This Take 5 report is for commerce, marketing, and digital leaders assessing how ready their retail, CPG, or travel and hospitality enterprise is for agent-mediated commerce.

Executive summary

Agentic commerce is a control inversion for ecommerce and digital leaders. Fifty-nine percent of retail, consumer products and goods (CPG), and travel and hospitality enterprises run less than 5% of direct consumer revenue through AI agent-mediated channels today. Yet the same share expects at least 15% over the next two years. The shift is coming faster than the infrastructure needed to support that, and brands see the threat clearly. Seventy-eight percent say first-party data and a direct consumer relationship will matter more in an agent-mediated world, but only 37% have a credible plan to keep that relationship when an agent sits in the middle of the transaction. Despite that, enterprises are continuing to fund the storefront while starving the execution foundation, with identity, authentication, and fraud as the top barrier drawing the least investment.

HFS Research, in partnership with Cognizant, surveyed 101 senior commerce, marketing, and digital leaders across retail, CPG, and travel and hospitality in the US and Canada to map how ready enterprises are for the shift to agent-mediated commerce.

The survey uncovered five key takeaways:

-

-

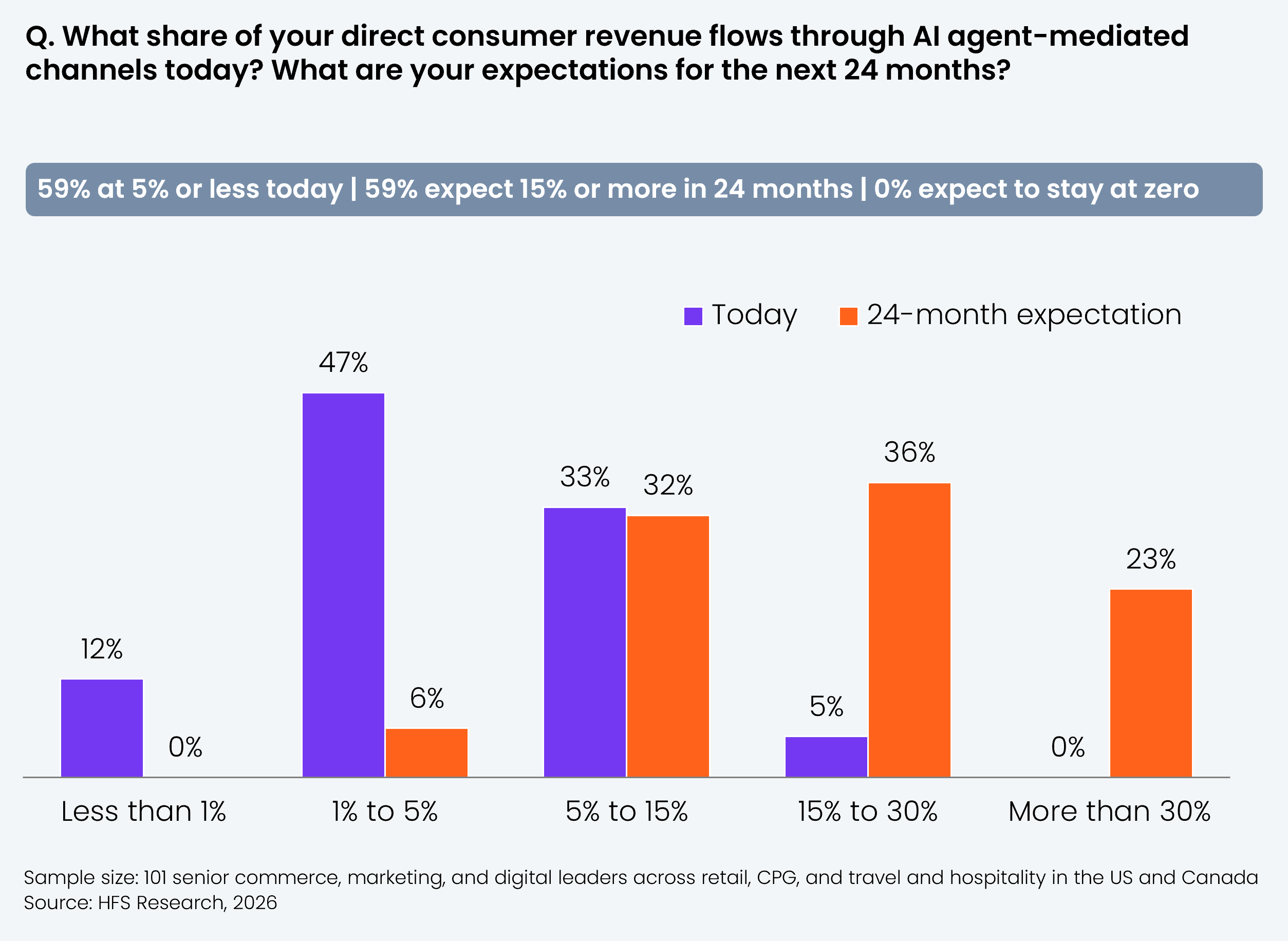

Agent-mediated revenue triples within 24 months, and not one enterprise expects to stay at zero

Fifty-nine percent run 5% or less of consumer revenue through agents today, but the same share expect at least 15% within two years. No one expects to stay at zero.

-

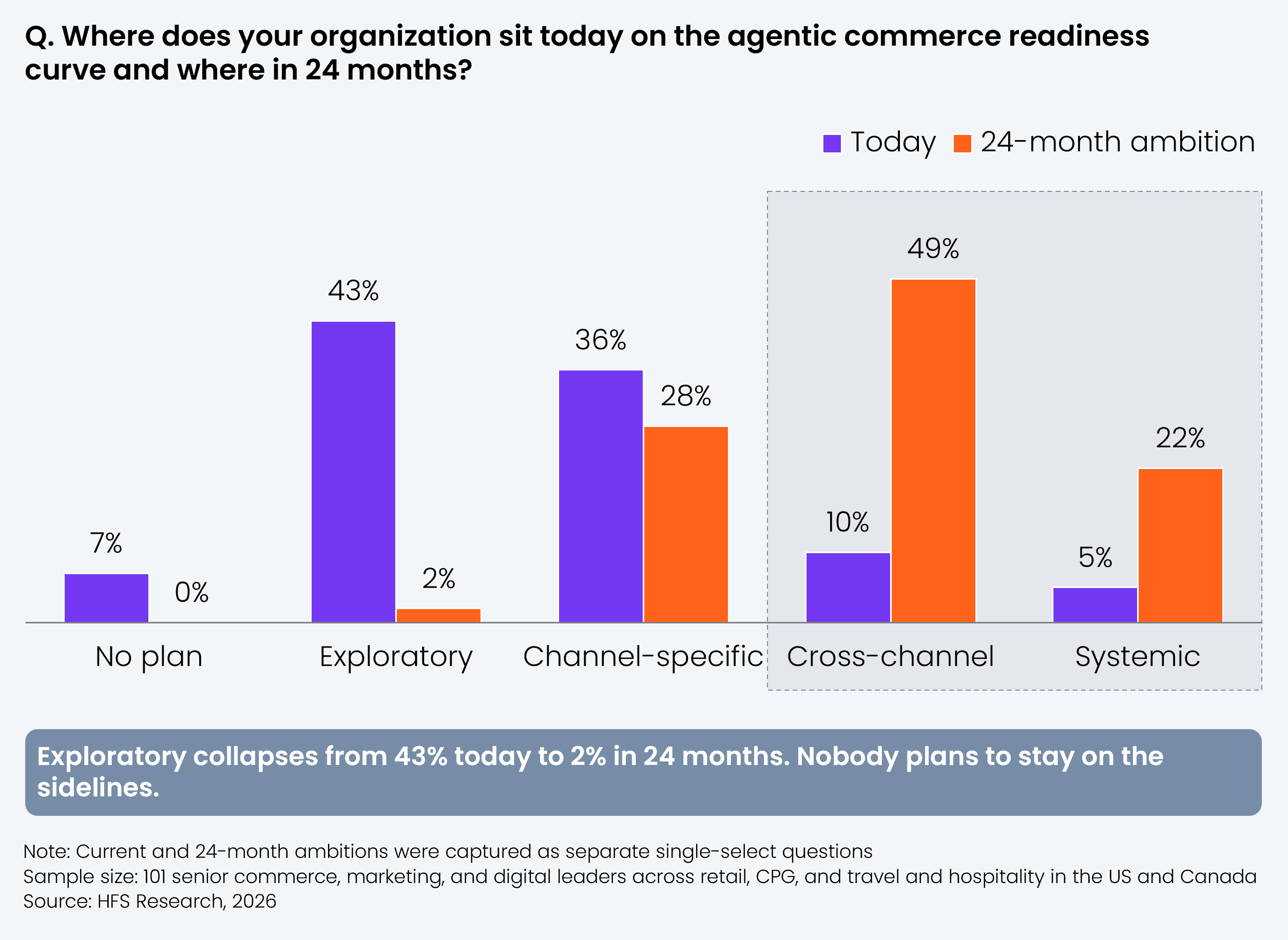

Only 15% are cross-channel or systemic today, but 71% intend to be within 24 months, a near-fivefold leap

The current, single-channel pilot playbook cannot bridge this gap.

