The world of finance and account business process services is poised to take a very different direction as labor arbitrage solutions are replaced by a combination of platforms, automation, AI, and ultimately blockchain. As one generation of services grinds to a halt, another is quickly ramping up to drive what we at HfS are calling F&A 3.0.

Simply put, the new direction has arrived and those who ignore it will quickly be left behind in a world where legacy business practices are no longer tolerated. Nearly every enterprise today has a focus on operating as a digital business with an appointed Chief Digital Officer and the data being controlled from finance is of paramount importance to support these business models. Hence, the pressure on CFOs to ditch legacy practices such as labor arbitrage driven F&A is reaching a critical juncture.

Third-party Finance & Accounting (F&A) Services have delivered considerable operational cost reduction for the Global 2000 over the last 20 years, ever since BP decided to outsource some of its F&A transactional activities to PwC and Accenture in the mid-nineties and helped create a brand new market segment. Primarily driven by competent offshore labor models and a proven capability to standardize processes, F&A services have thrived for more than two decades, alongside the success of offshore centric IT services.

Multi-process F&A BPO[1], as it became known, survived the heady rise and crash of multi-process HR outsourcing; it was always the bellwether for BPO growth as procurement services struggled to get real traction and call center services failed to get beyond basic voice work and labor arbitrage. However, despite its robust growth, even legacy F&A BPO has reached its saturation point, as most major enterprises have enjoyed all the low hanging fruit on offer from profitable, manageable F&A labor arbitrage and increasing numbers of them have figured out how to move more work into their GICs and make further cost benefits without ceding more control to third parties.

Multi-process F&A services have now matured to an $8 billion market. The growth has been driven by an offshore-centric model where enterprises can significantly drive down operational costs by leveraging a large base of accounting talent available in lower cost geographies, thereby helping the retained F&A team to focus on more core and strategic activities. However, the F&A market has struggled (despite trying very hard!) to offer a value proposition beyond cost reduction over its twenty-odd years of existence. All indicators of demand and supply suggest that this is about to change. Third-party F&A services are ripe for disruption.

Market Indicators That Suggest F&A Services Are About to Get Disrupted

CFOs Are No Longer Focused on Just Cost-Reduction

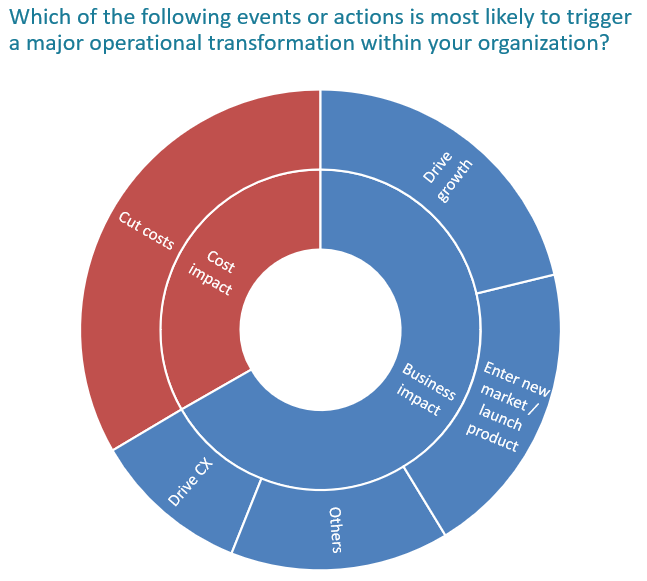

In 2017, we interviewed 75 senior finance executives in a joint study with Accenture titled Future Belongs to Intelligent Operations. While cost-reduction continues to be an important trigger for operational transformation, driving business impact is the No. 1 driver for finance executives (see Exhibit 1). Our study findings illustrate that finance is emerging as a critical business partner to power organizational business imperatives including driving growth, entering new markets, launching new products, and improving customer experience. As the role of finance radically transforms, the expectations from third-party F&A services are evolving where cost-reduction alone does not meet client needs.

Exhibit 1: CFOs Are No Longer Focused on Just Cost Reduction

Sample set: 75 Finance Executives

Source: HfS Research, 2017

Labor Arbitrage Is Tiring Out and Providing Diminishing Incremental Returns

Labor arbitrage has been the backbone of the growth and value proposition for F&A services, but it is a one-time impact. Most large organizations with mature shared services or third-party provider relationships that have been running on an arbitrage-led model are now searching for the next “silver bullet” to find that next 30% to 40% of cost or value impact from managing their operations.

