18 months building governance, commercial logic, and workforce design fit for AI-led delivery. The teams that do not will spend the same 18 months signing contracts they cannot price, govern, or defend, discovering that risk one deal at a time.

Register now for immediate access of HFS' research, data and forward looking trends.

Get StartedIf you don't have an account, Register here |

With the exception of our Horizons reports, most of our research is available for free on our website. Sign up for a free account and start realizing the power of insights now.

Our premium subscription gives enterprise clients access to our complete library of proprietary research, direct access to our industry analysts, and other benefits.

Contact us at [email protected] for more information on premium access.