-

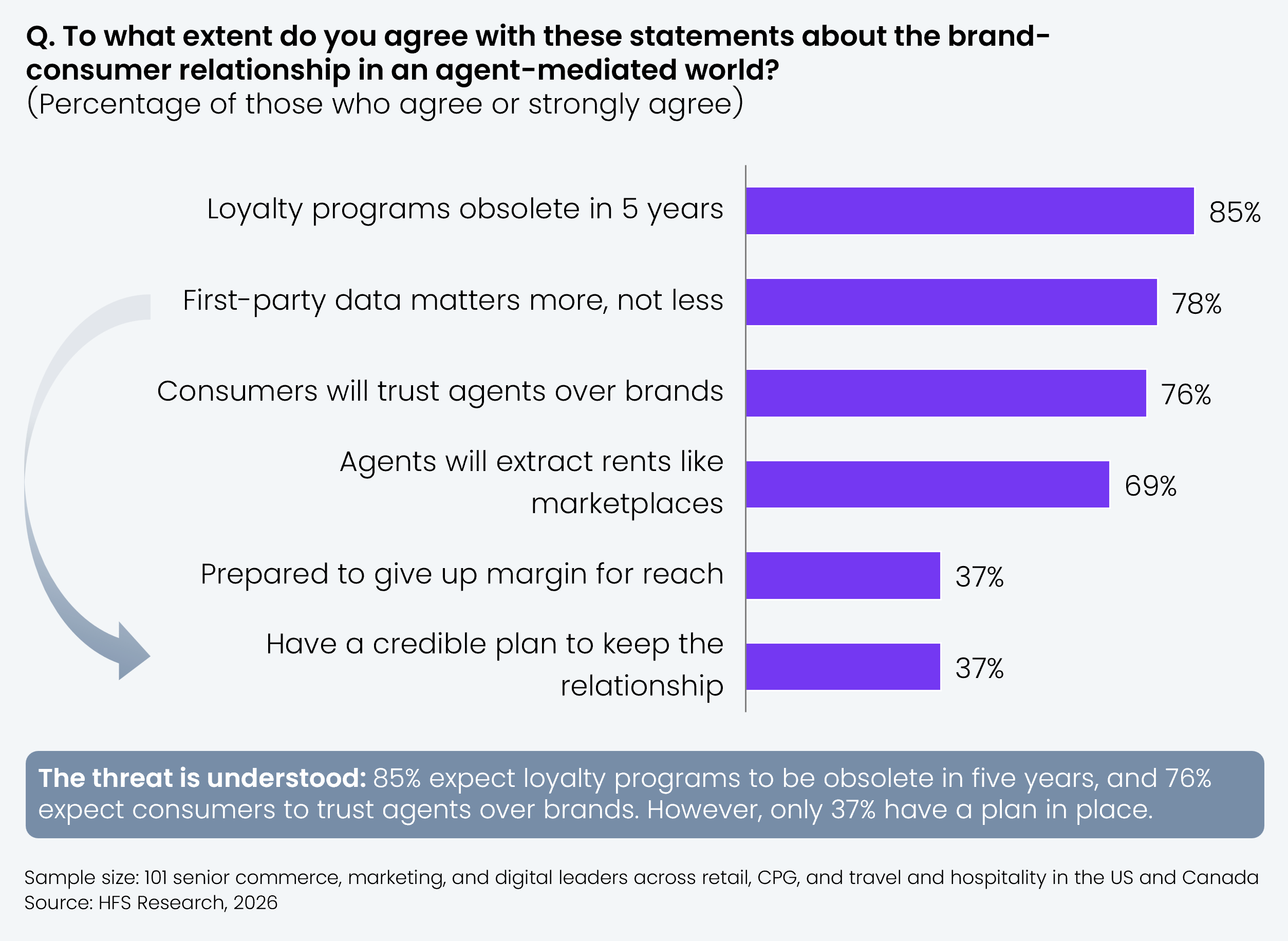

Seventy-eight percent say first-party data matters more in an agent world, yet only 37% have a credible plan

This points to a 41-point gap. Brands see the customer-relationship threat but have no answer.