Also, arbitrage has proven to be one dimensional; consequently, the F&A market has struggled to drive significant value creation beyond cost reduction. Service providers figured out how to create a low-risk model to move as-is processes into a more affordable delivery model, where some modifications were made to standardize processes and procedures. But, once the new model has been operationalized, there is little or no incentive to make further changes without cannibalizing the revenue of the service provider. Simply reducing the number of offshore employees to manage work is not to their advantage when that is their sole source of revenue generation.

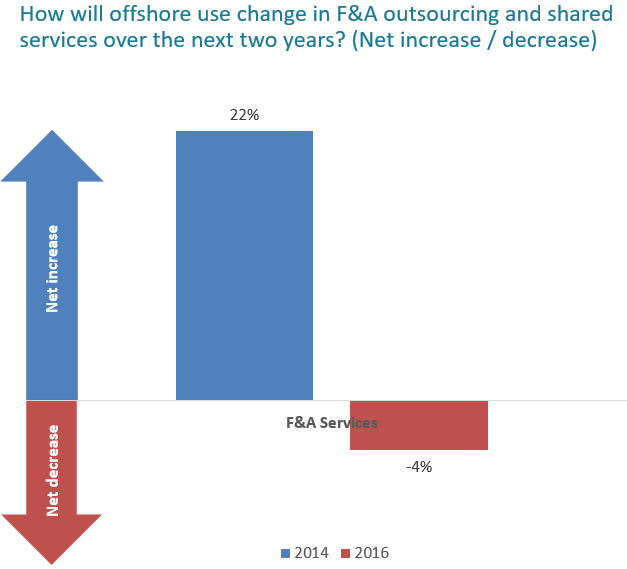

Moreover, the increasing protectionist sentiment in the west and the associated politics also do not augur well for this model, at least in the near term. Our joint study with KPMG titled State of Operations and Outsourcing 2017 predicts a net decrease of 4% in use of offshoring in F&A services over the next two years (see Exhibit 2).

Exhibit 2: Offshoring in F&A Is Slowing Down

Sample set: 454 Enterprise Executives

Source: HfS Research in conjunction with KPMG, “State of Operations and Outsourcing 2017.”

Slowing Market Growth and Commoditization Are Pushing the Need for Differentiation by Innovation

Growth in F&A Services has slowed down from about 15% YoY growth in the mid-2000s to about 5% YoY today. This is still healthy on a relative basis when you compare to other global service market segments such as IT Services, but not in absolute terms. The pipeline of new deals (especially large deals) for every leading service provider has dried up, and a large proportion of the current growth is based on expanding existing client relationships. A number of mature subsegments within F&A, such as payables and receivables, that account for a majority of the existing revenue base are also on the verge of commoditization. Tier-1 providers do not have a much different story to tell than Tier-2 and even Tier-3 providers when it comes to these mature subsegments. This does not bode well for the shareholders of these providers in the long term who are pushing them to innovate. Consequently, the inertia to linger with what worked for a better part of two decades is loosening up. At least the top leadership is becoming more transparent of pivoting their value propositions and trying something different.

Emerging Concepts and Technologies Promise Credible Value Creation Levers to Make a Real Difference

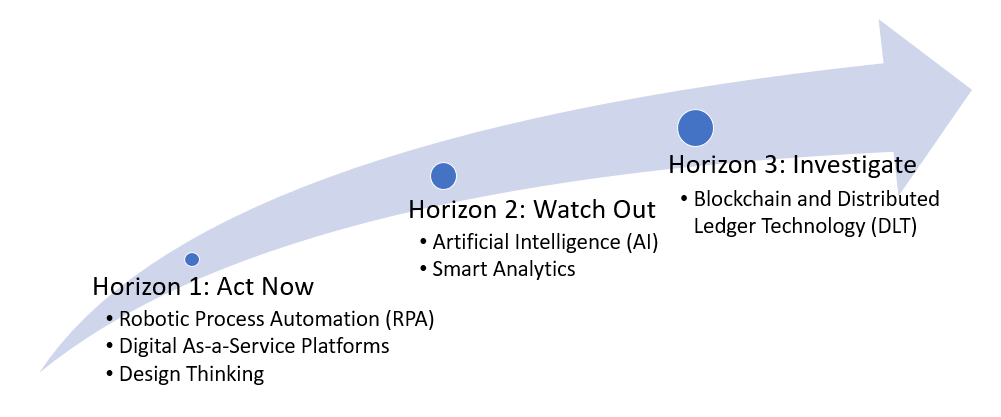

A range of new change agents is emerging that offers credible value to the tired value proposition of F&A services. We categorize them across three different time horizons (see Exhibit 3) based on their maturity to make an impact.