-

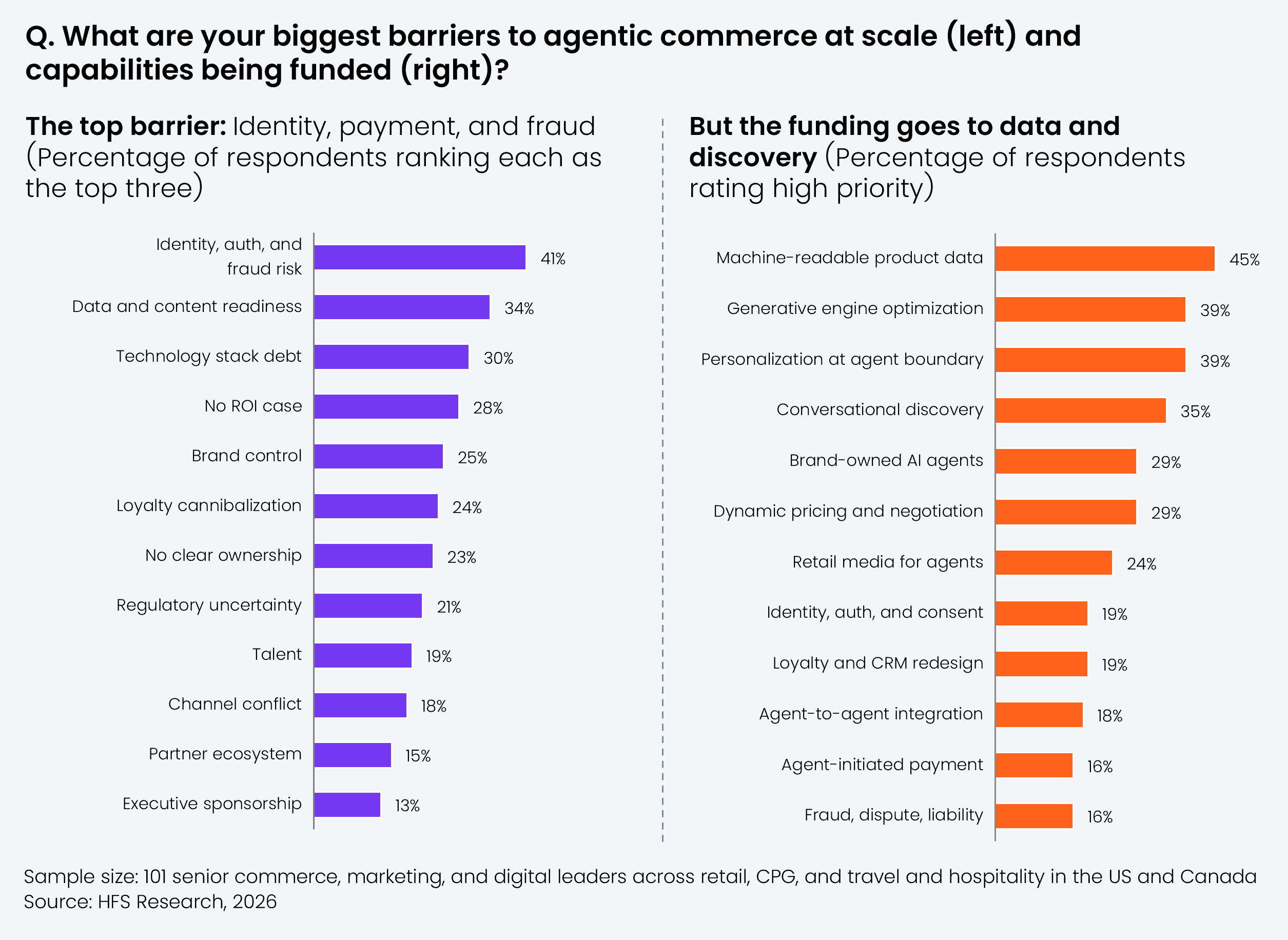

Enterprises are funding the storefront but underinvesting in the very capability they consider the greatest barrier to scaling agentic commerce

Identity, authentication, and fraud is the top barrier (41%), yet ranks last in the investment priority bucket. The plumbing remains unbuilt.