Exhibit 3: Emerging Value Creation Levers for F&A Services

Source: HfS Research, 2018

Horizon 1: Change agents that are starting to become mainstream. The rise of digital as-a-service platforms such as Concur, Tradeshift, Blackline, Trintech, and OmPrompt is changing how we think of traditional F&A value chains and associated service deliver as cloud-based solutions increasingly provide an end-game getting work done with vastly reduced needs for intensive labor and technology fixes. For example, Concur completely changed the market for travel and expense management. Most enterprises could simply standardize on a very effective SaaS app and vastly reduce all other people and technology investments to get the work done quickly, with the desired outcome (and data). As some of these solutions mature, they could, in a similar vein to Concur, dis-intermediate the traditional people-based services and completely automate parts of the procure-to-pay (P2P), order-to-cash (O2C), and record-to-report (R2R) processes. Design thinking being used to help finance executives become better partners within their businesses, to identify new areas of opportunity, and to shift the focus of work and engagement to the end consumer. The rise of robotic process automation (RPA) has also been nothing short of spectacular. All the 50 F&A BPS clients that we interviewed for the 2017 F&A Blueprint study were familiar with RPA and have some status to share, ranging from “discussion” of how and where to use it, working on a business case, or already using it either in-house or with service provider partners. Read here how Astra Zeneca and Cognizant leveraged RPA to drive speed, accuracy, and cost savings in the R2R.

Horizon 2: Change agents that are witnessing an explosion in pilots and PoCs. Elements of artificial intelligence (AI), especially machine learning (ML), natural language processing (NLP), and computer vision are starting to find their feet in F&A. For instance, Accenture is starting to use AI-based smart matching for real-time unapplied cash reconciliation. Intelligent invoicing solutions are emerging that help predict invoice accuracy and outcomes. We are also witnessing the rise of smart analytics through development of visualization tools with simulation capability. Examples include IBM’s use of ML algorithms to model how enterprise and market forces interact, using structured and unstructured and internal and external data sources to help optimize financial planning. The Triple-A Trifecta (intersection of RPA, AI, and smart analytics) is playing a major transformative role in the evolution of F&A Services.

Horizon 3: Change agents that are still nascent but promise tremendous value. Blockchain, or distributed ledger technology (DLT), is starting to offer a disruptive future vision for F&A: a world where recordkeeping is completely decentralized and where we might not even need the universal practice of double-entry book-keeping. For instance, Genpact is starting to investigate the use of blockchain-based smart contracts in O2C to eliminate billing errors and dramatically speed payments. Blockchain is still nascent but it is real, and leading organizations are investing and investigating as it could be a means to a sustainable competitive advantage that is very hard to find especially in the F&A services world.

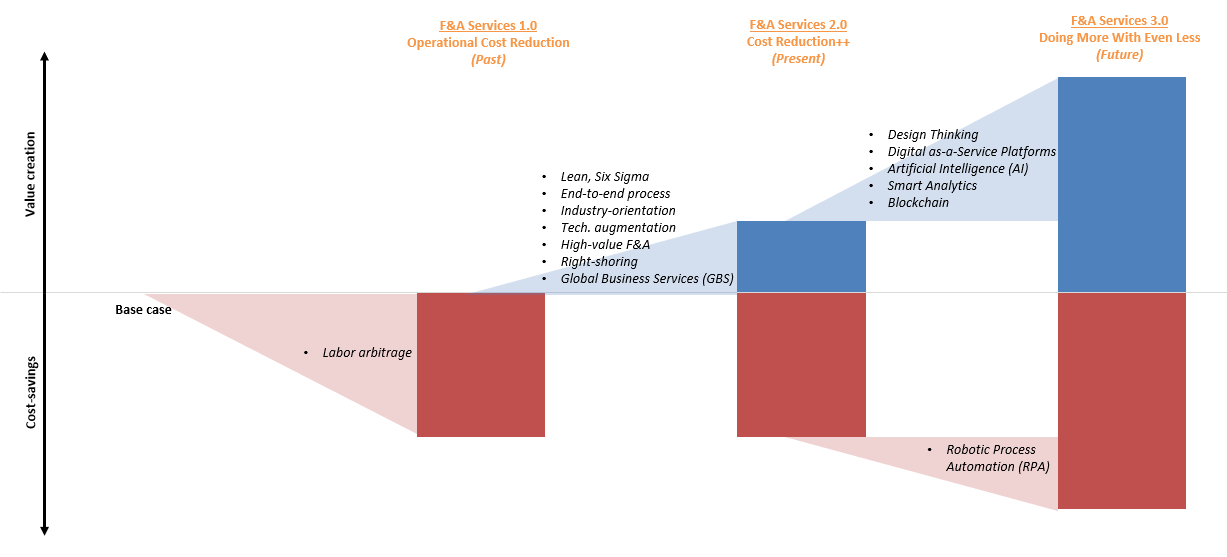

Introducing F&A 3.0—Doing More with Even Less

The factors described above lead us to believe that F&A Services is ready to move to a new S-curve that we call F&A 3.0—Doing more with even less. If we look at the history of F&A services, if we can see three distinct phases (see Exhibit 4).