-

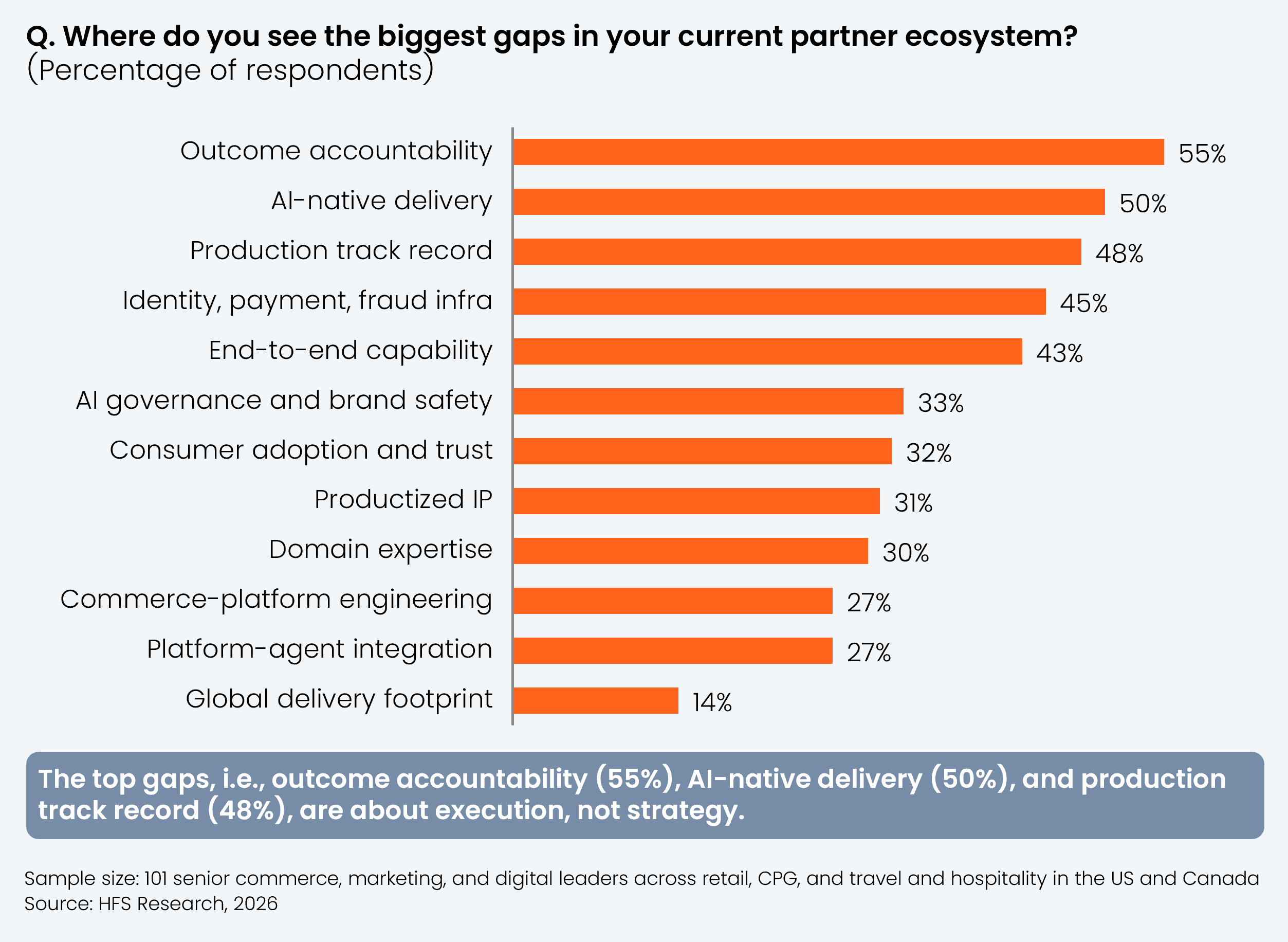

The partner ecosystem fails on outcomes and production, which buyers say require maximum retrospection

The biggest partner gaps are outcome accountability (55%), AI-native delivery (50%), and a production track record (48%). Buyers want doers, not slideware builders.

The Bottom Line: Your customer is about to be intermediated by an agent you do not control. Build the foundation, identity, payment, trust, and first-party data before the front end and treat the agent as a new buyer.