Exhibit 4: Introducing F&A Services 3.0 – Doing More with Even Less

Source: HfS Research, 2018

The early 2000s were characterized by F&A 1.0. It was all about cost-reduction. The market exploded with the powerful labor-arbitrage opportunity where you could access the similar quality of talent at a significantly lower cost base. This was hugely attractive for the G2000, but soon everyone realized that labor arbitrage was a one-time benefit. As large contracts matured, both clients and service providers started to wonder what else could be done. So, the market entered the phase of F&A 2.0—the decade of incremental value beyond cost-reduction. During this phase, the market started to evolve beyond the one-dimensional offering around arbitrage. A number of service delivery improvements were introduced, such as:

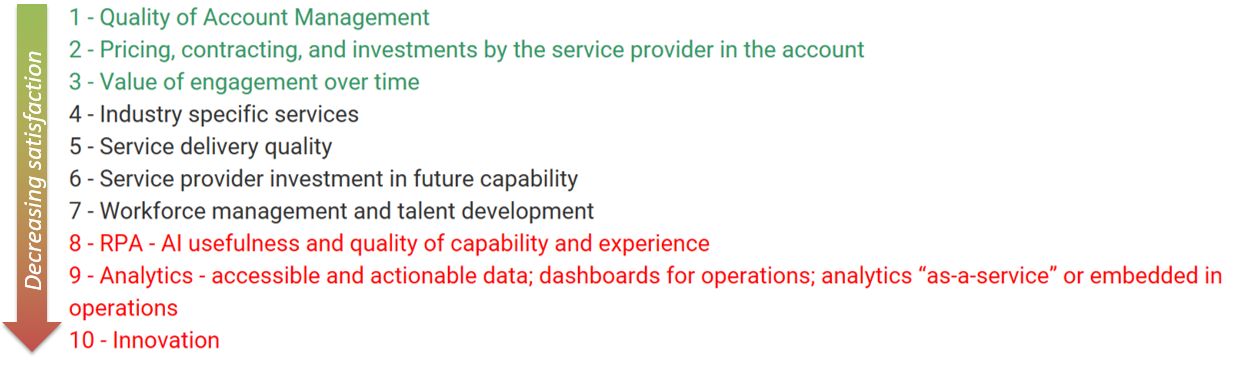

Despite the above efforts, F&A 2.0 is characterized by some paradoxical situations. Clients are generally satisfied, but many declare a lack of innovation as a pet peeve (see Exhibit 5). The watermelon effect is also widespread—the service levels are green but the heart of process transformation is still red! Business impact is promised, but relationships continue to be input-based, creating weird dynamics around aligning intent and incentives. In a nutshell, the biggest issue with F&A 2.0 is that the value proposition is still cost-reduction. All the other bells and whistles create some value, but it is only incremental.

Exhibit 5: Scoring Criteria Ranking Based on F&A Client Satisfaction (High to Low)

Sample: 50 F&A services client interviews

Source: HfS Research, 2017

The last two years have been characterized by the big, bold entry of new value creation levers (described above) in the F&A world. They promise to be the panacea for all that is wrong with F&A 2.0 by generating far more value with an even lower cost-base, thus paving the way for F&A 3.0 and doing even more with even less. The question is…How do we get to this promised land?

The Bottom Line: The Five Ps to Get to the Promised Land

Most providers (and even clients) are doing lip-service to the new value creation levers of F&A 3.0 because they are trying to force them into the existing model. People are used to the legacy way of procuring services via an FTE pricing model and are shifting to more effective ways of working that utilize technology-led services which threaten people’s status quo . However, as more and more firms are moving from labor-driven to technology-driven solutions, the pressure will increase on firms to move out of this legacy mindset.

In short, radical changes are required along the following five dimensions:

There are some promising technology innovations that can change the tired F&A narrative around cost-reduction, but technology alone will not solve the problem. The underlying F&A model must evolve to F&A 3.0.

This is the focus of our F&A research for 2018, so please reach out to us if you have an interesting story to tell!

[1] F&A BPO contracts over US $1 million in Total Contract Value (TCV) with a minimum of two core F&A processes in scope

Register now for immediate access of HFS' research, data and forward looking trends.

Get StartedIf you don't have an account, Register here |

With the exception of our Horizons reports, most of our research is available for free on our website. Sign up for a free account and start realizing the power of insights now.

Our premium subscription gives enterprise clients access to our complete library of proprietary research, direct access to our industry analysts, and other benefits.

Contact us at [email protected] for more information on premium access.