- Today 59% of enterprises run 5% or less of their direct consumer revenue through AI agent-mediated channels, and 12% run essentially none. Agentic commerce is still a rounding error on most P&Ls.

- However, the 24-month expectation is a totally different world. Fifty-nine percent expect at least 15% of consumer revenue to flow through agents within two years, and 23% expect more than 30%. The share running 5% or less collapses from 59% to 6%.

- Not a single respondent expects to stay at essentially zero. The direction of travel is uni-directional, even as most enterprises have built almost no infrastructure to capture it.

We have guests who have stayed with us dozens of times and still check in as strangers because they booked through an agent with a different identity.

— Head of Digital at a global hotel group

- Today the market sits early on the curve. Forty-three percent are still at the exploratory stage of one or two isolated pilots, and 36% have channel-specific programs. Only 15% have reached cross-channel or systemic, where agentic commerce is an integrated strategy with dedicated ownership.

- The 24-month ambition is a different curve entirely. Seventy-one percent intend to be cross-channel or systemic, and the exploratory stage would just empty out, falling from 43% to 2%. Nobody plans to be sitting on the sidelines.

- The leap from 15% to 71% cannot be reached by stitching together more single-channel pilots. Systemic agentic commerce demands orchestration, identity, and payment infrastructure that almost no enterprise has built.

We do not own checkout anyway, so being the brand the agent recommends is the whole game for us now.

— VP, eCommerce, at a specialty retailer

- Enterprises see the control inversion coming. Seventy-eight percent agree that first-party data and a direct consumer relationship will matter more in an agent-mediated world. Sixty-nine percent expect agent platforms to extract economic rents from their category the way marketplaces already do.

- They also see the relationship being severed. Eighty-five percent believe loyalty programs will be obsolete within five years, and 76% believe consumers will trust their agent over the brand.

- Yet only 37% have a credible plan to keep the direct relationship. The 41-point gap between seeing the threat and having an answer is the single most important finding in this study.

A customer rebooking is effectively a stranger to the agent handling the call, because the full picture of who they are sits with the intermediary, not with us.

— Director of Customer Experience at a travel intermediary

- The top barrier is foundation, with identity, authentication, and fraud risk cited by 41% of enterprises. Data and content readiness (34%) and technology stack debt (30%) follow close behind.

- But the foundation is starved as the money is going elsewhere. The most-funded capabilities are front-of-house: machine-readable product data (45%; high priority), generative engine optimization (39%), and personalization at the agent boundary (39%). Enterprises are investing in being found and how are they being shown.

- Budget and executive sponsorship sit at the bottom of the barrier list at 13%. The money and the mandate are there.

- The contradiction is self-inflicted. A discoverable, personalized agent experience that cannot verify the agent, settle the payment, or contain the fraud is a demo, not a business.

- When enterprises look for help building agentic commerce, the partner ecosystem disappoints on key execution capabilities.

- The biggest gaps are outcome accountability (55%), AI-native delivery (50%), and a proven production track record (48%), the three things where buyers see the biggest gap.

- Identity, payment, and fraud infrastructure (45%) and end-to-end capability (43%) round out the top five gaps. The pattern is clear: the ecosystem is built to advise on agentic commerce, not to ship it. Only 4% of enterprises say their partners have no significant gaps.

Invest in agent-accessible content infrastructure. Prioritize structured data an AI agent can actually consume and trust, not just better images and descriptions for humans.

— VP, Digital Commerce, at a CPG manufacturer

The Bottom Line: Your customer is about to be intermediated by an agent you do not control. Build the foundation, identity, payment, trust, and first-party data before the front end and treat the agent as a new buyer.

-

Fund the foundation, not just the storefront

Identity, payment, and fraud is the number one barrier (41%) yet the least-funded capability. Redirect investment from discovery features to the agent-ready plumbing that makes any of it transactable. A discoverable experience that cannot verify the agent or settle the payment doesn’t hold any business value.

Own the customer relationship before the agent takes it

Seventy-eight percent say first-party data will matter more in an agent world, but only 37% have a credible plan to keep the relationship. Close this 41-point gap now. Build the preference graph, identity spine, and direct value exchange that survive when an agent sits in the middle of every transaction.

Demand partners who ship, not partners who advise

The biggest partner gaps are outcome accountability (55%), AI-native delivery (50%), and a production track record (48%). When evaluating partners, the test is whether they will be measured on revenue and conversion and have executed agentic commerce at scale, not whether they can present a strategy for it.